Considering the AMB and the narrow money figures went parabolic, with the greatest increase in Fed history, these are somewhat unusual words from a Fed official.

Considering the AMB and the narrow money figures went parabolic, with the greatest increase in Fed history, these are somewhat unusual words from a Fed official.

Best to take him at his word. He is only saying the truth about what the Fed is already doing. This sounds like a classic misdirection.

Let's guess. In order to save us he Fed should give more money to the big money center banks through Fed programs? The Fed should buy bad assets at par from unconventional parties like every large corporation with bad debts? The Fed should more aggressively debase the currency and to transfers the wealth of savers of to those who caused this crisis?

This ought to be fun to watch.

Bloomberg

Fed Should Expand Supply of Money, Bullard Says

By Scott Lanman and Anthony Massucci

Feb. 17 (Bloomberg) - Federal Reserve Bank of St. Louis President James Bullard said the U.S. faces a risk of “sustained deflation” and called on the central bank to avert a decline in prices by expanding the money supply.

The prospect of deflation is a “significant downside risk” and may increase home foreclosures, Bullard said in a speech today in New York. Adopting a target “rapid” growth rate for the monetary base, which includes money in circulation and banks’ reserve deposits with the Fed, should “head off any incipient deflationary threat,” he said.

Bullard is one of a few Fed officials to advocate a new policy tool after the Federal Open Market Committee in December cut its main interest rate almost to zero. The central bank is using money-creation authority to put assets such as home loans on its balance sheet, aiming to unfreeze credit and end the longest recession since 1982.

“By expanding the monetary base at an appropriate rate, the FOMC can signal that it intends to avoid the risk of further deflation and the possibility of a deflation trap,” Bullard said in prepared remarks to the New York Association for Business Economics.

He didn’t propose a specific figure for the target.

The FOMC said in its Jan. 28 statement that there’s “some risk that inflation could persist for a time below rates that best foster economic growth and price stability in the longer term.”

Growth Target

The FOMC at its December meeting discussed setting a target for growth in measures of money, such as the monetary base. While a “few” policy makers favored a numerical goal for money growth, most preferred a more open-ended “close cooperation and consultation” with the Fed board on how to expand assets and liabilities, according to minutes of the session.

Bullard’s warning about deflation is stronger than comments by other central bank officials. Chicago Fed President Charles Evans said Feb. 11 that he’s “not tremendously concerned about deflation.”

Bullard told reporters after the speech he supports the adoption of an inflation target to prevent expectations for prices from falling too far. A target for inflation “would be helpful at this time,” he said.

“You have to consult with all players, including Congress,” he said. “If they don’t want to do it, then we don’t do it.”

17 February 2009

St. Louis Fed Chief Says Fed Must Inflate Money Supply More Aggressively

18 January 2009

The Fed is Monetizing Debt and Inflating the Money Supply

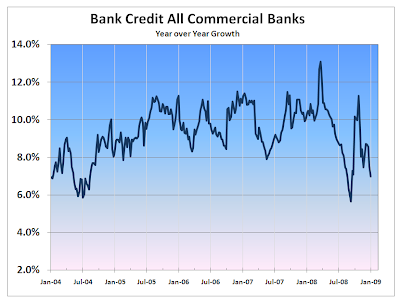

Here are the latest figures on the growth of the various money supply measures.

Here are the latest figures on the growth of the various money supply measures.

See Money Supply: A Primer for a review of measures and their differences.

The charts indicate that the growth in the money supply is due to a significant monetization of debt by the Fed in expanding its balance sheet and deficit spending by the Treasury, rather than organic growth from credit expansion from commercial sources and economic activity. The negative GDP figures confirm this.

You could imagine this as a tug of war if you wish. On one side is the deflationary force of bad debt and falling aggregate demand. On the other is the Treasury, the Fed, and the Congress, using the triple threat of deficit spending, monetization of debt, and stimulus programs. The limits of the power of the Feds are the value of the dollar and the acceptability of Treasury debt.

There is no lack of debt that can be monetized. To think otherwise is fantasy. But there are limitations about how much the dollar can bear, which is why the banks and moneyed interests have shoved their way to the front of the line, and are gorging themselves now with a little help from their friends in the Treasury and the Fed. When the time comes they intend to throw the public agenda under the bus. Its an old script, many times performed with minor enhancements.

