If there is a stock crash, all asset classes will suffer liquidation for a period of time, except perhaps for treasuries, and chart formations will get tossed out the window. But at some time after the primary crash, the currency is devalued, and bonds are taken out and beaten.

Crashes are low probability events, but need to be accounted for in your planning. I do that by hedging my positions with some shorts, and relying more on bullion than stocks during riskier periods.

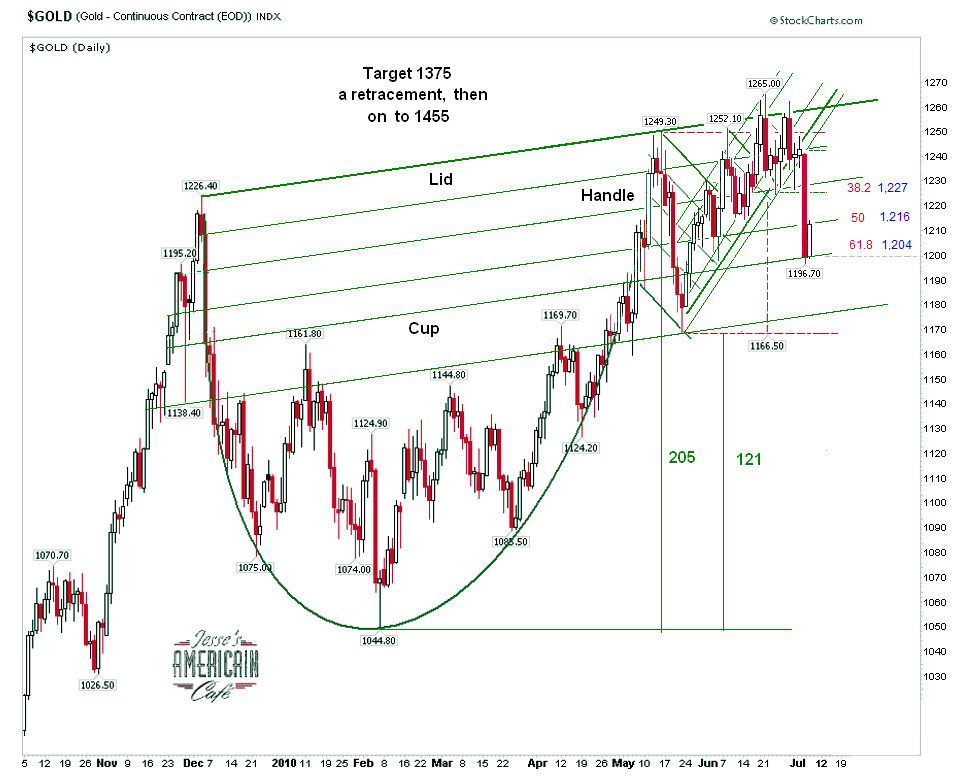

On every pullback, the permabears come out of their caves and do their dance. That is just how it goes in a bull market.

If there is a crash, gold would find significant support around the 1000 mark, as buyers who missed the last leg up will rush in at this chance to buy. However, most of the permabears will NOT buy, since they are now stuck in a cycle of always waiting for THE bottom and bragging rights to a low. If they did not buy in the last plunge, they will never buy.

Things are changing. The world has lost confidence in the dollar reserve currency regime thanks to the serial abuses of Greenspan and Bernanke, and the abusive use of power by the current and previous Administrations. Things that have been in place on a global scale for fifty years change slowly. But that change is happening, and that is what you are seeing in the chart below.

As I noted last year, the SDR recalibration would be a focal point for the BRIC's to attempt to dislodge the dollar hegemony. The US and UK are fighting it with their bag of financial tricks. This is why Obama refused to touch the gangs of NY in his so called reforms. The big banks and hedge funds are as much an instrument of US foreign policy as is its military. Europe is learning this lesson, and it is taking measures to protect itself. This is part of the long range forecast, and is known as the 'currency wars.'

Currency Wars and Coups d'Etat

I will not be surprised at all if in the next ten years certain US and UK officials, and those who claim that they were only acting on their government's behalf, merely following orders, become fugitives from justice. But there may be some 'suicides' and tragic airplane accidents among the weaker links first if things get dodgy. And of course the usual scapegoats, fall guys and patsies.

This is not something involving the United States alone. Iceland is a microcosm of what happened as the systems were overtaken by corruption and greed, and is running ahead of the larger countries because of its smaller scale. The German banks are deep into it. The UK is more likely to follow Iceland's path before the US, and may serve as a bellwether. The neo-con David Cameron is certainly no man of the people, and is likely to make the working classes in Britain howl before he is done with them. England, what were you thinking?

The financial crisis is being used to cover a subversion of justice, what history may some day regard as essentially a financial coup d'etat, wherein a small group of men, many of whom have their roots and connections with a handful of universities, institutions, and investment banks, essentially seized control of the banking system, and by extension the economy, co-opting the media and the political process, and have been bending it increasingly to their will ever since.

