Silk road total demand, including the growth of official reserves and commercial imports, has risen from 1,493 tonnes in the year 2000 to over 27,087 tonnes in 2015.

The greatest increase has been since the global financial crisis in 2008 with an astonishing increase of 450% over the total amounts accumulated until then.

As you may recall, gold was ending its long bear market with a price bottom and a long climb higher shortly after the currency crises of Asia and Russia in the 1990's.

Silk Road demand has easily exceeded total global mine production for the last two years. And quite Therefore, in addition to mining, other sources of gold have had to be found. This may include scrap, and gold held by other entities.

Has this surge in gold demand been an uniquely Chinese government phenomenon? Hardly.

In the second chart I show all the gold reserve increases for China AND Russia from the year 2000. They account for only about 11.4% of the growth in gold demand from the 'Silk Road' countries.

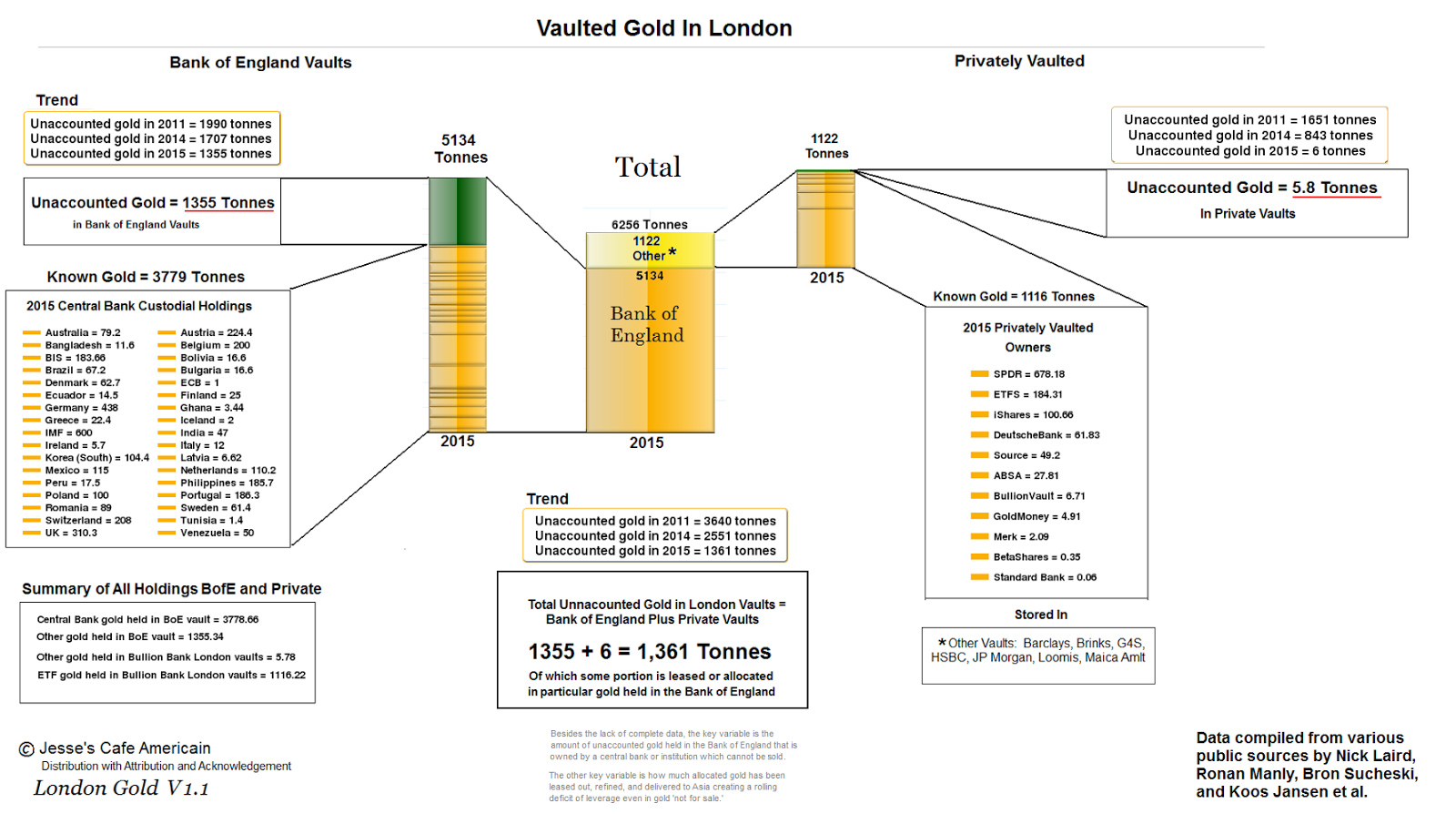

It is interesting to match this with the steady declines in Western gold vaults and the increased leverage in gold trading, what some call 'synthetic gold,' that became apparent in 2013.

I show that in the third chart vis a vis the Comex, and the fourth chart for the London Vaults.

The fifth chart compares the relative physical deliveries on the Shanghai Exchange and the NY Comex.

I am not trying to persuade or convince anyone, or argue with anyone, and certainly not sell anything.

Here are the facts as I have been able to discover them, and I cannot control what people may choose to think or not to think about them.

The data suggests that the volume of gold increased dramatically in 2013, when measures seem to have been taken to dampen the large increase in price up to the $1900 level, through rather clumsily determined selling programs in quiet hours.

This increased flow of bullion may be the result of Gresham's Law, which states that 'when a government overvalues one type of money and undervalues another, the undervalued money will leave the country or disappear from circulation into hoards, while the overvalued money will flood into circulation.'

The data suggests that gold is very underpriced in US dollars because of an effort to make the dollar appear to be strong and gold to be disreputable as an alternative store of wealth. Why should gold be more favored than cash money in their own currencies, which central bankers would also like to eliminate to smooth the way for further policy blundering and experimentation.

They are hardly without better alternatives to this. Except of course for their pride, and insular group thinking, and of course the credibility trap that does not allow for frank discussions of what the problems really are and how we might move along. But alas, that is not favored by The Banks and the moneyed interests. And so the very serious people are loathe to even raise the subject of genuine reform in a serious conversation, except in some mockery of a charade.

And the Congress is no better. The Congress may not know when it is talking nonsense about the economic situation, but the financiers, the Banks, and their hired hands do, but don't care.

Whatever else someone may say about this, it is apparent by any examination of the figures that gold bullion is flowing from West to East, and in some fairly consequential and increasing volumes.

The Silk Road has added over 25,000 tonnes of gold in the last fifteen years. The gold miners are hardly in a position to increase production and search for new supply. A gold mine takes four or more years to bring into production.

According to Nick Laird's figures, monthly global mining production is about 260 tonnes, and monthly demand is about 357 tonnes. I have included a list of the top gold producing countries in chart six.

Where will the supply for the Silk Road demand come from over the next five years, as it continues to grow faster than mining and even scrap production?

These two charts are from Nick Laird at goldchartsrus.com, with my annotations.