"If at the start this cancerous growth in the nation was not particularly noticeable, it was only because there were still enough forces at work that operated for the good, so that it was kept under control. As it grew larger, however, and finally in an ultimate spurt of growth attained ruling power, the tumor broke open, as it were, and infected the whole body." The White Rose, Munich 1942

"Und der Haifisch, der hat Zähne

und die trägt er im Gesicht

und Macheath, der hat ein Messer

doch das Messer sieht man nicht."

Berthold Brecht, Die Moritat von Mackie Messer, 1928

This is not a big surprise, since there were hints of this sort of drastic action in an obviously troubled bank since early October, but it is always newsworthy when one of The Global Banks feels troubled enough to eliminate its stock dividend for the foreseeable future.

Their goal is apparently to build up capital assets while cutting risky assets from the balance sheet and exiting certain markets.

And so a key global banking counterparty checks itself into rehab for an estimated two years.

Es ist eine Party!

Deutsche Bank scraps dividend for two years, sets financial goals

By Arno Schuetze, Frankfurt

Oct 28 Deutsche Bank is scrapping this year's and next year's dividends as new Chief Executive John Cryan overhauls Germany's biggest bank to restore growth and put past scandals behind it.

The lender said on Wednesday it was targeting a capital ratio of at least 12.5 percent from the end of 2018.

It is also now targeting a leverage ratio of at least 4.5 percent at the end of 2018 and at least 5.0 percent at the end of 2020 and a return on tangible equity of more than 10 percent by 2018.

"The plan is based on the elimination of the Deutsche Bank common share dividend for the fiscal years 2015 and 2016. The management board expects to recommend the payment of common share dividends commencing from fiscal year 2017 at a competitive payout ratio," Deutsche Bank said. (Reporting by Arno Schuetze; Editing by Georgina Prodhan)

The US dollar caught a bid on that 'hawkish' Fed statement, sending a number of commodities including the precious metals gold and silver lower.

Gold and silver looked like a pump and dump with the early rally higher which smelled like a set up.

About the last thing that the real economy needs is a truly stronger dollar. And I do not believe that most of the FOMC members would wish for that, but with the rest of the developed world seeming to ease, and some aggressively so, it is a difficult position for them to manage with credibility.

The primary beneficiaries of a strong dollar policy are the big holders of dollars who can use them to buy up attractive foreign assets more cheaply, and the holders of dollar denominated debt.

It be roughly said to be a policy that sets Main Street versus Wall Street, although the courtiers of the moneyed interests will proclaim the benefits of even more cheaper imports. Too bad the public has little spare income with which to purchase them. But that is a tradeoff that in the short term also benefits Big Money with little domestic wage pressure as more people have less employment prospects.

It is hard to say what the Fed will do for sure, and I doubt that even they know what they will do. Today was designed to dampen the asset bubble a bit, and to once again caution the market that a rate increase may be coming, provided the data gives the Fed cover to do so without becoming the bag-holder for another recession going into an exceptionally political season.

It is much too early to tell, but judging from the SP stock futures, the Street is not necessarily buying what the Fed is selling, at least for today.

The Fed would like to raise interest rates, and seeks to justify that decision whether the data indicates that it does or not. The data will be massaged, and if sufficiently so, the Fed will move when it wills. They would like to do so for policy purposes, and do not wish to do so close to the Presidential elections so that their actions will not be labeled as politically partisan.

For immediate release

Information received since the Federal Open Market Committee met in JulySeptembersuggests that economic activity ishas been expanding at a moderate pace. Household spending and business fixed investment have been increasing moderatelyat solid rates in recent months, and the housing sector has improved further; however, net exports have been soft. The labor market continued to improve, with solid job gains and declining unemployment. On balancepace of job gains slowed and the unemployment rate held steady. Nonetheless, labor market indicators, on balance, show that underutilization of labor resources has diminished since early this year. Inflation has continued to run below the Committee's longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation moved slightlylower; survey-based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term. Nonetheless, tThe Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate. The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring global economic and financialdevelopments abroad. Inflation is anticipated to remain near its recent low level in the near term but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintainwhether it will be appropriate to raise thise target range at its next meeting, the Committee will assess progress--both realized and expected--toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee's holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams. Voting against the action was Jeffrey M. Lacker, who preferred to raise the target range for the federal funds rate by 25 basis points at this meeting.

'Modern capitalism is masterful at producing services people don't need and in large part probably don't want. It is brilliant at convincing people that they do need and want them. But it has difficulty turning itself to the production of those services which people really do need.

Not only that, it often spends an enormous amount of time and effort convincing people that those services are either unrealistic, marginal or counterproductive.'

John Ralston Saul

Saul is referring not to capitalism but to Capitalism, that is, an economic system that rises from its proper role as a supporting tool or method to being the arbiter of end issues superior to the intents of public policy. Capitalism begins to dictate outcomes, and policy goals become not its director, but its servant.

