skip to main |

skip to sidebar

NYT Dealbook

Regulators Investigating MF Global

By BEN PROTESS, MICHAEL J. DE LA MERCED and SUSANNE CRAIG

Federal regulators have discovered that hundreds of millions of dollars in customer money have gone missing from MF Global in recent days, prompting an investigation into the company’s operations as it filed for bankruptcy on Monday, according to several people briefed on the matter.

The revelation of the missing money scuttled an 11th hour deal for MF Global to sell a major part of itself to a rival brokerage firm. MF Global, the powerhouse commodities brokerage run by Jon S. Corzine, had staked its survival on completing the deal.

Now, the investigation threatens to tarnish the reputation of Mr. Corzine, the former New Jersey Governor and Goldman Sachs chief who oversaw MF Global’s demise, making it the first American victim of Europe’s debt crisis.

What began as nearly $1 billion missing had dropped to less than $700 million by late Monday. It is unclear where the money went, and some money is expected to trickle in over the coming days as the firm sorts through the bankruptcy process, the people said....

Read the rest of the story here.

Kleptocracy, "rule by thieves" is a form of political and government corruption where the government exists to increase the personal wealth and political power of its officials and the ruling class at the expense of the wider population, often without pretense of honest service.

No outside oversight is possible, due to the ability of the kleptocrats to personally control both the supply of public funds and the means of determining their disbursal.

Is this the long awaited gut check for the longs?

A natural pullback after such a strong rally.

Let's see where it goes next.

|

| "Related Disciplines" |

A strong October as one of the most dangerous of market trading months goes.

Keep an eye on Europe.

This market is triple black diamond, full of hidden risks, much of it caused by corruption and lax regulation.

"There will come a moment when the most urgent threats posed by the credit crisis have eased and the larger task before us will be to chart a direction for the economic steps ahead. This will be a dangerous moment. Behind the debates over future policy is a debate over history—a debate over the causes of our current situation. The battle for the past will determine the battle for the present. So it’s crucial to get the history straight."

Joseph Stiglitz, Capitalist Fools, January 2009

What I find to be of primary concern is that the prescriptions now being circulated for a cure to the economic malaise is more of the same things that caused the financial crisis in the first place, with the addition of more pain for the middle class and the relatively innocent victims of calculated fraud.

The elite are attempting to rewrite history, and promote a field of servile stooges as candidates in the next election for their selfish benefits. And sadly for the nation, for what I believe will prove to be a tearing of the social fabric.

“People of privilege will always risk their complete destruction rather than surrender any material part of their advantage."

John Kenneth Galbraith

Read the original posting from December 2008 about this essay here.

Here is a summation of the Five Major Causes of our financial crisis. As Joe so correctly observes:

- Reagan's nomination of Alan Greenspan to replace Paul Volcker as Fed Chairman

- The Repeal of Glass-Steagall and the Cult of Self-Regulation

- Bush Tax Cuts for Upper Income Individuals, Corporations, and Speculation

- Failure to Address Rampant Accounting Fraud Driven by Excessive and Flawed Compensation Models

- Providing Enormous Bailouts to the Banks without Engaging Systemic Reform for the Underlying Causes of the Failure

There are other points that might be added, some that are not strictly financial in nature.

An international monetary exchange system that facilitates manipulation to create de facto barriers and subsidies in support of industrial trade policies. This creates destabilizing surpluses and deficits which may be the source of the next stage of the financial crisis.

The concentration of the ownership of the mainstream media in a handful of corporations has had a chilling effect on the newsrooms and commentators.

The lack of Congressional courage in exercising its obligations with regard to the extra-Constitutional excesses of the Executive Office. Certain mechanisms and instruments that facilitate the unilateral exercise of presidential power are tipping the balance of powers.

The existing system of funding inordinately expensive political campaigns is a breeding ground for favors and corruption.

The undue influence on prices, particularly global commodity prices, that is exercised by a handful of US banks operating far outside of traditional banking charters. This is a dangerously destabilizing influence on the real world economy and industrial growth and investment.

A significant step forward would be the imposition of position limits, greater and more timely transparency for those with more than 10% of any market's open interest, and an uptick rule with stronger enforcement against naked shorting and other forms of short term price manipulation.

Vanity Fair

Vanity Fair

The Economic Crisis:

Capitalist Fools

by Joseph E. Stiglitz

January 2009

Behind the debate over remaking U.S. financial policy will be a debate over who’s to blame. It’s crucial to get the history right, writes a Nobel-laureate economist, identifying five key mistakes—under Reagan, Clinton, and Bush II—and one national delusion.

There will come a moment when the most urgent threats posed by the credit crisis have eased and the larger task before us will be to chart a direction for the economic steps ahead. This will be a dangerous moment. Behind the debates over future policy is a debate over history—a debate over the causes of our current situation. The battle for the past will determine the battle for the present. So it’s crucial to get the history straight.

What were the critical decisions that led to the crisis? Mistakes were made at every fork in the road—we had what engineers call a “system failure,” when not a single decision but a cascade of decisions produce a tragic result. Let’s look at five key moments.

