"You are the very cause of your ignorance, yourselves. You put away the light, yourselves; you first pluck out both your own eyes, yourselves; and after that other men’s too, so that the blind may lead the blind, until you both fall into the pit.”

Thomas More, The Sadness of Christ (Gethsemane), Tower of London, 1535

"The IMF has put Monetary gold right at the top of the global reserve assets list – above SDRs. The IMF writes, '…The gold bullion component of monetary gold is the only case of a financial asset with no counterpart liability.'"

Koos Jansen

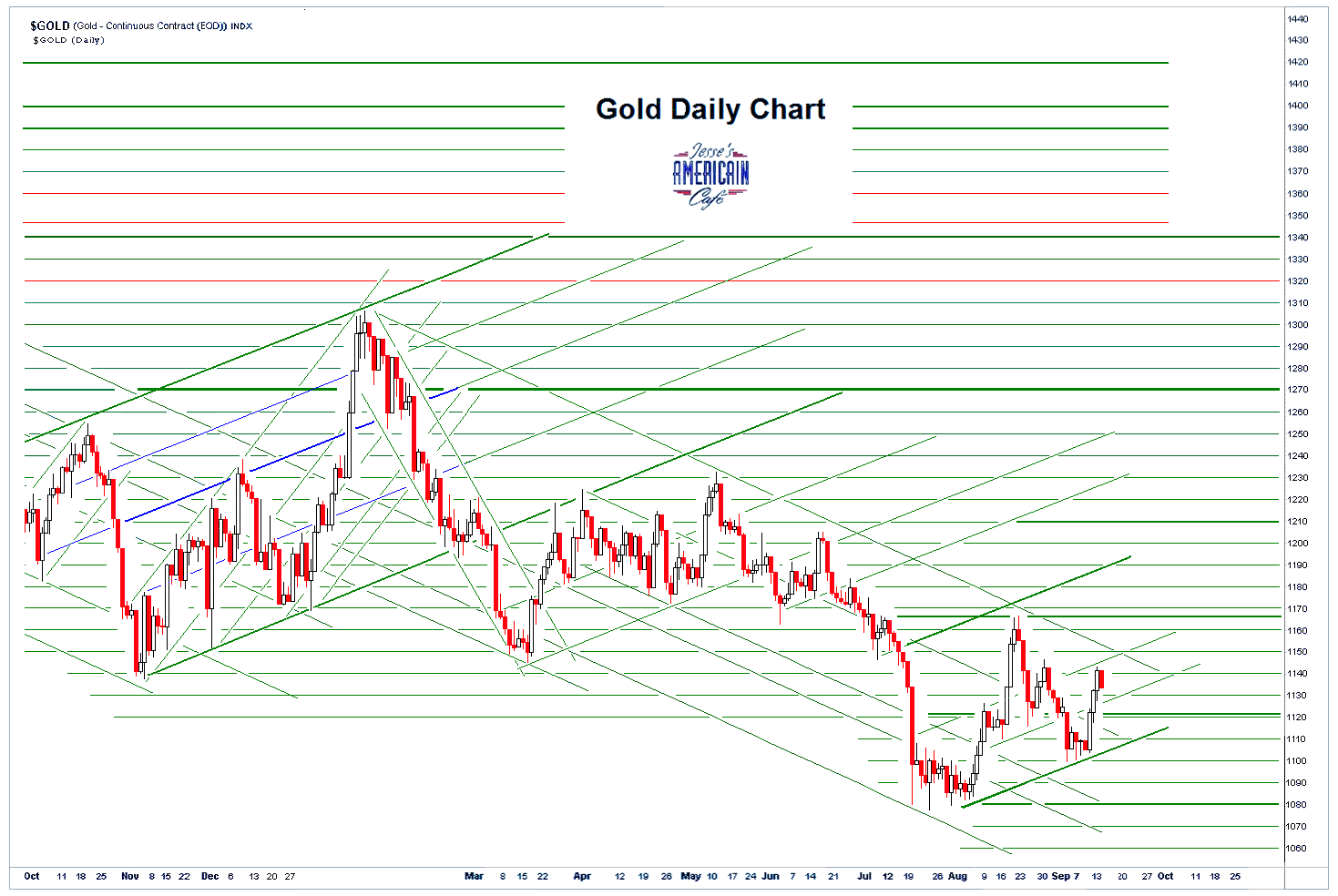

Gold took a light hit on the London PM fix and the opening of The Bucket Shop this morning. Silver took a hit as well but managed to bounce back up and finish positive on the day, probably because it is in an 'active month' at the betting parlor on the Hudson.

I read an analyst talking about the old 'gold vs. silver' argument over the weekend. In my opinion it is a fruitless argument to consider in the abstract, and so I don't.

Gold and silver are both precious metals, but have some not so subtle differences. Silver has a much higher beta, meaning it will go up more and down more than gold.

So if you can handle the volatility then silver is fine. If you would like less volatility and more 'insurance' then gold is more suitable. Gold has less of a component of industrial use than silver, but there is generally more free floating silver around than gold, and much of it is produced as a byproduct of mining base metals.

There is a place for both in any diversified precious metals portfolio. Arguing about the merits of one versus the other is like arguing about which is better, a screwdriver or a hammer. You have to consider the job at hand for yourself. And you can have a use for both of them.

I am personally persuaded by a growing amount of circumstantial evidence that there is a potential short squeeze developing in physical gold in London and New York, fueled by excessive paper trading and the insatiable demand in Asia.

It was electrifying last week when Jim Rickards said that the gold trade at the LBMA in London is wholly unallocated, and they hedge those positions on the Comex. I had thought it was a split trade at the least. If this is indeed the case, the public slipups admitting that the LBMA trade is running at 100:1 leverage implies that there is an enormous exposure to a shortfall of physical bullion for delivery and an unwinding of that leverage.

