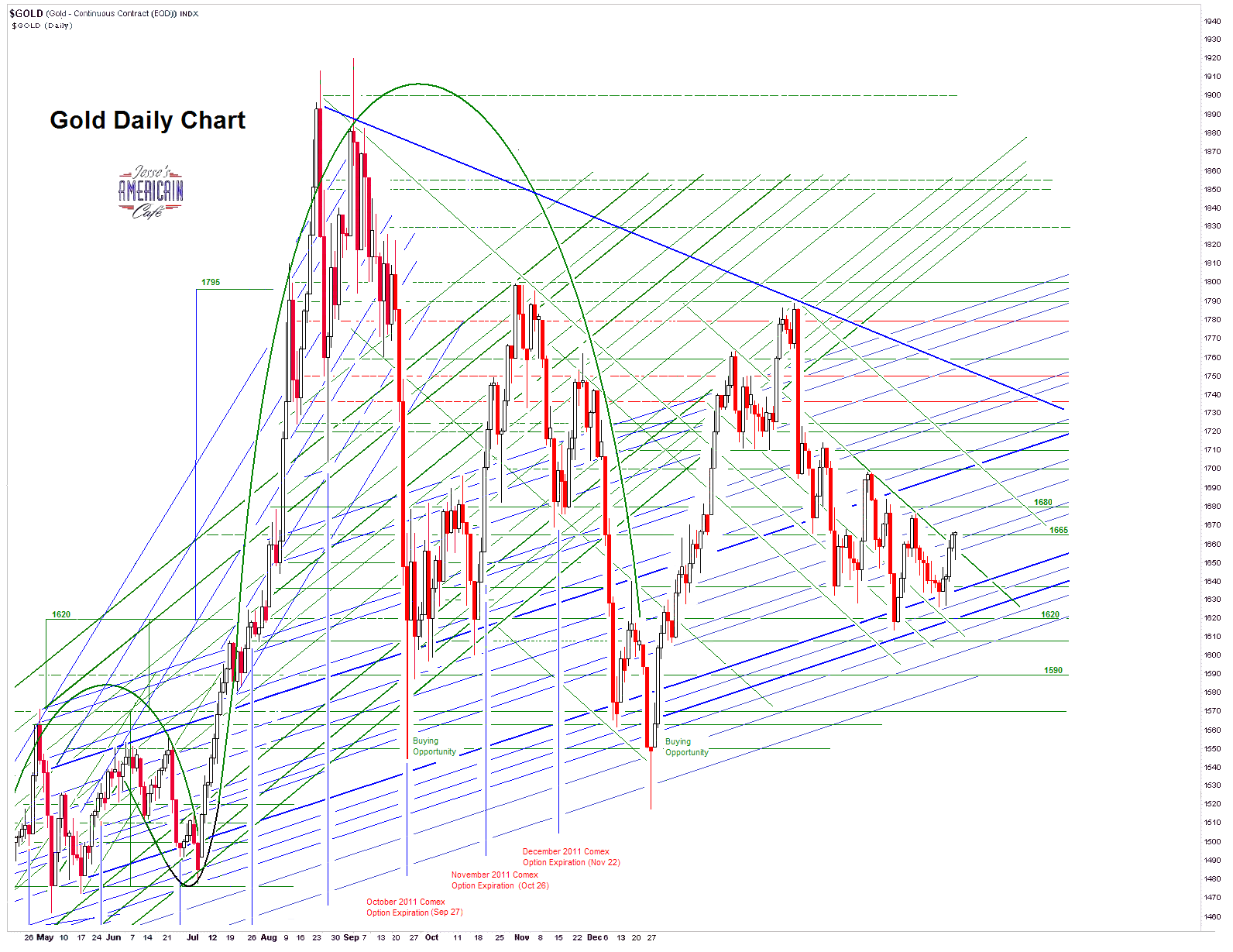

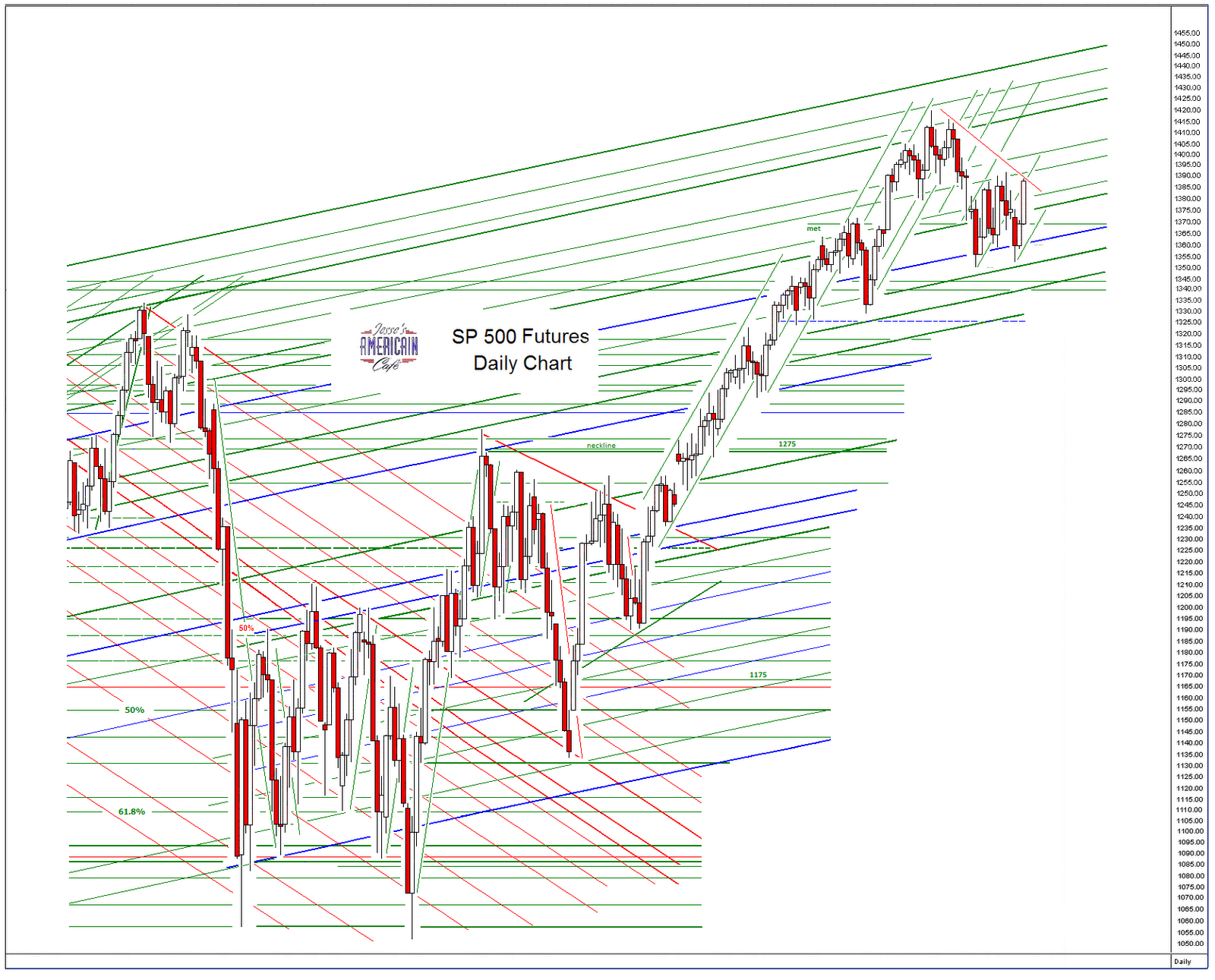

The fraud will continue until confidence is restored.

This is for my good friend Harold in Canada.

"You have accepted things you would not have accepted five years ago, a year ago, things that your father, even in Germany, could not have imagined. Suddenly it all comes to be, all at once. You see what you are, what you have done, or more accurately what you haven’t done. For that was all that was required of most of us: that we do nothing. You remember everything now, and your heart breaks. Too late. You are compromised beyond repair."

Milton Mayer, They Thought They Were Free

"...Vancouver resident Nina Rhodes-Hughes — a 78-year-old American-born television actress and a local theatre enthusiast in the city's Bowen Island community — was serving as a volunteer fundraiser for Kennedy's campaign when he was fatally shot in a kitchen pantry at the Ambassador Hotel on June 5, 1968.

He died from his wounds about 24 hours later, on June 6. Five others injured in the attack survived.

Rhodes-Hughes, after a Saturday interview with CNN sparked a worldwide resurgence of interest in the assassination, told Postmedia News on Monday that she heard at least 12 shots that day — not eight as argued by the California prosecutors who convicted Sirhan as the lone gunman.

The gun Sirhan had when he was arrested held only eight bullets.

"I gave them a true account of what happened," Rhodes-Hughes said of the FBI investigators who interviewed her following the Kennedy killing. "I had no idea what they were going to say I said. You trust, you know? But what I said about a second shooter was completely ignored."

Following Sirhan's conviction, Rhodes-Hughes said she felt she was "not in a position of power or influence" to raise questions about a single-killer theory. Then, years after she'd moved to British Columbia in 1987 and become a Canadian citizen, she was contacted by University of Massachusetts professor and freedom-of-information advocate Philip Melanson, who was writing a book raising questions about the RFK assassination — including various threads of evidence pointing to more than eight gunshots and a possible second assassin.

She recalls Melanson showing her a transcript of her 1968 interview with FBI detectives.

There were more than a dozen errors in the document, she said, "and they credited me with saying there were eight shots — which I never said."

Her eyewitness account of Kennedy's murder "was completely misconstrued and misrepresented," she added, vividly recalling details of where people were standing and what happened on the night of the assassination.