No. 1: Firing the Chairman

In 1987 the Reagan administration decided to remove Paul Volcker as chairman of the Federal Reserve Board and appoint Alan Greenspan in his place. Volcker had done what central bankers are supposed to do. On his watch, inflation had been brought down from more than 11 percent to under 4 percent. In the world of central banking, that should have earned him a grade of A+++ and assured his re-appointment. But Volcker also understood that financial markets need to be regulated. Reagan wanted someone who did not believe any such thing, and he found him in a devotee of the objectivist philosopher and free-market zealot Ayn Rand.

Greenspan played a double role. The Fed controls the money spigot, and in the early years of this decade, he turned it on full force. But the Fed is also a regulator. If you appoint an anti-regulator as your enforcer, you know what kind of enforcement you’ll get. A flood of liquidity combined with the failed levees of regulation proved disastrous.

Greenspan presided over not one but two financial bubbles. After the high-tech bubble popped, in 2000–2001, he helped inflate the housing bubble. The first responsibility of a central bank should be to maintain the stability of the financial system. If banks lend on the basis of artificially high asset prices, the result can be a meltdown—as we are seeing now, and as Greenspan should have known. He had many of the tools he needed to cope with the situation. To deal with the high-tech bubble, he could have increased margin requirements (the amount of cash people need to put down to buy stock). To deflate the housing bubble, he could have curbed predatory lending to low-income households and prohibited other insidious practices (the no-documentation—or “liar”—loans, the interest-only loans, and so on). This would have gone a long way toward protecting us. If he didn’t have the tools, he could have gone to Congress and asked for them.

Of course, the current problems with our financial system are not solely the result of bad lending. The banks have made mega-bets with one another through complicated instruments such as derivatives, credit-default swaps, and so forth. With these, one party pays another if certain events happen—for instance, if Bear Stearns goes bankrupt, or if the dollar soars. These instruments were originally created to help manage risk—but they can also be used to gamble. Thus, if you felt confident that the dollar was going to fall, you could make a big bet accordingly, and if the dollar indeed fell, your profits would soar. The problem is that, with this complicated intertwining of bets of great magnitude, no one could be sure of the financial position of anyone else—or even of one’s own position. Not surprisingly, the credit markets froze.

Here too Greenspan played a role. When I was chairman of the Council of Economic Advisers, during the Clinton administration, I served on a committee of all the major federal financial regulators, a group that included Greenspan and Treasury Secretary Robert Rubin. Even then, it was clear that derivatives posed a danger. We didn’t put it as memorably as Warren Buffett—who saw derivatives as “financial weapons of mass destruction”—but we took his point. And yet, for all the risk, the deregulators in charge of the financial system—at the Fed, at the Securities and Exchange Commission, and elsewhere—decided to do nothing, worried that any action might interfere with “innovation” in the financial system. But innovation, like “change,” has no inherent value. It can be bad (the “liar” loans are a good example) as well as good.

No. 2: Tearing Down the Walls

The deregulation philosophy would pay unwelcome dividends for years to come. In November 1999, Congress repealed the Glass-Steagall Act—the culmination of a $300 million lobbying effort by the banking and financial-services industries, and spearheaded in Congress by Senator Phil Gramm. Glass-Steagall had long separated commercial banks (which lend money) and investment banks (which organize the sale of bonds and equities); it had been enacted in the aftermath of the Great Depression and was meant to curb the excesses of that era, including grave conflicts of interest. For instance, without separation, if a company whose shares had been issued by an investment bank, with its strong endorsement, got into trouble, wouldn’t its commercial arm, if it had one, feel pressure to lend it money, perhaps unwisely? An ensuing spiral of bad judgment is not hard to foresee. I had opposed repeal of Glass-Steagall. The proponents said, in effect, Trust us: we will create Chinese walls to make sure that the problems of the past do not recur. As an economist, I certainly possessed a healthy degree of trust, trust in the power of economic incentives to bend human behavior toward self-interest—toward short-term self-interest, at any rate, rather than Tocqueville’s “self interest rightly understood.”

The most important consequence of the repeal of Glass-Steagall was indirect—it lay in the way repeal changed an entire culture. Commercial banks are not supposed to be high-risk ventures; they are supposed to manage other people’s money very conservatively. It is with this understanding that the government agrees to pick up the tab should they fail. Investment banks, on the other hand, have traditionally managed rich people’s money—people who can take bigger risks in order to get bigger returns. When repeal of Glass-Steagall brought investment and commercial banks together, the investment-bank culture came out on top. There was a demand for the kind of high returns that could be obtained only through high leverage and big risktaking.

