"Peace cannot be understood as the forced silence of the people. Ideologies based on lies and violence collapse; they bear evil fruit and moral devastation. It is not enough for a Christian merely to condemn evil, lies, cowardice, enslavement, hatred, and violence. A Christian must be a true witness, spokesman, and defender of justice, goodness, truth, freedom, and love. He must courageously demand these values for himself and for others." Jerzy Populesko, Solidarność, May 27, 1984

“When Fascism came into power, most people were unprepared, both theoretically and practically. They were unable to believe that man could exhibit such propensities for evil, such lust for power, such disregard for the rights of the weak, or such yearning for submission. Only a few had been aware of the rumbling of the volcano preceding the outbreak.”

Erich Fromm, Escape from Freedom

"I understand why an equality that was founded upon God involved neither contradiction nor disorder. Demagogy enters at the moment when, for want of a common denominator, the principle of equality degenerates into the principle of identity."

Antoine de Saint-Exupéry, Flight to Arras

"Fascism begins the moment a ruling class, fearing the people may use their political democracy to gain economic democracy, begins to destroy political democracy in order to retain its power of exploitation and special privilege."

Thomas Clement Douglas

As you know today was a quad witch in stocks, and shenanigans were expected to be at a high level.

Stocks traded wobbly most of the morning and Europe closed for the weekend quietly.

But around one stocks started dropping precipitously. I happened to be watching the stock futures and noticed the sharp change in trading 'tone' right away. They were dropping steadily and with some conviction on both the SP and the NDX. Something had clearly happened. So I pulled the trigger on a short order I had teed up for the weekend, and went looking.

Bloomberg TV was showing nothing. Even on their news headlines on the right side there was nothing showing except for a headline 'Breaking News' that Walmart was dropping e-cigarettes. The on air discussion was some infotainment discussion about how to play the next rally, yada yada.

I flipped over to Fox Business, which is something I almost never do, and bam, they were showing breaking news that China had just cancelled a visit to Montana to discuss agricultural purchases, and Trump was making noises about what a hard and complete deal he was going to be driving with China. Fox was covering the hell out of the story, and putting it in context with the market decline.

Back to Bloomberg and there was nothing. Even when their most seasoned news pro Mark Crumpton came on with the headlines at 1:30 there was nothing, and nothing on the sidebars.

Finally when she did a review of the markets, which were clearly dropping pretty hard, Scarlet Fu read off a piece of paper that the Chinese had cancelled their Montana meeting, and that some thought this is why stocks were dropping. And while they mentioned it a few more times in the afternoon, it was never really covered as news per se, although Joe Weisenthal had a chuckle about it, when they said that he was watching it.

So I was wondering if this was a real thing, or just some quad witch shenanigans. If so they should say so, not just ignore it.

Well I let it ride, since I wanted to have some short side coverage for my long holdings over the weekend.

But it seemed more than odd. Fox Business scooping Bloomberg on financial news that moves the markets is like the Orioles sweeping a three game series against the Yankees.

Let's see what happens next week. This is where the fog of corruption has descended over the markets.

There will be a fairly important gold option expiration on the Comex on the 25th. October is an active month for gold, not so much for silver.

Stocks went out near to their lows. Gold and silver went out near their highs. The VIX was higher along with the Dollar.

That precious metals market rigging charge, with RICO overtones, against JPM was such a big nothing, like some wiseguys have claimed, that the gold leverage lords of the LBMA just kicked the head of JPM's precious metals desk off their board. Is this like the time Lucky Luciano booted Dutch Schultz out of the Five Families for excessive moral turpitude? QED

And so we had a quiet flight to safety, ninja-style.

While much of the conversation regarding gold and silver centers on the Comex, the London Bullion Market Association which has a 200+ year history is lesser known amongst American readers. It has a significant role in the global physical bullion markets.

There are many more banking member of the LBMA, but they do not provide market making functions at this time.

This is from the LBMA website.

Of the fifteen LBMA Market Makers, five are full Market Makers and nine Market Makers. The five Full Market Makers quoting prices in all three products are:

Barclays Bank Plc

Goldman Sachs International

HSBC Bank USA NA *

JP Morgan Chase Bank *

UBS AG

*Also provide vaulting operations for physical bullion in London

The ten LBMA Market Makers who provide two way pricing in either one or two products are:

Citibank N A (S)

Credit Suisse (S,O)

Deutsche Bank AG (S,O)

Mitsui & Co Precious Metals (S)

Morgan Stanley & Co International Plc (S,O)

Societe Generale (S)

Standard Chartered Bank (S, O)

Bank of Nova Scotia -ScotiaMocatta (S, F)

Toronto-Dominion Bank (F)

BNP Paribas SA (F)

(S=Spot, O=Options, F=Forwards)

Definitions of Spot, Forward and Options

Spot (S). The current price in the physical market for immediate delivery of gold. This is normally taken to mean loco London delivery two working days after the date of the deal.

Forward (F). A transaction in which two parties agree to the purchase and sale of gold at a future date, commonly 1, 3, 6 and 12 months but also for longer dated tenors or dates into the future (see table above). Forward contracts are an important part of many swap arrangements.

Options (O). This gives the holder the right, but not the obligation, to buy or sell gold at a pre-determined price by an agreed date, for which he pays a premium (or a cost). The premium is the amount of compensation the seller receives from the buyer. The right to buy is commonly referred to as a call option and the right to sell as a put option.

Also from the LBMA website:

Loco London

The term Loco London refers to gold and silver bullion that is physically held in London. Only LBMA Good Delivery bars are acceptable for trading in the London market. The Loco London concept has evolved within the market. In the second half of the 19th century, gold from Californian, South African and Australian mines was sent to be refined and sold in London.

