skip to main |

skip to sidebar

This seems mildly reminiscent of the setup which Soros and unnamed Swiss parties engaged in when they took down the Bank of England's defense of the British Pound and its official peg to the Euro.

Will the US ultimately feel compelled to defend some of the gold and silver shorts, both in terms of bullion and derivatives, held by its Wall Street Banks? You could allow for the possibility, if you will, that there is a corresponding web of derivatives that has a links, and a possible chokehold, on a few key European institutions, particularly in England and Germany, involving counterparty derivatives and CDS, and collateral damage to professional and political careers. Ugly stuff, rather messy really. But there are historic precedents.

How Asian Buyers Are Maneuvering the Metals Shorts

There should be no confusion that this involves not only a few large Wall Street players, but also elements, past and present, in the US Treasury and the Federal Reserve. It makes the unfolding insider trading scandal look like a neighborhood numbers racket.

Therefore we should not discount the possibility that if a default should occur there will be an emotional and political reaction put forward as a means of deflecting the disclosure of the true nature of the financial corruption.

It would be most interesting and possibly entertaining to see if Ron Paul's congressional committee could be able to mount an effective investigation into the matter, or if events will take place to pre-empt and redirect such an inquiry to manage the potential collateral damage to careers and possibly governments, both at home and abroad.

It's never really the act itself, often minor infractions undertaken for practical purposes or what could be rationalized as such by some. Rather it is always the corruption of the policy actions to personal gain, and the subsequent cover-up, that tends to gather substance over time into a first class scandal, acts of felony and high crimes, and all the revelations that follow.

“Oh what a tangled web we weave, When first we practice to deceive." Sir Walter Scott

Non-event FOMC statement, the last of 2010, which is what had been expected. The macro retail sales picture was painted in high gloss, but the big miss by Best Buy cuts deeper to the heart of the truth.

The US is becoming two nations, one of privileged fraud and illusion, and another of harsh reality, difficult circumstances, and unnecessary hardship.

The first paragraph is the only thing that has changed and that from slow to insufficient. The Fed is dour on the jobless recovery and its self-sustainability.

"Information received since the Federal Open Market Committee met in September confirms that the pace of recovery in output and employment continues to be slow. Household spending is increasing gradually, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. Housing starts continue to be depressed. Longer-term inflation expectations have remained stable, but measures of underlying inflation have trended lower in recent quarters."

Contrast this opening paragraph from the Fed's November 3 Statement with their latest below.

Release Date: December 14, 2010

Federal Reserve Open Market Committee Statement

Information received since the Federal Open Market Committee met in November confirms that the economic recovery is continuing, though at a rate that has been insufficient to bring down unemployment. Household spending is increasing at a moderate pace, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. The housing sector continues to be depressed. Longer-term inflation expectations have remained stable, but measures of underlying inflation have continued to trend downward.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Currently, the unemployment rate is elevated, and measures of underlying inflation are somewhat low, relative to levels that the Committee judges to be consistent, over the longer run, with its dual mandate. Although the Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, progress toward its objectives has been disappointingly slow.

To promote a stronger pace of economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate, the Committee decided today to continue expanding its holdings of securities as announced in November. The Committee will maintain its existing policy of reinvesting principal payments from its securities holdings. In addition, the Committee intends to purchase $600 billion of longer-term Treasury securities by the end of the second quarter of 2011, a pace of about $75 billion per month. The Committee will regularly review the pace of its securities purchases and the overall size of the asset-purchase program in light of incoming information and will adjust the program as needed to best foster maximum employment and price stability.

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels for the federal funds rate for an extended period.

The Committee will continue to monitor the economic outlook and financial developments and will employ its policy tools as necessary to support the economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Sandra Pianalto; Sarah Bloom Raskin; Eric S. Rosengren; Daniel K. Tarullo; Kevin M. Warsh; and Janet L. Yellen.

Voting against the policy was Thomas M. Hoenig. In light of the improving economy, Mr. Hoenig was concerned that a continued high level of monetary accommodation would increase the risks of future economic and financial imbalances and, over time, would cause an increase in long-term inflation expectations that could destabilize the economy.