What will most likely trip them up is not so much the acts of fraud and insider dealing themselves, but the overreaching, the cover ups, the subornation of perjury to the Congress, and as always, obstruction of justice. But before we reach that point, I would not discount a more overt attempt to seize or direct the power of government through some staged event, some false flag.. But first and foremost they will use the softer means of deception, persuasion, intimidation, and of course the ridicule of anyone who questions their actions by their well paid demi-monde of analysts and commentators.

The oligarchs have almost ruined the US and the UK. They will now seek to subtly starve the middle and lower classes to pay for their piles of wealth which are largely pieces of paper, useless wagers, and will resist every effort to repeal the absolutely irresponsible tax cuts enacted during the administration of their chosen candidate G. W. Bush, and the setup to divert reform through their stalking horse, Barrack Obama.

They will speak out of both sides of their mouths. Unemployment insurance, Social Security benefits, healthcare, relief for the poor, and pensions are bad, and their unfortunate recipients lazy, stupid and an expendable drag on society. But the maintaining of ill gotten gains of the oligarchs, the enormous fortunes obtained through financial fraud, and paying little or no effective taxes on them through various loopholes, is a somehow a sacred requirement for economic recovery. And so we see how reform is floundering, and the smirks of the congressional chimps and pigmen are maintained even as the nations suffer the worst unemployment since the Great Depression.

There will be many 'useful idiots,' well outside the real circle of power but who consider themselves the well-to-do, that will agree with this injustice, and vehemently attack the unfortunate in society because of a combination of character flaws, usually selfishness, emotional immaturity, and just plain meanness. It is how it always is. Most Gestapo informants were actually neighbors, co-workers, bearing petty grudges and spites, not realizing the damage they were doing to real people. The coldness of the unenlightened human heart and the obtuse vanity of people in wishing suffering on others, with a kind of perverse self-righteousness, is sometimes a wonder to be hold.

As for the politicians and financiers, the oligarchs and those that surround them, I have tried to figure them out for a long time, often first hand. Some are just sociopaths, obsessively driven, as lacking in human feeling as the fellow who would shoot you in the face for your wallet. These white collar jokers have merely had better educational opportunities.

But as for the others, the many, I think that are just ordinary hard working people that over become so intellectually inbred that their viewpoint becomes like a clique, or a cult. They tend to be in positions where they can make or enforce the rules to suit themselves, and spend most of their time talking with others like them, with similar attitudes and feelings towards the world extensively influenced by their profession. They develop a feeling of isolation from the great bulk of humanity.

Principles such as morality, right and wrong, cease to be relevant, without the common cultural context, for them. They become so preoccupied in the particularities of their own piece of game. They lose sight of the big picture. And sometimes this can lead to terrible abuses and excesses.

As an aside, I thought the recent essay from the fellow at the Fed who did not believe that anyone who does not have a PhD were imbeciles incapable of discussing or understanding economics was a good example. Did he understand how silly he sounded, writing from the very heart of a disgraced profession, and from an organization that under Greenspan and then Bernanke look like incompetent clowns lacking even common sense? I was actually embarrassed for him. Coming from the world of technology and big corporations I know the type.

A corporate culture can degenerate into a dangerously compelling institutional blindness, especially in organizations that like to bring their people in young and 'mold them.' Whenever I see clusters of resumes with the words 'Goldman' and 'Yale' or 'Harvard' in them cringe. The CIA used to favor Yale for recruiting, since it seemed to impart an outlook in its students that was amenable to spycraft. I do not know if that is still the case, whether universities tend to develop outlooks by their choice and development of students, but major corporations certainly do.

The US cannot obtain a sustained recovery without serious and significant financial reform and restructuring of its economy, and the legal repatriation of the wealth stolen by the financiers through fraud. What complicates this is that the politicians have allowed themselves to be tainted by the same brush of corruption, so in the short term everything is illusion, deception, and cover up. Slowly but surely, the truth will out. But the delay causes damage.

The bad debts will be liquidated. They cannot be repaid. Starving the common people alone will not work, and selling the sovereign assets will not be enough. Taxes would have to be raised to post WW II levels, along the lines of 70+% for the wealthy. How likely is this? The wealthy elite will promote the confiscation of pensions and Social Security first. These will be dangerous times, full of deception. Greed and fear will reach high emotional states.

Therefore default, albeit selective, is the rationale alternative, excepting the contrivance of yet another war to stimulate demand and encourage compliant behaviour. And that default will be accomplished through devaluation of the currency, the basis of all the debt, which is the Fed's note of zero duration. It will spread the pain throughout all holders of US debt, including those that do not vote. Bernanke and his economists know this.

They will not admit it, because they are playing a confidence endgame with the people and with the holders of US sovereign debt, many of whom are foreign. The last thing they wish to cause is a panic. But at some point, there will be one, and it will not be pretty. The Democrats will attempt to kick that can down the road, delivering it to the successor to Obama, who is like to be a one term wonder 'unless something happens.'