With this business as a base, and in tandem with the increasing acceptance of the London Good Delivery List, clients from all over the world opened bullion accounts with individual London bullion dealing houses. It soon become evident that these Loco London accounts, which were used to settle transactions between bullion dealer and client, also could be used to settle transactions with other parties, by transfers of bullion in London. Today all third party transfers, on behalf of London market clients, are effected through the London bullion clearing system. Each segment of the market is described below.

Note: In this case 'loco' may derive from the Latin word 'locus' meaning to put in the place or location. It is not an acronym that I know of, and is ordinarily not capitalized in LBMA documents. It does not imply that the London gold trade is 'loco' in the modern sense, although it is understandable why some should think so. I suspect that the loco London rule was intended to rule out gold held in vaults outside of the general vicinity of London and especially overseas. Remember that this is a very old organization with a long history. Shaken by claims of fraud and price manipulation, it seems to be in decline now, becoming a price leveraging paper market like New York, with the physical precious metals markets moving more to Asia.

In the first chart we see that there were about 57 tonnes of gold bullion withdrawn from the SGE into China in the latest week. This is not 'official reserves' but all gold without regard to the receiving party.

This pushes the cumulative withdrawals of Shanghai gold over the 10,000 tonne mark. Not bad for less than seven years in the business.

This does not include gold that flows through Hong Kong, or through any other non-exchange means purported to be used by the People's Bank of China.

On the second chart you can see that Year-To-Date Shanghai has released 2,119 tonnes into China. Compared to prior years 2015 is clearly going to be a new record if the withdrawals maintain this pace.

One thing that struck me on that second chart tonight is that Shanghai withdrawals took a definite leg up in 2013.

This is also the same year that the price of gold in Dollars was smacked lower, and the ratio of potential claims to registered gold on the Comex began to climb, and eventually start to go parabolic this year.

Perhaps the bullion bank apologists and shills are right, and this is all just meaningless, an optical illusion, or some fantasy. Gold is just like pet rocks, and the majority of the people in the world, and throughout recorded history for that matter, are just confused and demented.

As I mentioned earlier this evening, the tails risks look rather fat. One might wonder that even a dingy gray swan with a weak wing could trigger a fairly impressive set of 'unforeseeable incidents.'

They'll never learn. Why should they? Winning....

But perhaps we are much closer to the end of this than most people might imagine. Given the explosive ingredients in place it may be hard to miss.

Gresham's law is an economic principle that states that when an official market or cartel overvalues one type of money or asset and undervalues another with respect to its fair market value and risks, the undervalued money or asset will leave the country as best it can, or will disappear from circulation into hoards, while the overvalued money or assets will flood into circulation.

Let me stipulate up front that when it comes to the global gold market, the Comex has actual gold flows that are so meager compared to the amount of trading which occurs on paper that I have said it is starting to look like The Bucket Shop.

And in recognition to the disclaimer statement that appears on all of their documents, the exchange makes no claims and accept no liability that any of these numbers are accurate. They are taking the originators of these numbers at their word, some of which are Banks which have recently been shown to be serial offenders when it comes to their financial dealings, pricing, and representations.

As of Wednesday, only 171,613 ounces (5.13 tonnes) were 'up for delivery.' In a global market where the daily deliveries are measured in metric tonnes, that is a very small amount.

In terms of overall active Comex contracts, that represents a paper to physical leverage of roughly 263 to 1, compared to a historic trend of about 24:1.

