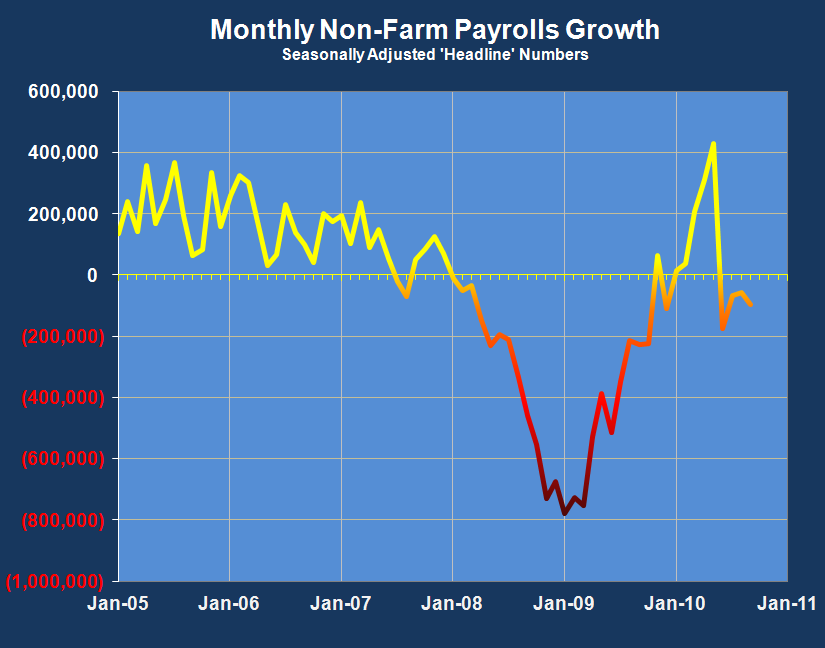

Here is an excerpt from today's Bureau of Labor Statistics Non-farm Payrolls report.

Here is an excerpt from today's Bureau of Labor Statistics Non-farm Payrolls report.

"The unemployment rate rose from 9.8 to 10.2 percent in October, and nonfarm

payroll employment continued to decline (-190,000), the U.S. Bureau of Labor

Statistics reported today. The largest job losses over the month were in con-

struction, manufacturing, and retail trade.

Household Survey Data

In October, the number of unemployed persons increased by 558,000 to 15.7

million. The unemployment rate rose by 0.4 percentage point to 10.2 percent,

the highest rate since April 1983. Since the start of the recession in

December 2007, the number of unemployed persons has risen by 8.2 million,

and the unemployment rate has grown by 5.3 percentage points...

The civilian labor force participation rate was little changed over the month

at 65.1 percent. The employment-population ratio continued to decline in

October, falling to 58.5 percent."

