Neither snow, nor rain, nor riots in Saudi Arabia or once in a hundred year earthquakes shall deter these markets from rallying into the close. Good old Benny, always can depend on him to turn a frown upside down.

Seriously, although the major US indices had a nice bounce off their lows, they are far from out of the woods, and we cannot yet be complacent about this correction.

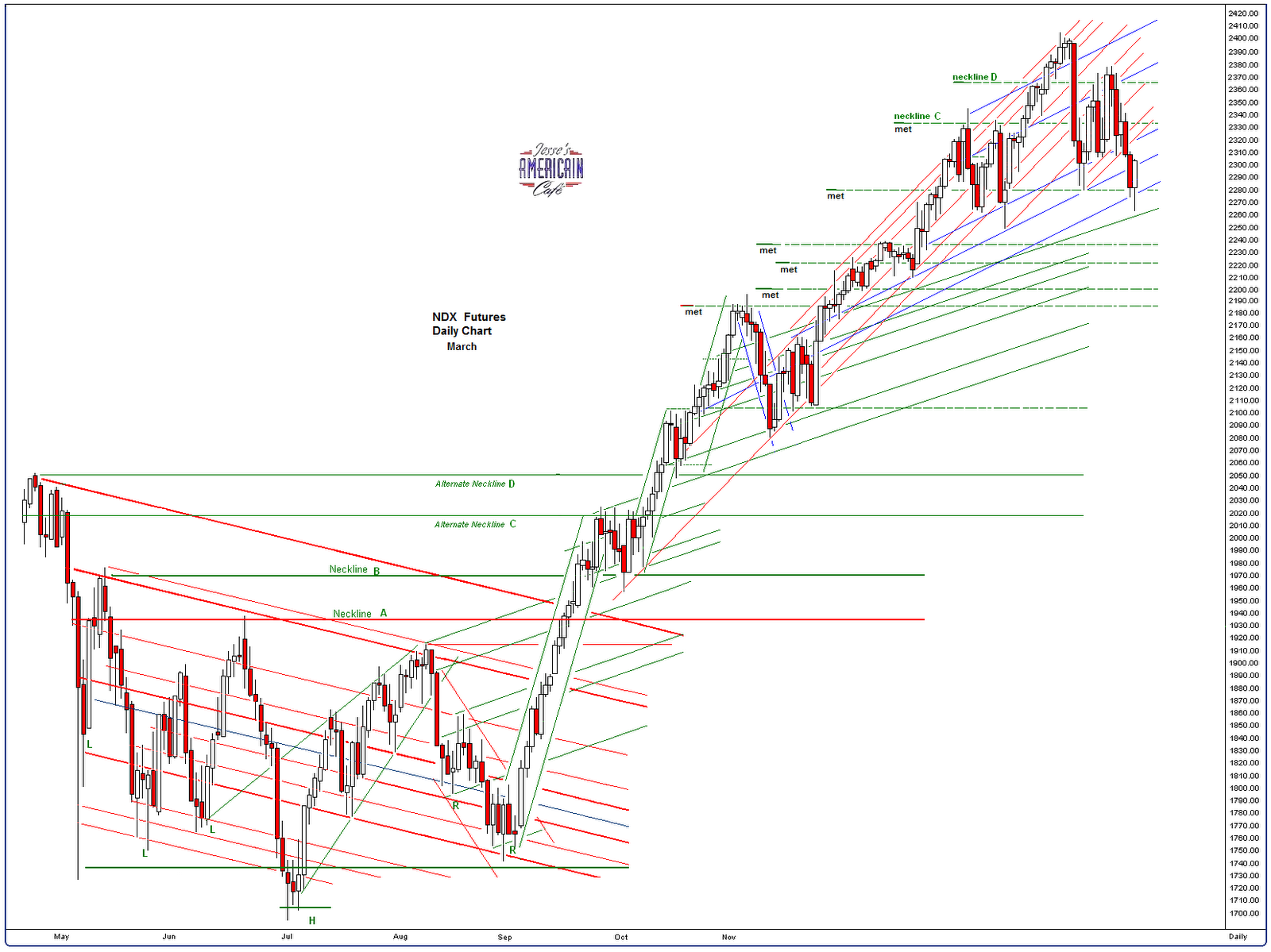

Defensive positions are recommended until the uptrend is re-established. While it was heartening to see the SP 500 climb back above its 50 DMA which is now around 1299, the NDX tech sector is still lagging withits 50 DMA around 2317, and this is the chart that I watch, in addition to financials and the Russell 2000, to judge the quality of any rallies. Too often they will jam the SP 500 futures higher and try to drag the rest of the market along with it.

I will be keenly interested in seeing the full extent of the damage in Japan, and any follow on problems to a quake of this magnitude, especially with regard to their nuclear infrastructure. I am sure they will handle it as they have done so many times in the past, rising as one people to the challenge. There will be many comparisons to how the markets reacted to the Kobe earthquake in the 1990's.

In terms of the US economy, there is no real recovery yet that I can determine. The earthquake of the financial crisis has left the country divided, its economy sputtering. Repairs have not been made, and those who created and benefited from the crisis are seeking conscripts to take their pain.

John Williams of Shadowstats had this to say:

"Markets Are Flying Blind.

In terms of meaningful economic reporting, the financial markets continue to be flying blind, at the moment. Economic data of questionable significance continue to flow from the government’s statistical bureaus, including this morning’s (March 11th) report of February retail sales. There will be a full review of the economic outlook in the Hyperinflation update, and the constant-dollar February retail sales will be assessed in the March 17th Commentary, following the CPI release.

On its surface, the February retail sales report was positive on a nominal (not-adjusted for inflation) basis, as well as likely in real (inflation-adjusted) terms. The reporting-quality problems remain in unstable monthly seasonal-factor adjustments. Seasonal patterns have been warped by the depth and duration of an economic downturn that is unprecedented in the post-World War II era of modern economic reporting. The retail data will be revised in a pending annual benchmark revision, scheduled for April 29th.

At that time, retail sales levels and growth of at least the last year should be subject to major downside revisions, showing a weaker economy than has been recognized previously. As with the recent, major downside revisions to payroll employment, and the pending downside revisions to industrial production later in March, the retail sales downgrade will be a precursor to major downside revisions in GDP history of the last several years, which are due for release in late July.

While there also are seasonal-adjustment issues with the trade data, the reported January 2011 deficit has set up a potential dampening of growth to be reported in first-quarter 2011 GDP, at the end of April."

|

| Weekend At Bennie's - Looking Good! |