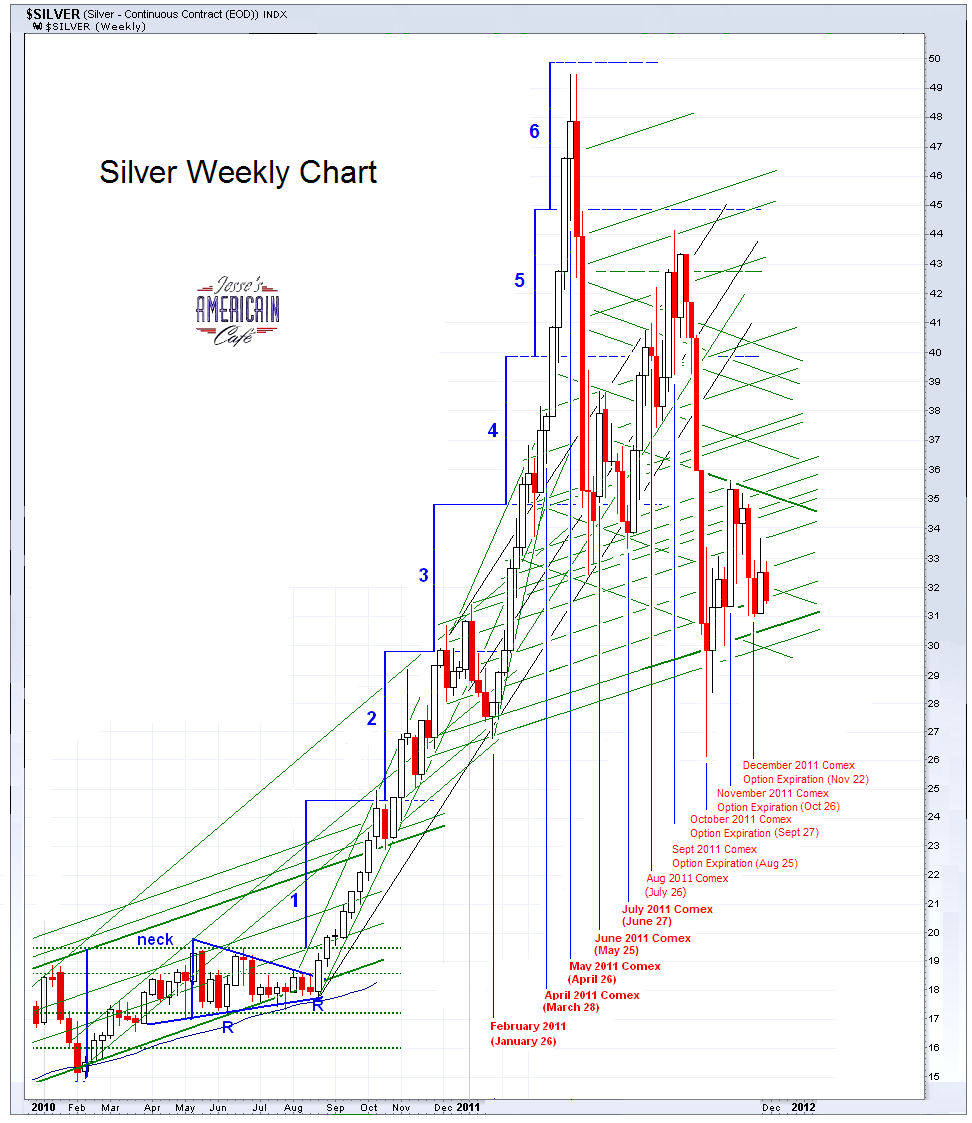

This felt like a 'drift higher' day more than anything else.

The VIX fell.

Watch for a possible SP downgrade of Eurozone debt next week.

"They will not see. They will not listen. Blindly they follow their seducers into ruin."