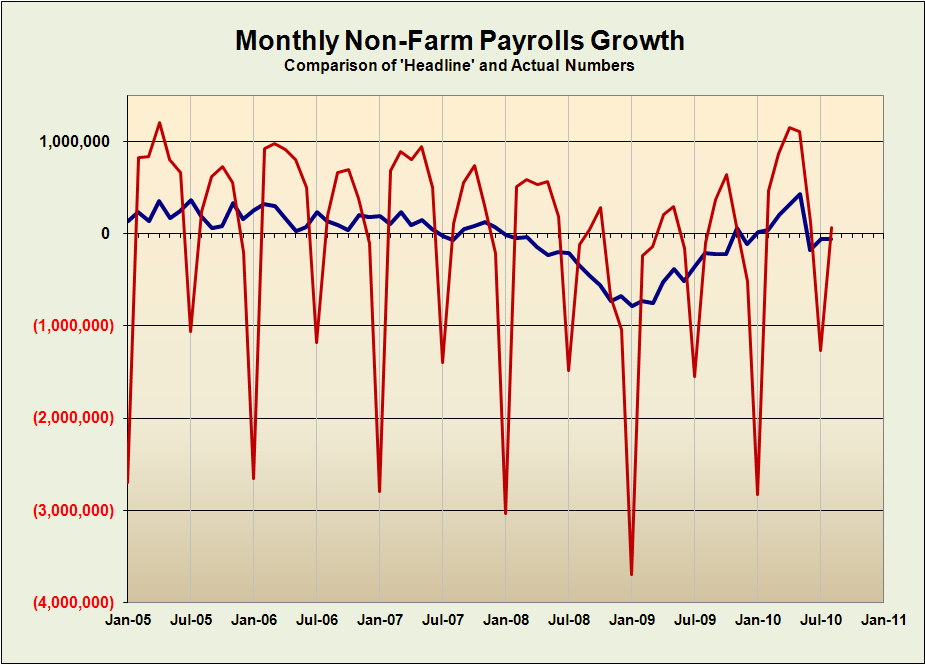

An astute reader noticed that the BLS press release says that 190,000 jobs were lost from payroll employment, but the number of unemployed persons increased by 558,000. What's up with that?

The BLS report consists of two independent data samples. BLS has two monthly surveys that measure employment levels and trends: the Current Population Survey (CPS), also known as the household survey, and the Current Employment Statistics (CES) survey, also known as the payroll or establishment survey.

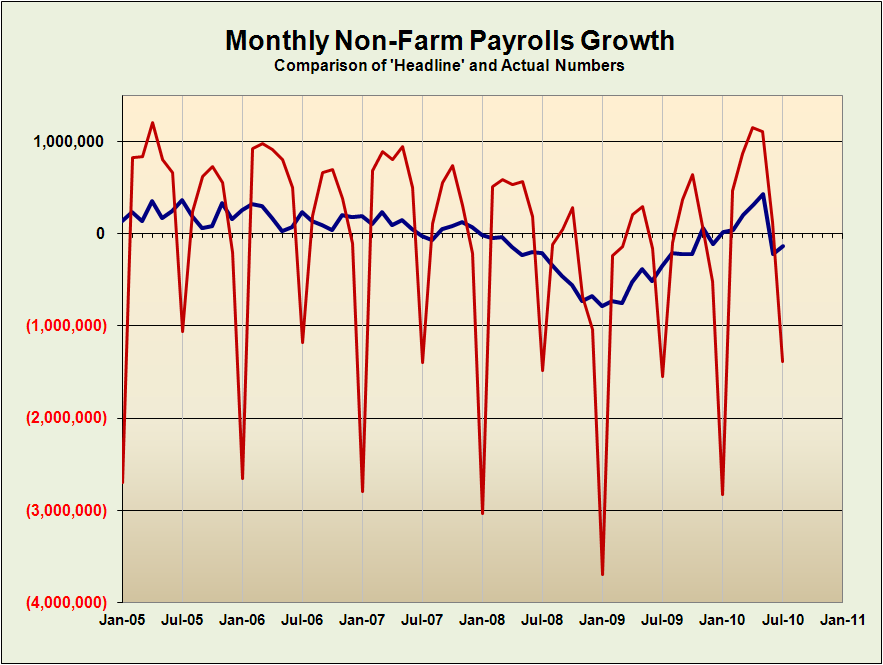

There is the "Establishment Survey" which is based on responses from a sample of about 400,000 business establishments, about one-third of total nonfarm payroll employment. The headline payroll number, the job loss of 190,000, is based on this data.

Then there is the "Household Survey" which is a statistical survey of more than 50,000 households with regard to the employment circumstances of their members, which is then applied to the estimates of the US population to obtain the unemployment number. This survey was started in the 1950's and is conducted by the Census Bureau with the data being provided to BLS. It is from the household survey that more detailed information is obtained about employment statistics within population groups like gender and age, wages, and hours worked. It is this study that is responsible for the unemployment rate of 10.2%.

So which survey is correct? Neither. The truth is somewhere in between.

