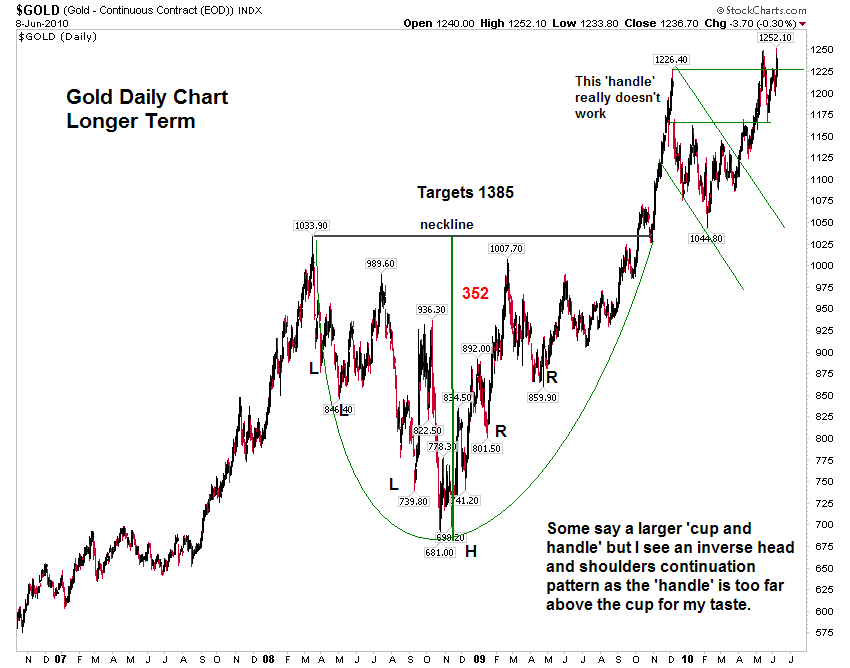

A friend and correspondent over at BullionVault reminded me the other day that some have been watching what they consider to be a larger cup and handle on the gold daily chart going back to 2008.

My depiction of that longer term chart formation is below.

I had carefully considered that interpretation last year but the handle formed much higher relative to the cup than I would prefer. Further, it did not form like a classic handle on the retracements. Instead I considered it to be a simple inverse Head and Shoulders continuation pattern in this bull market, from the extreme selling in the liquidity crisis.

The patterns have similar pricing objectives, unless you draw the lines as diagonals and attempt to measure off the top of the handle. Either way, each is a chart formation that is active and working with objectives north of where the cash price is today.

There are two reasons to use a cup and handle versus an inverse H&S. The first is that the breakout action on the handle is more easily charted and evaluated. A breakout through the neckline of any H&S is merely a binary event, whereas a handle permits more gradation. Head and Shoulder patterns are simple creatures. The second reason is that some people do not believe that an inverse H&S is an appropriate continuation pattern, and can only be used for a clear 'bottom' of a downtrend. I obviously do not agree with the latter. They can often act as continuation patterns after a severe selloff in a bull market trend that remains intact.

And there is of course, with the advent of modern computerized charting tools, the temptation to overcomplicate a chart and fill the page with far too many lines and circles and diagonal relationships to the point of obscurity, as though a Euclid of Alexandria had thrown up a lifetime of drawing on a basic price chart.

As an aside, sometimes readers will say things like 'So and So is a respected chart authority and he says...' And this is provided without justification, on the basis of authority. Well, one must always listen respectfully to learned opinions, but then look carefully at the empirical evidence, in a scientific manner, which in my book trumps theory and the 'rules' made by men.

When I was working at Bell Labs a very learned and internationally respected authority (and my boss' boss which was the ultimate power of that bureaucracy) told me that I "obviously did not understand information theory" when I presented the case for developing higher speed modems (> 9600 bps) , Digital Subscriber Line technology, and high speed local area transmission over unshielded twisted pairs, well in advance of their formative discussions on the CCITT and US IEEE committees. In other words, I have made my career in not accepting the conventional wisdom and authority of the day. Sometimes what you think you know prepares you for a world that no longer exists, because it was an illusion. And that goes double for macroeconomics, which seems now more like marketing than mathematics, more astrology than physics. The US financial system is largely a confidence game, or more appropriately a racket dominated by rival white collar crime gangs.

And that goes double for macroeconomics, which seems now more like marketing than mathematics, more astrology than physics. The US financial system is largely a confidence game, or more appropriately a racket dominated by rival white collar crime gangs.

