Koos Jansen has an interesting piece out this morning, that asks some very insightful questions in the ongoing attempt to connect the dots between the shocking decline in the 'float' of unencumbered gold out of the London Vaults with the tremendous, and not always fully visible, flows of gold into strong hands and Asian Vaults.

As you may recall it was Koos' groundbreaking work in analyzing the Shanghai Gold Exchange that blew the lid off the enormous flows of physical gold into China, despite the stubborn opposition of some well paid establishment analysts.

And all of this is relevant to what some have called 'the currency war,' which is the attempt to forge a new international monetary regime out of the ruins of the Bretton Woods Agreement and the fiat petrodollar.

This analysis ties together with a number of highly significant events, including the backwardation of gold price, the flight of gold from the registered category at Comex, and the tightness of physical supply in London as shown by lease rates and informed observations, despite the usual scoffing from apologists.

I have seen various estimates that the London float is now adequate for about 4 to 12 months at most, given this draining of supply, before the market gets into serious trouble. That is unless a central bank or gold pool friendly semi-official fund undertakes to divest itself of more their nation's gold, as England apparently did by selling their sovereign gold wealth on the cheap near the turn of the century to bail out their banking chums, in the odd case of Brown's Bottom.

The gold in this current instance seems more likely to have been taken out as leases and sales from custodial gold holdings at the Bank of England, and the stores of gold that is backing ETFs and Funds in private vaults, having been disgorged by the actions of their participants and custodians, often the self-dealing bullion banks.

Perhaps this is mistaken. Perhaps there is a reasonable explanation for all this oddness in the gold market. Good then let us hear it, and not these silly scoldings and transparent fabrications of nonsense that seem to be the stock in trade of the bullion bullies and paperati which only serve to fuel more doubt and questions.

And why is it again that the US and UK were unable to return Germany's national gold stores in a reasonable timeframe? And India desperately looks for ways to limit their peoples' appetite for physical bullion of their own? So many questions, so much leverage, secrecy, and stonewalling.

As Koos Jansen observes:

You may read the entire piece and its complete evidence and reasoning The London Float And PBOC Gold Purchases.Consider the following:

- Good Delivery gold bars can be monetized – in countries like the UK, Hong Kong, Switzerland and Singapore – from where they can be shipped into China while circumventing global trade statistics. This is because monetary Good Delivery gold bars are exempt from global trade statistics (UN, IMTS 2010). Needless to say monetary imports into China are conducted by the PBOC.

- Non-monetary Good Delivery gold bars (declared at international customs departments) imported into the Chinese domestic gold market are required to be sold through the SGE. However, trading volume at the SGE in GD bars has been a mere 3 tonnes in all of history.

