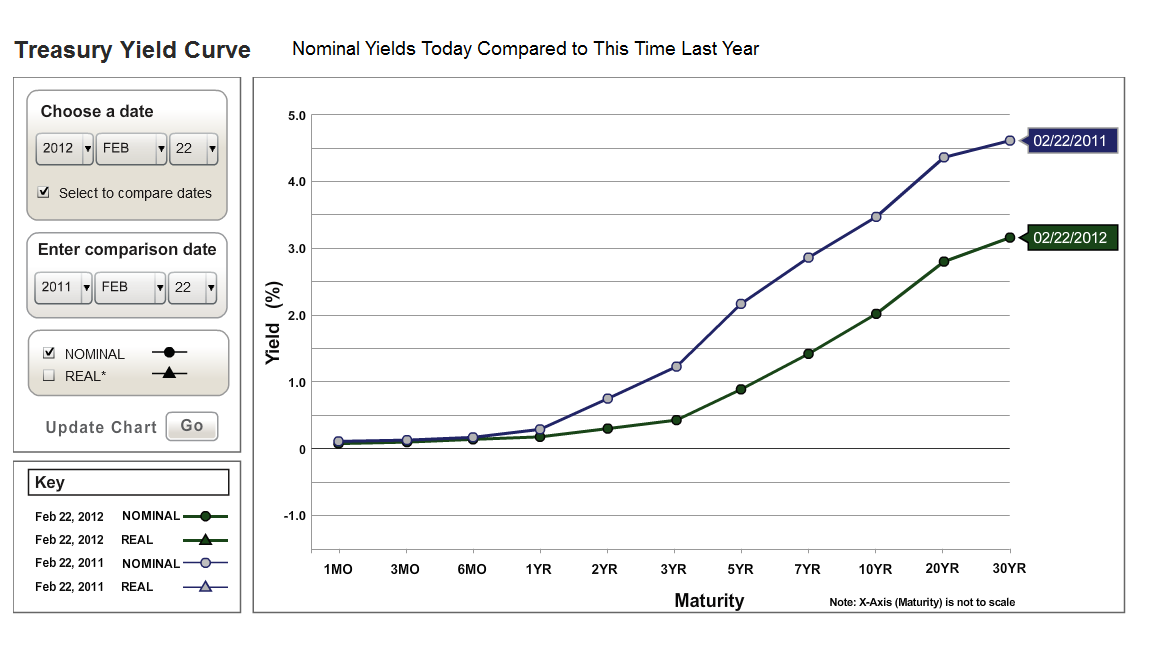

These charts compare the Nominal and Real Treasury Yield Curves provided by the Treasury Department.

The 'real' return is the return on the debt less expected inflation. A note on how the Treasury calculates this is below. Since they use TIPS the real yield are only done for notes of 5 years or more duration.

The comparison is between February 22 data from this year and last year.

As one can see, the Fed's "Operation Twist" has had a profound effect on the real returns achieved by holders of US sovereign debt.

The real yields turn positive about the 15 year mark. The real return these days on a 30 Year Bond is about .76%. And that is probably using rather optimistic assumptions about inflation risk.

What this implies is that savers are by and large paying the US government to borrow from them.

Is this an effective economic stimulus for the real economy, or a sophisticated form of seignorage being performed by the Fed on behalf of its member Banks?

Interesting experiment. I hope Benny's model has the right risk parameters plugged in. If not, as Fed policy errors go, this one could be memorable.

No wonder certain alternative stores of wealth are rallying as a haven from this soft confiscation.

"Treasury Real Yield Curve Rates. These rates are commonly referred to as "Real Constant Maturity Treasury" rates, or R-CMTs. Real yields on Treasury Inflation Protected Securities (TIPS) at "constant maturity" are interpolated by the U.S. Treasury from Treasury's daily real yield curve. These real market yields are calculated from composites of secondary market quotations obtained by the Federal Reserve Bank of New York. The real yield values are read from the real yield curve at fixed maturities, currently 5, 7, 10, 20, and 30 years. This method provides a real yield for a 10 year maturity, for example, even if no outstanding security has exactly 10 years remaining to maturity."