There were other important steps down the deregulatory path. One was the decision in April 2004 by the Securities and Exchange Commission, at a meeting attended by virtually no one and largely overlooked at the time, to allow big investment banks to increase their debt-to-capital ratio (from 12:1 to 30:1, or higher) so that they could buy more mortgage-backed securities, inflating the housing bubble in the process. In agreeing to this measure, the S.E.C. argued for the virtues of self-regulation: the peculiar notion that banks can effectively police themselves. Self-regulation is preposterous, as even Alan Greenspan now concedes, and as a practical matter it can’t, in any case, identify systemic risks—the kinds of risks that arise when, for instance, the models used by each of the banks to manage their portfolios tell all the banks to sell some security all at once.

As we stripped back the old regulations, we did nothing to address the new challenges posed by 21st-century markets. The most important challenge was that posed by derivatives. In 1998 the head of the Commodity Futures Trading Commission, Brooksley Born, had called for such regulation—a concern that took on urgency after the Fed, in that same year, engineered the bailout of Long-Term Capital Management, a hedge fund whose trillion-dollar-plus failure threatened global financial markets. But Secretary of the Treasury Robert Rubin, his deputy, Larry Summers, and Greenspan were adamant—and successful—in their opposition. Nothing was done.

No. 3: Applying the Leeches

Then along came the Bush tax cuts, enacted first on June 7, 2001, with a follow-on installment two years later. The president and his advisers seemed to believe that tax cuts, especially for upper-income Americans and corporations, were a cure-all for any economic disease—the modern-day equivalent of leeches. The tax cuts played a pivotal role in shaping the background conditions of the current crisis. Because they did very little to stimulate the economy, real stimulation was left to the Fed, which took up the task with unprecedented low-interest rates and liquidity. The war in Iraq made matters worse, because it led to soaring oil prices. With America so dependent on oil imports, we had to spend several hundred billion more to purchase oil—money that otherwise would have been spent on American goods. Normally this would have led to an economic slowdown, as it had in the 1970s. But the Fed met the challenge in the most myopic way imaginable. The flood of liquidity made money readily available in mortgage markets, even to those who would normally not be able to borrow. And, yes, this succeeded in forestalling an economic downturn; America’s household saving rate plummeted to zero. But it should have been clear that we were living on borrowed money and borrowed time.

The cut in the tax rate on capital gains contributed to the crisis in another way. It was a decision that turned on values: those who speculated (read: gambled) and won were taxed more lightly than wage earners who simply worked hard. But more than that, the decision encouraged leveraging, because interest was tax-deductible. If, for instance, you borrowed a million to buy a home or took a $100,000 home-equity loan to buy stock, the interest would be fully deductible every year. Any capital gains you made were taxed lightly—and at some possibly remote day in the future. The Bush administration was providing an open invitation to excessive borrowing and lending—not that American consumers needed any more encouragement.

No. 4: Faking the Numbers

Meanwhile, on July 30, 2002, in the wake of a series of major scandals—notably the collapse of WorldCom and Enron—Congress passed the Sarbanes-Oxley Act. The scandals had involved every major American accounting firm, most of our banks, and some of our premier companies, and made it clear that we had serious problems with our accounting system. Accounting is a sleep-inducing topic for most people, but if you can’t have faith in a company’s numbers, then you can’t have faith in anything about a company at all. Unfortunately, in the negotiations over what became Sarbanes-Oxley a decision was made not to deal with what many, including the respected former head of the S.E.C. Arthur Levitt, believed to be a fundamental underlying problem: stock options. Stock options have been defended as providing healthy incentives toward good management, but in fact they are “incentive pay” in name only. If a company does well, the C.E.O. gets great rewards in the form of stock options; if a company does poorly, the compensation is almost as substantial but is bestowed in other ways. This is bad enough. But a collateral problem with stock options is that they provide incentives for bad accounting: top management has every incentive to provide distorted information in order to pump up share prices.

The incentive structure of the rating agencies also proved perverse. Agencies such as Moody’s and Standard & Poor’s are paid by the very people they are supposed to grade. As a result, they’ve had every reason to give companies high ratings, in a financial version of what college professors know as grade inflation. The rating agencies, like the investment banks that were paying them, believed in financial alchemy—that F-rated toxic mortgages could be converted into products that were safe enough to be held by commercial banks and pension funds. We had seen this same failure of the rating agencies during the East Asia crisis of the 1990s: high ratings facilitated a rush of money into the region, and then a sudden reversal in the ratings brought devastation. But the financial overseers paid no attention.

No. 5: Letting It Bleed

The final turning point came with the passage of a bailout package on October 3, 2008—that is, with the administration’s response to the crisis itself. We will be feeling the consequences for years to come. Both the administration and the Fed had long been driven by wishful thinking, hoping that the bad news was just a blip, and that a return to growth was just around the corner. As America’s banks faced collapse, the administration veered from one course of action to another. Some institutions (Bear Stearns, A.I.G., Fannie Mae, Freddie Mac) were bailed out. Lehman Brothers was not. Some shareholders got something back. Others did not.