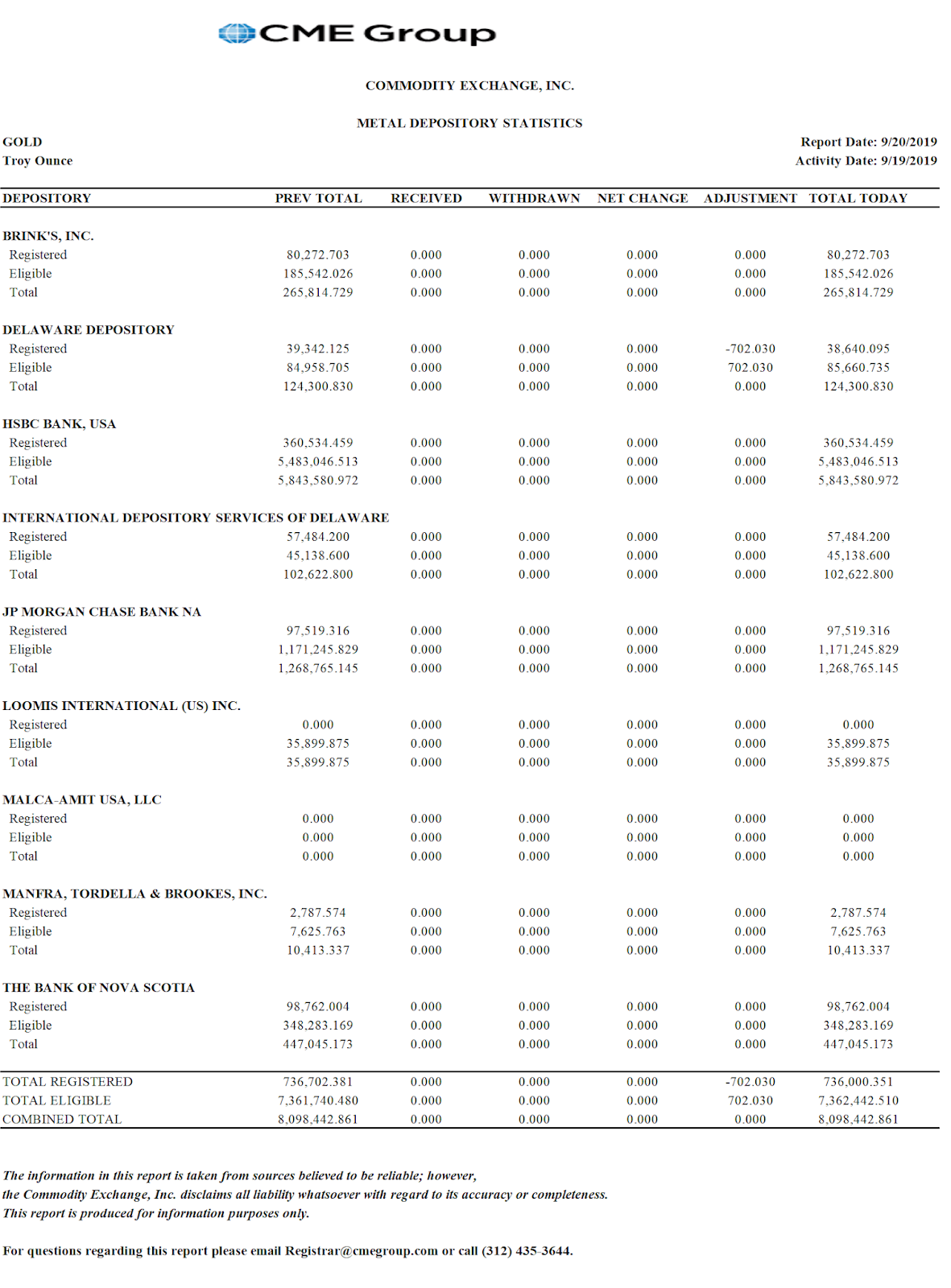

And as I looked things over, I was struck by the fact that of those meager ounces available, 101,312 (3.2 tonnes) were from the vaults of Nova Scotia, or roughly 60% of the total.

That struck a chord in my memory, so I looked over the list of deliveries for the month of October.

Of the pathetically small amount of 240 contracts, or 24,000 ounces (.75 tonnes) delivered in the entire month, 17,600 have come from the 'house account' at Nova Scotia.

And the 'takers' of those few ounces have been the 'house accounts' at JP Morgan and HSBC.

So what I am trying to prove with all this? Nothing. I am merely showing an interesting trend change that has gone largely overlooked, except in some notable exceptions of the 'smart money.'

And I am documenting some facts for those who have a mind to see them, and to establish a record that people can refer to when these jokers blow up yet another market through their reckless obsession with gambling large.

It shows that in a world of global gold flows, very little is moving in the Comex warehouses, and the little that is changing hands seems to be moving between the houses of three of the big bullion banks.

And it tend to support a hypothesis that the gold trading in London and New York has taken on the character of currency crosses, and lost their ties to the physical commodity nature of the product. This divergence may be convenient for the management of the price, and for easy profits for those managing the game.

But it has longer term consequences which will eventually come back to shock the markets. Where have we seen these types of divergences among risk, valuation, and the underlying realities before? In just about every financial fraud and following crisis in the modern era at least.

So remember this when the next crisis comes, and the distraction, dissimulation, and duplicities are put forward, and the search for non-consequential scapegoats is underway. And you are expected to bail out these jokers once again 'to save the system.'

I am fairly confident that all of this will come to pass if things do not change, and serious reform and enforcement of the rules of the markets are not undertaken. So far the changes we have are largely cosmetic. In a plutocracy big money manages the government and the media; they have bought and paid for it. And eliminating government only serves to eliminate the middleman. Transparency and reform are the only sustainable answer.

The big action in the precious metal bullion markets is in Asia.

And gold and silver bullion are steadily flowing from West to East because of a mispricing of valuation and risks. And the reason for the stunning drop in physical trading activity in the West is because in a manifestation of Gresham's Law, the hypothecated paper metals are driving out the bullion out of the market.

This is a trend, and it has significance to those who are willing to see it.

It is reasonable to estimate that London, in all the vaults, has only about 900 to 250 tonnes of gold available for physical delivery, which is a shockingly low figure given the current demand from 'The Silk Road' nations alone that is running about 1,700 tonnes per year. And even that 250 number is questionably high, depending on the status of the gold in the Bank of England.

The objective is to attempt to determine how much available physical gold for delivery can be wrung out of London and New York, in excess of what can be had from scrap, minining and leasing. We are calling that 'the gold float,' and it is feeding the demand for bullion in Asia. At that point we might estimate when the pressure on price becomes irresistible.

We are thinking months, not years, at least with things as they are.

I wish to acknowledge up front the debt that is owed to Ronan Manly and Nick Laird especially for the data contained herein, as well as Koos Jansen for his ground breaking work in estimating Asian gold demand, and Bron Sucheki for his participation.. I have listed some of the pertinent published articles below.

It is regretful that one can only provide estimates. But that is the nature of this beast that operates with secrecy of supply and distortion of actual demand.

What manner of business is this to enable price discovery in a public market, by covering so many fundamentals with secrecy? Where is the mining community in all this?

The LBMA is said by those who are in a position to know these things to be running 90:1 or more leverage to each of its unallocated ounces of gold, which according to Jim Rickards is all of them.

The potential claims per deliverable ounce at the Comex right now is at an historic nosebleed high by of about 255:1, supposedly because the owners which to avoid a 'short squeeze' in bullion, although the party who said this did not say 'where.' London probably, maybe Switzerland.

Peter Hambro says that "there is not enough physical about. There are endless promises."

In a nutshell, we now know that physical gold for global delivery, of which the London vaults are a major supplier, are rather tight, especially given the increasing demand for physical bullion in the East.

There is plenty of room for questioning the numbers and casting doubt on them, while hiding behind a curtain of exchange secrecy. One might suppose that the gold bullion bank apologists will be hard at it soon enough again.

They too often do not help to advance the understanding of the public, preferring to selectively twist the data to say 'all is well.' They deride the supply problems that people in the industry are encountering, always saying they are not real. And they like to include all the gold that exists in the warehouses for their calculations, whether someone else already owns it and is clearly not interested in selling at these prices.

More details would be useful, because if we could obtain a better idea on the extent of central bank leasing, we would be better able to estimate the risks and the relative fragility in the highly leveraged and hypothecated supply of gold in New York and London.