White Rose, Fifth Leaflet, January 1943

Fraus est celare fraudemAnd as sacred as a former US Senator may be, if one of the TBTF Banks is involved as the circumstances seem to indicate, this is the holy of holies in the Pax Americana.

“Poverty wants, but greed wants everything, and more.”Customers run for safety, from one place to another, not sure what or whom they can trust. One thing they may do is to stop trading on margin, and shut down their margin accounts, going to strictly cash investing wherever possible. And for your long term investments, you can take possession of the physical shares and keep them in a safer place than an account statement from any of the TBTF banks and hyper-hypothecating commodity brokers.

Jon Corzine Dodges the Fraud Question

By Janet Tavakoli

12/9/11 07:56 AM ET

It's as if Jon Corzine's PR machine is in top spin mode. You'll recall Jon Corzine is the former head of Goldman Sachs and former CEO of MF Global that appeared in front of Congress yesterday to answer questions about an estimated $600 million to $1.2 billion in missing money from the segregated accounts of customers of MF Global.

Yesterday and today, I heard confusion about whether or not MF Global's diverting customer funds was allowable and the possibility that customers will eventually get the money back.

Let me be clear. The diverting of customer funds from segregated accounts is not legal or allowable, and even if the money is later "found" it is fraud...

"Finding" Money Doesn't Excuse Fraud

Let me address the implication of the potential to "find" the money. The money may indeed be "found." If the bonds mature and pay off one hundred cents on the dollar, it may be possible to claw back money from MF Global's trading partners without much of a fight. Otherwise there may be a legal battle for money that as creditors of MF Global, they were never entitled to in the first place.

The rights of MF Global's customers are superior to the claims of these creditors. But eventually replacing the filched funds is not the same as restitution, since reputations and businesses have already been ruined. Damage has also been done to the trust in the global futures market and Futures Commission Merchants (FCMS).

Never Allowable to Filch Customers' Funds

The key issue is that it is never allowable to divert money from customers' segregated accounts. CFTC Commissioner Jill E. Sommers did a good job of stating that in her testimony yesterday. Moreover, if any trades mimicking Corzine's were done on behalf of the tiny minority of customer accounts that could engage in this trade, the trades would have to be segregated and credits or losses would show up in the relevant customers' accounts.

That still doesn't explain the missing funds in most customer accounts. Most customer accounts would not even be eligible for the "Corzine sovereign bond trade." Why is that? Here's an excerpt from Sommers' testimony: "Under Section 4d of the CEA, customer segregated funds may be invested in: general obligations of a sovereign nation (to the extent the FCM holds customer funds denominated in that sovereign nation's currency)." Most MF Global customers now missing money did not hold foreign currency accounts.

Pushing the idea that this trade was "allowable" for some customer is a distraction trick to avoid the question of whether MF Global impermissibly wired money from customers' accounts to satisfy margin calls for its own trades. Wire fraud is a federal crime.

At Issue is Massive Fraud

The issue under investigation is what appears to be a bold and massive fraud, and Jon Corzine offered no alternative explanation, in fact it seems he cannot explain anything about the firm he ran to anyone's satisfaction.

Jon Corzine may not know where the money is right now, but as head of MF Global, he knew or should have known his trades needed collateral and that customers' money went missing to satisfy part of that need. If it is proved that fraud occurred -- and money missing this long is a very suspicious sign -- it's not plausible to me that Jon Corzine was unaware it was happening at MF Global.

It seems Jon Corzine would have Congress believe he's hopelessly incompetent, because it is better to have them believe that than the business for which he was responsible was breathtakingly wrong.

Gold is cheap relative to the idea that you could have a life’s fortune on a statement from a clearing agent and then find out that you don’t have a penny left anywhere. Which should you have had, physical gold or that clearing house statement? Gold is cheap because of the condition of other things.

Jim Sinclair

"A good parson once said that where mystery begins, religion ends. Cannot I say, as truly at least,

of human laws, that where mystery begins, justice ends?"

