AEIR

Triffin’s Dilemma, Reserve Currencies, and Gold

By Walker Todd

Nearly 50 years ago, Yale University economist Robert Triffin identified the inevitable future deterioration of the dollar in his book, Gold and the Dollar Crisis: The Future of Convertibility (1960). Essentially, Triffin argued, under the Bretton Woods system in which the U.S. dollar was the world’s principal reserve currency (instead of gold, for example), the United States had to incur large trade deficits in order to provide the rest of the world with the liquidity required for functioning of the global trading system.

Unfortunately, Triffin wrote, U.S. trade deficits eventually would undermine the foreign exchange value of the dollar because foreign accounts would hold an increasing quantity of dollars. Restating Triffin's argument in contemporary terms, as the proportion of dollar claims held abroad versus U.S. gross domestic product (GDP) increases, the foreign exchange value of the dollar must decline if dollar interest rates do not increase at about the same rate as the foreign dollar claims.

Issuing the reserve currency gives domestic policy makers an advantage by making it easier to finance either domestic budget deficits or foreign trade deficits because there always is a ready bidders' market for any financing instruments from that issuer. Issuing the reserve currency enables the domestic population to consume more goods and services from whatever source than otherwise would be feasible. And issuing the reserve currency gives foreign policy officials of that nation the upper hand in determining multilateral approaches to either diplomacy or military action.

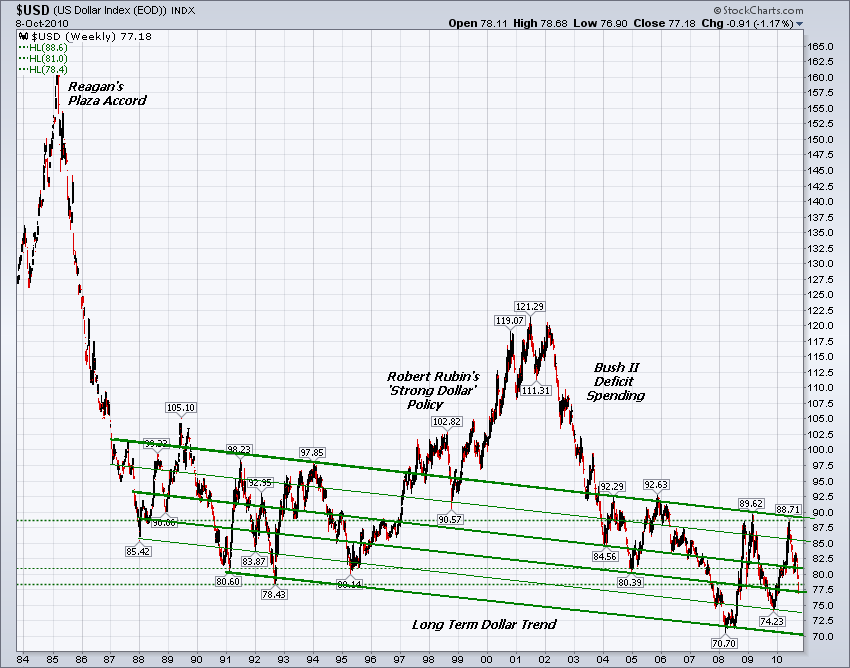

This last reason probably is why U.S. policy makers clung to the original Bretton Woods format for about 10 years beyond the point at which it still was viable, with the whole apparatus finally collapsing in August 1971.

Let us reconsider the effect of reserve currency issuance on domestic and foreign trade for a moment. Unless the issuing authorities can discover a way to allow their currency to depreciate more or less in proportion to the growing foreign trade deficits—by reducing interest rates or otherwise stimulating domestic inflation, for example—then a sustainable equilibrium becomes impossible.

Either the currency remains overvalued (good for the reserve currency status) and the trade deficits continue to increase, or the currency maintains fair external value (implicitly, a proportional devaluation, which is bad for the reserve currency status) and the trade deficits either stabilize or shrink. This latter proposition is what Professor Triffin was writing about in 1960, and it has been called Triffin's dilemma ever since.

Lewis Lehrman and John Mueller revived the discussion of Triffin's dilemma, without calling it that, in an article that appeared on December 15, 2008, in National Review Online. They suggested that the proper international reserve currency should be gold. I agree and wrote as much in a commentary, in the Christian Science Monitor, November 17, 2008.

Lehrman and Mueller argue correctly that no country willingly should volunteer for the reserve currency role. Such an endeavor necessarily leads to the same pattern of persistent overvaluation and trade deficits that plagued the United States since European currencies became generally convertible in 1959. Our abandonment of the international gold exchange standard in August 1971 accelerated and intensified our external deficits and the volatility of exchange rates.

Among advanced economies that were key members of the old Bretton Woods system, tolerating large amounts of external claims in their currencies always was a sore point because they wanted to avoid de facto reserve currency status and the curse (Triffin's dilemma) that accompanies it.

In the last two decades, roughly since the fall of the Berlin Wall in 1989, European countries have adopted the euro and allowed large external claims in euros to arise. The Japanese bubble of the 1980s finally burst and relieved the reserve currency pressure of large external claims there until the last couple of years. Recently prosperous nations like China, India, and Brazil linked their currencies to the dollar and managed exchange rates so as to avoid the accumulation of large external claims. Thus, none of the most likely candidates is volunteering for reserve currency status...