"A new tyranny is thus born, invisible and often virtual, which unilaterally and relentlessly imposes its own laws and rules."

Jorge Mario Bergoglio, Francis I

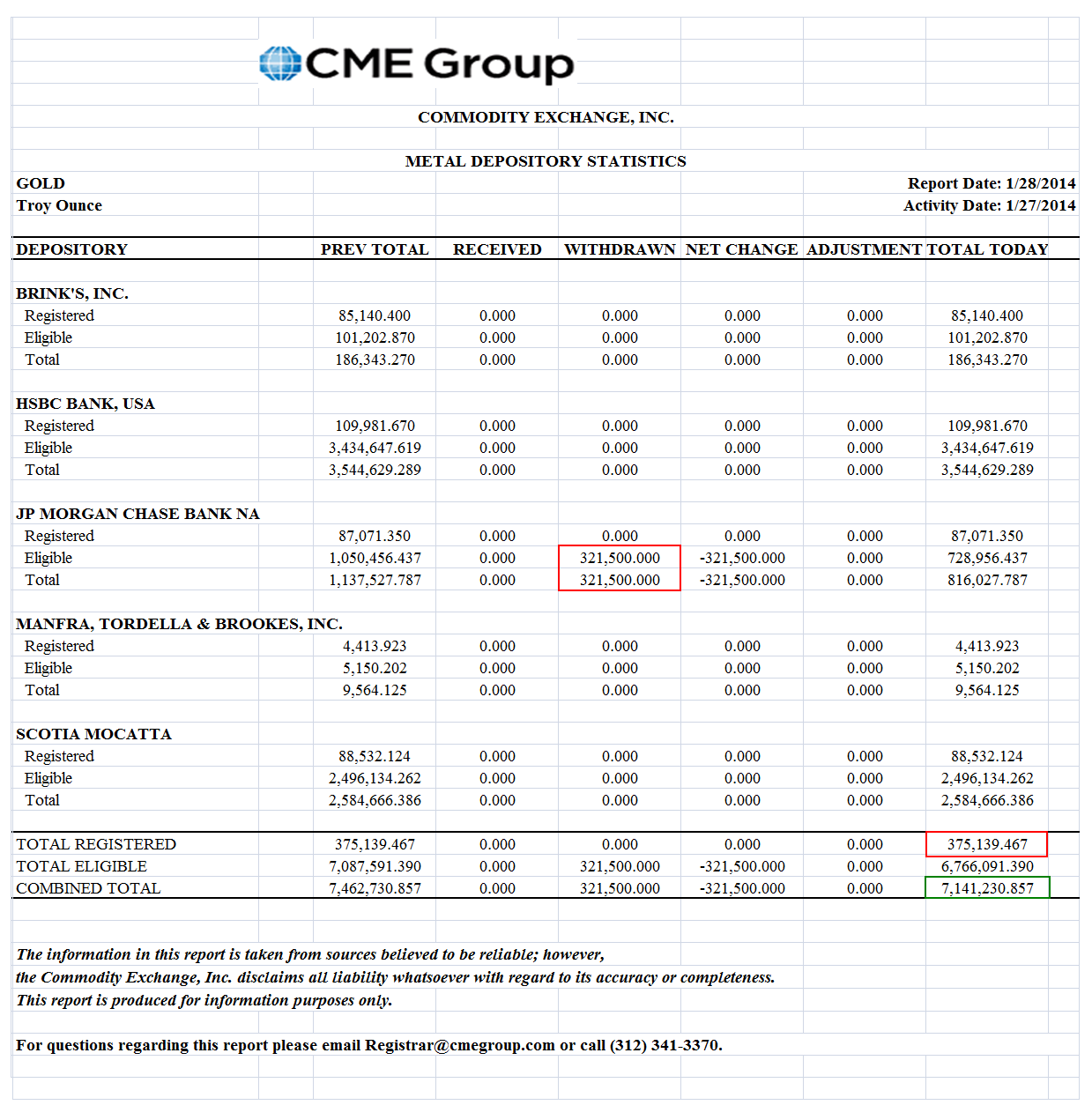

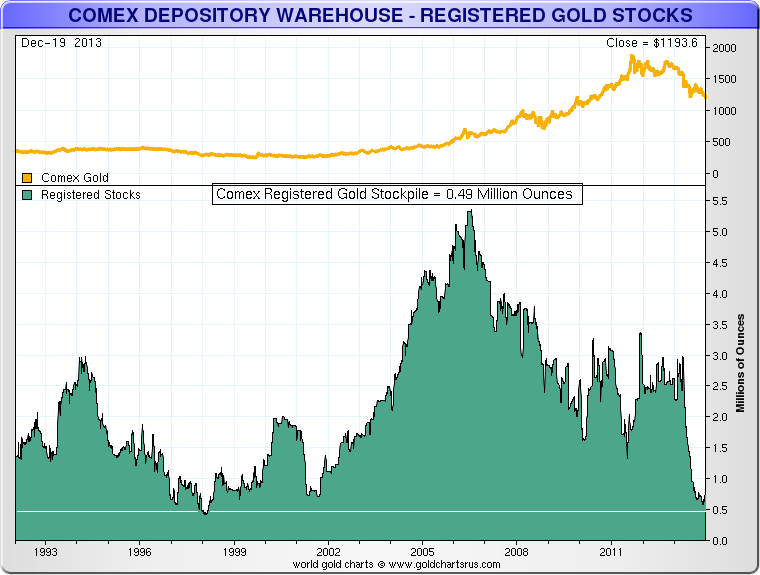

Here are the latest inventory figures of registered (deliverable) gold in Comex approved warehouses.

I am not sure

approved can really apply, given the distancing that the Comex recently instituted in the disclaimer on their inventory report.

"The information in this report is taken from sources believed to be reliable; however, the Commodity Exchange, Inc. disclaims all liability whatsoever with regard to its accuracy or completeness. This report is produced for information purposes only."

Perhaps we should start saying

recognized, or

acknowledged. Comex takes the quantity and quality and availability of gold bullion in these warehouses at 'face value' based on unaudited reports from the vault managers and releases the data 'for information purposes only.'