Edmund Burke

"Jill Sommers did a great job with her testimony leaving no room for doubt that 1) the cases in which investment in foreign sovereign debt for customers’ own accounts are limited to the extent of their foreign exchange deposits (so a small minority of accounts) and 2) it is never allowable to transfer money out of the customer accounts to commingle with MF’s investments."

"When a broker-dealer is also a registered FCM, as MF Global was, there is one dually-registered entity and the entire entity gets placed into liquidation. Because there is one entity, it is not possible to initiate a SIPA liquidation of the broker-dealer, and a separate bankruptcy proceeding for the FCM. It is important to note, however, that when a dually-registered BD/FCM is placed into a SIPA liquidation proceeding, the relevant provisions and protections of the Bankruptcy Code, the Commodity Exchange Act (“CEA”), and the Commission’s regulations apply to customer commodity accounts just as they would if the entity were solely an FCM and in a non-SIPA bankruptcy proceeding.

An obvious point to make is that if a firm is involved in a bankruptcy proceeding, something must have gone very wrong. Bankruptcy proceedings can be very complicated and at times, messy. This can be magnified when the bankruptcy is among the largest in history and there are serious questions about the location of customer funds. The Commission is no stranger to FCM bankruptcies. Lehman Brothers and Refco are the two most recent FCM bankruptcies. While the Lehman Brothers bankruptcy was monumental in scale, and the Refco bankruptcy involved serious fraud at the parent company, commodity customers did not lose their money at either firm. In both instances, commodity customer accounts were wholly intact, that is, they contained all open positions and all associated segregated collateral. That being the case, customer accounts were promptly transferred to healthy FCMs, with the commodity customers having no further involvement in the bankruptcy proceeding. Unfortunately that is not what happened at MF Global because customer accounts were not intact.

In FCM bankruptcies, commodity customers have, pursuant to Section 766(h) of the Bankruptcy Code, priority in customer property. This includes, without limitation, segregated property, property that was illegally removed from segregation and is still within the debtor’s estate, and property that was illegally removed from segregation and is no longer within in the debtor’s estate, but is clawed-back into the debtor’s estate by the Trustee. If the customer property as I just described is insufficient to satisfy in full all the claims of customers, Part 190 of the Commission’s regulations allow other property of the debtor’s estate to be classified as customer property to make up any shortfall. A parent or affiliated entity, however, generally would not be a “debtor” unless customer funds could be traced to that entity.

Within the first weeks of the MF Global bankruptcy, the Trustee for the BD/FCM had, with the encouragement and assistance of the CFTC, transferred nearly all positions of customers trading on U.S. commodity futures markets, and transferred approximately $2 billion of customer property. On November 29th, the Trustee moved to transfer an additional $2.1 billion back to customers, to be used to “top up” all commodity customers to at least two-thirds of their account values as reflected on the books and records of MF Global, Inc. The Bankruptcy Court will hear the motion on December 9th. If the Court grants the motion we expect the transfer may be complete in two to four weeks, given the Trustee’s estimate of the timeframe within which he can complete the administrative functions necessary to effectuate the transfer. These transfers demonstrate that commodity customers are indeed receiving the highest priority in claims to customer property. We understand that more must be done...

While an FCM is permitted to invest customer funds, it is important to note that if an FCM does so, the value of the customer segregated account must remain intact at all times. In other words, when an FCM invests customer funds, that actual investment, or collateral equal in value to the investment, must remain in the customer segregated account at all times. If customer funds are transferred out of the segregated account to be invested by the FCM, the FCM must make a simultaneous transfer of assets into the segregated account. An FCM cannot take money out of a segregated account, invest it, and then return the money to the segregated account at some later time."

"I will be as harsh as truth, and as uncompromising as justice. On this subject, I do not wish to think, or speak, or write, with moderation. Tell a man whose house is on fire, to give a moderate alarm; tell him to moderately rescue his wife from the hand of the ravisher; tell the mother to gradually extricate her babe from the fire into which it has fallen; but urge me not to use moderation in a cause like the present. I am in earnest - I will not equivocate - I will not excuse - I will not retreat a single inch - and I will be heard."