One would think from the known data that the unallocated gold in London is counter-claimed many times, and even the allocated and custodial gold is likely to have multiple claims upon it. So the actual 'gold float' is probably quite a bit less than 1,361 tonnes. Each of us has our own favorite ballpark number ranging from 900 to 250 tonnes and less, not fully accounting for leases and leverage on the remaining stock.

Nick Laird had a secondary outlier estimate which he expressed in colloquial Australian, which I dare not repeat here. But it was quite low. lol. Maybe four months worth of float left.

And it would certainly be nice to have more information about silver, especially since to my knowledge the central banks have dealt their own supply away some years ago and there are quite a few indications of tightness of supply, although not in the Comex yet.

I do consider this analysis to be a work in progress, Nick Laird and Ronan Manly are the key data organizers I believe, with help from Koos Jansen and Bron Suchecki, and the odd bit from Jesse the consulting detective. So I would look to their sites for explication of their methods and sources. Ronan Manly in particular is a public source and he goes into quite a bit of detail.

Given the struggle it has been to obtain the data, and the refusal of central bank personnel to discuss their own supplies on orders from above, there may surely be gaps and errors in this, but not for lack of effort.

If I have any major concern it is that the management, the exchanges and the regulators, will allow the traders to sleep walk themselves into a rather serious situation. And don't we know how little self-restraint these traders have been showing.

The remedy for this situation is not even more leverage, or more hypothecation of the unallocated stock, or even more leasing by the central banks, or more programs in India to dampen demand.

The longer they allow this price rigging and leveraging up, the slower productive mines will come on line, and the worse the tightness on the remaining physical supply will become. But as they say in New York and London, 'nothing is broken yet.'

The market solution for this tightness of supply is HIGHER PRICES and not increasingly ludicrous jawboning, spin, and bear raids.

And if higher prices might inconvenience the policy and perception management aspirations of the Wall Street financiers, their enablers and associated hirelings, well then too bad. Try to behave more responsibly, and stop attempting to make the rest of the world pay for your excessive gambling losses and poor judgement.

Here are a few additional charts from Nick Laird's site at goldchartsrus.com to break out a bit more detail and to provide some context for the estimated physical supply compared to physical demand.

physical tightness of flow is reflected in the price not at all.

Gold is moving in one direction from west to east with small exceptions over the last year.

The danger of less supply moving forward is more likely than the comfort of more supply."

I found this discussion between John Ward of Physical Gold Fund SP and an executive at one of the top Swiss Refiners highly informative, and suggest that you give it a listen.

The most difficult part I have found in presenting information is that once a group has amassed a great deal of data and putting it into some organized form of information, an arduous task indeed, the next step of taking that information and putting it into a relatively simple and easier to understand format is a very important task and none too easy in itself.

I certainly learned that lesson through years of making presentations to the principal executives of Fortune 100 companies. Most of the time they wish to have everything on one sheet or slide, with backup optional for their staffs or key questions they may ask in 'drilling down.' If you have ever worked at a large company I am sure you know the feeling.

I hope to have something out on this issue later day.

But this is quite interesting and stands alone. We have been hearing about this 'tightness' from quite a few quarters recently including some bank analysts and Peter Hambro.

You may read about this and listen to the actual podcast at Physical Gold Fund.

The gentleman we are interviewing is part of senior management of one of the largest Swiss refineries. His refinery is one of only 5 global LBMA referees, which takes samples from other refineries around the world and certifies them to produce gold meeting the purity and form factor of the LBMA good delivery standard, which makes it part of the very core of the industry globally.

He has over 30 years experience in the gold markets and has in our view one of the most authoritative perspectives into global physical gold flows in the world. His unique outlook, formed from internal data on gold flows through the refinery, combined with colleagues throughout the industry including the largest bullion banks (versus news outlets) is an invaluable source of information and paints an important picture for the gold markets moving forward.

Topics include:

*Why trying to correlate physical flows with the price can be misleading;

*On-going tightness in the physical gold markets;

*There is less liquidity in the physical market;

*The physical tightness of flow is reflected in the price “not at all”;

*As long as the spot market is settled with cash settlement, the physical flows are not determining price;

*If investors dealing in cash markets begin to take delivery, the physical is just not around;

*The current pricing mechanism can continue indefinitely unless investor behavior changes to taking delivery versus cash settlement;

*The gold price has “no correlation to the physical market”;

*If this behavior changes (to taking physical delivery) it could become dramatically dangerous;

*Gold is moving in one direction from west to east with small exceptions over the last year;

*90% of the refinery’s business is currently supplying demand from the east (India, China) and 10% to western markets;

*China has imposed a new standard on the LBMA good delivery system of 1 kilo, 999.9 fineness;

*400oz bars being melted and refined to 1 kilo 999.9 fine bars and shipped into China are coming out of London and particularly the ETF’s such as GLD;

*In the next gold upleg, scrap may not be readily available – overall scrap has decreased remarkably;

*Declining investment in the mining sector and geo-political issues affecting mining viability will unavoidably reduce gold supply moving forward;

*The danger of less supply moving forward is more likely than the comfort of more supply.

“Our clients will call up saying ‘I hear the Comex is running out of gold, what do you make of it?’ and our quick answer is that this is a non-issue,” Jeffrey Christian, managing director at CPM Group, said in a telephone interview.

“Even if you look at the fact that registered stocks have declined, the fact of the matter is most Comex futures contracts” are cash-settled, and traders don’t take delivery of the metal, he said.

While the percentage of Comex gold open interest covered by total Comex reported stocks has fallen over the past year and a half, it “remains very high by historical standards and presents no perceptible risk of imminent problems with deliveries,” CPM Group said in a report dated Sept. 14...

Barclays Plc said in a report this week that emerging-market demand for gold has shifted some metal into Asia, and that “coverage of physical stocks in Comex remains solid.”

“Anything that has more upside than downside from random events (or certain shocks) is antifragile; the reverse is fragile.”