New York really trades overwhelmingly on a non-physical basis these days, so The Bucket Shop is more likely to be a late stage 'tell' and collateral damage than an actual precipitant of a short squeeze. And as a physical hedge it seems about as useful as fur coat in a flood.

London is the real Occidental bullion hub, and they tend to shroud their leverage and pricing antics behind a curtain of privileged secrecy. But London and Switzerland are the pivot points where the physical bullion of the West is flowing East.

Let's see how the bullion banks deal with this as we muddle on towards the final months of the year that are historically difficult for the gold pool.

Let's keep a close on the gold and silver markets in terms of physical supply, because that is the weak point of all late stage gold pool operations, or any pooling operation that deals in leverage.

I have kept myself aware as possible of the global gold bullion flows through Nick Laird of goldchartsrus.com. His site is an invaluable source of information.

There is clearly more work to be done as Koos has suggested, and I await Ronan Manly's final analysis. I hope that he is able to sort through enough of it to provide us some meaningful data.

What sort of efficient market arrives at price discovery by hiding the details of available supply?

In a nutshell there is an enormous demand for physical gold (and silver) in India, China, Russia and the Mideast. And it appears that, at least in the short term, the physical demand is running close to or even possibly outrunning the short term physical supply AT THESE PRICES. Should they allow the price to rise and free up more bullion for sale, or just keep increasing the leverage on the supply that they have?

Let's see how this works out. The central banks apparently bailed the gambling crowd out before from a tight squeeze when Sir Eddie George stared into the abyss, or at least there are indications to that effect. They may do so again, if they need to, and IF they can. Even the mighty central banks cannot make real gold out of their folly.

But you know what? I have come to believe that I can write about the market data all day long, and give people 'timely cautions,' and just a few will really notice or do anything. And the paperati apologists will keep spouting their nonsense, until the price of gold jumps $100 overnight and starts running to $2,000, and silver takes out $20. And then the markets and the greater mass of traders will begin to wake up.