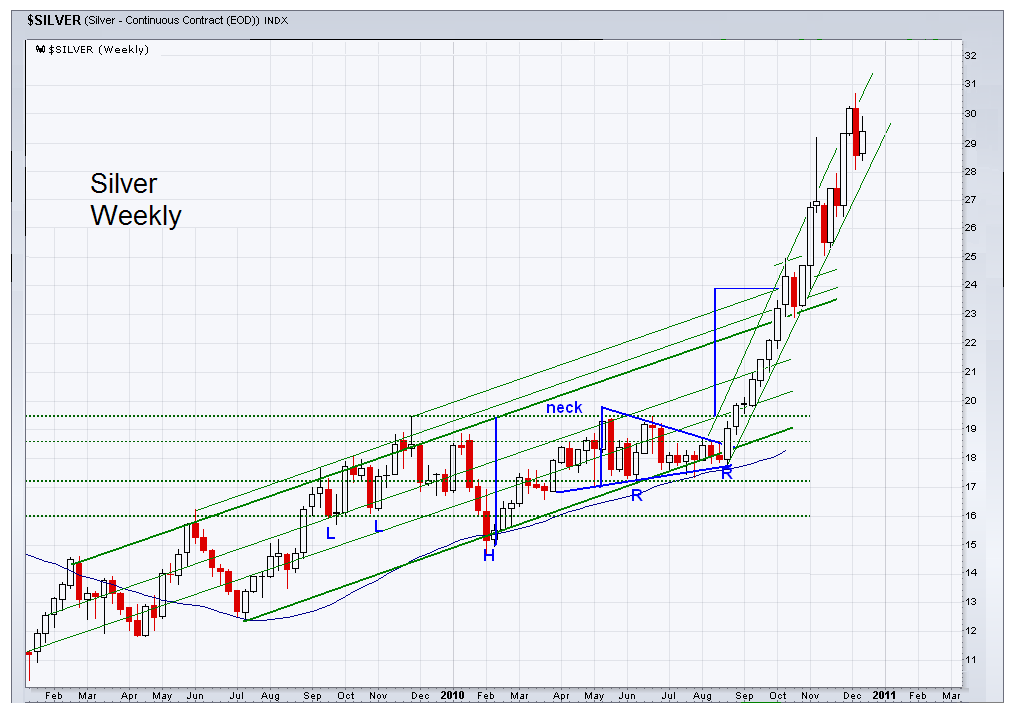

Well, it could be worse. He could be short silver, too.

S - A - V - E - - - M - E - - - B - E - N - N - N - n - n - n - n - n ...

"I listened to Kitco's Nadler on the Bloomberg channel this morning. He's been bearish on gold for months, and I thought he sounded like a know-nothing fool today. Why didn't Bloomberg interview someone who's been bullish and right about gold?"

Richard Russell

The US dollar did a quietly impressive 'cliff dive' today.

Harvey Organ's metals commentary is interesting this evening. It appears that some rather large customers are pulling their silver bullion out of storage in the Comex vaults. Trying to beat the Christmas rush?

Volume in the gold ETF IAU was 700% of average today. Perhaps some players are diversifying out of GLD.

FT had a story that the big US bank JPM is trying to reduce its silver short and edge towards the exits. Good luck with that.

Madoff trade off?

From an interview with Timothy Verdon, Art Historian and Canon of the Cathedral of Florence.

"God is infinitely beyond human comprehension – God is God, we are creatures. And yet in everything that the Judeo-Christian tradition tells us about God, it is clear that God wants to communicate with his creatures, God wants to be known by his creatures.

The whole point of the law and the prophecy in ancient Israel was that God wanted his creatures to understand him and themselves – a creature is a reflection, to some degree, of the Creator. This will of God to make himself understood – and in that process help us understand ourselves – reaches fulfilment in Christ. Christ is the Word of God where the Scriptures are many words that come from God and are filtered through the inspired authors; Christ is the very Word that all those other words try to give partial expression to.