Nassim Taleb, Antifragile

Gold is anti-fragile. This is why it must be handled with care, and not with fragile systems. Gold is intractable to the kinds of manipulation by the financial system that can bend paper to its will. This is why they hate gold, and seek to paper over it with leverage and secrecy.

Above is a commentary on the physical bullion situation at the Comex as it was reported at Bloomberg News yesterday. The 'deriding', which means ridicule and contempt, is coming from CPM group's Jeff Christian, and from a report from Barclays.

The title of the article is a bit odd, because I have not see any 'theories' about this subject at least here, just presentations of the facts using exchange provided information. And as for deriding, it seems more like a sign of weakness and fear than solid reassurance. But that is just my own experience in seeing that sort of thing when someone points out a changing situation that could pose a problem.

One thing the story fails to make clear is that only registered gold is deemed deliverable to fulfill futures contracts. Yes, all the gold in all the warehouses could potentially satisfy demand, IF IT WAS UP FOR SALE. But it is not.

The total supplies at the Comex have as much to do with the current demand for bullion as all the automobiles in your neighborhood have on the price that you are going to pay tomorrow for a used car, eg. the calculation cannot include items that are not up for sale. Yes there are many cars that would satisfy your requirements. But only those that are for sale are available for you to drive home.

Jeff Christian says that "even if you look at the fact that registered stocks have declined..."

Yes, 'even if' you look at the heart of the argument, 'registered stocks have declined,' and that is quite the understatement of the facts.

Here is the history of 'registered gold bullion' on the Comex going back to 2001.

And of course if almost no one asks for any of the gold, then there is no problem. Yep.

This is the problem. For anything except speculating with paper the Comex is now significantly fragile, moreso than at any time it has been in the last twenty years at least.

Jeff goes on to say that "most Comex futures contracts” are cash-settled, and traders don’t take delivery of the metal,"

And that is correct. Here is the history of deliveries, ignoring any cash settlements, on the exchange.

As should be easy to see, the amount of gold bullion deliveries is declining quite a bit.

The Comex lacks the market discipline of delivery of the goods and restraint on the potential hypothecation of available supply. What is acting to hold leverage to some reasonable level other than 'nothing has broken yet.'

Let's take a quick look at the ratio of total contracts to registered gold, that is gold up for sale.

The Comex is a significant price discovery market for the global gold supply. The data shows that it has diverged significantly from the physical bullion markets primarily in Asia.

While the inventories at the Comex remain flat overall and declining sharply with regard to deliverable bullion, the physical deliveries of gold into India and China are increasing steadily.

And I hasten to remind everyone that gold is truly a global market.

Nick Laird at sharelynx.com has created chart that tracks the known physical gold demand for what he calls 'The Silk Road.'

Even though I do not expect a default at Comex, as I have said many times before, the point is that if there is even a mild problem in one of the physical markets in Asia or London, the Comex is price positioned for a market dislocation and potential fails to deliver bullion on request.

The deliverable gold is a little under 6 tonnes. But even if price were no object, the total gold held in private hands in all the Comex warehouses is about 6,716,000 troy ounces, or roughly 209 tonnes. That is all of it no matter who owns it or why.

Or less than one month's supply for the Silk Road countries.

Normally none of this *should* be problem, although one has to admit that according to historical norms the amount of deliverable gold is very thin by any measure. Why is this? Why are the better informed withdrawing their bullion from the deliverable category? I read that they are afraid of the bullion being caught in a 'short squeeze,' but the trader who said that did not specify a short squeeze where.

This week I learned from an interview with Jim Rickards that some very large bullion banks were said to be using the Comex gold futures to hedge shorts in bullion delivery markets in London, called the LBMA.

That kind of a hedge might work to guard against paper losses, but against a genuine fail to deliver in a physical market you can see that the immediate deliverables at these prices are about 6 tonnes, which is a rounding error on the Silk Road.

It's the fragility, always the fragility.

What if something that is not completely normal and expected happens? What if, instead of 2% of the contracts asking for delivery, a delivery short squeeze in London prompts 4 or 5 percent of the contract holders to attempt to exercise their contracts to receive physical bullion to cover their obligations elsewhere?

The fragility of such an arrangement is bothersome to anyone from outside who looks at it from a systems engineering perspective.

If some firms are using the Comex as a backup system for gold deliveries in London and points east, it is hardly equipped to take that role without a significant market dislocation in price.

If I was only working short term trades and would never mind a settlement in cash, then the Comex seems like a fine place to do the trade.

However, if my goal is to have a solid claim on physical bullion, even within some reasonable length of time measured in several months, it does not appear that the Comex is appropriate for that particular objective.

Do you see the potential problem here that is so blithely 'derided?'

I do not wish to alarm anyone. I am putting out the word because I do not think people understand the situation that has developed, over the past two years in particular, as shown by the potential claims per ounce.

Globally huge market with increasing demand, a market where the available inventories are exceptionally thin, and a price that is derived without a tight rein on leverage and the discipline of delivery. What could possibly go wrong?

The usual retort is 'it has not broken yet.' Yes, and in the light of our experience over the past ten years or so, some might find rather thin comfort in that. The important thing is for traders and investors to be fully informed, that they may use financial instrument in a manner that is appropriate to their objectives.

For example, using Comex as a backup for bullion positions on the LBMA might be fine, if you are not expecting to receive delivery of bullion that can be used to satisfy your obligations there.

The exchange might consider another look at their rules in the light of this unusual 'leverage' of potential claims to bullion, rather than count on price fixing all problems, and few standing for delivery, especially in a changing and very dynamic global market.

I do not have good visibility into the leverage and available inventories at the LBMA in London. If those are in any way similar to the Comex, then I would take some action fairly quickly to secure my ownership of bullion given the potential for a misstep that spins out of bounds.

If you hold an allocated receipt that is as 'good as gold?' Tell that to the investors who used MF Global, and found their holdings sorted out in court against a lawyered up megabank.

