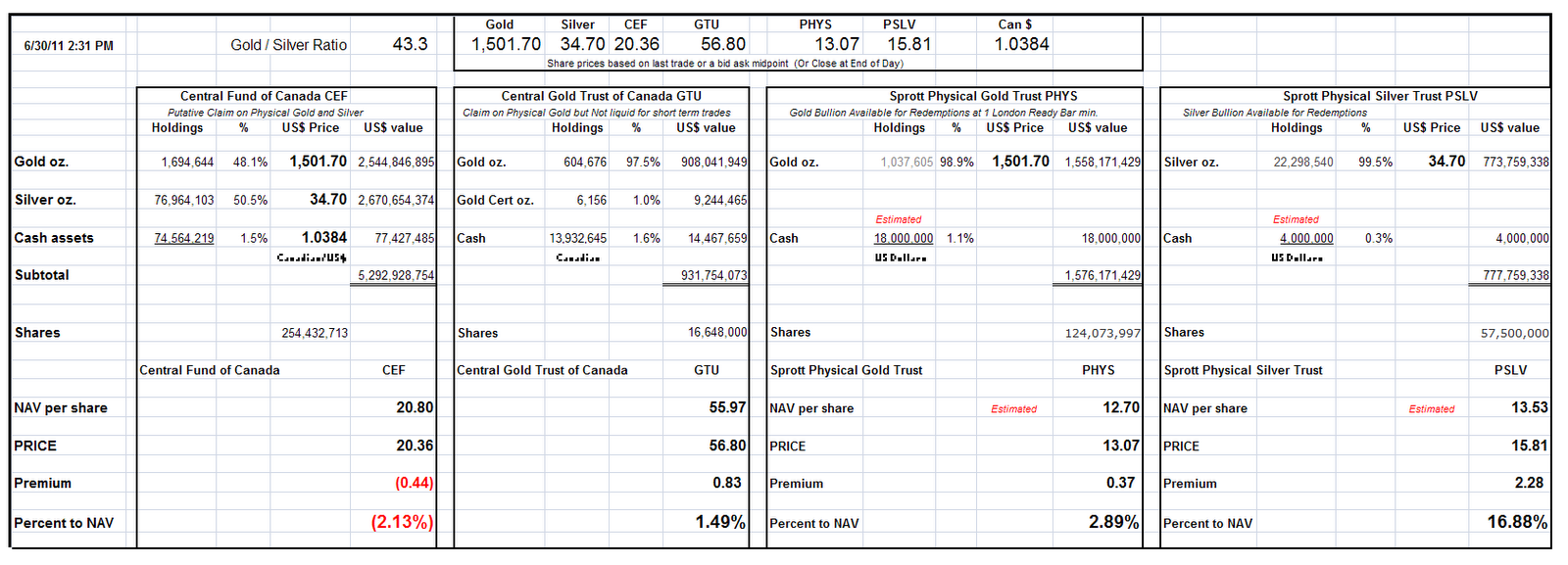

I am using this opportunity to combine two items of interest to precious metals investors. I do not consider them to be particularly related. In other words, I do not consider any of the funds to have the same counterparty risk as some other financial assets purporting to represent an avenue towards the protection of precious metal ownership such as GLD and SLV and even Comex Futures contracts and options.

I do still think the premium on Sprott silver reflects the scarcity of bullion and the relatively friendly terms of taking ownership of metals from the fund, but this is just a theory.

"We have a very tough time understanding those bearish arguments against silver. We look at the real silver market, and based on the supply and demand data coming from the real, physical markets for silver, the fundamentals are only getting stronger.

And yet there exists another silver market, which as we’ve shown, is not very connected to the physical realm at all. And though silver investors have for decades suffered the tyranny of a rigged paper monopoly over silver price discovery, it appears to us that the tides are turning. In the age of QE to infinity, investors are being more scrupulous with their capital and as such they are demanding physical silver in quantity.

With more and more dollars flowing into the silver markets and a finite supply of physical to meet that demand, the theoretical losses for the paper silver short-sellers are near infinite. And with such a skewed and obvious risk/reward payoff vastly favoring the longs, we pose the following question.

Who is most at risk in the silver markets: the buyers of a scarce and real asset that serves a growing multitude of purposes, or the sellers, who are short a quantity of silver which may very well not even be obtainable at anywhere near current prices?

Let the Seller Beware!"

Sprott Asset Management, Caveat Venditor

I should add that buyer must also beware, because of the growing counter-party risk as the leverage extends and the available supply shrinks. If the dominos start to tumble, we have seen that the counter party risk can quickly cause the problem to reach critical mass. This is because the financial sector is grounded in leveraged speculation and gaming, and not in the real economy.

For years I had watched the charts showing the 'netting' effect of the derivatives markets, and how the nominal risks were really much lower because of the netting effect. However, once the markets were actually stressed, the netting fell apart because of a couple of major participants who could not deliver.

I think the same situation still exists in a number of markets due to the very weak financial reform and lax oversight of the Fed, the SEC, and the CFTC in particular. And of course the extreme moral hazard of bailing participants out of their oversized risks when they fail.

When you go to collect your silver, you may find only a stack of paper IOU's depending on which vehicle you are using.