The original proposal by Treasury Secretary Henry Paulson, a three-page document that would have provided $700 billion for the secretary to spend at his sole discretion, without oversight or judicial review, was an act of extraordinary arrogance. He sold the program as necessary to restore confidence. But it didn’t address the underlying reasons for the loss of confidence. The banks had made too many bad loans. There were big holes in their balance sheets. No one knew what was truth and what was fiction. The bailout package was like a massive transfusion to a patient suffering from internal bleeding—and nothing was being done about the source of the problem, namely all those foreclosures. Valuable time was wasted as Paulson pushed his own plan, “cash for trash,” buying up the bad assets and putting the risk onto American taxpayers. When he finally abandoned it, providing banks with money they needed, he did it in a way that not only cheated America’s taxpayers but failed to ensure that the banks would use the money to re-start lending. He even allowed the banks to pour out money to their shareholders as taxpayers were pouring money into the banks.

The other problem not addressed involved the looming weaknesses in the economy. The economy had been sustained by excessive borrowing. That game was up. As consumption contracted, exports kept the economy going, but with the dollar strengthening and Europe and the rest of the world declining, it was hard to see how that could continue. Meanwhile, states faced massive drop-offs in revenues—they would have to cut back on expenditures. Without quick action by government, the economy faced a downturn. And even if banks had lent wisely—which they hadn’t—the downturn was sure to mean an increase in bad debts, further weakening the struggling financial sector.

The administration talked about confidence building, but what it delivered was actually a confidence trick. If the administration had really wanted to restore confidence in the financial system, it would have begun by addressing the underlying problems—the flawed incentive structures and the inadequate regulatory system.

Was there any single decision which, had it been reversed, would have changed the course of history? Every decision—including decisions not to do something, as many of our bad economic decisions have been—is a consequence of prior decisions, an interlinked web stretching from the distant past into the future. You’ll hear some on the right point to certain actions by the government itself—such as the Community Reinvestment Act, which requires banks to make mortgage money available in low-income neighborhoods. (Defaults on C.R.A. lending were actually much lower than on other lending.) There has been much finger-pointing at Fannie Mae and Freddie Mac, the two huge mortgage lenders, which were originally government-owned. But in fact they came late to the subprime game, and their problem was similar to that of the private sector: their C.E.O.’s had the same perverse incentive to indulge in gambling.

The truth is most of the individual mistakes boil down to just one: a belief that markets are self-adjusting and that the role of government should be minimal. Looking back at that belief during hearings this fall on Capitol Hill, Alan Greenspan said out loud, “I have found a flaw.” Congressman Henry Waxman pushed him, responding, “In other words, you found that your view of the world, your ideology, was not right; it was not working.” “Absolutely, precisely,” Greenspan said. The embrace by America—and much of the rest of the world—of this flawed economic philosophy made it inevitable that we would eventually arrive at the place we are today.

I was out most of the day.

The markets were quiet, digesting the recent developments in the US domestic economy, but especially with the European debt situation.

See you Monday.

The 'gut check' in metals was very short-lived, as the precious metals rallied with the melt up in financial assets on the debt monetization plans out of Europe to save their banks. It was 'risk on.'

What next? We may have some follow on, but continued upside depends on additional QE3 from the Fed, as well as the actions by all the world's central banks to monetize the private banking debt and inflate their currencies.

The metals will do well in this kind of an environment. But the sailing is not yet clear. There will likely be more upside after corrections, but if this works, then the major test will come with the December option expiration.

As a reminder I will be out of pocket tomorrow and will not be looking at emails or the markets, probably not until late night or Saturday.

A massive rally in US equities today led by financials as there was relief that Europe will be bailing out the sovereign debt of some of their members, and most importantly of all, the large European and US banks.

The US GDP came in well. Intraday commentary was provided, and it was a hollow victory as household income continued to decline.

I think the stock rally may have more to go, but it might take QE3 to take it much higher into year end. And if we do get QE3, we then go into bubble watch as financial assets inflate at the expense of the real economy.

This is what happens when one applies monetary stimulus to a broken economy.

One picture is worth a thousand words...

Buffaloed Tim and Howdy Bernanke

Another nice up day in the metals running a bit counter to commodities.