If the current trend continues, it will have an inflationary effect on certain financial assets and commodities, and a negative impact on the dollar. There are lags in the appearance of this, but it will come.

Because the Dollar Index (DX) is an outmoded and artificial measure of dollar strength, containing nothing to account for the Chinese renminbi for example, it may not be a true reflection of the progress of this inflation. Time will tell.

A similar case might be made for certain strategic commodities, gold and oil, which are the instrument of government policy. Although it is much less important, silver may be one of the first commodities to break out because the government maintains no significant physical inventory of it as it does for gold and oil.

The huge short interest in silver may be an ignored scandal on the order of the Madoff Ponzi fund, not in dollar magnitude, but likely in terms of regulatory lapse and deep capture.

M1 has become a much less useful measure of the money supply these days because of changes in banking rules and technology. However, M1 is a good intermediate measure of the impact of the growth in the Fed's balance sheet as it feeds through the system.

Growth in MZM frequently results in financial asset expansion once it gains traction.

The US Dollar does not generally react well to aggressive growth in MZM.

The growth of credit, organic growth from economic activity, is sluggish.

The growth in the Monetary Base due to Fed inflationary activity has been nothing short of spectacular, without equal in US monetary history. This makes all Money Multiplier measures that use the AMB in the denominator meaningless for now.

The spike in Treasury settlement failures is one measure of the stress in the financial system. It seems to be quieter now, after spiking in response to seizures in the bonds trading. We will maintain a watch on this.

06 January 2009

Bill Poole: The Fed is Now Expanding Its Balance Sheet by Printing Money

We have long held Paul Volcker, William Poole and Jerry Jordan in high respect as former Fed governors. When they speak we listen, although Jerry seems to be more reticent, enjoying his retirement these days.

In a discussion with Kathleen Hays this afternoon during her "On the Economy" show on Bloomberg Television, Bill Poole took uncharacteristically sharp exception to the latest decisions by the Bernanke FOMC from their December Meeting minutes.

"The Fed is now expanding its balance sheet by printing money."

He was also visibly perturbed that the FOMC appears to no longer be stepping up to managing the money supply which is its mandate, but rather is allowing the Board of Governors to expand the money supply 'willy-nilly' with no eye to targets, just an uncoordinated roll out of special facilities.

For a minute we had to make sure this was Bill Poole speaking and not Willem Buiter, who delivered a round house commentary at Jackson Hole on the Bernanke Fed.

Yes, this is not the first time you have heard this, that the Fed is now printing money, monetizing the debt, especially if you are a regular reader here.

But it was unmistakable that in Bill Poole's mind the FOMC has now "crossed the Rubicon" and "will greatly regret their recent decisions in the future."

Jimmy Rogers has it right. "Bernanke’s going to keep printing money until they run out of trees."

The Fed is confident that they know how to stop inflation after the Volcker era, this much they have said, and it is clear they are acting on that belief.

A lot of theories are going to be road-tested, and the experiment in monetary and Keynesian economics will be rigorous.

This will be interesting, indeed.

Facilis descensus Averno;

Noctes atque dies patet atri ianua Ditis;

Sed revocare gradum superasque evadere ad auras,

Hoc opus, hic labor est.

Smooth is the descent, the way down below;

Day and night the gates of Hell stand wide open;

But to retrace your steps, and return to clear skies:

This is the task, this is the real work.

Vergil, Aeneid

03 January 2009

Chicago Fed Says Take Interest Rates "Below Zero" and Monetize Debt (to Devalue Dollar)

Quantitative easing to mimic interest rates 'below zero' effectively penalizes the buyers of US bonds and dollar savings by providing a negative rate of return after inflation.

Quantitative easing to mimic interest rates 'below zero' effectively penalizes the buyers of US bonds and dollar savings by providing a negative rate of return after inflation.

Inflation is desirable if you are a net debtor and you control the value of the method of your payment, ie. cheaper dollars to pay off service your debt.