I do not know Jeff Christian or the fellow from Barclays. I am sure that they have good reasons for what they are saying and the advice they appear to be giving to their customers. I am sure they can all work out all their concerns and particular issues among themselves.

Objectives amongst customers do vary and it is the fiduciary duty of any advisor to help them make an appropriate choice. And I can see many uses for Comex positions that are entirely suitable for some. A short term trader for instance, who in merely placing wagers that he expects to settle for cash.

But as for this article in Bloomberg, it is a bit of a gloss, heavier on the deriding and short on information for readers to use in making their own informed decisions. 'Trust us' and 'nothing has broken yet' are, as I said previously, non-starters these days.

I have set forth only a few of the oddities that are becoming apparent in the gold market. There are quite a few more, including backwardation and tightness in the London physical market as noted by Peter Hambro and an analyst at Mitsubishi recently, and in articles by Koos Jansen and Ronan Manly.

How about the pivotal London market, is it 'well-supplied?' How well supplied is it? What is the potential impact on the Comex of a bullion shortfall at the LBMA?

Has there ever been a 'stress test' of what it would be like at the Comex if there were an afternoon failure to deliver physical bullion in London? Or are you assuming as your baseline that such a shortfall could never happen in any non-Comex market? Is the process at Comex for some event like that, besides halting the exchange and forcing cash settlements?

I do think that one can become so involved in a system, for so long a period, that when it changes, when the market dynamics start shifting, the old hands may be the last to notice the forest for all those familiar trees. That is why companies bring in quality teams to inspect their processes for soundness and failure points.

What could have possibly changed in the global gold market in the past few years. "Barclays Plc said in a report this week that emerging-market demand for gold has shifted some metal into Asia,"

How about this? Some shift. Some metal.

Here is what Kyle Bass recently had to say about the situation. Maybe you can 'deride' him. Then again, maybe not.

In the light of how the MF Global debacle was sorted out by the courts, and based on a growing body of circumstantial evidence and market indicators, if you are holding your gold bullion 'insurance' in the form of unallocated or opaque holdings, or a hypothecated paper claim in one of the major exchange trading warehouses, you may wish to take measures to safeguard your ownership claims without much delay.

I wrote something overnight, On the LBMA and Their Unallocated Holdings, in which I lay out the case, based on facts and some presumably informed speculation from Jim Rickards, that there is a serious physical shortfall in gold bullion developing that may not resolve as readily as it did in 1999, when the Bank of England presumably bailed out the trading houses.

Commodity backwardation is not all that unusual. But it is somewhat unusual in the precious metals. And in combination with a few other items, it seems worthy of note and some preventative measures.

Koos Jansen notes that gold is now in backwardation in both London and New York.

"Not often in financial markets is the future price of gold is lower than the spot price (live), but lately we’ve witnessed such an event in both the New York and London gold market. This is called backwardation, the opposite of contango.

What causes backwardation and will it increase the price of gold? In my opinion there are two possible scenarios: the market expects the gold price to fall in the future, or there is scarcity now."

Please note that I am not suggesting that you should rush out and take large long positions in gold with the maximum leverage, pile into penny miners hoping for a 'home run'.

I suppose that quite a few will miss this caution since it is not heralded with blaring headlines of imminent doom, but perhaps those who need to hear it will do so. And I am sure that the apologists and the paperati will find their usual ways to dismiss all this, and urge us to ignore all these odd doings in the warehouses. Such are the times.

And I am not ruling out a much larger development behind the scenes with regard to the international monetary regime, that is 'leaking out' from official sources to banking cronies who may act on it ahead of time. But I have no strong indications of that. The IMF seems incapable of resolving the developing monetary crisis because of Anglo-American intransigence.

This is a purely circumstantial case. As was the case that Harry Markopolos presented for years on Bernie Madoff. And it may be wrong, or it may be right and vastly understated. But I think that we have means, motive, and opportunity, and so one may advisably act with caution. And so I have discharged my conscience in not remaining silent while potential trouble looms and the denizens of the markets take care of themselves. It is not so easy a decision to make when you do not have sound evidence because of secrecy and misinformation. And I am sure many will take this, use it as their own, and wrap this in florid headlines and dire predictions of doom.

I suspect at this point that a price correction is still possible as a remedy, but I am not so optimistic to rule out a greater effort to cover it all up that will make things exponentially worse, in the manner of the London Whale and MF Global and LTCM and so many examples of reckless hubris.

There is quite a bit of official interest in bailing out these wanton rich boys from their gambling debts and assorted scrapes, as Sir Eddie George of the Bank of England noted in 1999. And the central banks may rise to the occasion and lease out the people's gold on the cheap to get them out of this one as well. And all under the radar, hush hush. Insiders never speak ill of insiders, or do anything to inhibit the kleptocracy.

"Nor can private counterparties restrict supplies of gold, another commodity whose derivatives are often traded over-the-counter, where central banks stand ready to lease gold in increasing quantities should the price rise."

Alan Greenspan, Congressional Testimony, July 24, 1998

The denouement of the New York-London Gold Pool is coming, but it may not be here yet. These things tend to drag on and on, wearing most everyone who suspects them out. Lots of people make claims about 'paper markets'. They paper the landscape with them. And if something happens, they will all claim to be the first. The point is to drill down and attempt to assemble the data against determined effort to distort and obfuscate and hide it.

There are people who make calls, and people who make money. I don't make 'calls.' I try to calculate odds, and then take some guidance from the probabilities. There are no sure things in this life, except that we will all meet the same end, and I believe will be called to account for our actions.

Timely caution is advisable, perhaps on a number of fronts.

"The August turbulence in global [equity] markets has produced significant shifts, including a 6.6% fall in equity prices. The currencies of emerging market countries have depreciated substantially against the G-4, while emerging market borrowing rates for sovereigns and corporates [bonds] have moved higher. Global oil prices have been whipsawed as have G-4 bond yields.