Can you believe that the big tickle for stocks on financial television today was whether or not the Fed would raise rates at the next meeting?

OMG these jokers are so infantile I could just throw up.

Supposedly the Fed 'shocked' the market by doing nothing last week and so now traders are jittery that the economy is so bad that it cannot take a 25 basis point rate increase.

US equities were selling off today. The Fed's Bullard, a lone dissenter and a hawk, was telling everyone who asked for the Fed to restrain themselves to 'shut up' from the IMF to Larry Summers.

Dennis Lockhart, also of the Fed, came out and suggested that traders ought not to worry because the Fed will be raising rates sometime this year and so stocks took back some of their losses.

I cannot believe these idiots. This market is nuts, and the ruling class is gulping down their own Kool-Aid.

Yes, I believe that the economy is weak, and could be heading into a recession. And yes, I think the Fed can raise 25 basis points because their 'QE' is a trickle down policy error subsidizing asset bubbles and not improving much for the real economy, so they can rates just to quiet down the insatiable crying babies of Wall Street.

The real problem the US faces is an individual balance sheet recession, and the Fed and the government are doing almost NOTHING, not one thing, to help the individual person get back up on their feet. They are too busy enabled new ways for their wealthy friends and donors to cheat the public and skin them with fees, hidden expenses, growing monopolies, and substandard healthcare plans. And this is killing aggregate demand.

"The enormous gap between what US leaders do in the world and what Americans think their leaders are doing is one of the great propaganda accomplishments of the dominant political mythology."

Michael Parenti

Most economists and financial analysts think that 'currency war' merely refers to the competitive devaluations that nations sometimes engage in to help boost their domestic economies, as they had done in the 1930's for example.

This time the currency war is a much more profound confrontation of differing agendas revolving around the historically unusual role of the US dollar, based on nothing more than the will of the Federal Reserve and the 'full faith and credit' of the US, as the reserve currency for global central banks and international trade.

When a single nation begins to wield such an 'exorbitant privilege' to underwrite the speculative excesses of a crony capitalist banking system, and perhaps even more importantly, as an instrument in support of their international policy, one ought not be surprised that the rest of the world will begin to resist it.

A currency must be policy neutral, without regard to any party if it is to be a true medium of exchange. Can this still be said of the US Dollar as it has been managed, especially since 1990?

As Alan Greenspan once correctly pointed out, but certainly did not heed when he was at the Fed, if a fiat dollar is managed by monetary policy such that it emulates gold, then it will be perceived as fair, and will certainly be above the particular domestic issues or international policy biases of a single nation that de facto wields the reserve currency status.

"And so it is an odd situation where all the central bankers -- while none of them are advocating a return to the gold standard -- nonetheless try to replicate the various types of interest rate policies that the gold standard would have created. And it is an interesting question whether you call that regulation, or basically functioning of a central bank in stabilizing the economy."

It might help one to understand this if they were to imagine a world in which Russia, for example, in a quirk of history had established the ruble as the benchmark currency for the world. The ruble was recommended for use by all nations as the means of paying for oil, and for settling international trade even when Russia is not involved in the transaction. Each country was thereby compelled to hold a substantial portion of its international reserves in rubles.

And how would one be likely to react if the Russian Central Bank started using the ruble as an instrument of their international policy and extension of their quest for imperial power? What if they began creating more rubles to underwrite the domestic bubbles which were created in their own corrupted financial system to bail out their banks and oligarchs?

And let's be serious and think 'like the other guys' for a moment. What if some other nation that held the enormous power of the world's reserve currency was exhibiting a crop of candidates for their leader like the current choices for the US Presidency? I would expect that some of the rhetoric being tossed about in these debates would send a chill to the very bottom of our toes. Who could place their confident trust in their good and selflessly wise judgement to do the right things for other nations around the world, even if it might not favor the powerful special interests that give them so many millions in campaign donations?

Would you be content if your own government went quietly along with this abusive sort of monetary system? Is this not indeed taxation without representation when the money supply is expanded and handed over directly to the hands of a few Bankers?

