Jimmy Carter

"They claim to be super-patriots, but they would destroy every liberty guaranteed by the Constitution. They demand free enterprise, but are the spokesmen for monopoly and vested interest."

Henry Wallace, April 1944

"Our plutocracy, whether the hedge fund managers in Greenwich, Connecticut, or the Internet moguls in Palo Alto, now lives like the British did in colonial India: ruling the place but not of it."

Mike Lofgren, The Deep State

"Our future could be one in which continued tumult feeds the looting of the financial system, and we talk more and more about exactly how our oligarchs became bandits and how the economy just can’t seem to get into gear."

Simon Johnson, The Quiet Coup, May 2009

“The main problem in any democracy is that crowd-pleasers are generally brainless swine who can go out on a stage and whip their supporters into an orgiastic frenzy— then go back to the office and sell every one of the poor bastards down the tube for a nickel apiece.”

Hunter S. Thompson

"But there is a sort of 'Ok guys, you're mad, but how are you going to stop me' mentality at the top."

Robert Johnson, Audacious Oligarchy

Stocks moved lower again today, and went out near their lows.

Gold and silver were hit hard in the early trading, but managed to take back a good chun of their losses by the close.

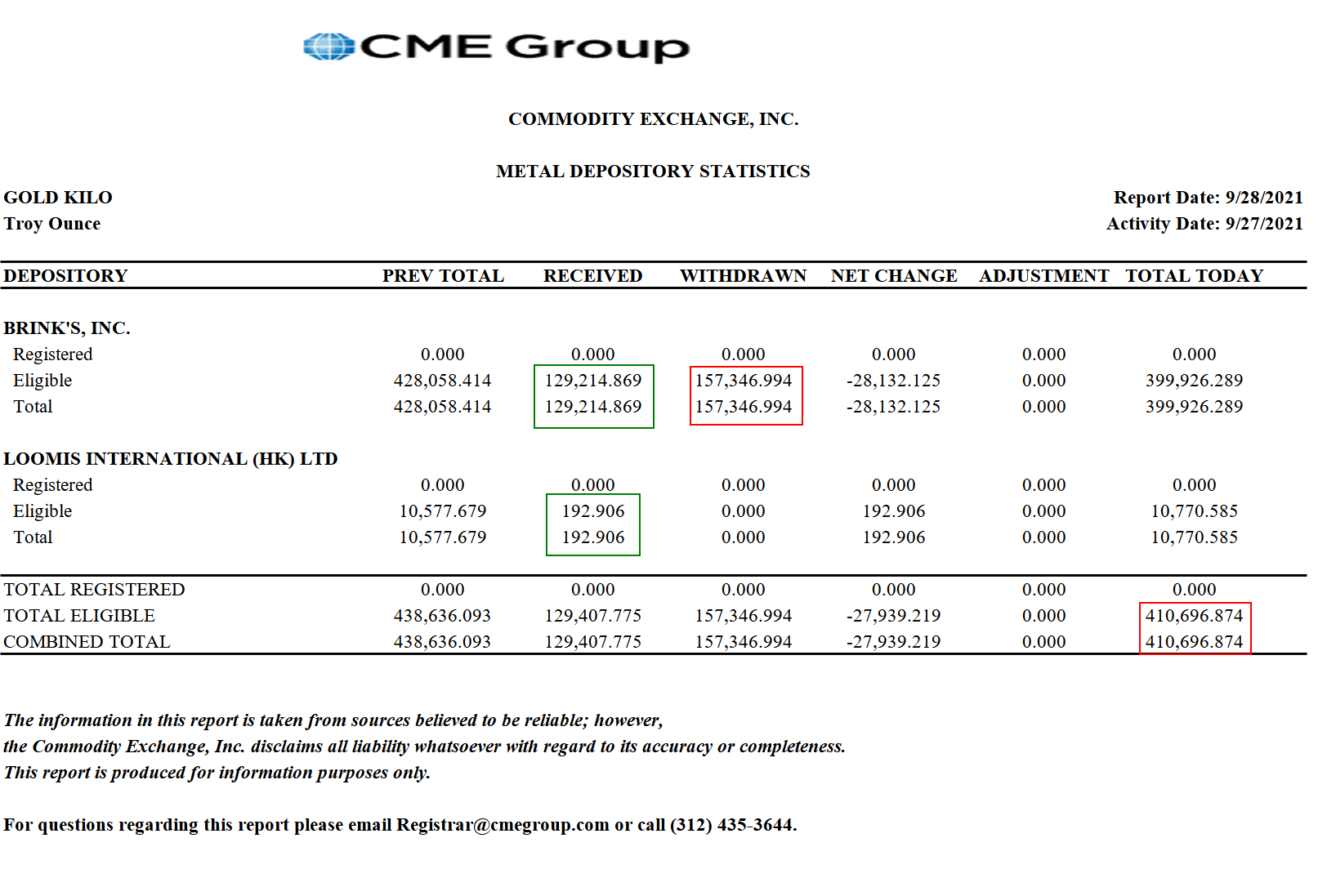

The physical kilo bar inventory in Hong Kong is getting rather low again.

Time to scour more physical out of the ETFs?

The Dollar rose on higher Treasury yields.

Congress engaged in the usual toothless showmanship in discussing the economy in testimony today.

I am sitting all in cash in my short term account now , although I did flip a few miners off the morning bloodbath.

Agnico-Eagle will be acquiring Kirkland Lake in a 'merger of equals (kind of).

The saga of the gambling Fed Presidents continues, and so we have another fine piece from the Martens today here.

Apparently a Fed President was actively placing short term million dollar directional bets, including the SP futures, during the crisis and the bailouts, with pockets full of insider information.

Must have been like shooting fish in a barrel.

And it was all legal so they say, and ethical. But details are being stonewalled.

All in all not extraordinary, in this attractive but deceitful world of routine abuse of honor, office, power, and the truth.

Have a pleasant evening.