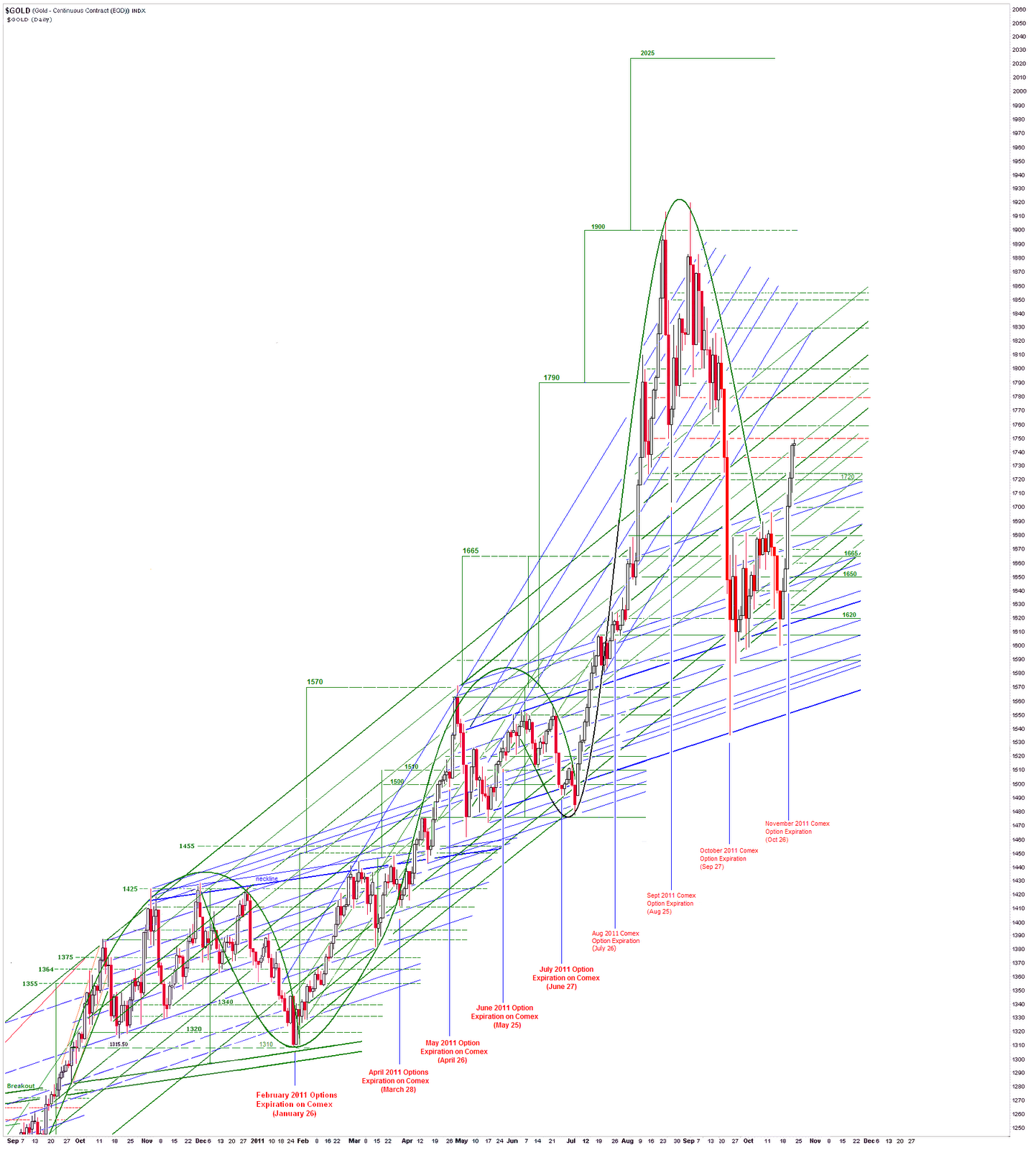

Gold finished around the big resistance of 1720. Today was a quiet expiration and it may be that the new holders of futures, compliments of their 'in the money' calls, will be given a gut check tomorrow or the next day.

But the news and the headlines from Europe are so dominant in this market that this is the primary driver, and most other things are secondary.

I put my own portfolio in a defensive position into the close. I will be out of pocket almost all day on Friday so there will be no updates until very late, or on Saturday.

A bit of a drift higher with a short squeeze based on a report (rumor) that China will ride in on a white horse and bail out Europe by buying their euro bonds.

This is a very mixed market and headline driven. So we wait for the next headline which is what it will take to fuel a sustained rally if it is favorable and substantial.

I think this is a superb list, but a bit misdirected, because as is obvious from my title, the advice ought not to go to the Fed, but to the government in Washington. Timmy is Ben's colleague and quasi-boss, and the problems are intertwined.

That takes nothing from Bill Black who would be an appropriate choice to head one of the big regulatory agencies. And it is unlikely that Obama would appoint him.

The Fed is a critical part of the problem, and is unable to reform itself because it is owned by the banks and the monied interests.

But so is Washington. And that is a matter for a much deeper discussion on the crying need for serious political reform, and how it might be achieved.

They will throw out a landscaper's nightmare of tangled branches, but the key is to strike at the root of it, which is campaign finance reform and the access to power of organized money, and the personal benefits received therein by politicians.

This may not happen now, and the pampered princes of the political aristocracy may put it off yet again. But it will almost certainly happen, one way or the other, after the next financial crisis.

The tragedy is that much of this is within Obama's reach, despite his problems with a fanatical element in the Congress. His priority now is four more years, and to accomplish that he is taking money and orders from the Wall Street bankers.

«Le papier-monnaie revient finalement à sa valeur intrinsèque - Zéro.»

Voltaire

Turk and Keiser Discuss the French Experience with L'illusion de la Monnaie Fiduciaire

"Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one."

Charles Mackay

The US is remarkable, not for any unusual distribution of psychopaths amongst its people, but rather for the high regard and admiration in which the more articulate and successful psychopaths and sociopaths among their ranks are held by the public, their natural prey.

