In the overnight action, prices have marked out where they will be going.

As for today, those powerful few who use public and private resources to

twiddle the markets in the short term, and quite a few other data metrics as well, are giving their brethren who were caught offsides by last night's election a chance to square up and get ready. That's what they do.

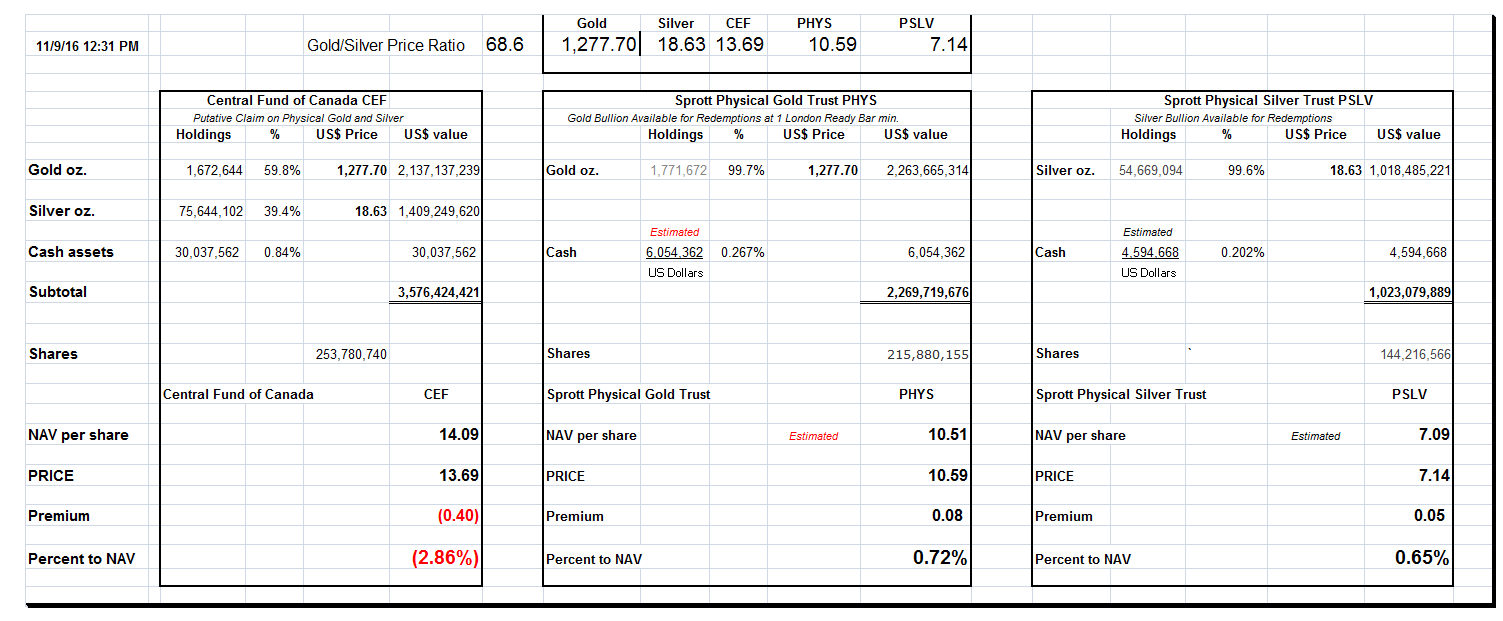

They bought the SP 500 futures for stocks, and sold paper gold and silver for the metals.

And they wished to send all the rest of us a message— vote all you like, but

we are still in control.

Being an insider means never having to say you are sorry, or mistaken. You do not have to, being a true

ubermensch and a member of the right sort, from the right schools and with the right connections in the masterful power elite.

You cannot be wrong,

ipso facto, because you rule by virtue a claim to a natural worthiness and superiority. To admit error is to deny yourself as you wish others to perceive you to be. And you become ever more deeply mired in frauds of every kind.

That is the

credibility trap.

However, let us not mistake this bravado from the Wall Street globalisation project and the system of calculated inequality for what it really is.

They were wrong on the election, they are wrong on money, and they have been wrong on the economy for far too long.

They have been compounding their errors as they go, almost compulsively down a selfishly dangerous path, because it benefits them and their patrons financially, and they do not know what else to do without admitting that they were wrong.

We have seen worse, even in my short lifetime, and certainly in that of our parents and grandparents.

This is the point where you find your 'inner man,' to borrow a time worn phrase, and carry on because it is your obligation and your calling to do so.

And for those with a comedic or cynical bent, the next four years will most likely be a treasure trove of material on the borders of absurdity.

That is my take on this. And being just a man, with all that implies, I could be wrong.