Today was more of the same, with an easy hit on price during the NY trade.

There was some movement into the customer storage (eligible) category on Friday of about 31,000 ounces.

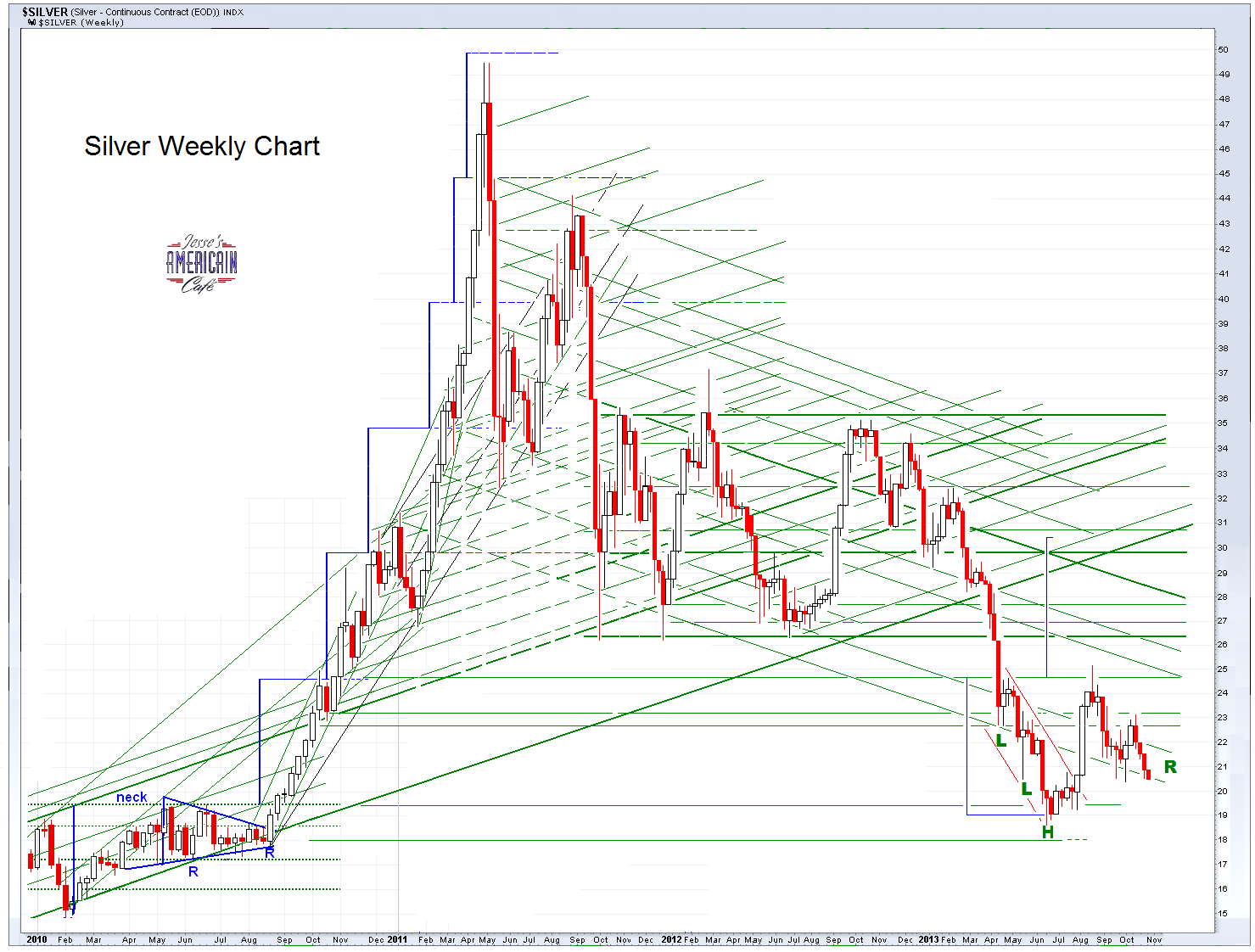

Have a pleasant evening.

"You are the very cause of your ignorance, yourselves. You put away the light, yourselves; you first pluck out both your own eyes, yourselves; and after that other men’s too, so that the blind may lead the blind, until you both fall into the pit.”

Thomas More, The Sadness of Christ (Gethsemane), Tower of London, 1535

“I recently made fairly detailed presentations to two Asian central banks... I was struck by the fact that one of the central bankers did volunteer to me that most central bankers are aware of the fractional reserve nature of the Western gold banking system, and its vulnerabilities.

He clearly acknowledged their understanding that gold does not back all of the claims to gold that are floating around the world financial system, particularly when it comes to the West. You would probably never get a central banker to acknowledge that publicly, but that is precisely what he said to me off the record.”

Chris Powell, KWN

“Let us not, in the pride of our superior knowledge, turn with contempt from the follies of our predecessors. The study of the errors into which great minds have fallen in the pursuit of truth can never be uninstructive...

Hitherto no difficulty had been experienced by any class in procuring specie for their wants. But this system could not long be carried on without causing a scarcity. The voice of complaint was heard on every side, and inquiries being instituted, the cause was soon discovered. The council debated long on the remedies to be taken, and [John] Law, being called on for his advice, was of the opinion, that an edict should be published, depreciating the value of coin five per cent below that of paper.

The edict was published accordingly; but, failing of its intended effect, was followed by another, in which the depreciation was increased to ten per cent. The payments of the bank were at the same time restricted to one hundred livres in gold, and ten in silver. All these measures were nugatory [pointless] to restore confidence in the paper, though the restriction of cash payments within limits so extremely narrow kept up the credit of the Bank.

In February 1720 an edict was published, which, instead of restoring the credit of the paper, as was intended, destroyed it irrecoverably, and drove the country to the very brink of revolution...”

Charles MacKay, Extraordinary Popular Delusions and The Madness of Crowds

"Bright star, would I were steadfast as thou art..."

John Keats

"So you are lean and mean and resourceful, and you continue to walk on the edge of the precipice, because over the years you have become fascinated by how close you can walk without losing your balance."

Richard Nixon