"There was no way that the shots coming from my right at such rapid fire were done by Sirhan Sirhan," said Rhodes-Hughes, who spoke with Postmedia News Monday.

Rhodes-Hughes said in her CNN interview that she believes Sirhan — 24 at the time of the assassination and now 68 — "was absolutely there" as a participant in the killing and "I don't feel he should be exonerated."

But she added on Monday that "there is a great urgency" to identify the second shooter, "who I believe was the one that hit Senator Kennedy..."

Read the rest here.

Cross Posted from The European

"Politics Is at the Root of the Problem"

The European: Four years after the beginning of the financial crisis, are you encouraged by the ways in which economists have tried to make sense of it, and by the ways in which those insights have been taken up by policy makers?

Stiglitz: Let me break this down in a slightly different way. Academic economists played a big role in causing the crisis. Their models were overly simplified, distorted, and left out the most important aspects. Those faulty models then encouraged policy-makers to believe that the markets would solve all the problems. Before the crisis, if I had been a narrow-minded economist, I would have been very pleased to see that academics had a big impact on policy. But unfortunately that was bad for the world. After the crisis, you would have hoped that the academic profession had changed and that policy-making had changed with it and would become more skeptical and cautious. You would have expected that after all the wrong predictions of the past, politics would have demanded from academics a rethinking of their theories. I am broadly disappointed on all accounts.

The European: Economists have seen the flaws of their models but have not worked to discard or improve them?

Stiglitz: Within academia, those who believed in free markets before the crisis still do so today. A few people have shifted, and I want to give credit to them for saying: “We were wrong. We underestimated this or that aspect of our models.” But for the most part, the response was different. Believers in the free market have not revised their beliefs.

The European: So let’s take a longer view. Do you think that the crisis will have an effect on future generations of economists and policy-makers, for example by changing the way that economic basics are taught?

Stiglitz: I think that change is really occurring with the young people. My young students overwhelmingly don’t understand how people could have believed in the old models. That is good. But on the other hand, many of them say that if you want to be an economist, you still have to deal with all the old guys who believe in their wrong theories, who teach those theories, and expect you to believe in them as well. So they choose not to go into those branches of economics. But where I have been even more disappointed is American policy-making. Ben Bernanke gives a speech and says something like, there was nothing wrong with economic theory, the problems were a few details in implementation. In fact, there was a lot wrong with economic theory and with the basic policy framework that was derived from theory. If your mindset is that nothing was wrong, you will not demand new models. That’s a big disappointment.

The European: There seemed to have been quite a bit of disagreement among Obama’s economic advisers about the right course of action. And in Europe, fundamental economic principles like the absolute focus on GDP growth have finally come under attack.

Stiglitz: Some American policy-makers have recognized the danger of “too big to fail,” but they are a minority. In Europe, things are a bit better on the rhetorical side. Influential economists like Derek Turner and Mervyn King have recognized that something is wrong. The Vickers Commission has thoughtfully re-examined economic policy. We have nothing like that in the United States. In Germany and France, the financial transactions tax and limits to executive compensation are on the table. Sarkozy says that capitalism hasn’t worked, Merkel says that we were saved by the European social model – and they are both conservative politicians! The bankers still don’t understand this, which explains why we still see the head of the European Central Bank, Mario Draghi, arguing that we have to give up the welfare system at a time when Merkel says the exact opposite: That the social model kept us going when the central banks failed to do their regulatory job and used politics to change the nature of our societies.

The European: How have your own convictions been affected by the crisis?

Stiglitz: I don’t think that there has been a fundamental change in my thinking. The crisis has reinforced certain things I said before and shown me how important they are. In 2003, I wrote about the risk of interdependence, where the collapse of one bank can bring about the collapse of other banks and increase the fragility of the banking system. I thought it was important, but the idea wasn’t picked up at the time. The same year we looked at agency problems in finance. Now we recognize just how important those issues are. I argued that the real issue in monetary economics is about credit, not money supply. Now everybody recognizes that the collapse of the credit system brought down the banks. (I don't agree, the collapse of the credit system was a symptom not a cause. It was the fraudulent paper, and the subsequent insolvency it promoted, that collapsed confidence which is the foundation of credit - Jesse) So the crisis really validated and reinforced several strands of theory that I had explored before. One topic that I now consider much more important than I did previously is the question of adjustment and the role of exchange rate systems like the Euro in preventing economic adjustment. A related issues is the linkage between structural adjustment and macroeconomic activity. The events of the crisis have really induced me to think more about them.

The European: The financial transaction tax seems to have died a political death in Europe. Now, economic policy in Europe seems largely dominated by the logic of austerity, and by forcing other European countries to become more like Germany.