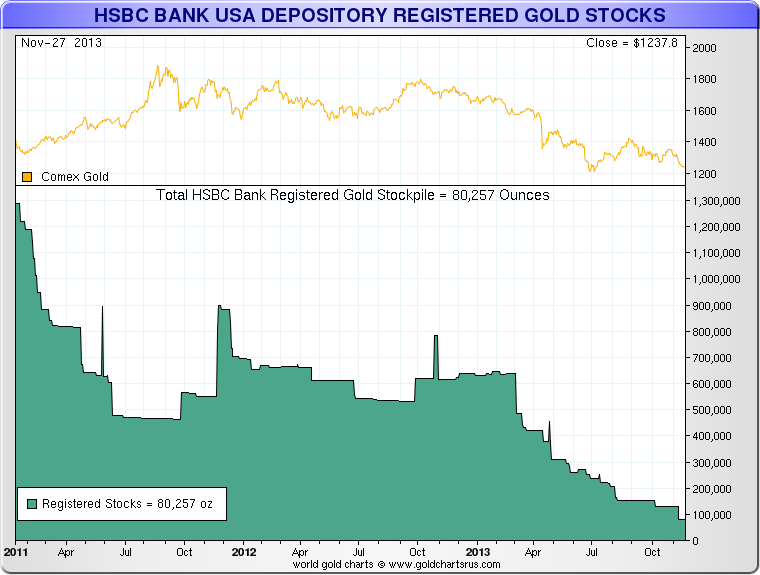

I will never forget the instance where Harvey Organ and son paid a visit to the Scotia Bank vault, and found so little actual bullion on the premises. Here is

their audio interview from 2010.

The Scotia reports show that the backing for their gold and silver certificates had fallen to 43% at fiscal year end of 2009. This situation was corrected after being reported to officials.

While some cavalierly dismiss this incident, saying that Harvey and son 'should have known,' in fact the point was that this was a surprise to many, and it was corrected only through an accidental encounter of a customer with the reality of what the Bank had been doing.

Sometimes these accidents occurred during periods of stress, as in the case of MFGlobal. It has to do with the discrepancy between

supply and

apparent supply.