We have to wonder how well negative real interest rates will support the enormous increase in the supply of Treasury debt that is coming to market this year because of a soaring national debt of about two trillion dollars.

The obvious target buyers are the exporting countries such as OPEC, Japan and China. We also suspect the Fed will start buying the yield curve, quietly and indirectly if not transparently.

Other central banks, such as Europe, will be expected to follow suit and devalue their own currencies through lower rates, to decrease the perceived impact of a dollar devaluation, in a group 'ratcheting down' of the developed nations' currencies.

This will require 'management' of the price of real things like commodities. Fortunately the price for most of them is set in London and New York. Life is tough for an exporting nation when you are riding the dollar reserve currency regime and an industrial policy of 'beggar your people' to support it.

The boundary constraint on the Fed in a purely fiat regime is the value of the US dollar and the Treasury debt. Greenspan's Fed managed to inflate its way out of the tech crash of 2000-2 with bubbles in equities and housing prices, a significant dollar devaluation, but an amazingly resilient bond thanks to official buying by a few foreign central banks.

Alan Greenspan famously stated, in a repudiation of his earlier views while responding to Congressman Ron Paul, that a fiat dollar as the reserve currency is viable because "the Federal Reserve does a good job of essentially mimicking a gold standard and...the Fed does not facilitate government expansion and deficit spending."

We expect to see Bernanke and the Congress test the limits of monetary and Keynesian economic theory again this year, and the acceptance of the US dollar and fiat currencies as a faux gold standard, as being of the utmost integrity and impartiality, immutable and nationless.

We tend to remain skeptical of the outcome however, keeping in mind the words of George Bernard Shaw, "You have a choice between the natural stability of gold and the honesty and intelligence of the members of government. And with all due respect for those gentlemen, I advise you, as long as the capitalist system lasts, vote for gold."

The major challenge for the governments of the world for the remainder of this decade, other than blowing us all to pieces, will be to create a viable alternative to the US dollar as the world's reserve currency and a major vehicle for international trade.

This could be one for the record books.

Reuters

Evans says Fed needs to mimic below-zero rates

By Ros Krasny

Sat Jan 3, 2009 8:18pm EST

SAN FRANCISCO (Reuters) - A grim economic outlook highlights the need for the Federal Reserve to step up quantitative measures to boost growth, with official interest rates already effectively at zero, Charles Evans, president of the Chicago Fed, said on Saturday.

Evans said that based on the outlook for rising unemployment, falling industrial production and a wider output gap, economic models suggest rates should be below zero. "If it were not constrained by zero, those models would want to push it below zero, but that's not possible," Evans told reporters after a panel at the American Economic Association's meeting in San Francisco.

"If it were not constrained by zero, those models would want to push it below zero, but that's not possible," Evans told reporters after a panel at the American Economic Association's meeting in San Francisco.

Quantitative easing, a way to flood the banking system with large amounts of money, "is a way to mimic below-zero rates and provide support to the economy," he said. (They would intend to create a monetary inflation to take the 'real rate' below zero. "Quantitative Easing" is Fedspeak for "printing money." - Jesse)

The process often involves buying up large quantities of assets from banks, such as the Fed's latest programs to buy mortgage-backed securities. (This is known as "monetizing debt." - Jesse)

In December, the Federal Open Market Committee, the Fed's policy-setting body, took the surprising step of lowering the federal funds rate to a range of zero to 0.25 percent. Cash fed funds had been trading below the previous 1 percent target rate for several weeks.

In his remarks, Evans, who is a voting member of the FOMC in 2009, said the Fed's various lending programs should help cushion the impact of the year-old U.S. recession but a large traditional fiscal stimulus plan is also needed, even with the problems it could create over the longer term.

"I believe a big stimulus is appropriate," Evans said. "But it is sobering to be deploying large amounts of taxpayer funds at a time when our fiscal balance sheet is already coming under significant stress."

Without the Fed's programs to help unfreeze credit markets and to-the-bone rate cuts, "the downturn -- and its costs to society -- would be even more severe than what we are currently facing," said Evans. Since the financial market crisis erupted, the Fed has created several new programs aimed at bypassing the traditional banking system and smashing through the credit-market logjam, including the direct purchase of mortgage-backed securities.