Stiglitz: Austerity itself will almost surely be disastrous. It is leading to a double-dip recession that could be quite serious. It will probably make the Euro crisis worse. The short-term consequences are going to be very bad for Europe. But the broader issue is about the “German model.” There are many aspects to it – among them the social model – that allow Germany to weather a very big dip in GDP by offering high levels of social protection. The German model of vocational training is also very successful. But there are other characteristics that are not so good. Germany is an export economy, but that cannot be true for all countries. If some countries have export surpluses, they are forcing other countries to have export deficits. Germany has taken a policy that other countries cannot imitate and tried to apply it to Europe in a way that contributes to Europe’s problems. The fact that some aspects of the German model are good does not mean that all aspects can be applied across Europe.

The European: And it does not mean that economic growth satisfied the criteria of social fairness.

Stiglitz: Yes, so there is one other thing we have to take into account: What is happening to most citizens in a country? When you look at America, you have to concede that we have failed. Most Americans today are worse off than they were fifteen years ago. A full-time worker in the US is worse off today than he or she was 44 years ago. That is astounding – half a century of stagnation. The economic system is not delivering. It does not matter whether a few people at the top benefitted tremendously – when the majority of citizens are not better off, the economic system is not working. We also have to ask of the German system whether it has been delivering. I haven’t studied all the data, but my impression is no.

The European: What do you say to someone who argues thus: Demographic change and the end of the industrial age have made the welfare state financially unsustainable. We cannot expect to cut down on our debt without fundamentally reducing welfare costs in the long run.

Stiglitz: That is absurd. The question of social protection does not have to do with the structure of production. It has to do with social cohesion or solidarity. That is why I am also very critical of Draghi’s argument at the European Central Bank that social protection has to be undone. There are no grounds upon which to base that argument. The countries that are doing very well in Europe are the Scandinavian countries. Denmark is different from Sweden, Sweden is different from Norway – but they all have strong social protection and they are all growing. The argument that the response to the current crisis has to be a lessening of social protection is really an argument by the 1% to say: “We have to grab a bigger share of the pie.” But if the majority of people don’t benefit from the economic pie, the system is a failure. I don’t want to talk about GDP anymore, I want to talk about what is happening to most citizens.

The European: Has the political Left been able to articulate that criticism?

Stiglitz: Paul Krugman has been very strong on articulating criticism of the austerity arguments. The broader attack has been made, but I am not sure whether it has been fully heard. The critical question right now is how we grade economic systems. It hasn’t been fully articulated yet but I think we will win this one. Even the Right is beginning to agree that GDP is not a good measure of economic progress. The notion of the welfare of most citizens is almost a no-brainer. (Median is the message. - Jesse)

The European: It seems to me that much of the discussion is still about statistical measurements – if we’re not measuring GDP, we’re measuring something else, like happiness or income differences. But is there an element to these discussions that cannot be put in numerical terms – something about the values we implicitly bake into our economic system?

Stiglitz: In the long run, we ought to have those ethical discussions. But I am beginning from a much narrower base. We know that income doesn’t reflect many things we care about. But even with an imperfect indicator such as income, we should care about what happens to most citizens. It’s nice that Bill Gates is doing well. But if all the money went to Bill Gates, the system could not be graded as successful.

The European: If the political Left hasn’t been able to fully articulate that idea, has civil society been able to fill the gap?

Stiglitz: Yes, the Occupy movement has been very successful in bringing those ideas to the forefront of political discussion. I wrote an article for Vanity Fair in 2011 – “Of the 1%, by the 1%, for the 1%” – that really resonated with a lot of people because it spoke to our worries. Protests like the ones at Occupy Wall Street are only successful when they pick up on these shared concerns. There was one newspaper article that described the rough police tactics in Oakland. They interviewed many people, including police officers, who said: “I agree with the protesters.” If you ask about the message, the overwhelming response has been supportive, and the big concern has been that the Occupy movement hasn’t been effective enough in getting that message across.

The European: How do we move from talking about economic inequality to tangible change? As you said earlier, the theoretical recognition of economic problems has often not been translated into policy.

Stiglitz: If my forecast about the consequences of austerity is correct, you will see a new round of protest movements. We had a crisis in 2008. We are now in the fifth year of crisis, and we haven’t solved it. There’s not even a light at the end of the tunnel. When we come to that conclusion, the discourse will change.

The European: The situation needs to be really bad before it will get better?

Stiglitz: Yes, I fear.

The European: You recently wrote about the “irreversible decay” of the American Midwest. Is this crisis a sign that the US has begun an irreversible economic decline, even while we still regard the country as a potent political player?

Stiglitz: We are facing a very difficult transition from manufacturing to a service economy. We have failed to manage that transition smoothly. If we don’t correct that mistake, we will pay a very high price. Already, the average American is suffering from the failed transition. My concern is that we have set in motion an adverse economics and an adverse politics. A lot of American inequality is caused by rent-seeking: Monopolies, military spending, procurement, extractive industries, drugs. We have some economic sectors that are very good, but we also have a lot of parasites. The hopeful view is that the economy can grow if we rid ourselves of the parasites and focus on the productive sectors. But in any disease there is always the risk that the parasites will devour the healthy body parts. The jury is still out on that.