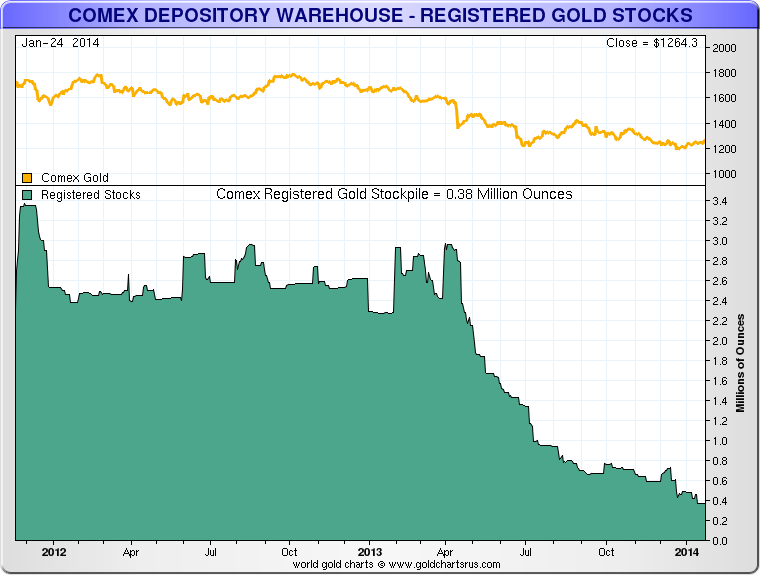

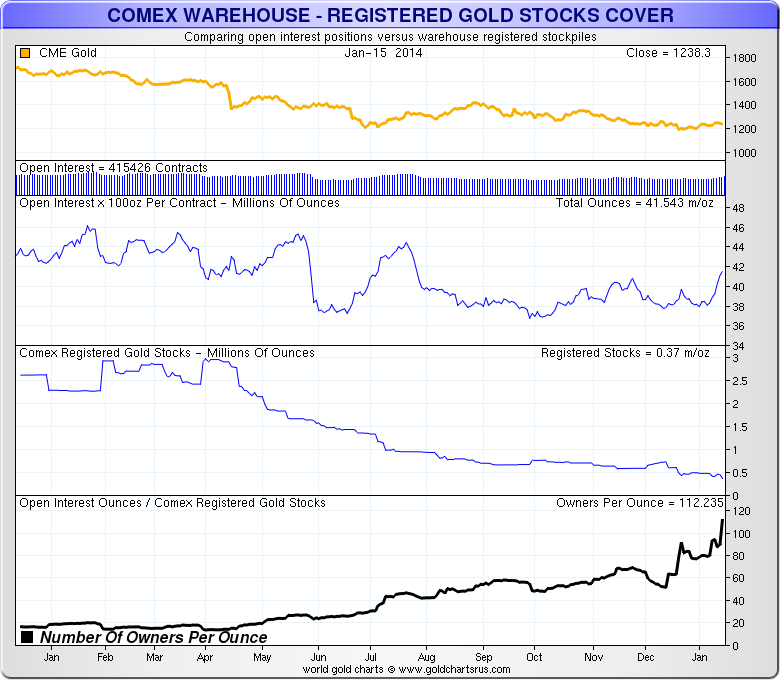

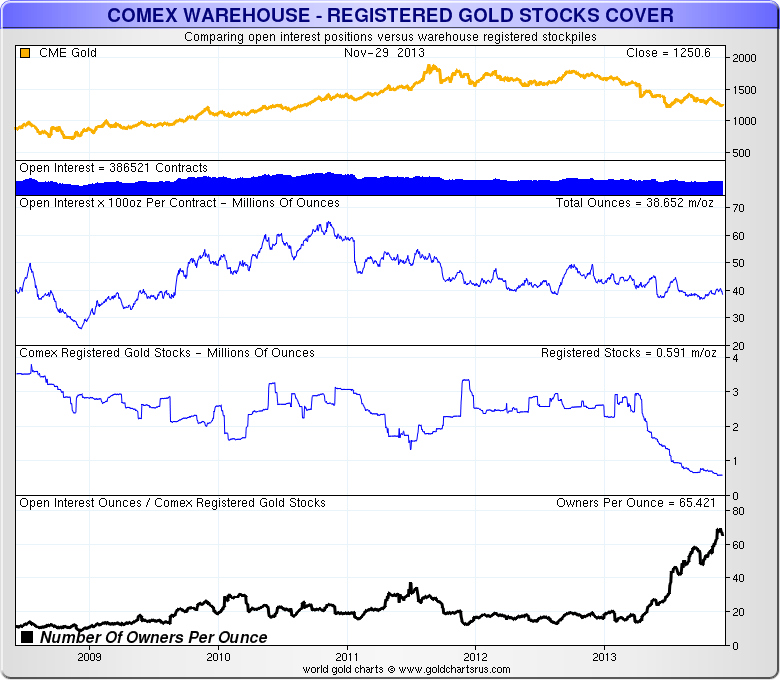

As a quick word, although some like to refer to the chart below as 'owners per ounce,' I think it is important to remember that the Comex is not really a physical market, and so only a small minority of contracts actually become presented for delivery.

