Rickards has a target of $2,000 for gold in the near term, and $5,000 for the intermediate term.

ECB has capitulated on the monetization of debt and joined the Fed, but it is hard to see how this will really solve the problem.

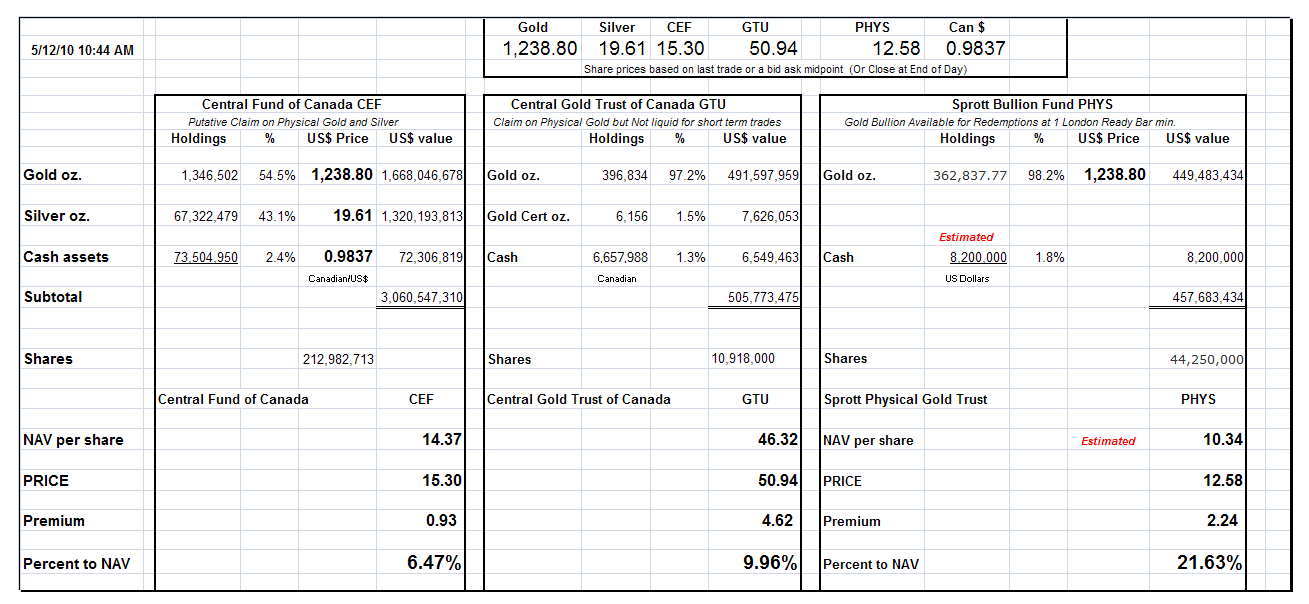

Europeans are running to buy physical bullion, rather than paper pledges in a kind of a 'run on the bank' over fears of the future of the Euro.

The subject of the meeting in Zurich yesterday was for the G20 to discuss the composition and role of SDR's as a reserve currency.

Triffin's dilemma: need for a 'liquidity pump' to drive world trade, someone who is able to sustain deficits without going broke. Now that the US is going broke, a new source of liquidity has to be found.

Rickard views SDR's as pure fiat on a pro rata basis. He does not see any accountability on the part of the IMF or any sort of external control.

While I see some of his points, I think Jim is confused about the notion that the SDR is a 'basket of currencies,' that already exist, unless they are changing the basis of the SDR to debt of their own issuance. I was not at all clear on this, and I would be a little surprised if that is the case.

What the IMF has been proposing with the support of the BRIC countries, is to put the SDR forward as a 'clearing mechanism' for international trade. They are also actively lobbying for a recomposition of the SDR to shift some of the monetary authority from the west to the east.

If the SDR is a 'basket of currencies,' each with their own debt balance sheet, and the SDR is not intended to replace or supplant domestic currencies, and especially if the SDR contains some element of gold and silver, then I view it as a natural development from the Bretton Woods system, and the failure of the US Federal Reserve to responsibly manage its currency 'like it was a gold standard.'

The IMF is attempting to replace the US dollar as the world's reserve currency with a portfolio of major fiat currencies, with the notion that the result will be more stable, more diversely based. Again, an element of gold and silver would further strengthen it.

I could be mistaken in what the IMF intends. But I have seen nothing to indicate that yet, and I think for now that Jim Rickards is mistaken in the assumptions underlying some of his statements.

IF the IMF decides to create a fiat currency of its own, and call it the SDR, and base it solely on its own balance sheet, with an arbitrary ability to expand and distribute it, then it really is the beginning of a new world order, and a one world government. But for now I do not see that to be the case. I can find no statement on the IMF homepage to this effect.

Why not go directly to a gold and silver standard? The greatest obstacle is that the Anglo American nations, or more properly their central banks and politicians, would not accept it. It would be inimical to their monetary power and financial engineering. The US Federal Reserve will not even agree to be audited by its own government! And do you think they would agree to the constraint of an external gold standard? This is a highly political as well as economic topic, and to ignore that is to completely misunderstand what is happening.

An evolutionary path to something less arbitrary than the dollar, but not quite as strict as gold, is most likely. This is being driven by China and Russia and the developing countries, and on the other side of the table are the Anglo-American banks, and to a less extent, Europe, after having been whipped into place by assaults on its monetary union.

It is an interesting interview. I only caution that more details need to be given from the IMF on what they are doing before conclusion can be drawn. I have been expecting this for a long time, and it is a development that the BRIC countries have been lobbying to obtain. The Anglo-Americans exert considerable influence over the IMF. This is a classic struggle for power between the old world powers and the developing world.

This is not to say that I am comfortable with the IMF. I have attempted to lay out the parameters to assess what they are doing with respect to a basket and clearing house versus a completely new global currency. Since the US and UK hold inordinate sway over the IMF, we have to be aware of the possibility that the IMF could merely become a much larger successor to the Federal Reserve, and owned and controlled by the Anglo-American banking interests. This is why gold and silver are the ultimate solution, and why the status quo will oppose them with all their power.

His follow on discussion of how hedge funds and financial institutions can attack a nation's currency using derivatives is very worth hearing.

Click here to listen to the Rickards Interview on King World News.