The intransigence of the Anglo-American financial establishment to recognize the legitimate issues of the rest of the world with regards to the manner in which they have conducted their control of the IMF, the World Bank, and the international reserve currency has ignited a currency war that is now becoming increasing visible, to just about everyone it seems except for those sequestered in their ivory towers at the heart of the Empire. Or perhaps they think it too dangerous to even acknowledge that it exists, because then they might be compelled to render an opinion on it.

This is a 'big event' and it is all the more remarkable because the policy makers in the US act as though it is not even happening, or is not happening for any of the reasons for which it is. They prefer to view it as a challenge to their authority, and to react uncompromisingly and with force.

I think that historians will find the start of the currency war in the Asian currency crises and the fall of the Russian ruble in the 1990's, with the roots of it in the closing of the gold window by Nixon in 1971. But from the following essay it seems that China and a few astute Western observers have marked it as being visible from March 2015.

But whatever the date of its commencement, this dispute over the international monetary regime is the basis for the ongoing currency war that seeks to rebalance the terms of international trade and finance.

It is the old story of the very powerful resisting change that benefits the few of them inordinately. And as in so many wars of the past, those few who benefit from it do not include the bottom 90% of their own people at the least.

Most economists and analysts are ignoring this, or are unaware of it. When they do finally wake up they will likely get busy finding ways to justify it, or dismiss it as an issue, and 'prove' that there is nothing wrong with it. And very few will acknowledge the price of it in terms of economic stagnation and human misery. All is well.

Here is an excerpt of a recent article that was published in Chinese and then translated into English in the journal of the International Monetary Institute in Beijing. (It is a little funny that they published his last name as Widdlekoop, but if you were writing in hanzi would you know if a similar looking character is upside down?)

Has the US Lost its Role as the Underwriter of the Economic System?

By Willem Middlekoop

The recent news that Britain aspires to become one of the founding members of the new Asian Infrastructure Investment Bank (AIIB), has shocked many. Larry Summers, who served as a Secretary of the US Treasury between 1999 and 2001, immediately understood the significance of these developments, and wrote in an op-ed for the Washington Post: 'March 2015 may be remembered as the moment the United States lost its role as the underwriter of the global economic system. I can think of no event since Bretton Woods comparable to the combination of China's effort to establish a major new institution and the failure of the United States to persuade dozens of its traditional allies, starting with Britain, to stay out.‘

This British announcement was highly criticized by the US. The Financial Times quoted an unnamed US official: 'We are wary about a trend toward constant accommodation of China, which is not the best way to engage a rising power. This decision was taken after no consultation with the US.‘

Summers was also highly critical of the US‘ strategy toward the newly founded AIIB: 'The U.S. misjudged the situation tremendously, put pressure on allies and developing countries to under no circumstances be part of AIIB. Largely because of resistance from the right (neo-conservatives more precisely), the United States stands alone in the world in failing to approve International Monetary Fund governance reforms that Washington itself pushed for in 2009. By supplementing IMF resources, this change would have bolstered confidence in the global economy. More important, it would come closer to giving countries such as China and India a share of IMF votes commensurate with their increased economic heft.‘

With Britain and many more major European countries signing up as founding members of the AIIB, the US economic hegemony has been dealt an enormous blow. For the first time since the end of the Second World War, the US is not in the driving seat during the foundation of a highly significant global institution. Of course, this will not change the world economic system overnight, but when we look back in five, ten or even fifteen years‘ time, March 2015 may be remembered as a turning point in economic history...

Another criticism is that the US move to more neoliberalism and global capitalism since the 1980‘s, has led to a change in the functions of the IMF. Critics claim allies of the US receive 'bigger loans with fewer conditions‘. Foreign governments who are non-allies have to sacrifice their political autonomy in exchange for IMF-funds and often have to sell assets crucial for their economy to foreign (often US) companies.