The most obvious reason for the discrepancy is that job creation in the US seems to be centered in the smaller business and the self-employed areas in recent years. These sectors are not polled by the BLS and their impact would only be obtained by the Household Survey's interviews.

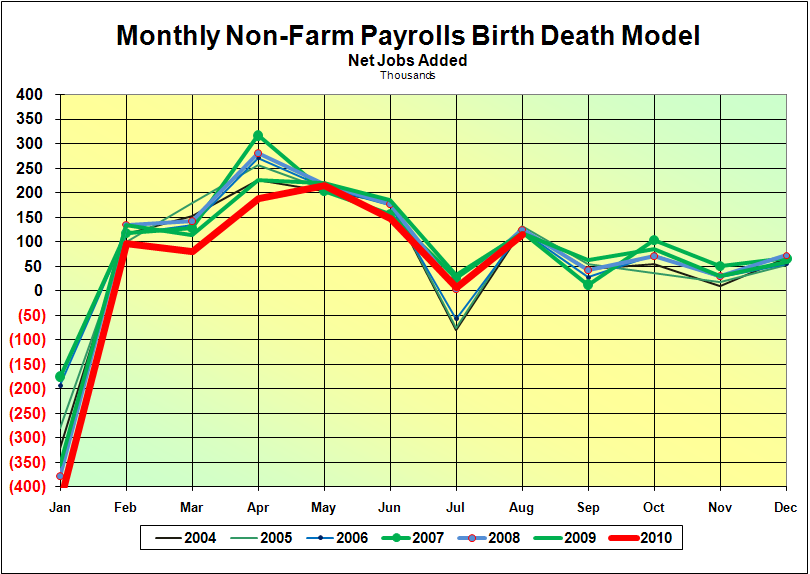

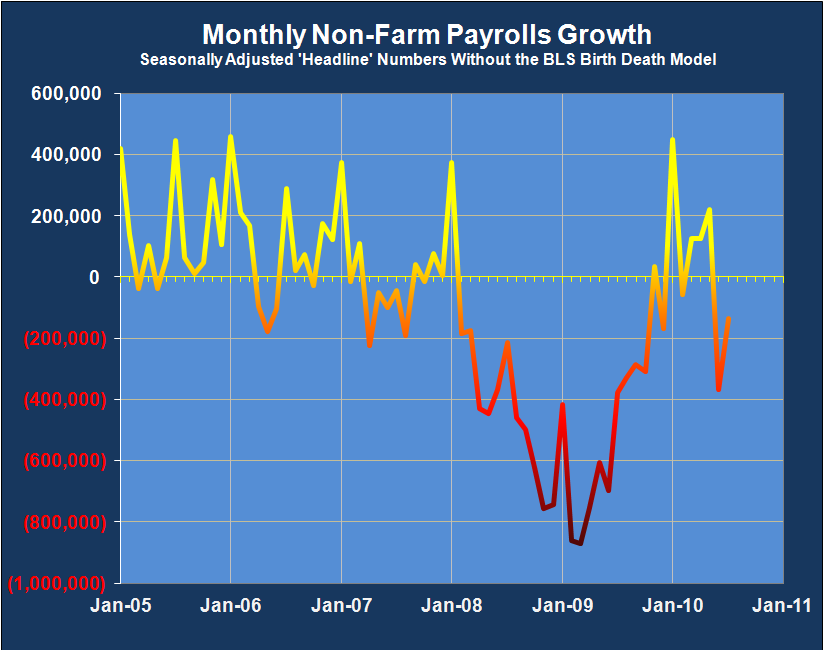