William Lloyd Garrison

"Recognizing the enormous impact on many peoples’ lives resulting from the events surrounding the MF Global bankruptcy, I appear at today’s hearing with great sadness. My sadness, of course, pales in comparison to the losses and hardships that customers, employees and investors have suffered as a result of MF Global’s bankruptcy. Their plight weighs on my mind every day – every hour. And, as the chief executive officer of MF Global at the time of its bankruptcy, I apologize to all those affected."I am a former US Senator and am therefore untouchable. So, after the Congressmen are done uselessly yelling at me for the benefit of their constituents, can I go home with my money?

"With weak collateral rules and a level of leverage that would make Archimedes tremble, firms have been piling into re-hypothecation activity with startling abandon. A review of filings reveals a staggering level of activity in what may be the world’s largest ever credit bubble.I was slow to use this Thomson Reuters piece because some of the things it seems to suggest in the beginning do not quite ring true. As Jill Sommers, the head investigator from the CFTC into MF Global made very clear yesterday, and as Janet Tavakoli encapsulates so well,

Engaging in hyper-hypothecation have been Goldman Sachs ($28.17 billion re-hypothecated in 2011), Canadian Imperial Bank of Commerce (re-pledged $72 billion in client assets), Royal Bank of Canada (re-pledged $53.8 billion of $126.7 billion available for re-pledging), Oppenheimer Holdings ($15.3 million), Credit Suisse (CHF 332 billion), Knight Capital Group ($1.17 billion),Interactive Brokers ($14.5 billion), Wells Fargo ($19.6 billion), JP Morgan($546.2 billion) and Morgan Stanley ($410 billion).

Nor is lending confined to between banks. Intra-bank re-hypothecation is also possible as evidenced by filings from Wells Fargo. According to disclosures from Wachovia Preferred Funding Corp, its parent, Wells Fargo, acts as collateral custodian and has the right to re-hypothecate and use around $170 million of assets posted as collateral.

The volume and level of re-hypothecation suggests a frightening alternative hypothesis for the current liquidity crisis being experienced by banks and for why regulators around the world decided to step in to prop up the markets recently. To date, reports have been focused on how Eurozone default concerns were provoking fear in the markets and causing liquidity to dry up.

Most have been focused on how a Eurozone default would result in huge losses in Eurozone bonds being felt across the world’s banks. However, re-hypothecation suggests an even greater fear. Considering that re-hypothecation may have increased the financial footprint of Eurozone bonds by at least four fold then a Eurozone sovereign default could be apocalyptic.

U.S. banks direct holding of sovereign debt is hardly negligible. According to the Bank for International Settlements (BIS), U.S. banks hold $181 billion in the sovereign debt of Greece, Ireland, Italy, Portugal and Spain. If we factor in off-balance sheet transactions such as re-hypothecations and repos, then the picture becomes frightening."

"Jill Sommers did a great job with her testimony leaving no room for doubt that 1) the cases in which investment in foreign sovereign debt for customers’ own accounts are limited to the extent of their foreign exchange deposits (so a small minority of accounts) and 2) it is never allowable to transfer money out of the customer accounts to commingle with MF’s investments."And as Commissioner Sommers said in her testimony today,

"In FCM bankruptcies, commodity customers have, pursuant to Section 766(h) of the Bankruptcy Code, priority in customer property. This includes, without limitation, segregated property, property that was illegally removed from segregation and is still within the debtor’s estate, and property that was illegally removed from segregation and is no longer within in the debtor’s estate, but is clawed-back into the debtor’s estate by the Trustee. If the customer property as I just described is insufficient to satisfy in full all the claims of customers, Part 190 of the Commission’s regulations allow other property of the debtor’s estate to be classified as customer property to make up any shortfall. A parent or affiliated entity, however, generally would not be a “debtor” unless customer funds could be traced to that entity."