The machinery of the market takes precedent over the well being of mankind. It creates winners and losers, and panders to the selfish interests of its moneyed pharisees and their corporate acolytes.

This divergences between myth and reality has caused the modern landscape to become a convoluted wasteland of profane gods and deep wells of subjectivity. The preoccupation becomes form rather than the substance of results.

No where is this more visible than in modern economics, with its worship of willfulness in power and the delphic marketplace. They are as devoted to their dogma as any fundamentalist, seeking to hide their ideological bent behind a wall of jargon, slogans, and false proofs.

Something is worth what it is because we say it is, and we have the power to make that stick. And there can be no disagreement or discussion on this subject. Because theirs is a received religion.

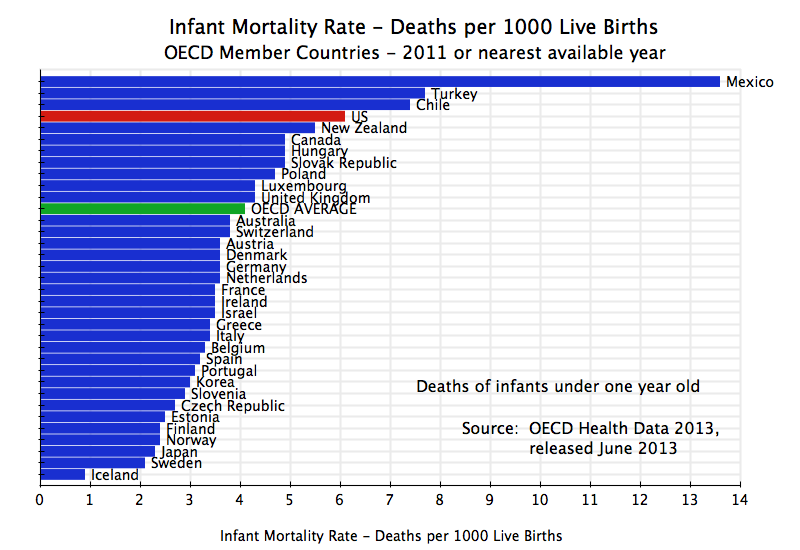

One only has to consider that most Americans are convinced that their medical system is the best in the world, a model of capitalistic success, when even a cursory consideration of the facts shows that it excels only in overall expense, and grossly underperforms in first things of public policy like infant mortality.

It may provide very good results, but selectively for its own adherents. Those overall results are strictly rationed, and distributed by privilege and access to money.

The marketplace, in the very literal sense of the word, decides who will suffer and who will thrive, who may live, and who will die.

And too often the opposition to the Neoliberal free-marketeers become less a reform and more like a rival religion. This is no reformation, but a substitution of other top down ideologies. Communism is a fairly good example of a rival utopian ideology. Almost any system taken to an extreme for its own sake can fit the bill.

I can see many well-intentioned reformers falling into a dogma of their own. The key difference is that the focus shifts from the ends, the reform and remediation of wrongs and public policy issues to the dictates of a new utopian system with its own set of jargon, based on top down commandments, to be worshiped and embraced without question. And woe to those who dare to raise any objections, for they will be shunned and attacked.

Even while they are collapsing in practice, and badly and even tragically so, there can be no deviation from their solutions which are prescribed, top down, by ideology. This is the most important distinction, that in an ideology the results are subordinate to the top down principles followed.

The US has the most expensive medical system in the world by most measures. And yet it is producing rather inferior results in certain key categories. Look at all these children who are suffering and dying. And the pharisees of Capitalism will say, oh well you see, these are the offspring of economic infidels, collateral damage to the beauty and purity of the system. They have brought it on themselves because of their lack of zeal in pursuing self interest. They are pre-destined to be poor and to suffer because they do not have our superior qualities of the exceptional, the elect.

And when the dispossessed start seizing the moment and the initiative, the privilged react with anger and repression. They lose the ability to deal with the problems that they themselves have created. They are caught in a credibility trap. They cannot deny the perfection of the system without denying their own god. It is a religion in character, but a religion grossly disproportionate to its use, out of place. Like other abuses of religion past, they make a profane idol which is used to justify their own worldly wishes rather than effect a change and constrain their selfish behaviour to some larger objective.

This is the difficulty that economic agnostics and freethinkers have with the schools, like globalism, the socially atheistic libertarians, the Austerians, the Stimulati, and assorted modern theories that tend to reason from the top down and prescribe the imposition of a comprehensive system to set policy priorities, rather than setting objectives to be achieved through some set of largely political constraints, within a social contract of one form or another.

But they are not to be dictated like the end result of an equation from the oracle of the marketplace. And that is the very crux of the issue and the heart of our problems. We have lost out way.

Let us pray for those whose hearts are hardened against His grace and loving kindness by greed, fear, and pride, and the seductive illusion and crushing isolation of evil.

We pray that we all may experience the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness. And in so doing, may we obtain abundant life, and with it the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.