What, The Bucket Shop?

Are they truly delivering 'tonnes' of gold into markets where people actually take delivery of the bullion and withdraw it from the warehouse?

Stop the presses. Man bites dog.

Yes they seem to be. Just not in the United States.

The CME has opened a futures market in Hong Kong and from reading the documents and looking at the warehouse reports it appears to be a market of 'physical delivery.'

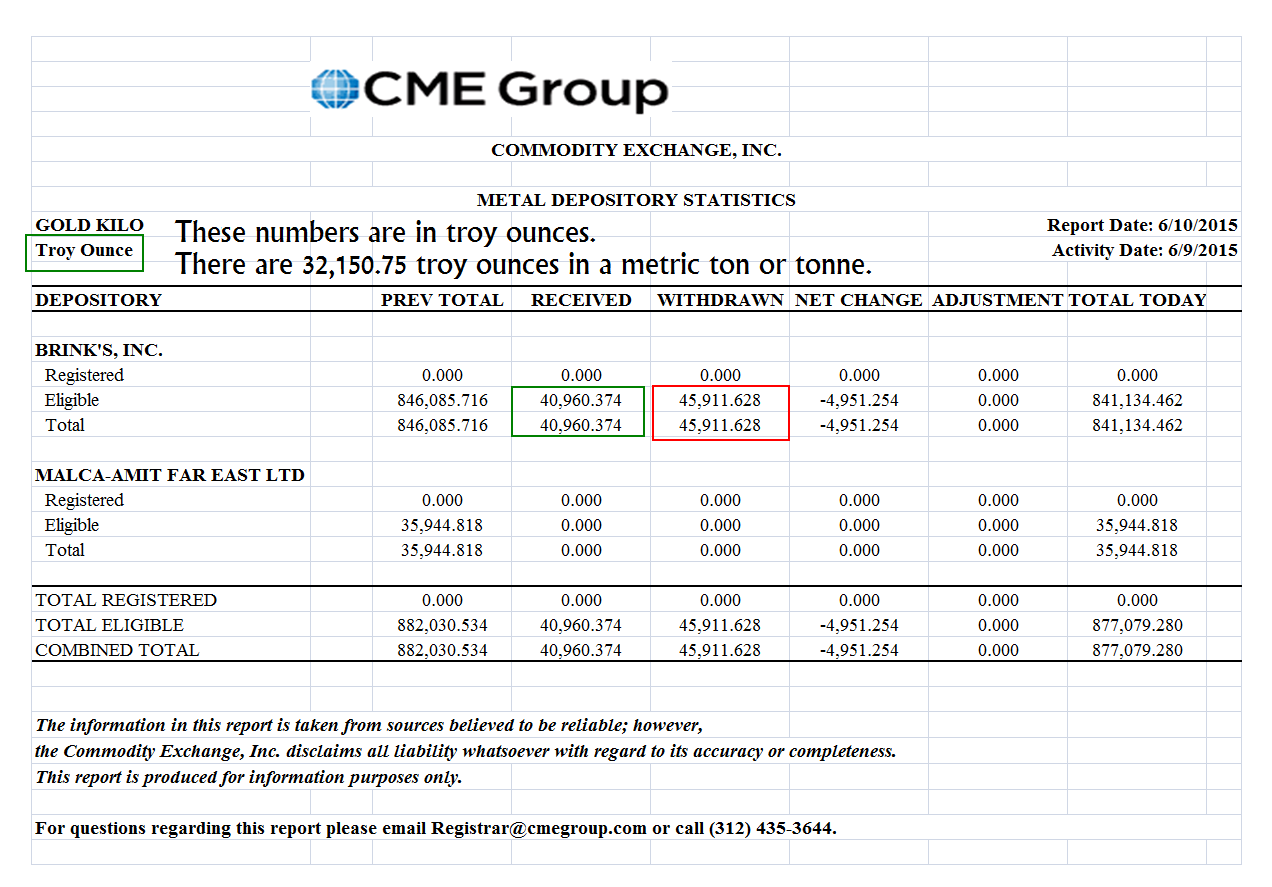

And are they ever delivering as you can see below. Since March they seem to have delivered 257 tonnes of gold bullion into Hong Kong.

I went over this a bit last night with Nick Laird, the Aussie data wrangler from near the Great Barrier Reef, who tends to ride herd on all things precious metals at Sharelynx.com.

Now there may be a hook in this somewhere. We would have to determine how easy it is to roundtrip the metal in and out, even if that does not seem to be the way they do their gold business in Asia. We do not know who is really playing on that exchange. It could be the usual suspects. Or it might be a new source of additional demand we must track into China.

But it certainly bears watching.