"At what point shall we expect the approach of danger? By what means shall we fortify against it?-- Shall we expect some transatlantic military giant, to step the Ocean, and crush us at a blow? Never!--All the armies of Europe, Asia and Africa combined, with all the treasure of the earth (our own excepted) in their military chest; with a Buonaparte for a commander, could not by force, take a drink from the Ohio, or make a track on the Blue Ridge, in a trial of a thousand years.

At what point then is the approach of danger to be expected? I answer, if it ever reach us, it must spring up amongst us. It cannot come from abroad. If destruction be our lot, we must ourselves be its author and finisher. As a nation of freemen, we must live through all time, or die by suicide...

I do not mean to say, that the scenes of the [American] revolution are now or ever will be entirely forgotten; but that like every thing else, they must fade upon the memory of the world, and grow more and more dim by the lapse of time. In history, we hope, they will be read of, and recounted, so long as the bible shall be read;-- but even granting that they will, their influence cannot be what it heretofore has been. Even then, they cannot be so universally known, nor so vividly felt, as they were by the generation just gone to rest.

At the close of that struggle, nearly every adult male had been a participator in some of its scenes. The consequence was, that of those scenes, in the form of a husband, a father, a son or brother, a living history was to be found in every family-- a history bearing the indubitable testimonies of its own authenticity, in the limbs mangled, in the scars of wounds received, in the midst of the very scenes related--a history, too, that could be read and understood alike by all, the wise and the ignorant, the learned and the unlearned.--

But those histories are gone. They can be read no more forever. They were a fortress of strength; but, what invading foeman could never do, the silent artillery of time has done; the leveling of its walls. They are gone.--They were a forest of giant oaks; but the all-resistless hurricane has swept over them, and left only, here and there, a lonely trunk, despoiled of its verdure, shorn of its foliage; unshading and unshaded, to murmur in a few gentle breezes, and to combat with its mutilated limbs, a few more ruder storms, then to sink, and be no more.

They were the pillars of the temple of liberty; and now, that they have crumbled away, that temple must fall, unless we, their descendants, supply their places with other pillars, hewn from the solid quarry of sober reason. Passion has helped us; but can do so no more. It will in future be our enemy. Reason, cold, calculating, unimpassioned reason, must furnish all the materials for our future support and defence.

Let those materials be moulded into general intelligence, sound morality, and in particular, a reverence for the constitution and laws: and, that we improved to the last; that we remained free to the last; that we revered his name [George Washington] to the last; that, during his long sleep, we permitted no hostile foot to pass over or desecrate his resting place; shall be that which to learn the last trumpet shall awaken our Washington.

Upon these let the proud fabric of freedom rest, as the rock of its basis; and as truly as has been said of the only greater institution, the gates of hell shall not prevail against it."

Abraham Lincoln, Lyceum Address, 27 January 1838

What a difference there was in attitude, in the American of Lincoln's day, to the memory of the great patriots and Founding Fathers, which still was so fresh in their minds. Yes, there are always outliers and lawbreakers. But then there was a sense of outrage and disgrace at the exceptions, not a cynical acceptance of dishonor and deception as a rule.

But above all, their humility and devotion under God, to the oaths which they had solemnly taken, to preserve, defend, and to uphold the Constitution, trampled on almost daily now, from outrage to outrage, by a corrupt and greedy Congress and Executive and Judges, cynical politicians and their whoremasters the bankers, who consider themselves as gods, and the Constitution as 'just a goddamn piece of paper.'

As Andrew Jackson said of the Federal Reserve Bank of his day:

"Gentlemen, I have had men watching you for a long time and I am convinced that you have used the funds of the bank to speculate in the breadstuffs of the country. When you won, you divided the profits amongst you, and when you lost, you charged it to the bank. You tell me that if I take the deposits from the bank and annul its charter, I shall ruin ten thousand families. That may be true, gentlemen, but that is your sin! Should I let you go on, you will ruin fifty thousand families, and that would be my sin! You are a den of vipers and thieves. I intend to rout you out, and by the grace of the Eternal God, will rout you out."

Jackson had government officials secretly investigating the bankers, to obtain the evidence of their schemes and frauds. But the cowardly President, and craven and corrupt Congress, do not appear to even have the courage and the will to audit it, to force it to answer questions truthfully and with the appropriate oversight, and make itself accountable, even in the face of conflicts of interest and the appropriation of billions in funds under false pretenses, which they gave to their cronies on Wall Street. Such are the times.

Knowledge grows by sharing. When you find it, repost and and forward it wherever you can. Little by little, the truth will find a way, but it takes our efforts to set it free. I think that I am running about 12 to 24 months ahead of the curve, so the ideas expressed here will not obtain much credit now. But watch as things unfold. There is more to tell, but revelations have to be made in their due course.

And if by chance, for whatever reason, this blog should ever go dark before happier times can come, then remember me in your thoughts and prayers, as I will remember you.