The former Tanzanian President Julius Nyerere, who was angered that debt-ridden African states were forced to hand over their sovereignty to the IMF (and World Bank), once asked: 'Who elected the IMF to be the ministry of finance for every country in the world?‘ And now the Chinese have openly asked for a 'new world wide central bank‘.

Joseph Stiglitz, a former chief economist at the World Bank, has also agreed that the IMF 'was reflecting the interests and ideology of the Western financial community‘. The 'helpful hand‘ by the IMF and World Bank towards military dictatorships friendly to the West‘ has been criticized as well.

It might be remembered as the start of an openly Chinese confrontation with the US over the world‘s economic leadership. As Summers points out, all of this has taken place because the Chinese leadership has had to wait a full five years for a change in the IMF-voting structure...

Gold and silver continued to rally today, even as the Dollar took back quite a bit of its recent loss after the Fed did what everyone expected them to do, which is nothing. Keep in mind that the Dollar DX index is antiquated, and potentially misleading since it is so heavily weighted to the old order currencies.

Currencies are under closer examination now, because we are in a period of change that some have called 'the currency wars.' Sometimes analysts will narrow that definition down to just the competitive devaluations that governments engage in to help to boost exports and curb imports to their faltering domestic economies.

But it is much more than that. They are missing the bigger picture because it is the kind of change that occurs over long periods of time. One day they will look up and see it, and surprise. Who could have seen it coming?

Gold is the king of currencies, the crème de la crème of monetary vehicles. If you have an ancient gold coin now, even if it is not of collectible merit, its value is still sustained as bullion after all these years, no matter what country or ruler may have happened to have issued it. And the same is true for silver.

That is because physical precious metals have no counterparty risk. No paper currency may make that claim, since they exist on either the strength of a promise, or the force of a threat. And as the promises erode, the application of force often increases.

It is the international force of wills that is causing the currency wars. Some wish to uphold the existing regime, the dollar as the reserve currency, whether it makes sense or not. That is because money is power. There is little that is noble in this effort. It is the greed of the merchants and the will to power that they serve. And the rest of the world has grown weary of it.

Others would aspire to grow the power of the Anglo-American empire at any cost, most of it to be paid by other people. It is an old story, one of the oldest. Pride and the will to power, and from them spring jealousy and greed. Enough is never enough for some.

There was overnight commentary about gold, and some recent controversy about the supplies of gold in London and New York. You might take the time to read Deriding the Theory of Gold Tightness at the Comex.

What goes around comes around. And what is coming around the corner may be enlightening.

Today was a quad witching day on the equity markets.

Stocks continued to sell off on disappointment that the Fed did exactly what everyone thought that they would do.

I think with the options expiration the punters got caught offsides, and the sharks who have the advantage of a much clearer vision of who has what in their hands were determined to take the markets down no matter what the Fed would have done.

After all it's a quad witch, and the smaller fish were schooling in the options and ETFs.

“Our clients will call up saying ‘I hear the Comex is running out of gold, what do you make of it?’ and our quick answer is that this is a non-issue,” Jeffrey Christian, managing director at CPM Group, said in a telephone interview.

“Even if you look at the fact that registered stocks have declined, the fact of the matter is most Comex futures contracts” are cash-settled, and traders don’t take delivery of the metal, he said.

While the percentage of Comex gold open interest covered by total Comex reported stocks has fallen over the past year and a half, it “remains very high by historical standards and presents no perceptible risk of imminent problems with deliveries,” CPM Group said in a report dated Sept. 14...

Barclays Plc said in a report this week that emerging-market demand for gold has shifted some metal into Asia, and that “coverage of physical stocks in Comex remains solid.”

“Anything that has more upside than downside from random events (or certain shocks) is antifragile; the reverse is fragile.”

Nassim Taleb, Antifragile

Gold is anti-fragile. This is why it must be handled with care, and not with fragile systems. Gold is intractable to the kinds of manipulation by the financial system that can bend paper to its will. This is why they hate gold, and seek to paper over it with leverage and secrecy.