The speed and magnitude of these movements is reminiscent of past episodes in which financial crises emerged or the global economy slipped into recession. However, nothing appears to be breaking. Global activity indicators have, on balance, disappointed but remain consistent with a modest pickup in the pace of growth. Additionally, despite the turbulence in financial markets, there is no sign of unusual stress in short-term funding markets or of a credit crisis in any large Emerging Markets economies."

Bruce Kasman, Chief Economist, JP Morgan

So be of good cheer, nothing appears to be breaking, yet.

"We looked into the abyss if the gold price rose further. A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake. Therefore at any price, at any cost, the central banks had to quell the gold price, manage it."

Sir Eddie George, Bank of England, September 1999

Below is a partial transcript of an interview with Jim Rickards on The Gold Chronicles from July 16, 2015.

You may listen to the entire interview here. This transcript is for the portion that runs from about minute 31 through 42. It is a very interesting interview and if you have the time you might wish to listen to the whole thing.

The reason I wished to share this transcript is the nice, compact description that Jim gives of the LBMA and how they manage their gold bullion contracts.

What provoked this discussion was an earlier question about the reported very large long positions of two banks, JPM and Citi, on the Comex that were noted back in May-June of this year.

Jim's supposition is that they must have had a physical gold short exposure elsewhere, and possibly on the LBMA. As Jim relates it the Banks do not typically take large positions in one direction but tend to work on spreads and make their profits with leverage on those fairly thin trades. And Jim should know since that massive buildup of leverage on thin trades that refused to perform is what blew up LTCM while he was there.

As is clear from this interview, the LBMA is a 'fractional reserve' exchange, with much of the gold being hypothecated some number of times.

IF there is a shortage of physical bullion developing, it will most likely appear in either London or Switzerland. That is because London is the gold hub for the West, and they tend to operate on some multiple of claims to actual free holdings. And Switzerland is where the gold is procured and refined for the formats of the Asian markets

As you know, I have been looking carefully for some time at the odd happenings with physical bullion on the Comex. At least they seem very odd to me if not to some others. You can be the judge.

And as you may recall, there were some pieces in the news about the 'tightness' of gold in London and the dearer prices being paid for gold available for immediate delivery. Again, nothing huge, but another point of data.

And of course there is Goldman in there taking delivery of bullion for their house account reportedly.

And this flurry of schemes coming out of India to do more domestic mining, and monetize the gold held by private individuals and their temples, to stem the demand for bullion imports.

IF the Banks were short of physical bullion in London around July when Jim gave this interview, then by his estimates we would tend to see the strains on the free holdings of physical bullion about-- now.

I do not know what has caused Jim to say that "people are taking their gold out of banks and putting it into new vaults because they’re losing confidence in the banking system. These new vaults are private storage vaults owned by private companies, not by banks." I do not have his level of contacts. But it does seem that there is a slow but steady bleed of bullion out of the Comex warehouses. And 'deliverable' gold is at record low levels.

One would hope that the Banks were wise, and would not pyramid their web of wagers in size and term, hoping that the shortages of physical gold do not become deeper and more stubbornly set. This could turn into a feedback loop of shortage and demand that would have Sir Eddy George back staring into the abyss once again.

But alas, this time the central banks are net buyers, not sellers. And the gold manipulators must contend with the great engines of physical demand in the East. Surely by now the Banks must have learned their lessons about recklessly gambling with other people's money and assets.

What have we learned, at long last, about bailing these fellows out?

What makes this a more potentially serious problem is that the willful battering of the miners may make a resilient source of non-central bank supply more difficult to ramp up A typical gold project takes many years to get into meaningful production.

Perhaps the central banks will use the people's sovereign wealth, this time in the form of gold as well as paper, to bail out their banking buddies from their reckless wagering once again.

When I was in Switzerland for Physical Gold Fund, we actually saw the gold that belongs to the investors in Physical Gold Fund. We had auditors, they had bar numbers and manifests, and we went item by item. Those bars actually belonged to the fund.

That’s not true with these LBMA agreements. You don’t have any allocated gold. That means a bank can have, say, one ton of gold and they can sell 20 tons of gold. They use the one ton to back all 20 of those contracts. In effect, they’re short 19 tons. They own one ton physical and sell 20 tons to a bunch of institutional investors or high-net-worth individuals who want to own gold, so they’re short.

They depend on their customers not asking for the gold. As long as this is all on paper, it works fine. Where it breaks down is if the customer comes in and says, “You know that unallocated gold? I would like to make it allocated and actually have the physical gold. In fact, not only do I want it allocated, but I would like you deliver it from your vault to a private vault run by Brinks or Loomis or one of the big secure logistics providers.”

That is what’s going on. People are taking their gold out of banks and putting it into new vaults because they’re losing confidence in the banking system. These new vaults are private storage vaults owned by private companies, not by banks.

Going back to my original scenario, the bank has one ton of gold and they sell 20. If even five customers show up and say, “I’d like my gold,” one ton each, you’re now short four tons. You have one ton of physical, but you have five tons of requests from five different customers. You’re short four tons, so you have to go out into the market and buy four tons of market. Guess what? That’s a big order. Good luck finding it. You can find it eventually, but you might not be able to find it quickly. So you have price exposure. You’re suddenly short the gold because your customers are demanding it.

What would you do? You’d go out and buy the futures. Now you’re hedged. You’re short to the customer who sent you the notice, you’re long on the futures, but you’re price exposure is hedged. Now you can take 30 or 60 days or however long it takes to source the physical and make delivery to the customer. The customer may think the gold is sitting in the vault and can be delivered tomorrow, but trust me, they can’t. They’ll be lucky to get it in 30 days and could even take a few months.

When I see a massively long futures position, it suggests to me – again, to be clear, I cannot prove this – that banks are turning up short in some other part of the operation, probably on these unallocated gold forwards. Customers are taking their gold out of the bank, the bank has to deliver to those customers, they’re short, they’re getting long futures to hedge, and they’re going to spend the next couple months going out and buying gold.