The European: Have we at least understood the disease well enough to prescribe the correct therapy? Especially with regard to policy-making and the Euro crisis, there seems to be a lot of shooting into the dark.

Stiglitz: I think the problem is not a lack of understanding by dispassionate social scientists. We know the basic dilemma, and we know the effect of campaign contributions on policy-makers. So we are facing a vicious circle: Because money matters in politics, that leads to outcomes in which money matters in society, which increases the role of money in politics. You have more gerrymandering and more disillusionment with parliamentary politics.

The European: Has politics become too focused on outcomes, and is it not sensitive enough to the processes that lead to those outcomes? The bedrock of democracy seems to hinge on the avenues for participation, not on the effectiveness of particular policies.

Stiglitz: Let me put it this way: Some people criticize by saying that we have become too focused on inequality and are not concerned enough about opportunity. But in the United States, we are also the country with the biggest inequality of opportunity. Most Americans understand that fraud political processes play in fraud outcomes. But we don’t know how to break into that system. Our Supreme Court was appointed by moneyed interests and – not surprisingly – concluded that moneyed interests had unrestricted influence on politics. In the short run, we are exacerbating the influence of money, with negative consequences for the economy and for society.

The European: Where is change rooted? In parliament? In academia? In the streets?

Stiglitz: You look in the streets and a little bit in academia as well. When I say that the major thrust of the economics profession has disappointed me, I need to qualify that statement. There have been groups that push new economic thinking and challenge the old models.

The European: You have written that the challenge is to respond to bad ideas not with rejection but with better ideas. Where is the longest and strongest lever to bring new economic thinking into the realm of policy?

Stiglitz: The diagnosis is that politics is at the root of the problem: That is where the rules of the game are made, that is where we decide on policies that favor the rich and that have allowed the financial sector to amass vast economic and political power. The first step has to be political reform: Change campaign finance laws. Make it easier for people to vote – in Australia, they even have compulsory voting. Address the problem of gerrymandering. Gerrymandering makes it so that your vote doesn’t count. If it does not count, you are leaving it to moneyed interests to push their own agenda. Change the filibuster, which turned from a barely used congressional tactic into a regular feature of politics. It disempowers Americans. Even if you have a majority vote, you cannot win.

The European: We’re looking at six months of presidential campaigning. The role of money has been embraced by both parties. Campaign finance reform seems rather unlikely.

Stiglitz: Even the Republicans have become more aware of the power of money by seeing how it influenced and distorted the primaries. The outcomes are not what the Republican party establishment had hoped for. The disaster is becoming clear – but that will not lead to immediate remedies. Those who become elected depend on that money. It will require a strong third party or civil society to do something about this.

"...The conservative social web has been freaking out this morning over a story from the Daily Caller who reported:

Rural kids, parents angry about Labor Dept. rule banning farm choresTwitchy even highlighted some of the knee-jerk reactionaries (I’m laughing with some of you) who took to Twitter to create the #ObamaFarmChores hashtag to mock the supposed impending doom of farm chores for boys and girls across America. Not that the kids would mind. Amiright?!

A proposal from the Obama administration to prevent children from doing farm chores has drawn plenty of criticism from rural-district members of Congress. But now it’s attracting barbs from farm kids themselves.

The Department of Labor is poised to put the finishing touches on a rule that would apply child-labor laws to children working on family farms, prohibiting them from performing a list of jobs on their own families’ land.

Read more: http://dailycaller.com/2012/04/25/rural-kids-parents-angry-about-labor-dept-rule-banning-farm-chores/

This Internet urban (or rural, in this case) myth is much ado about nothing. In the very US Labor Department proposal that the Daily Caller cited, the language is clear about this. From the 2nd paragraph of the US Labor Department proposal (my emphasis in bold):

The department is proposing updates based on the enforcement experiences of its Wage and Hour Division, recommendations made by the National Institute for Occupational Safety and Health, and a commitment to bring parity between the rules for young workers employed in agricultural jobs and the more stringent rules that apply to those employed in nonagricultural workplaces. The proposed regulations would not apply to children working on farms owned by their parents.Also, getting everyone in a tizzy is the rumor that 4-H would be eliminated under this proposal. Not true. From the US Labor Department site:

There are some portions of this US Labor proposal that do need some attention, but not the one being widely misreported. The lesson here: trust, but verify."Five Facts about the Proposed Child Labor in Agriculture Rule

Fact # 1: The proposed Child Labor in Agriculture rule will not prohibit all people under the age of 18 from working on a farm.

The proposed rule would not change any of the Fair Labor Standards Act’s minimum age standards for agricultural employment. Under the FLSA, the legal age to be employed on a farm without restrictions is 16. The FLSA also allows children between the ages of 12 and 15 years, under certain conditions, to be employed outside of school hours to perform nonhazardous jobs on farms. Children under the age of 12 may be employed with parental permission on very small farms to perform nonhazardous jobs outside of school hours.