Above is a commentary on the physical bullion situation at the Comex as it was reported at Bloomberg News yesterday. The 'deriding', which means ridicule and contempt, is coming from CPM group's Jeff Christian, and from a report from Barclays.

The title of the article is a bit odd, because I have not see any 'theories' about this subject at least here, just presentations of the facts using exchange provided information. And as for deriding, it seems more like a sign of weakness and fear than solid reassurance. But that is just my own experience in seeing that sort of thing when someone points out a changing situation that could pose a problem.

One thing the story fails to make clear is that only registered gold is deemed deliverable to fulfill futures contracts. Yes, all the gold in all the warehouses could potentially satisfy demand, IF IT WAS UP FOR SALE. But it is not.

The total supplies at the Comex have as much to do with the current demand for bullion as all the automobiles in your neighborhood have on the price that you are going to pay tomorrow for a used car, eg. the calculation cannot include items that are not up for sale. Yes there are many cars that would satisfy your requirements. But only those that are for sale are available for you to drive home.

Jeff Christian says that "even if you look at the fact that registered stocks have declined..."

Yes, 'even if' you look at the heart of the argument, 'registered stocks have declined,' and that is quite the understatement of the facts.

Here is the history of 'registered gold bullion' on the Comex going back to 2001.

And of course if almost no one asks for any of the gold, then there is no problem. Yep.

This is the problem. For anything except speculating with paper the Comex is now significantly fragile, moreso than at any time it has been in the last twenty years at least.

Jeff goes on to say that "most Comex futures contracts” are cash-settled, and traders don’t take delivery of the metal,"

And that is correct. Here is the history of deliveries, ignoring any cash settlements, on the exchange.

As should be easy to see, the amount of gold bullion deliveries is declining quite a bit.

The Comex lacks the market discipline of delivery of the goods and restraint on the potential hypothecation of available supply. What is acting to hold leverage to some reasonable level other than 'nothing has broken yet.'

Let's take a quick look at the ratio of total contracts to registered gold, that is gold up for sale.

The Comex is a significant price discovery market for the global gold supply. The data shows that it has diverged significantly from the physical bullion markets primarily in Asia.

While the inventories at the Comex remain flat overall and declining sharply with regard to deliverable bullion, the physical deliveries of gold into India and China are increasing steadily.

And I hasten to remind everyone that gold is truly a global market.

Nick Laird at sharelynx.com has created chart that tracks the known physical gold demand for what he calls 'The Silk Road.'

Even though I do not expect a default at Comex, as I have said many times before, the point is that if there is even a mild problem in one of the physical markets in Asia or London, the Comex is price positioned for a market dislocation and potential fails to deliver bullion on request.

The deliverable gold is a little under 6 tonnes. But even if price were no object, the total gold held in private hands in all the Comex warehouses is about 6,716,000 troy ounces, or roughly 209 tonnes. That is all of it no matter who owns it or why.

Or less than one month's supply for the Silk Road countries.

Normally none of this *should* be problem, although one has to admit that according to historical norms the amount of deliverable gold is very thin by any measure. Why is this? Why are the better informed withdrawing their bullion from the deliverable category? I read that they are afraid of the bullion being caught in a 'short squeeze,' but the trader who said that did not specify a short squeeze where.

This week I learned from an interview with Jim Rickards that some very large bullion banks were said to be using the Comex gold futures to hedge shorts in bullion delivery markets in London, called the LBMA.

That kind of a hedge might work to guard against paper losses, but against a genuine fail to deliver in a physical market you can see that the immediate deliverables at these prices are about 6 tonnes, which is a rounding error on the Silk Road.

It's the fragility, always the fragility.

What if something that is not completely normal and expected happens? What if, instead of 2% of the contracts asking for delivery, a delivery short squeeze in London prompts 4 or 5 percent of the contract holders to attempt to exercise their contracts to receive physical bullion to cover their obligations elsewhere?