Christ assumes a form that makes him intelligible to human beings – the Word becomes flesh. And then the Gospel of John immediately adds that he dwelt among us, and we saw his glory. What Christ did while he was on earth was to reveal the identity, the personality of the Father: all of the wonderful things that he did that reveal the father – the words he spoke, the miracles, the acts of mercy – even after Christ’s Resurrection and Ascension, they continue...

What’s the relationship of all of this with art which is my specific field? The relationship is simple. When Christ took a Body – when the Word of God took a body from the humanity of Mary – it was to be seen. Christ is now invisible except in the abstract forms of the sacraments – we see water and we know that we’re being cleansed, we see bread and wine and we know that his Body and Blood are present, but we don’t really see the body and blood. But somehow the extreme simplicity of that communication that God wanted in Christ’s Incarnation is now filtered by a symbolic system of sacraments and signs. So we don’t actually see, but the art of the Church allows us to see. It extends down through the centuries, something like that privileged experience of the people of Jesus’ own time when they saw him and intuited that there was more than just a man here. Art allows us to continue to enjoy that experience...

So the ancient desire of human beings to see God, Moses on the mountain asks God to show him his face…. In Christ people really contemplated the Face of God. Christ tells us that we see him in the poor and the needy, and so on. But the works of visual art that surround these privileged moments in which [people] come into direct contact with Christ, and which usually tell stories from the life of Christ, or of Mary or of the saints, in whom we also contemplate Christ – the works of art are part of this process.

Much of what I’ve done as an art historian is to try to remind other art historians of this whole dimension that I’m describing, which usually has not been discussed. And that’s a grave omission, because the artists and the patrons were more or less conscious of all of this. They lived within this system. So the art historians should be aware of it, because if not they are going to talk about these works in a way which is misleading. Certainly the style, the economical features – all of these things are interesting and real and an important part of the history of art, but the larger framework within which these works were meant to function was something more like what I’ve been describing.

I try to call the attention of colleagues to these things, and even more, perhaps, I try to reawaken Christians to the extraordinary eloquence and beauty of this visual heritage which today ordinary believing Christians have the equipment to understand. They may not be art historians but they have keys to understanding the works of architecture and painting and sculpture that many art historians don’t have. And those keys come from their own faith, from the simple experience of life in church, the life of the sacraments.

One could add that something that Christians tend not to reflect upon and that historians of art and of sacred music and sacred architecture similarly tend not to reflect upon, is that the great work of art that Christianity has produced since its beginning is the Liturgy.

What believing Christians have been harried by the Spirit to do right from the beginning is to seek those poetic forms of expression and those physical actions and those material objects that can be called into play to express their faith. Really Jesus himself taught us to do this. At the Last Supper, he took bread, and then he said words: “This is my Body”. Jesus, who is himself the Word made flesh, in order to communicate, takes physical things that already have their own range of meanings and says words that open that implicit range of meanings to a much more specific and explicit communication.

So Jesus himself is the first teacher of how you combine things and actions and words in order to create a composite work, which is basically a work of art. At the Last Supper, he puts on an apron, he kneels down, he washes their feet. He’s continually doing things that invite reflection and then making sure that we understand what he’s doing.

What I’m saying is that you can’t really just talk about the visual art of the Church, or the music of the Church, or the Liturgy. All of this is part of a single creative impulse that flows from the experience of Christ himself, the Word who becomes flesh. A conceptual expression of God who becomes visible and tangible. The First Letter of St John says that this is what we have seen and touched and contemplated with our own eyes; it’s a total sensory and intellectual experience. The Liturgy is that. So an artist working for the church and for its Liturgy is within this millennial creative action which, in the last analysis, is a continuation in time and space of the Creation described in Genesis."

An epic struggle between power and the people, that surprisingly so few among the people really understand even today.

“The money power preys upon the nation in times of peace, and conspires against it in times of adversity. It is more despotic than monarchy, more insolent than autocracy, more selfish than bureaucracy. It denounces, as public enemies, all who question its methods, or throw light upon its crimes. It can only be overthrown by the awakened conscience of the nation."

William Jennings Bryan

It will be interesting to see if the funds can keep this rally going into the year end. The volumes are thin.

Lots of speculation about fiscal action from China over the weekend.