skip to main |

skip to sidebar

This seems mildly reminiscent of the setup which Soros and unnamed Swiss parties engaged in when they took down the Bank of England's defense of the British Pound and its official peg to the Euro.

Will the US ultimately feel compelled to defend some of the gold and silver shorts, both in terms of bullion and derivatives, held by its Wall Street Banks? You could allow for the possibility, if you will, that there is a corresponding web of derivatives that has a links, and a possible chokehold, on a few key European institutions, particularly in England and Germany, involving counterparty derivatives and CDS, and collateral damage to professional and political careers. Ugly stuff, rather messy really. But there are historic precedents.

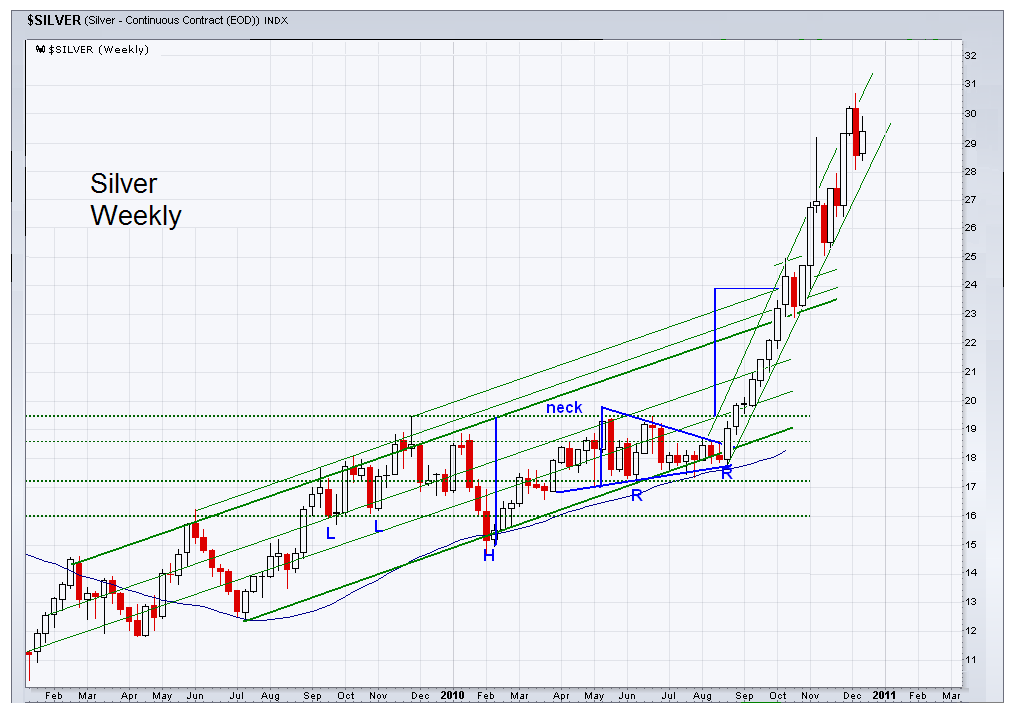

How Asian Buyers Are Maneuvering the Metals Shorts

There should be no confusion that this involves not only a few large Wall Street players, but also elements, past and present, in the US Treasury and the Federal Reserve. It makes the unfolding insider trading scandal look like a neighborhood numbers racket.

Therefore we should not discount the possibility that if a default should occur there will be an emotional and political reaction put forward as a means of deflecting the disclosure of the true nature of the financial corruption.

It would be most interesting and possibly entertaining to see if Ron Paul's congressional committee could be able to mount an effective investigation into the matter, or if events will take place to pre-empt and redirect such an inquiry to manage the potential collateral damage to careers and possibly governments, both at home and abroad.

It's never really the act itself, often minor infractions undertaken for practical purposes or what could be rationalized as such by some. Rather it is always the corruption of the policy actions to personal gain, and the subsequent cover-up, that tends to gather substance over time into a first class scandal, acts of felony and high crimes, and all the revelations that follow.

“Oh what a tangled web we weave, When first we practice to deceive." Sir Walter Scott

Non-event FOMC statement, the last of 2010, which is what had been expected. The macro retail sales picture was painted in high gloss, but the big miss by Best Buy cuts deeper to the heart of the truth.

The US is becoming two nations, one of privileged fraud and illusion, and another of harsh reality, difficult circumstances, and unnecessary hardship.

The first paragraph is the only thing that has changed and that from slow to insufficient. The Fed is dour on the jobless recovery and its self-sustainability.

"Information received since the Federal Open Market Committee met in September confirms that the pace of recovery in output and employment continues to be slow. Household spending is increasing gradually, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. Housing starts continue to be depressed. Longer-term inflation expectations have remained stable, but measures of underlying inflation have trended lower in recent quarters."

Contrast this opening paragraph from the Fed's November 3 Statement with their latest below.

Release Date: December 14, 2010

Federal Reserve Open Market Committee Statement

Information received since the Federal Open Market Committee met in November confirms that the economic recovery is continuing, though at a rate that has been insufficient to bring down unemployment. Household spending is increasing at a moderate pace, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. The housing sector continues to be depressed. Longer-term inflation expectations have remained stable, but measures of underlying inflation have continued to trend downward.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Currently, the unemployment rate is elevated, and measures of underlying inflation are somewhat low, relative to levels that the Committee judges to be consistent, over the longer run, with its dual mandate. Although the Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, progress toward its objectives has been disappointingly slow.

To promote a stronger pace of economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate, the Committee decided today to continue expanding its holdings of securities as announced in November. The Committee will maintain its existing policy of reinvesting principal payments from its securities holdings. In addition, the Committee intends to purchase $600 billion of longer-term Treasury securities by the end of the second quarter of 2011, a pace of about $75 billion per month. The Committee will regularly review the pace of its securities purchases and the overall size of the asset-purchase program in light of incoming information and will adjust the program as needed to best foster maximum employment and price stability.

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels for the federal funds rate for an extended period.

The Committee will continue to monitor the economic outlook and financial developments and will employ its policy tools as necessary to support the economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Sandra Pianalto; Sarah Bloom Raskin; Eric S. Rosengren; Daniel K. Tarullo; Kevin M. Warsh; and Janet L. Yellen.

Voting against the policy was Thomas M. Hoenig. In light of the improving economy, Mr. Hoenig was concerned that a continued high level of monetary accommodation would increase the risks of future economic and financial imbalances and, over time, would cause an increase in long-term inflation expectations that could destabilize the economy.

Well, it could be worse. He could be short silver, too.

S - A - V - E - - - M - E - - - B - E - N - N - N - n - n - n - n - n ...

"I listened to Kitco's Nadler on the Bloomberg channel this morning. He's been bearish on gold for months, and I thought he sounded like a know-nothing fool today. Why didn't Bloomberg interview someone who's been bullish and right about gold?"

Richard Russell