However, the 'potential claims per ounce' of deliverable is a useful metric, especially at the extremes, in much the same way that 'days to cover' is a useful metric for short interest in stocks, keeping in mind the presumption in that figure that the price can rise without restraint. No one expects all the shorts having to cover at the same time, but the metric is a useful measure of short interest nonetheless.

And so it is with potential claims per ounce, although in this case we are looking at what is considered deliverable, rather than every ounce of bullion that could potentially exist in the world for what I would think are obvious reasons.

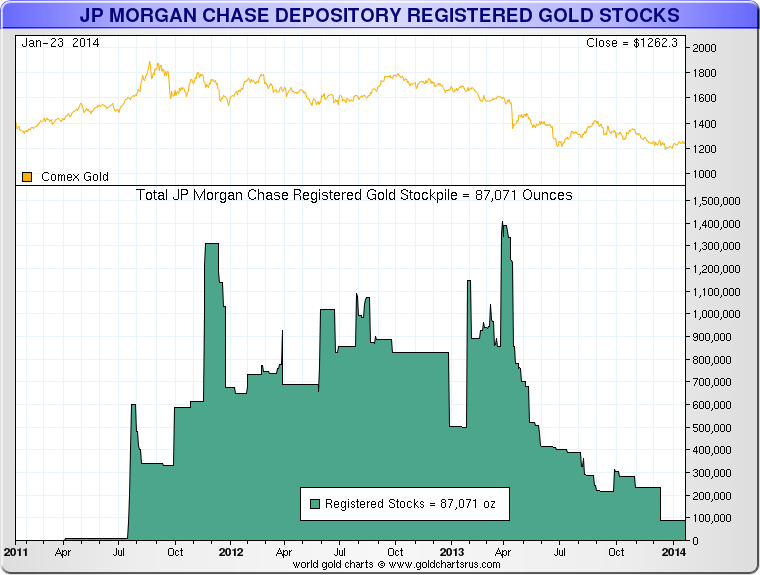

Why don't I just look at the eligible? Well I do, but one must keep in mind that just because bullion is called eligible does not indicate that it is for sale, not at all. It is just bullion being stored in a particular form in a particular vault. It is the registered or deliverable bullion that is available at the current price levels, which is really the point after all, isn't it?

And for those who watch the Comex for default, eligible does not work all that well, because in the case of a run on bullion, I would imagine those who have bullion in storage in one of the those acknowledged warehouses would pull their own stock out fairly quickly, as they might be permitted.

As you know, and as I must remind you, Comex could suffer a break in confidence, a

de facto default, but an actual default is not likely because of the exchange's ability and possible willingness to invoke

force majeure and dictate a settlement in paper money.

If some incident should provoke owners and investors to wish to take possession of their bullion, one must consider what the implications might be. How long will they have to wait to receive their property, if it will be returned at all, or in kind at some dictated settlement price?

Is this some extreme circumstance not worth considering, to be sneered at by the usual apologists, those who think of bullion very cynically as

just a trade? Don't worry, nothing to see here, move along.

There is plenty of hyperbole on both sides of these questions. I try not to add to it, but to keep going with what can be discovered, in the hope of shedding some light on the subject. And so I tend to ignore the misleading statements or insubstantial comments made by those who are merely seeking an audience. And I would urge those who are on the bullion side of things to tone it down to the facts as well, although the urge to be heard is often a strong allure.

If anything, I blame the government regulators and the exchanges for the opacity and lack of firm understanding in the markets for certain commodities. If there was clarity, the amount of speculation would be significantly reduced. But apparently they do not wish to do this for whatever motives they might have.

How can one have confidence in a commodity system in which prices are set on an exchange that rarely involves actual delivery, and whose inventory levels are issued 'for information purposes only' without audits?

Given the recent experiences of those who held bullion claims with MF Global who were handed a dictated settlement, and the people of the nation of Germany who will be waiting seven years for the delivery of their property, I think not.

There are always those who will say, 'no problem, nothing has broken yet. Don't be an alarmist.' And they will continue to do so until a thing finally hits the wall, and people get hurt. And then they will have walked away, no longer to be found. This is what happened at MF Global. And in the financial crisis of 2007-2008. And continues to happen today.

As always, the devil is in the details and the leverage, and what has been hidden will be revealed. Eventually.