Far too many economists tell people what they wish to hear, or what their masters are promoting, and attempt to give it the trappings of respectability with professional jargon, self-referential theories and elaborate faux proofs, with the trappings of equations based on falsified assumptions. If you want to measure a contemporary economist, see what they are saying, if anything, about reforming and restructuring the financial system.

A government needs to decide first what sort of nation it wishes to be, and then use economics as one means of sorting out more granular choices among policy decisions. To treat economics as a primary determinant of social policy is to perpetuate the hoax of the efficient markets hypothesis and the inherent goodness of 'free trade.' But it does helps economists to gain funding from the plutocrats, and serves to divert the public from the discussion of meaningful reforms.

Finally, at this point in my third career, I AM a 'chart authority' of sorts in my little circle, and it is my money on the line when I am investing, so I think I have some say, at least in my own kitchen, as long as she-who-must-be-considered is out front. lol.

Here is a picture of the pullback on the cup and handle we have been watching for the past few weeks. So far it is as expected.

09 June 2010

Gold Bulls Are In Their Cups and the Bull Market in Confidence Games and Voodoo Economics

17 April 2010

Wealth Dispersion and General Thoughts on the Future of Economics on a Saturday Afternoon

Here is an interesting graph of wealth distribution, or dispersion, as I call it from Cherchez La Verite.

I am not sure I agree with his conclusions or even his premise, not because I disagree but because it requires some thinking and leisure to digest it. But the data is most interesting.

I wonder if any of the quant economists have performed simulations on virtual populations, and then examined the results of varying different tax rates, and concentrations of wealth because of fiscal policy and regulatory structure, among other things.

I have an hypothesis that great concentrations of wealth lead to economic stagnation, but I am afraid that I have not the means or the talent anymore to conduct that type of research.

The difficulty in a study like this is that the assumptions are greatly magnified into the results. If you assume certain buying, spending, and savings behaviours, the downstream impact can greatly alter, and even distort, the outcomes.

And when people reason through this verbally, rather than perform a structured simulation based on transactions, the distortions increase by an order of magnitude or more based on their own biases.

I used to create simulations like this all the time, for industrial and commercial purposes, and also did a decent amount of econometric modeling. So I am sure someone is doing it somewhere. But I suspect they are doing it in think tanks and places where the outcome is predetermined by the basis of their grant.

Concentrated wealth magnifies the needs and predispositions of the holder. Since the amount they require for basic necessities can only consume so much, one would think that the amount spend on the aggregate of necessities will eventually be reduced. And what they do with their excess of necessity wealth is going to be greatly influenced by their character. Are they a gambler, who inherited the wealth? Are they productive and beneficent? Are they dissolute and venal?

And what about government? Taxation can concentrate enormous wealth in the government. What sort of government does one have, or does one assume? Are they warlike, productive, redistributive, and how corrupt? What about corporations? They can be like small governments, and levy taxes through monopoly and persistent frauds. How are they managed? Corporations are not rational machines, as the efficient market hypothesis would probably presume. Indeed, corporations are often much worse than governments in terms of sheer blockheadedness, greed, and short-termism.

Hard to say. But there is a related field of study in decision making theory, which looks not at wealth but the distribution of decision making power in organizations. It is concerned with the validity and effectiveness of decisions made across a range of broader consensus to a narrow oligopoly and even a great man dictatorship.

The general observation I came to in this study was that decisions tend to be more valid depending on the quality of the information, the facility of the evaluation of it, or intelligence/learning/experience, less the biases and distortions.

A decision becomes a little better if the information is more widely dispersed and a variety of actors can exchange freely in increasing and refining it. There is a point of decision dispersion where the returns not only diminish, but become counterproductive because of the noise and inability of new actors to add value, and actually detract from the process. But finally what I found interesting is that in the aggregate personal error, bias and distortions tends to diminish quickly as a detractor from the result, assuming a non-homogeneous population with some independence of thought.

So too this same sort of study can be applied to the concentration of wealth, since wealth is power. But it is even more interesting because spending habits will vary since the percentage of spending on essentials changes much more slowly than wealth can increase.

And how one assesses the outcomes is also essential. What is thought to be a 'good outcome?' Not necessarily in a rough measure like aggregate GDP, but perhaps GDP with modifiers like the median wage, and a poverty level of essential spending. This is important because so often economic policy arguments are presented with the goal of optimizing short term GDP.

Alas, I have little hope that this will be done now, for the US has had a leadership role in quantitative economic studies, and their work has been twisted generally into the service of whores, robber barons, and gamblers as the speculative society reaches a crescendo. But some day this too will change.