The problem is not that there are disturbed and destructive people in a society. The problem is when they are able to subvert a culture to satisfy their goals, when their animalistic cunning and heartlessness becomes fashionable, imitated, and even respected.

It is surely the greatest triumph of madness over common sense since the self-destruction of nations in the 20th century. Whole peoples surrendered themselves to ruthless leaders, thrilled to be ravaged by power without weakness. They drank deeply from the cup of madness and danced with the culture of death. And that is what it is to be without boundaries or constraints, free as gods on earth.

"He may have destroyed men, women, and children, and condemned thousands of families to homelessness and despair, but he never wavered in his resolve and conviction while doing it. He amassed great power and fortune, and he never got caught. He believed in himself, and he's a winner."

"The manipulative con-man. The guy who lies to your face, even when he doesn’t have to. The child who tortures animals. The cold-blooded killer. Psychopaths are characterised by an absence of empathy and poor impulse control, with a total lack of conscience.

About 1% of the total population can be defined as psychopaths, according to a detailed psychological profile checklist. They tend to be egocentric, callous, manipulative, deceptive, superficial, irresponsible and parasitic, even predatory.

The majority of psychopaths are not violent and many do very well in jobs where their personality traits are advantageous and their social tendencies tolerated. However, some have a predisposition to calculated, “instrumental” violence; violence that is cold-blooded, planned and goal-directed.

Psychopaths are vastly over-represented among criminals; it is estimated they make up about 20% of the inmates of most prisons. They commit over half of all violent crimes and are 3-4 times more likely to re-offend. They are almost entirely refractory to rehabilitation. These are not nice people.

So how did they get that way? Is it an innate biological condition, a result of social experience, or an interaction between these factors?

Longitudinal studies have shown that the personality traits associated with psychopathy are highly stable over time. Early warning signs including “callous-unemotional traits” and antisocial behaviour can be identified in childhood and are highly predictive of future psychopathy.

Large-scale twin studies have shown that these traits are highly heritable – identical twins, who share 100% of their genes, are much more similar to each other in this trait than fraternal twins, who share only 50% of their genes. In one study, over 80% of the variation in the callous-unemotional trait across the population was due to genetic differences. In contrast, the effect of a shared family environment was almost nil.

Psychopathy seems to be a lifelong trait, or combination of traits, which are heavily influenced by genes and hardly at all by social upbringing.

The two defining characteristics of psychopaths, blunted emotional response to negative stimuli, coupled with poor impulse control, can both be measured in psychological and neuroimaging experiments...They do not seem to process heavily loaded emotional words, like “rape”, for example, any differently from how they process neutral words, like “table”.

This lack of response to negative stimuli can be measured in other ways, such as the failure to induce a galvanic skin response (heightened skin conduction due to sweating) when faced with an impending electrical shock...

The psychopath really just doesn’t care. In this, psychopaths differ from many people who are prone to sudden, impulsive violence, in that those people tend to have a hypersensitive negative emotional response to what would otherwise be relatively innocuous stimuli."

Craig, M., Catani, M., Deeley, Q., Latham, R., Daly, E., Kanaan, R., Picchioni, M., McGuire, P., Fahy, T., & Murphy, D. (2009). Altered connections on the road to psychopathy Molecular Psychiatry, 14 (10), 946-953 DOI: 10.1038/mp.2009.40

"And remember, where you have the concentration of power in a few hands, all too frequently men with the mentality of gangsters get control. History has proven that."

Lord Acton

Income inequality such that it suppresses the middle class is a practical policy problem for what I hope are obvious reasons of inadequate demand and economic stagnation. As the US currently has one of the most extreme income distributions since the Great Depression it is currently a topic of renewed interest.

Mark Thoma has an interesting discussion of this here: Income Inequality Is Hobbling the Middle Class

But in addition to this more practical discussion, Matt Taibbi brings out a key point in his most recent essay on the financial crisis. It is not so much the inequality per se that is troubling people, but rather the concomitant gaming of the system, the blatant cheating, that is making people angry.

"When you take into consideration all the theft and fraud and market manipulation and other evil shit Wall Street bankers have been guilty of in the last ten-fifteen years, you have to have balls like church bells to trot out a propaganda line that says the protesters are just jealous of their hard-earned money...At last count, there were 245 millionaires in congress, including 66 in the Senate. And we hate the rich? Come on. Success is the national religion, and almost everyone is a believer. Americans love winners. But that's just the problem. These guys on Wall Street are not winning – they're cheating. And as much as we love the self-made success story, we hate the cheater that much more."

OWS's Beef: Wall Street Isn't Winning – It's Cheating - Matt Taibbi

The perception is that the US has slipped from meritocracy to oligarchy, with the implications for long term growth and competitiveness of course. Oligarchies are quite often a study in stagnation and decline, plagued by idiot sons and frivolous dissipation of wealth and vitality. It is the deep capture and ravaging of the American dream by dishonest and dishonorable men.