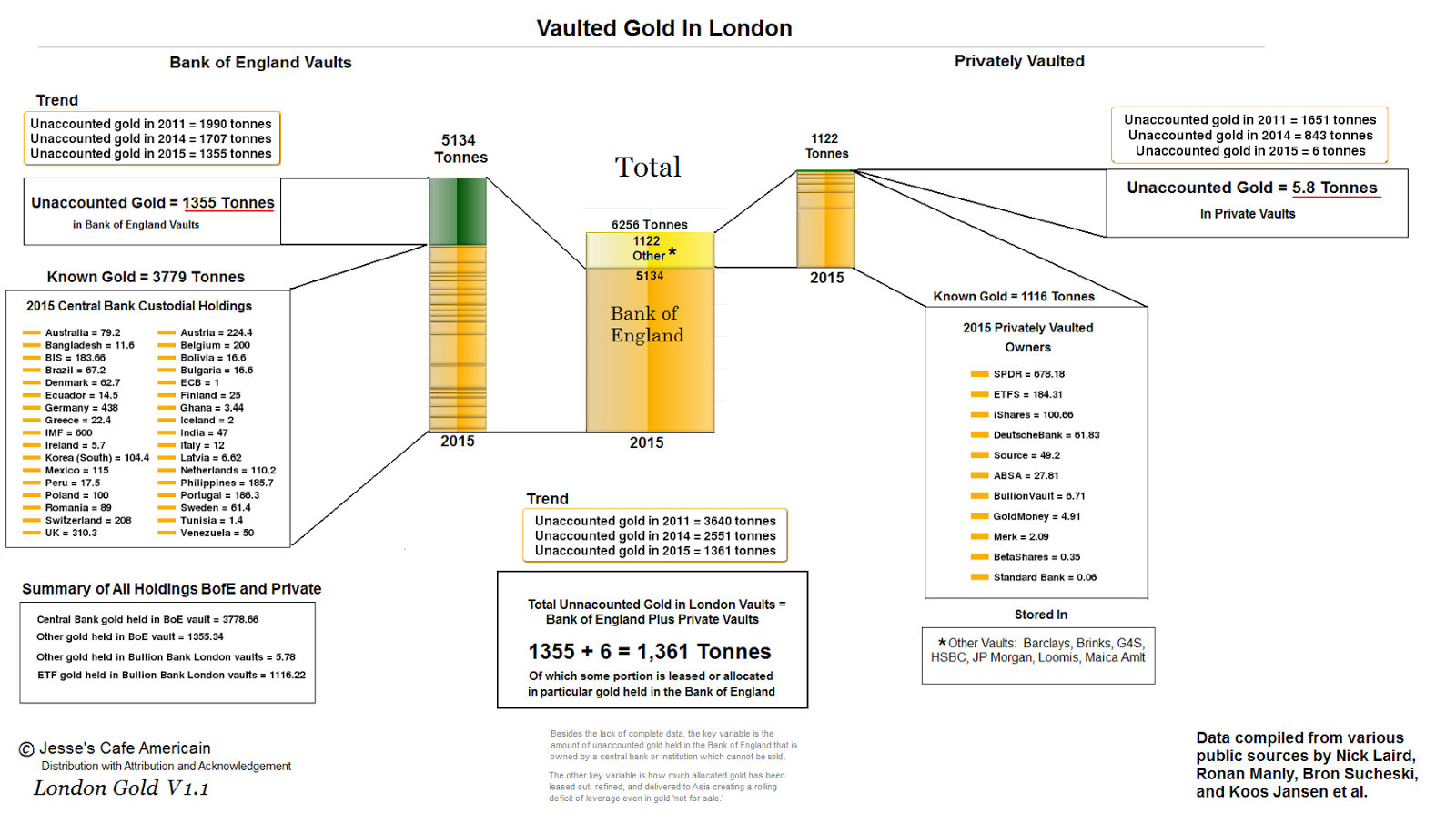

We can thus conclude that if any Good Delivery gold bars have entered China these did not go through the SGE system where Chinese citizens, banks and institutions buy gold. Instead, it’s likely that the Good Delivery gold bars that crossed the Chinese border went directly to the PBOC vaults...Nick Laird and I noticed that although the total amount of physical gold in London fell roughly 2,744 tonnes (9,000 – 6,256) over four years (graph 1), only 997 tonnes were net exported as non-monetary gold (graph 4). This makes me wonder where the residual 1,747 tonnes (2,744 – 997) went. Possibly, this gold has been monetized in the UK and covertly shipped to a central bank in Asia, for example China. I don’t have rock hard evidence, but it fits right into the wider analyses.

One thing that is strikingly odd about this is that it is one of the more revelatory accumulations of data on the shadowy corners of the global gold market since Frank Veneroso's seminal study of the flows in the gold market involving central bank gold at the beginning of the great bull market that began at the start of the new century.

And yet so many sites still have not picked up on this sea change and unfolding currency war, despite it tying together so many other observations and data and market tremors. Perhaps it is insufficiently pedigreed. The contrarian perspective says that this may be the hallmark of the real thing.