The fragility of such an arrangement is bothersome to anyone from outside who looks at it from a systems engineering perspective.

If some firms are using the Comex as a backup system for gold deliveries in London and points east, it is hardly equipped to take that role without a significant market dislocation in price.

If I was only working short term trades and would never mind a settlement in cash, then the Comex seems like a fine place to do the trade.

However, if my goal is to have a solid claim on physical bullion, even within some reasonable length of time measured in several months, it does not appear that the Comex is appropriate for that particular objective.

Do you see the potential problem here that is so blithely 'derided?'

I do not wish to alarm anyone. I am putting out the word because I do not think people understand the situation that has developed, over the past two years in particular, as shown by the potential claims per ounce.

Globally huge market with increasing demand, a market where the available inventories are exceptionally thin, and a price that is derived without a tight rein on leverage and the discipline of delivery. What could possibly go wrong?

The usual retort is 'it has not broken yet.' Yes, and in the light of our experience over the past ten years or so, some might find rather thin comfort in that. The important thing is for traders and investors to be fully informed, that they may use financial instrument in a manner that is appropriate to their objectives.

For example, using Comex as a backup for bullion positions on the LBMA might be fine, if you are not expecting to receive delivery of bullion that can be used to satisfy your obligations there.

The exchange might consider another look at their rules in the light of this unusual 'leverage' of potential claims to bullion, rather than count on price fixing all problems, and few standing for delivery, especially in a changing and very dynamic global market.

I do not have good visibility into the leverage and available inventories at the LBMA in London. If those are in any way similar to the Comex, then I would take some action fairly quickly to secure my ownership of bullion given the potential for a misstep that spins out of bounds.

If you hold an allocated receipt that is as 'good as gold?' Tell that to the investors who used MF Global, and found their holdings sorted out in court against a lawyered up megabank.

I do not know Jeff Christian or the fellow from Barclays. I am sure that they have good reasons for what they are saying and the advice they appear to be giving to their customers. I am sure they can all work out all their concerns and particular issues among themselves.

Objectives amongst customers do vary and it is the fiduciary duty of any advisor to help them make an appropriate choice. And I can see many uses for Comex positions that are entirely suitable for some. A short term trader for instance, who in merely placing wagers that he expects to settle for cash.

But as for this article in Bloomberg, it is a bit of a gloss, heavier on the deriding and short on information for readers to use in making their own informed decisions. 'Trust us' and 'nothing has broken yet' are, as I said previously, non-starters these days.

I have set forth only a few of the oddities that are becoming apparent in the gold market. There are quite a few more, including backwardation and tightness in the London physical market as noted by Peter Hambro and an analyst at Mitsubishi recently, and in articles by Koos Jansen and Ronan Manly.

How about the pivotal London market, is it 'well-supplied?' How well supplied is it? What is the potential impact on the Comex of a bullion shortfall at the LBMA?

Has there ever been a 'stress test' of what it would be like at the Comex if there were an afternoon failure to deliver physical bullion in London? Or are you assuming as your baseline that such a shortfall could never happen in any non-Comex market? Is the process at Comex for some event like that, besides halting the exchange and forcing cash settlements?

I do think that one can become so involved in a system, for so long a period, that when it changes, when the market dynamics start shifting, the old hands may be the last to notice the forest for all those familiar trees. That is why companies bring in quality teams to inspect their processes for soundness and failure points.

What could have possibly changed in the global gold market in the past few years. "Barclays Plc said in a report this week that emerging-market demand for gold has shifted some metal into Asia,"

How about this? Some shift. Some metal.

Here is what Kyle Bass recently had to say about the situation. Maybe you can 'deride' him. Then again, maybe not.

Let us pray for those whose hearts are hardened against His grace and loving kindness by greed, fear, and pride, and the seductive illusion and crushing isolation of evil.

We pray that we all may experience the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness. And in so doing, may we obtain abundant life, and with it the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.