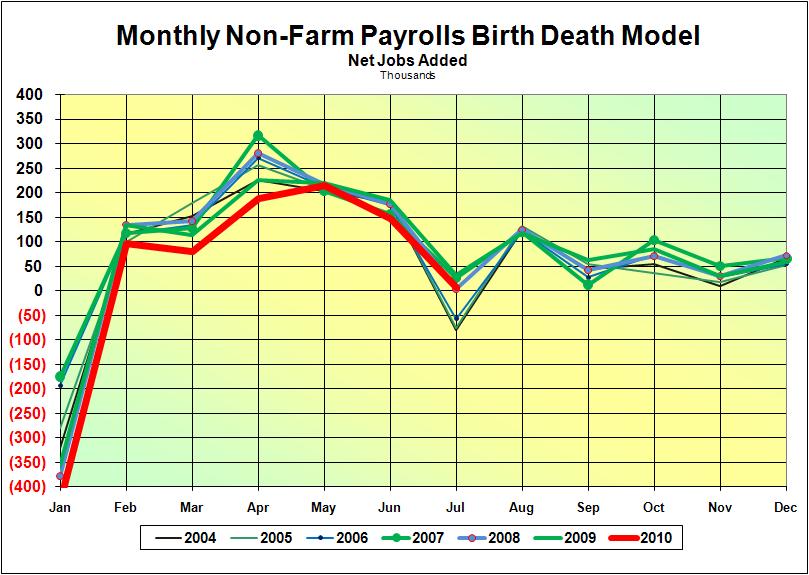

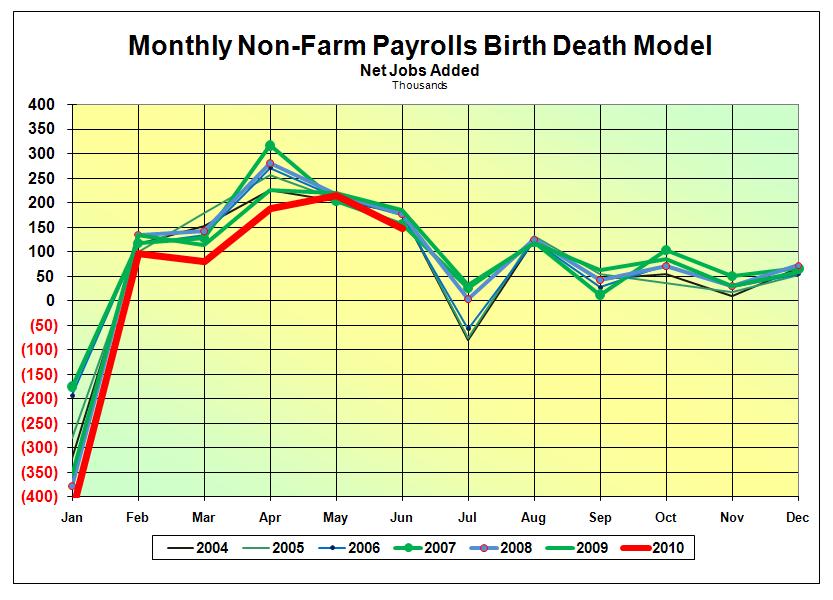

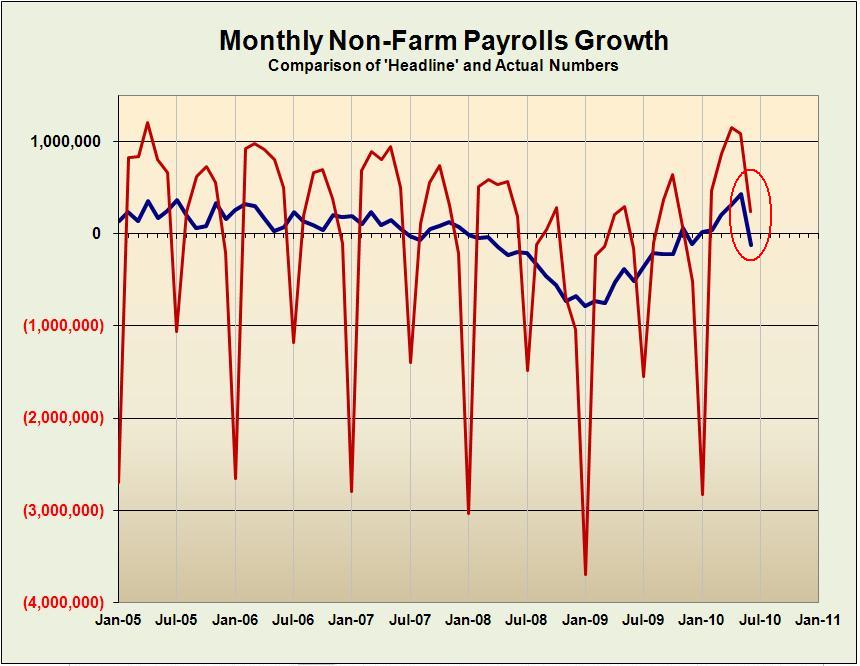

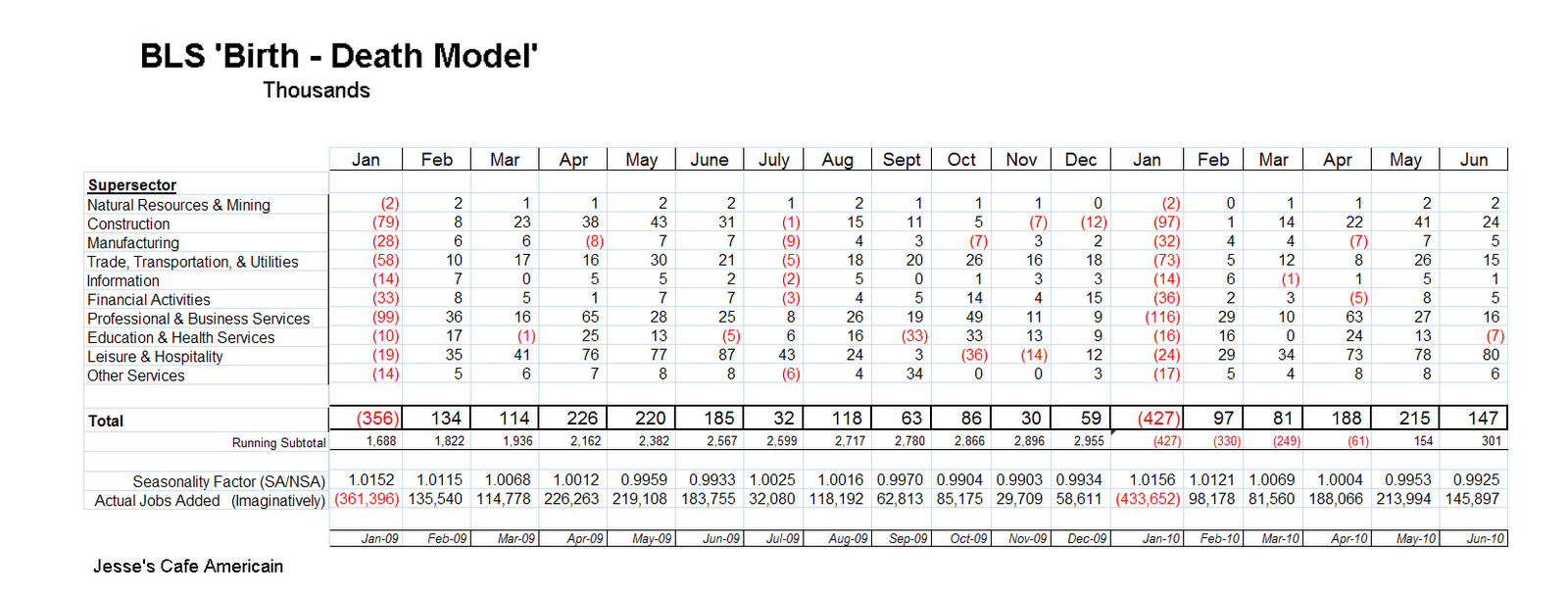

The BLS does have a way to account for this called the "Birth Death Model" which is supposed to estimate jobs created by smaller businesses. That model is a bit of a joke actually since it almost always follows the same pattern of adding jobs, with two big corrections in January and July of each year when it will do the least damage to the headline number. Any model that does not reflect the job declines that started in 2007 can most certainly be called a statistical joke. Small business is not immune to business cycles.