Since the financial market crisis erupted, the Fed has created several new programs aimed at bypassing the traditional banking system and smashing through the credit-market logjam, including the direct purchase of mortgage-backed securities.

Even so, the U.S. jobless rate appears on pace to exceed 8 percent in 2009, from the most recent reading of 6.7 percent in November, Evans said.

Although the current recession started with the collapse of the U.S. housing market, Evans said many non-financial industries now face the risk of "long-term structural impairment." (It was the Fed's reflationary effort after the Crash of 2000-2 that created the housing bubble. - Jesse)

Evans said fiscal programs to support growth "must be large in order to be effective and to instill badly needed confidence" given the severity of the downturn. (We have an intuition that the Congress will meaningfully explore the concept of 'large' government programs - Jesse)

President-elect Barack Obama has said that signing a major economic stimulus package will be his first priority when he takes office on January 20, with a goal of creating 3 million jobs over two years.

Evans also said the market crisis that erupted in 2007 showed huge holes in financial regulation.

"Significant weaknesses have been revealed in our system of financial regulation. ... These failures call for a reassessment of the roles of market discipline and our regulatory structures," he said

16 December 2008

Bernanke Unleashes the Power of the Monetary Force

The Fed will lead us out of deflation, but how many years will we spend in the wilderness?

The Fed will lead us out of deflation, but how many years will we spend in the wilderness?

Federal Reserve Open Market Committee

Release Date: December 16, 2008

For immediate release

The Federal Open Market Committee decided today to establish a target range for the federal funds rate of 0 to 1/4 percent. (That's it, we're effectively at ZERO - Jesse)

Since the Committee's last meeting, labor market conditions have deteriorated, and the available data indicate that consumer spending, business investment, and industrial production have declined. Financial markets remain quite strained and credit conditions tight. Overall, the outlook for economic activity has weakened further.

Meanwhile, inflationary pressures have diminished appreciably. In light of the declines in the prices of energy and other commodities and the weaker prospects for economic activity, the Committee expects inflation to moderate further in coming quarters.

The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. In particular, the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time. The focus of the Committee's policy going forward will be to support the functioning of financial markets and stimulate the economy through open market operations and other measures that sustain the size of the Federal Reserve's balance sheet at a high level. As previously announced, over the next few quarters the Federal Reserve will purchase large quantities of agency debt and mortgage-backed securities to provide support to the mortgage and housing markets, and it stands ready to expand its purchases of agency debt and mortgage-backed securities as conditions warrant. The Committee is also evaluating the potential benefits of purchasing longer-term Treasury securities.

The focus of the Committee's policy going forward will be to support the functioning of financial markets and stimulate the economy through open market operations and other measures that sustain the size of the Federal Reserve's balance sheet at a high level. As previously announced, over the next few quarters the Federal Reserve will purchase large quantities of agency debt and mortgage-backed securities to provide support to the mortgage and housing markets, and it stands ready to expand its purchases of agency debt and mortgage-backed securities as conditions warrant. The Committee is also evaluating the potential benefits of purchasing longer-term Treasury securities.

Early next year, the Federal Reserve will also implement the Term Asset-Backed Securities Loan Facility to facilitate the extension of credit to households and small businesses. The Federal Reserve will continue to consider ways of using its balance sheet to further support credit markets and economic activity. (TASLF for homes and businesses. Will that be a two-page form like TARP? Can I fill it out online? - Jesse)

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Christine M. Cumming; Elizabeth A. Duke; Richard W. Fisher; Donald L. Kohn; Randall S. Kroszner; Sandra Pianalto; Charles I. Plosser; Gary H. Stern; and Kevin M. Warsh. (Did Ben threaten them with martial law? Or just scare the hell out of them? - Jesse)

In a related action, the Board of Governors unanimously approved a 75-basis-point decrease in the discount rate to 1/2 percent. In taking this action, the Board approved the requests submitted by the Boards of Directors of the Federal Reserve Banks of New York, Cleveland, Richmond, Atlanta, Minneapolis, and San Francisco. The Board also established interest rates on required and excess reserve balances of 1/4 percent.

{kind=link}

{kind=link}