Young people can be employed to perform many jobs on the farm – and this would be true even if the proposed rule were adopted as written. The proposed rule would, however, prohibit the employment of workers under the age of 18 in nonagricultural occupations in the farm-product raw materials wholesale trade industries. Prohibited establishments would include country grain elevators, grain elevators, grain bins, silos, feed lots, feed yards, stockyard, livestock exchanges, and livestock auctions not on a farm or used solely by a single farmer. What these locations have in common is that many workers, including children, have suffered occupational deaths or serious injuries working in these facilities over the last few years.

Fact # 2: The proposed rule would not eliminate the parental exemption for owners/operators of a family farm.

The parental exemption for the owner or operator of a farm is statutory and cannot be eliminated through the regulatory process. A child of any age may perform any job, even hazardous work, at any age at any time on a farm owned by his or her parent. A child of any age whose parent operates a farm may also perform any task, even hazardous jobs, on that farm but only outside of school hours. So for children working on farms that are registered as LLCs, but operated solely by their parents, the parental exemption would still apply.

Fact # 3: This proposed regulation will not eliminate 4-H and FFA programs.

The Department of Labor fully supports the important contributions both 4-H and the FFA make toward developing our children. The proposed rule would in no way prohibit a child from raising or caring for an animal in a non-employment situation — even if the animal were housed on a working farm — as long as he or she is not hired or “employed” to work with the animal. In such a situation, the child is not acting as an “employee” and is not governed by the child labor regulations. And there is nothing in the proposed rule that would prevent a child from being employed to work with animals other than in those specific situations identified in the proposal as particularly hazardous.

Fact # 4: Under the proposed rule, children will still be able to help neighbors in need of help.

In order for the child labor provisions of the FLSA to apply, there must first be an employer/employee relationship. The lone act of helping a neighbor round up loose cattle who have broken out of their fencing, for example, generally would not establish an employer/employee relationship.

Fact # 5: Children will still be able to take animals to the county fair or to market.

A child who raises and cares for his or her animal — for example, as part of a 4-H project — is not being employed by anyone, and thus is outside the coverage of the FLSA. Even if the child needs to rent space from a farm, the animal is not part of the farm’s business and with regard to the care of the animal no employer/employee relationship exists, so the child labor provisions would not apply. Likewise, there would be no problem with taking the animal to the county fair or to market, since the child is doing this on his/her own behalf – not on behalf of an employer. The proposed prohibitions would apply only if the child was an employee of the exchange or auction.

"Even in a time of elephantine vanity and greed, one never has to look far to see the campfires of gentle people.

Lacking any other purpose in life, it would be good enough to live for their sake."

Garrison Keillor

Finding the Culprits

Derivatives expert Janet Tavakoli takes a hard look at what — and who — caused the financial crisis.

By Jane Wollman Rusoff

...Now Tavakoli sees another huge financial crisis looming.

The University of Chicago MBA has traded, structured and sold derivatives at firms including Merrill Lynch, PaineWebber and Westdeutsche Landesbank; and she had earlier stints at Bear Stearns and Goldman Sachs. Research recently talked with her about red flags and preventive solutions.

You write that, in the past three years nothing has been fixed but that we must hold Wall Street responsible for the fraud that resulted in the financial crisis. What should be done?

We need to have investigations. But with the pushback and all the lobbying, what they’ve been counting on is that the statute of limitations for some of these frauds is expiring. So if you don’t file complaints, you may not be able to.

Members of Congress are enabling the lack of punishment and covering up great misdeeds in our financial system — and they’re doing it with no fear of consequences — i.e., being voted out of office, in which case they could find themselves the subject of investigation.

What do you mean: “covering up”?

Many people are covering up for cronies who have a lot of money sloshing around. We threw money into the financial system with no accountability and thus made the problem worse. Our system has been completely infiltrated and bought off. Things aren’t changing because Big Money doesn’t want it to change.

What other indications are there of a cover-up?

The MF Global dog-and-pony show. The attitude toward bundlers like Jon Corzine [the firm’s ex-CEO], who is a big bundler for the Obama campaign, is that the guy can do no wrong. This was before he even testified. People who are raising big money for campaigns get off with no real investigation.

In the Sarbanes-Oxley age, for MF Global to say they were unaware of what they were doing beggars belief. And yet there has been no indictment.

Is President Obama part of the cover-up?

Yes, in that he’s enabled it. He’s left people in place who crashed the global financial system in the first place: [Treasury Secretary] Tim Geithner and [Federal Reserve chair] Ben Bernanke. Obama had told us: “You can’t keep doing things the same way and expect different results.” So he’s been quite a hypocrite.

Who else is in the cover-up?

Mary Schapiro was appointed [by President Obama] to head the SEC. She was formerly head of FINRA, the antichrist of investor advocacy! Yet she was chosen SEC [chair] because the regulators are captive by and serve the people they’re supposed to be regulating. They do not serve investors.