The payroll survey for October will be revised several times in the short term, with each release of monthly data, and even larger revisions will be done periodically, every year or so, to correct the whole series and sometimes dramatically.

The household survey is not revised per se, but the data against which it is statistically evaluated, the census data of the population, will be revised and this will change the representation of the monthly samples. Let's hope that lowering of the population is only done by revision of the numbers, and not the more draconian things practiced throughout the earlier part of the 20th century.

There was a famous joke that the Household Survey and the Establishment Survey were synchronized under George W. Bush by getting rid of people, by lowering the estimates of the population that is, which is something his pappy did when he was the president. In the states there will be a new Census conducted in 2010 as you yanks may already know, so we will have to see if the census bureau's population estimates are lowball or highball.

So what are we to conclude from this?

First, that Wall Street and the government use the monthly jobs data as tools to achieve their particular ends, to justify programs, to buy and sell, to promote certain ideas and behaviours in the public. Secondly, people will believe what they wish to believe to suit their biases if they are not fact-based in their thinking.

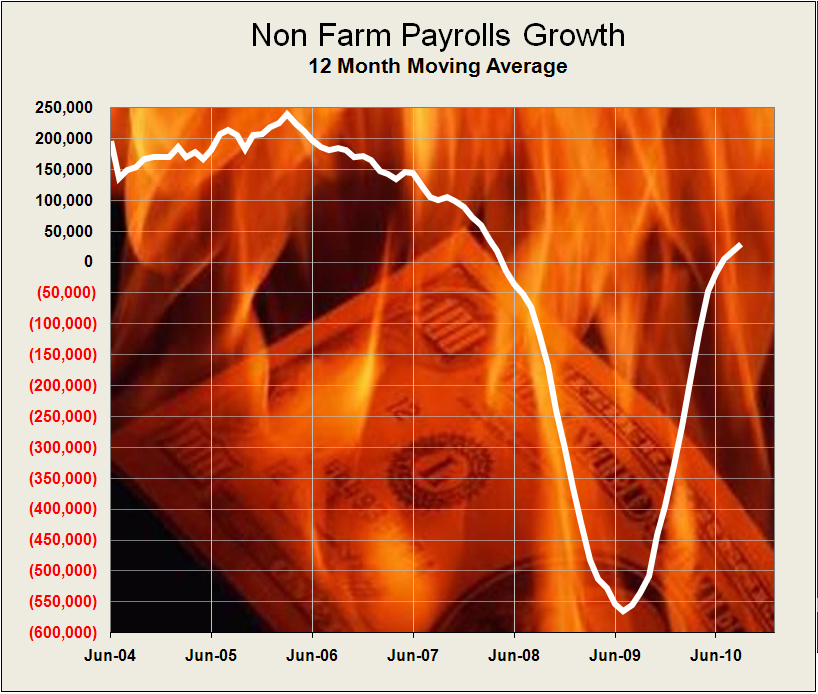

The truth is more clearly demonstrated in the long term trends, the averaging of the data over time. It does not seem that the long term data is as manipulated as the Consumer Price Index information which has become a statistical disgrace with its hedonic adjustments.

So what do we do, the average person with too little time and too many other priorities, at times seemingly held captive by the flows of information from the mainstream media? As always, we must sift what the government and business tell us, with a keen eye for deception which is an unfortunate part of human nature especially when things are not going well and it is easy to rationalize many things, and do what seems to be the right thing based on our own judgement and a broader analysis of all the news.