Stocks were pulling back to key support levels today.

Let's see what tomorrow brings.

"You have accepted things you would not have accepted five years ago, a year ago, things that your father, even in Germany, could not have imagined. Suddenly it all comes to be, all at once. You see what you are, what you have done, or more accurately what you haven’t done. For that was all that was required of most of us: that we do nothing. You remember everything now, and your heart breaks. Too late. You are compromised beyond repair."

Milton Mayer, They Thought They Were Free

"Central Fund's Gold and Silver Bullion is stored in the highest security rated treasury vaults at a Canadian chartered bank on an unencumbered, allocated and segregated basis."

“The tyrant is a child of Pride

Who drinks his sickening cup

Of recklessness and vanity,

Until from his heights he headlong

Plummets into the dust of hope.”

Sophocles, Oedipus Rex

"GLD Is Collapsing Its Shares And That Gold Is Being Shipped Directly To Asia"

By Tekoa Da Silver

August 9, 2013

I had the chance to reconnect with a source in the bullion management business, whose operations deal on a direct basis with the shipping desks at the GLD. While remaining unnamed at this time, it was a powerful conversation, and he was quite liberal in sharing thought.

Speaking to what his group is hearing from the main GLD custodian [HSBC], he noted that, “GLD is collapsing in [terms of] the number of share issuance, and [is] being redeemed…we are hearing from my end…that the GLD main custodian has been collapsing it and redeeming it, and that gold is just being shipped via their shipping desk directly to Asia.”

He further added that, “It is quite clearly a major establishment using their shipping desk to ship gold bullion, and potentially having it re-smelted down in Singapore, Hong Kong, etc. It (the gold) is moving.”

When asked his thoughts on the potential for a short-squeeze down the road as all this gold moves east, he concluded by saying, “Anything that can go down as hard as [gold] has, can obviously have a dramatic short squeeze at some time…at the end of this market [I expect] you will have a ridiculous squeeze.”

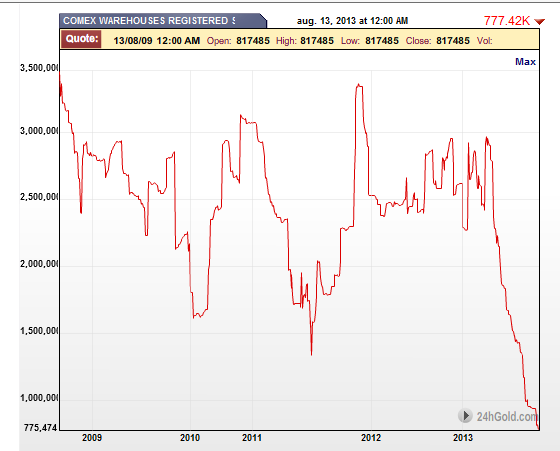

While much is left unanswered in the public domain regarding this year’s mysterious clearing out of physical gold from Comex warehouses, it would make sense for such events to occur right before a massive run-up in price—whether it be through freely traded markets or by governmental decree...

Read the entire article here.

"We looked into the abyss if the gold price rose further. A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake.

Therefore at any price, at any cost, the central banks had to quell the gold price, manage it."

Sir Eddie George, Bank of England, in private conversation, September 1999

"JPMorgan reported it is under investigation by the Justice Department in six separate areas; being pursued by multiple state attorneys general; Congress; at least five federal agencies; regulators around the world including the European Commission, the UK’s Financial Conduct Authority, the Canadian Competition Bureau, and the Swiss Competition Commission.Read the entire article by Pam Martens here.

In addition, in a trial in Italy, two of its employees were “found guilty of aggravated fraud with sanctions of prison sentences, fines and a ban from dealing with Italian public bodies for one year.” In the same matter, JPMorgan was fined €1 million and ordered to forfeit profit from the transaction of €24.7 million."

"Gottes Mühlen mahlen langsam,

mahlen aber trefflich klein

Ob aus Langmut er sich säumet,

bringt mit Schärf' er alles ein."

Friedrich von Logau