In a way, Obama has been the anti-regulator because he didn’t put people in the regulatory agencies, the Fed or the Treasury who would investigate and fix things that are wrong in our global financial system.

If he’s re-elected, then presumably, things will continue in this same way?

Yes.

What if a Republican is elected President?

Who else is not in the pocket of Big Money interests! (Ron Paul - Jesse)

So, no matter who’s President, these crimes — if you want to call them crimes — will be perpetuated?

Yes. And we do want to call them crimes! They are crimes.

What should Obama do now to help Americans?

He has a lot of resources at his disposal, one main one being moral suasion — he’s got the pulpit. When there was a crisis, Reagan, Carter, Bush went on television and explained what needed to be done. We haven’t seen that kind of leadership from President Obama. If anything, the American people have been told things to make them think [conditions] aren’t really as bad as they are: inflation isn’t as bad as you think because an iPad is cheaper now — nonsense like that.

So the public is being poorly informed?

Yes. Therefore, financial advisors need to be doing fundamental analysis of investments and not [only] be reading the Wall Street Journal or, God forbid, watching CNBC. (Don't look for any appearances on CNBC or Bloomberg TV, Janet - Jesse)

In other words, FAs should do their own research and figure things out for themselves.

Yes. Sadly, you’re on your own. That’s part of how we got into this mess: We lost the art of rolling up our sleeves and looking for opportunities.

On Internet TV, you stated that we’re “absolutely vulnerable to a repeat [crisis] because the fraud went unpunished and we printed money like crazy to bail us out of the last one.” That’s scary.

But the fact is we’ve bailed people out and had no consequences for them. So it emboldened them to turn around and behave in the same way. Look at banks like JP Morgan: Shortly after the crisis, they thumbed their nose at the idea of trying to separate speculation from the rest of the bank. So if you don’t have restraints on behavior, you’ll see it repeated. And now we’ve made it worse. It’s like handing a drunk driver who got into a crash the keys to a bigger, faster car together with a bottle of vodka.

In every area of finance where we bailed people out, you see the same wrongdoers volunteering to help fix the situation. That’s pretty funny: They weren’t trustworthy before, and they’re not trustworthy now.

But what about the investigations that already have been held?

They’re all for show, and people end up with a slap on the wrist for minor issues. Investigators should be looking instead at the interconnected fraud that infected the mortgage lending market. And there is still a lot today, especially fraud on borrowers. If you go to the root of the problem and choke off the money supply, you stop the fraud in its tracks.

But the banks say they lost money.

The fact that a bank lost money isn’t an indication that they were a victim as opposed to being a perpetrator. A classic problem with control fraud is that the parasites destroy the host — in this case, the host being the bank and the parasites being the bank employees. If you were the victim of a control fraud by the people who worked in your own bank but meanwhile, you were collecting huge bonuses, you overlooked the control fraud within your own institution.

Why haven’t the apparently guilty been punished?

We haven’t seen the felony indictments that these people richly deserve because our regulators and investigators are captive — and Congress, more than ever, has been lobbied, courted and bought off by Wall Street. More than any time in the past, you’ve seen these big-money interests protected by Congress.

Is there an alternative to bailouts, such as those of the financial crisis?

Yes. Troubled financial entities should be restructured, old shareholders should be wiped out and we should return Glass-Steagall.

What should have been done in the case of, say, AIG?

Bankruptcy declared, and then [the government] says: “We’ll back-stop your contracts for now, but we’re going to investigate all those fraudulent credit derivative contracts and ‘claw’ money ‘back’ from your counterparties — like Goldman Sachs and Credit Suisse — if need be.” So there’s a controlled demolition. You’re not just handing money out with no consequences....

Read the rest here.

Alternet

MF Global: The Untold Story of the Biggest Wall Street Collapse Since Lehman

By Pam Martens

April 20, 2012

There are plenty of lessons to be learned from MF Global, all of which we can count on Congress to ignore at the behest of Wall Street money until the next financial crisis.

Only on Wall Street can you bankrupt a company; misplace $1.6 billion of customers’ money; lose 75 percent of shareholders’ money in two weeks; speed dial a high priced criminal attorney and get a court to authorize the payment of your multi-million dollar legal tab from the failed company’s insurance policies; have regulators waive your requirements to take licensing exams required to work in the securities and commodities industry; have your Board of Directors waive your loyalty to the firm; run a bucket shop out of the UK; and still have the word “Honorable” affixed to your name in a Congressional investigations hearing.

This is not a flashback to the rotting financial carcasses of 2008. This putrid saga has been playing out in five Congressional hearings since December with the next episode scheduled for Tuesday, April 24, before the Senate Banking Committee under the auspicious title: “The Collapse of MF Global: Lessons Learned and Policy Implications.” (The title might more appropriately be, “MF Global: Lessons Never Learned and Policy Implications of a Wild West Financial System Just One TradeAway from the Next Taxpayer Bailout.”)

