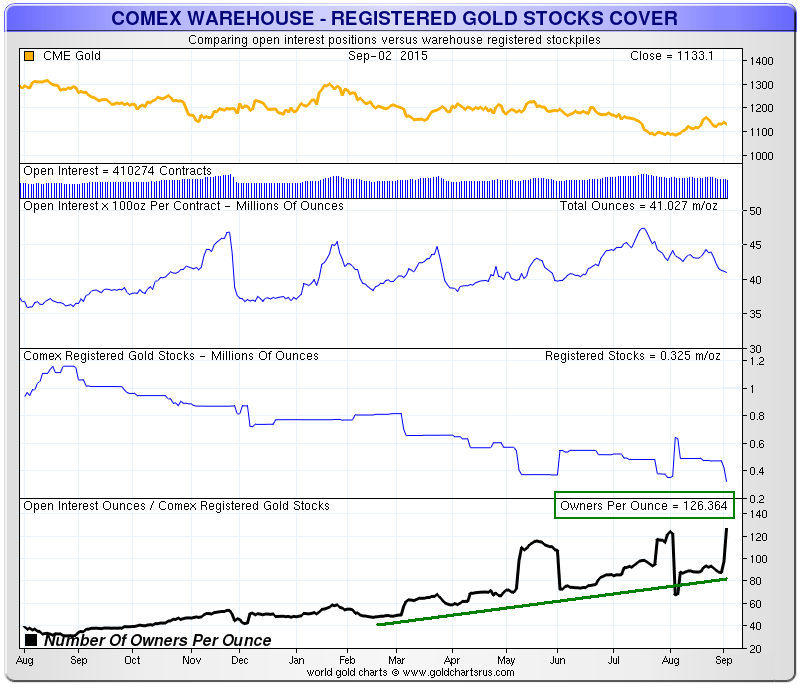

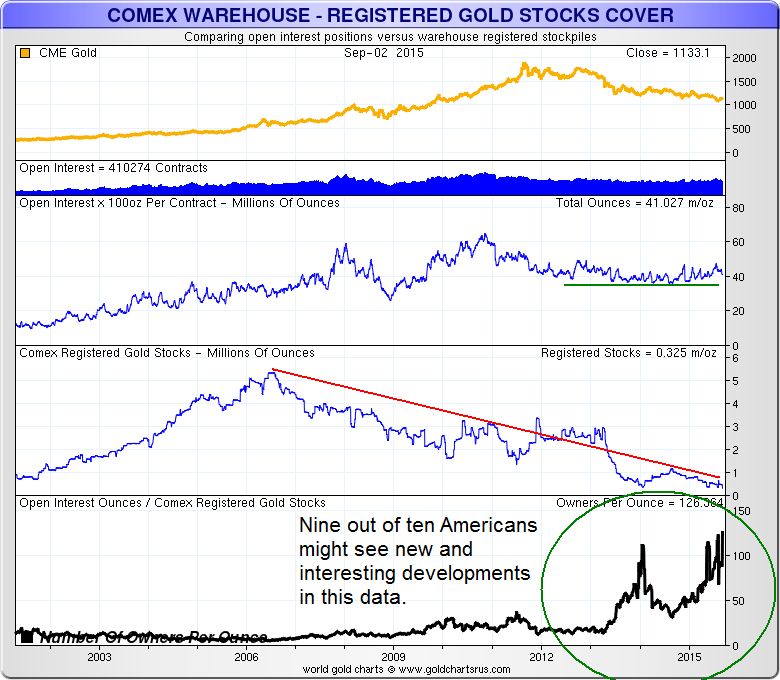

As someone asked, since hardly anyone is buying gold on the Comex and taking it out, why would be concerned about any inventory levels of deliverable gold?

Indeed, why be concerned about price if it is just all a part of an extended game of liar's poker between speculative interests?

It is almost just a betting parlor now, hence the title The Bucket Shop.

However, that does call into question its role in price discovery in the global trade around the world, much if not most of which is physical.

And that price discovery in London at the LBMA is asserted almost every day in one of the clearest patterns of price manipulation that one might even try to imagine.

As I have said on a number of occasions, I am not looking for a 'default' in NY. How can one default when forced settlements in cash can be easily accomodated at the Fed's window at any time?

No, the first cracks in the facade of the modern Gold Pool will appear in a key node of the physical market, most likely in London or Switzerland as fails to deliver. Perhaps even in Shanghai.

However, like the ebbing of the tide, a ready supply of gold for delivery will likely start disappearing from the shelves around the world at both the wholesale and retail level as the vortex of actual delivery in Asia consumes the ready supply at current prices. The cost of 'borrowing' gold will increase dramatically as the risk of a counterparty failure to return the bullion will intensify.

There will be a divergence between the price for immediate delivery of bullion and the paper price in the future, until the discrepancy becomes so obvious that there is a 'run' on the available short term physical supply, and real gold bullion goes to 'none offered' at any price close to the 'price discovery' of the paper markets. And then there will be a halt, a settling, and a reset.

If the source where you hold your bullion does not offer a guarantee of the bullion itself, rather than the 'value of the bullion' then chances are unacceptably high that you will be force settled in cash prior to a reset of the price substantially higher.

This is what happened in the US in 1933 when the official gold currency in circulation was recalled. People who had gold stored in the Banks had their monetary gold taken, a paper payment was received for it at the official price, and then afterwards the price of bullion in US dollars was set 41% higher. The increase in reserves was used to help prop up the insolvent banking sector.

Although such an action today is less likely since gold is no longer a monetary metal with a claim from the state, nevertheless such an action in a force majeure breakdown in the financial system whereby borrowed and 'shared' gold could not be returned at the current price faces a similar fate. This is how the failure of MF Global was recently resolved, and I can easily see the same rules applying for a market break in any leveraged system of ownership.

Related: Why the Federal Government Seized Gold In 1933