But in what is nominally still a democratic republic, the rise of an oligarchy is a tearing of the social fabric with some serious long term consequences. And there will be a serious price to pay if dissent and efforts at reform are further suppressed.

If legitimate criticism and reform is stifled, rising domestic turmoil often results in a change of regime, or at least a shifting of power. We are seeing this in various countries across the world as the great empire totters. But sometimes the local bully boys are able to suppress domestic dissent, and so other interested but exogenous parties become involved. We most recently have seen this in Libya for example.

If the rest of the world acts first, and expresses its revulsion at the long endured abuses of the Anglo-American banking cartel, we may see a flight from a capital system gone rotten, with all the chaos and wealth destruction and death of innocence that this implies.

This is the most probable scenario for a hyperinflation that I can imagine.

"Turn where we may, within, around, the voice of great events is proclaiming to us, Reform, that you may preserve."

Thomas B. Macaulay

It was 'risk off' today as domestic economic news was weak and Euro-optimism was subdued.

There was intraday commentary on today's somewhat unusual rally in gold and silver here.

The economy in the US continues to weaken, and the political leadership seems preoccupied with doing more trickle down favors for their wealthy contributors.

There was an interesting divergence as gold and silver were up sharply as stocks were lower. That's a change of pace.

Tomorrow is the November option expiration on the Comex. I discussed this intra-day here.

Markets took a pause today on less optimism on Europe and domestic US recovery.

Keep an eye on the sovereign debt situation in Europe because that is a primary short term driver of this market.

Amazon missed and lowered after the bell, and so is getting hammered a bit in the late trade.

The US economy is not recovering and the plans being put forward for change are not likely to help anyone but those who are already fortunate, which does little for the economy but is a great source of personal income for the pigmen and their support system.

Keep an eye out for the next two Comex option expirations in the metals, both tomorrow 26 October but in particular the December expiry on 22 November. Perhaps not so much tomorrow but the days after. And of course December is a key month. I see resistance at 1720 that may prove to be important.

And never forget how the metals markets were ruthlessly slammed down into the October expiration on Sept 27, when the shills and apologists for the banks and hedge funds tell you how sound and fair the markets are, and denounce any evidence to the contrary.

Sometimes it seems that, as Chris Powell so astutely observed, "there are no markets anymore, just interventions."

This is what Markopolos faced when attempting to expose the great Madoff fraud, and it repeats almost endlessly in times of sanctioned corruption. Evidence is gathered by outsiders, presentations are made and ignored, the testimony of whistleblowers is ridiculed and even assaulted, the fraudulent scheme falls in a collapse, the public is tasked to absorb the losses and insiders keep their gains, and the many enablers move on as the public is distracted and forgets.

Nothing will change while crime pays. And even as things change, reform is taken away from the hands of the people, and carefully managed in back rooms and private deals.

"The most dangerous moment for a bad government is when it begins to reform."

Alexis de Tocqueville

Those in positions of authority and beneficiaries of the status quo understand this well. That is the credibility trap that is the impediment to recovery. Reform is an impulse to be carefully managed and directed by the insiders, and those who are implicated in corruption and sometimes even great crimes. The benefits of genuine reform are secondary to the appearance that 'something is being done.'

And if the charade goes on long enough, the people begin to take to the public squares and the streets, because they are otherwise being ignored, betrayed and abused.

The moment is most dangerous when the decision is made whether to answer the people with change, or stifle their just complaints with repression. Then the die is cast, and the great moment of history truly begins.

It is good to see gold open interest on the Comex at relatively low levels here, as the commercials continue to cover ahead of the enactment of position limits, projected to occur in the first month of 2012.

"The desire of gold is not for gold. It is for the means of freedom and knowledge."

Ben Davies

Gold and silver diverged from US equities today as fresh jitters over the Euro bailout put a damper on stocks.

Keep the $45+ rally in context of the current trading range however as is shown below. It has not yet broken out.

If you are trading with Level II market view in something like the miners or a less liquid ETF, you may place a bid or ask of a thousand shares or more, and it quickly finds a lot of 'friends' of a lesser amount jumping in front of it. And when you place a sell into a group of bids, a tiny amount may be filled, but then the bids disappear and drop lower.

These are thin, volatile markets, permeated by fraud, deception, and front-running of everything from global headlines down to individual bids. The talking heads and Wall Street demimonde are spinning stories and alternatively feeding hysteria and euphoria, greed and fear, under cover of the lax regulation and co-opted public policy.

The US financial system has gone predatory. The political system has given itself over to the corporate interests. Nothing could be more clear in the regressive tax proposals coming out of the Republican debates, and the Democrats are feeding greedily at the same trough of foul campaign funds and special privileges.

If you are a daytrader and can make money playing the momentum in this then good for you. But I think that most people who attempt to trade these markets will make very little on net, and are more likely to lose money. Better to stay with the longer term trends based on fundamentals. This will get worse before it gets better.

Markets were cheered by a better than expected economic activity report from China and good earnings from CAT. Europe was forgotten for the day.

Gold and Silver had decent gains as the dollar slumped.