There are plenty of lessons to be learned from MF Global and heart-pounding policy implications; all of which we can count on Congress to ignore at the behest of the Wall Street money and lobby machine until the next epic financial crisis – an eventuality that is growing more likely each day as Congress refuses to restore the Glass-Steagall Act, the depression era legislation that bars Wall Street securities firms from owning banks holding insured deposits...

Read the rest here.

PBS Frontline: Money, Power, and Wall Street

"The final $680 million or so was transferred to other financial institutions with which MF Global did business, including a substantial portion that went to JPMorgan. Giddens said his team has "a solid basis for seeking the recovery of some of the funds that were transferred to JPMorgan," and is engaged in ongoing talks on the issue."

CNN Money

$1.6 billion in missing MF Global funds traced

By James O'Toole

April 24, 2012: 6:49 PM ET

NEW YORK (CNNMoney) -- Investigators probing the collapse of bankrupt brokerage MF Global said Tuesday that they have located the $1.6 billion in customer money that had gone missing from the firm.

But just how much of those funds can be returned to the firm's clients, and who will be held responsible for their misappropriation, remains to be seen.

James Giddens, the trustee overseeing the liquidation of MF Global Inc, told the Senate Banking Committee on Tuesday that his team's analysis of how the money went missing "is substantially concluded."

"We can trace where the cash and securities in the firm went, and that we've done," Giddens said.

MF Global failed last year after its disclosure of billions of dollars worth of bets on risky European debt sparked a panic among investors. About $105 billion in cash left the firm in its last week, Giddens said, as clients withdrew their funds and trading partners called for increased margin payments, leaving the firm scrambling to make good on its obligations.

It has since emerged that MF Global tapped customer funds for its own use during this crisis and failed to replace them, in violation of industry rules.

Roughly $700 million of the missing money is now locked up with MF Global's subsidiary in the United Kingdom, where Giddens and his team are engaged in litigation to have it returned to U.S. customers. Giddens said he is "reasonably confident" that these funds will be recovered, though he added that it will be a lengthy process with no guarantee of success.

Another $220 million was transferred inadvertently from the accounts of securities customers to those of commodities customers. That money is now in limbo amid a dispute over which customers it belongs to, said Kent Jarrell, a spokesman for Giddens.

The final $680 million or so was transferred to other financial institutions with which MF Global did business, including a substantial portion that went to JPMorgan.

Giddens said his team has "a solid basis for seeking the recovery of some of the funds that were transferred to JPMorgan," and is engaged in ongoing talks on the issue. JPMorgan did not immediately return a request for comment....

Read the rest here.

"But please, to our friends in the Big Media, could we stop saying that we don't know the location of the missing $1.6 billion of client funds from MF Global? The money is safe and sound at JPM and other counterparties. As with Goldman Sachs et al and American International Group, the banks have been bailed out at the cost of somebody else. And the various agencies of the federal government are complicit in the fraud...

The effort by former New Jersey governor and MF Global CEO Jon Corzine to save his firm by stealing customer funds seems to warrant further discussion, yet instead we have silence...

So why is it that the Large Media have such trouble reporting this story? The fact seems to be that the political powers that be in Washington are protecting JPM CEO Jamie Dimon from a possible career ending kind of stumble with respect to MF Global."

Chris Whalen, Institutional Risk Analyst, February 2012

"I don't think this has any practical implications,” says David Rapach, associate professor of economics at St. Louis University. “This could be a combination of nostalgia toward both states' rights and the gold standard, but we moved away from those types of models for good reasons.”

Missouri's Sound Money Bill Is Really a Protest

By David Nicklaus

April 24, 2012

When the dreaded hyperinflation arrives, the Missouri House wants Missourians to be ready.

Last week, the legislative body passed the Missouri Sound Money Act of 2012, which declares U.S. gold and silver coins to be legal tender in the state.

That sounds a bit odd, especially since the federal government already recognizes its bullion coins as legal tender. It's just that nobody's going to pull out a $50 gold piece to pay for snacks at QuikTrip, because the ounce of gold in the coin is really worth $1,600.

Backers of the Sound Money Act envision a system in which you could deposit gold and silver coins in a vault and get a debit card tied to their metal value. If the Federal Reserve debases the value of the dollar – a favorite prediction among the gold-bug set – gold and silver would rise in value, and prescient Missourians could brag about their enhanced purchasing power.

Utah passed a legal-tender law last year, and South Carolina's legislature is considering one this year.

Rich Danker, economics director of conservative lobbying group American Principles in Action, said a couple of institutions in Utah are working to create the gold debit-card system. Until that's in place, sound-money advocates have to spend out of bank accounts denominated in dollars, just like the rest of us.

Missouri's legal-tender bill would benefit precious metals investors by eliminating state capital gains taxes on U.S.-minted coins. A fiscal note says the state treasury could lose more than $370,000 a year.

That's a small price to pay, backers argue, for monetary freedom....

Read the rest here: Missouri's Sound Money Bill Is Really a Protest - St. Louis Today