I see that the apologists for the status quo are actively 'refuting' the tightness of physical gold in the London markets, largely by ignoring that and concentrating on the Comex, which they assert is 'well-stocked.'

Clever people learn from the political process to ignore the tough questions that they do not wish to answer, and to misconstrue the question into whatever it is they would rather answer, often squirming through the issues to put some proposition in the most favorable light for their firms.

So we see this in so much commentary from the bullion bank and trading house apologists this past week. I won't dignify them by citing their names, but I think you will know who they are.

Peter Hambro's recent point was fairly clear. It is almost impossible to obtain sizable amounts of physical gold in London which is the center of the Western physical gold trade.

"It is virtually impossible to get physical gold in London to ship to those countries now. We get permanent requests in Russia now. Would we please sell our physical gold to India and to China?

Because there is not enough physical about. There are endless promises. And I worry that the market, the paper market, could be stamped on and people say 'sorry we're going to have a financial closeout' and it's all over. If you want to be in the gold business, you ought to be in the physical business."

Peter Hambro

The gold apologists bravely assert that there is plenty of gold in the Comex, relative to the demand there. Never better. More on that later.

As I have pointed out on any number of occasions, the amount of physical gold in all of the Comex warehouses of any categories is a rounding error on the physical markets of Asia. As I said the other day:

I am certainly not suggesting that there will be hard default at the Comex. How could one expect that in a relatively small market that almost always settles in cash and is dominated by a few, very large insiders who are actively working both sides of the trade? No, if there is a default anywhere, it will precipitate in a physical marketplace where bullion changes hands and form, more likely in London, perhaps even Switzerland. And then it will cascade to all the other markets quickly.

The portion of the gold in London that is not specifically 'spoken for' and held closely is considered to potentially be part of 'the float.'

That was the key point that the apologists are ignoring. They ignore the physical market, and concentrate on a scenario at the Comex which is becoming almost atavistic, but still worth noting nonetheless as a kind of barometer. Comex seems to have lost its position as a source of genuine price discovery relative to the greater market of physical demand and supply.

The Comex gold warehouses, all of them, are a rounding error on the physical gold demand in India and China alone. The Comex serves as a diversion from the developing situation with the supply of bullion.

As you know if you frequent this site, there is an interesting phenomenon of diminished deliveries and stocks of gold at Comex that is 'for sale' that extends back to 2013.

Further, the volumes of paper contracts traded against the physical backing for them is reaching unprecedented numbers of leverage, even going back twenty or more years.

Yes Comex is well supplied in relation to its deliveries if one is to assume that it is just a betting parlor unrelated to the physical market worldwide for which it presumably provides price discovery.

And so his concerns are answered by apologists again pointing to plenty of supply on the Comex.

Anyone who questions this situation, who looks at the data, who sees the almost daily slamming of the price of gold into the London PM fix and the New York trade, is obviously a hysterical conspiracy theorist, right? And we must do what is required to intimidate them, to shut them up.

After all, what could be odd about such a multi-year pricing pattern like this in a market that purports to genuine price discovery, not for two cities alone, but for the world?

One *could* explain this by saying that Asia is buying, and the West, particularly London and New York, are selling. And you could cast aspersions on the foolish Orientals for wasting their money on 'pet rocks.' All of this has been done.

That is not the point. The point is that there is such a phenomenon, it is valid, and it tells us something that some people apparently do not wish us to think about.

Given the opaque nature of the markets, and the lack of honest disclosure and discussion of what is happening, it is difficult to engage in reasoned arguments about this, especially when the sides quickly degenerate into hysteria, name calling, and all too often in search of headlines.

It happens on both sides of the argument, although I will confess that the paid professionals are getting rather good at it, and may confound many. Clever boys are well taken care of by this foul and rotten financial system. Oh you think I exaggerate? Where have you been the last ten years?

No, this situation will be resolved by a hard failure to deliver, and most likely in London or Switzerland. The last place I will look for a clear indication of the market is at the Comex, although as Hambro was suggesting it is likely to be significant collateral damage. That is what he said.

And then when that tide goes out, we will see who is who and what is what. And we may have to wait awhile. But given that so many major markets have been proven to have been manipulated for the benefit of a few powerful firms, even though perhaps justice has not been done and settlements made without criminal admission, I think questioning the odd events and integrity of this particular market is certainly worthwhile in the light of its recent performance.

And for my own part, the arguments that seek to 'explain' the oddness in these markets are found to be wanting at the very least, and disingenuous in far too many. But I understand that one must do what their position requires.

So tell me fellows, is London well stocked relative to gold available AT THESE PRICES? Are we secure in the knowledge that continuing levels of demand from 'Chindia' and elsewhere will be met AT THESE PRICES? Is the true state of the Comex and the LBMA transparent to all market participants?

The total amount of ALL gold held by ALL market participants at ALL the Comex warehouses, whether it is on offer or not, is about 218 tonnes. That is less than one month's demand for physical bullion in China and India and India alone. And by far the vast majority of that gold is not for sale AT THESE PRICES.

And given the leverage of paper claims everywhere, not just Comex but at the more important LBMA, and one can see that a misstep by the gambling goofballs of Wall Street could lead to quite a messy market situation. This also is what Peter Hambro said.

Oh no, they would NEVER overextend their positions in the quest for easy money. Who could even think that?

It is good to keep a level head, and be guided by common sense. And I think it is all too easy to fall into the habit of either shutting up and keeping your head down, or answering ridiculous excuses with equally ridiculous assertions, and so leave the poor bewildered investor in a state of confusion.

Let's recall what Kyle Bass, who is not so easily dismissed as a 'crank' had to say.

Let us pray for those whose hearts have grown cold, and become hardened against His grace by greed, fear, and the seductive illusions of pride.

We ask to receive the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness—so that we may obtain abundant life, and the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.