The trend is not clear here and the breakouts are still pending.

Big up day but on light volumes.

CAT earnings provided the domestic push, and better than expected data from China cooled fears of global recession.

The punters were whistling pass the graveyard on Euro debt today.

Let's see if they can break stocks out from here and make it stick ahead of the European meeting on Wednesday.

NFLX guided lower and was punished after the bell.

It was 'Risk On' today as stocks rallied and went out on their highs and gold followed.

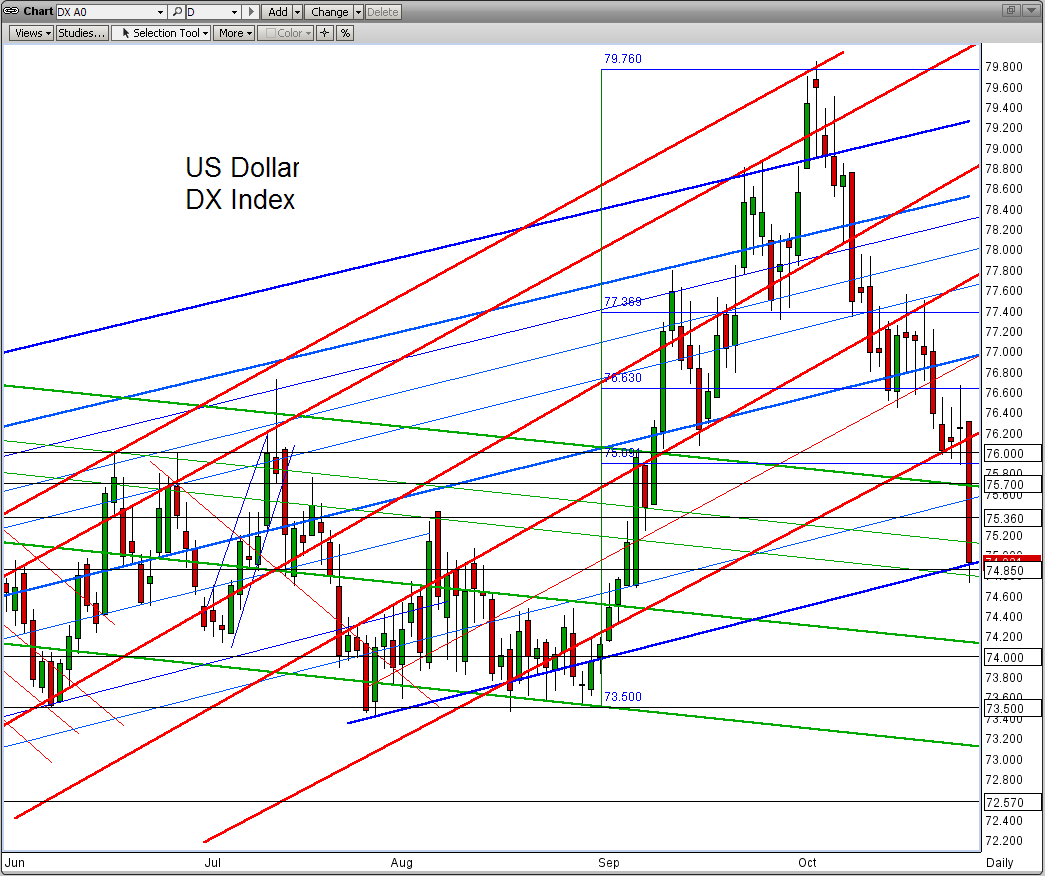

The US Dollar dropped to a post WW II low against the Yen on talk of QE3. I suspect strongly that someone in Treasury shared some prospective monetary actions with their Asian counterparts today. Apparently they are not so sanguine about the benign affects of modern monetary theory, even of the more benign and traditional Keynesian sort.

The Fed Is Laying the Groundwork for Further Easing - Thoma

Stimulus will not work in a system that remains unbalanced and broken, with the real economy skewed to support a non-productive financial class. And austerity will merely bring the final crash and counter reaction more quickly. It will not 'get it over with.' It is more like driving faster so you can impact with this bridge abutment rather than one further down the road. A flaming wreck is rarely a good outcome. We might consider fixing the car instead. But that would require a change of drivers.

See you Sunday night.

Wax on and Wax off for option expiration.

The Risk Trade was On today on words from the Fed's Yellen amongst others hinting at a new round of QE3 from the Fed. Expectations are high that Europe will bail out its banks via the PIGS sovereign debts, in the manner that the US bailed out the Wall Street banks both directly, and indirectly via AIG.

If you have Level II trading you may notice that whenever you post a bid you could be getting a lot of fast company depending on the size of it. At least this is my experience and it is becoming increasingly annoying. Today I was posting bids and asks of between 1000 to 5000 shares, just to see the kind of shenanigans from the various exchanges, and in dull stocks!

If this thing gets going to the downside it could be quite the spectacle. But Benny and the Boyz are in there bailing out the banks, make no mistake about it. Wall Street is Job One.

See you Sunday night. Here we go again.