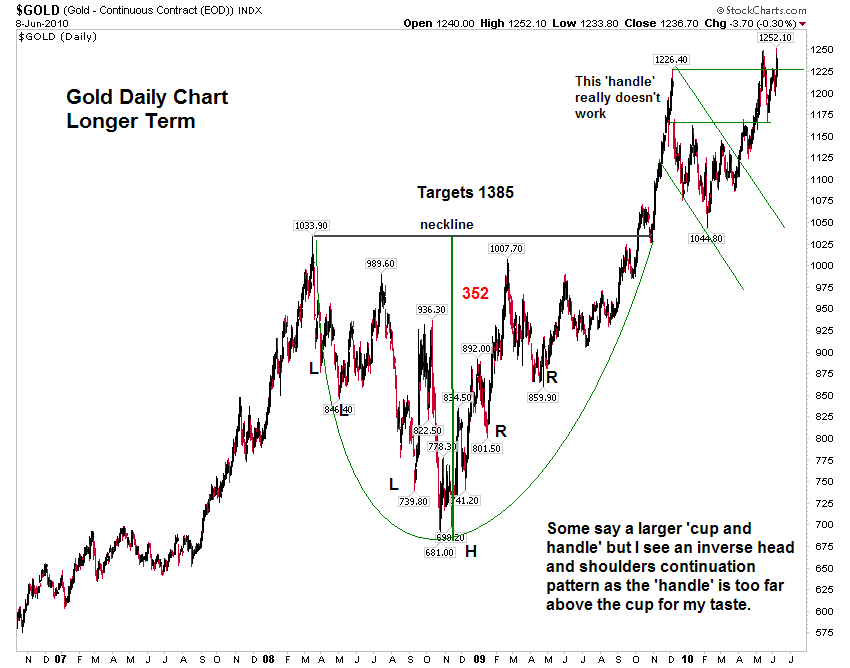

This interview with William Black in Barron's is an articulate and reasonably detailed summary of our own view of the current crisis from an exceptionally well-informed and experienced source.

The big question in our own mind is the depth of complicity and the motivations of the government, the media and major institutions in continuing to support this financial corruption through silence or participation.

Is Obama really merely listening to the wrong advice from highly placed sources in the Democratic Party? And how sincere are they? The record of corruption in the Obama Administration in the form of conflicts of interest and tax evasion is already the smoke that warns of fire.

All good questions, more relating to the length of time to a cure rather than its essential character.

The banks must be restrained, the financial system must be reformed, before there can be a sustained economic recovery.

Barron's

The Lessons of the Savings-and-Loan Crisis

By Jack Willoughby

11 April 2009

AN INTERVIEW WITH WILLIAM BLACK: The current bank scandal dwarfs the 1980s savings-and-loan crisis -- and could destroy the Obama presidency.

WILLIAM BLACK CALLS THEM AS HE SEES THEM, which is why we enjoy talking with him. Black, 57 years old, was a deputy director at the former Federal Savings and Loan Insurance Corp. during the thrift crisis of the 1980s, and now serves as an associate professor, teaching economics and law at the University of Missouri, Kansas City. At FSLIC, a government agency that insured S&L deposits, Black prevailed in showdowns with the powerful Democratic Speaker of the House, Jim Wright, and helped identify the infamous Keating Five, a group of U.S. senators (including Sen. John McCain, the Arizona Republican who lost his bid for the presidency in 2008) who tried to quash his attempt to close Charles Keating's Lincoln Savings & Loan. Wright eventually resigned amid unrelated ethics charges, and the senators were reprimanded for poor judgment. Keating went to jail for securities fraud.

For Black's provocative thoughts on the current financial crisis, read on.

Barron's: Just how serious is this credit crisis? What is at stake here for the American taxpayer?

Black: Mopping up the savings-and-loan crisis cost $150 billion; this current crisis will probably cost a multiple of that. The scale of fraud is immense. This whole bank scandal makes Teapot Dome [of the 1920s] look like some kid's doll set. Unless the current administration changes course pretty drastically, the scandal will destroy Barack Obama's presidency. The Bush administration was even worse. But they are out of town. This will destroy Obama's administration, both economically and in terms of integrity.

So you are saying Democrats as well as Republicans share the blame? No one can claim the high ground?

We have failed bankers giving advice to failed regulators on how to deal with failed assets. How can it result in anything but failure? If they are going to get any truthful investigation, the Democrats picked the wrong financial team. Tim Geithner, the current Secretary of the Treasury, and Larry Summers, chairman of the National Economic Council, were important architects of the problems. Geithner especially represents a failed regulator, having presided over the bailouts of major New York banks.

So you aren't a fan of the recently announced plan for the government to back private purchases of the toxic assets?

It is worse than a lie. Geithner has appropriated the language of his critics and of the forthright to support dishonesty. That is what's so appalling -- numbering himself among those who convey tough medicine when he is really pandering to the interests of a select group of banks who are on a first-name basis with Washington politicians.

The current law mandates prompt corrective action, which means speedy resolution of insolvencies. He is flouting the law, in naked violation, in order to pursue the kind of favoritism that the law was designed to prevent. He has introduced the concept of capital insurance, essentially turning the U.S. taxpayer into the sucker who is going to pay for everything. He chose this path because he knew Congress would never authorize a bailout based on crony capitalism.

Geithner is mistaken when he talks about making deeply unpopular moves. Such stiff resolve to put the major banks in receivership would be appreciated in every state but Connecticut and New York. His use of language like "legacy assets" -- and channeling the worst aspects of Milton Friedman -- is positively Orwellian. Extreme conservatives wrongly assume that the government can't do anything right. And they wrongly assume that the market will ultimately lead to correct actions. If cheaters prosper, cheaters will dominate. It is like Gresham's law: Bad money drives out the good. Well, bad behavior drives out good behavior, without good enforcement.

His plan essentially perpetuates zombie banks by mispricing toxic assets that were mispriced to the borrower and mispriced by the lender, and which only served the unfaithful lending agent.

We already know from the real costs -- through the cleanups of IndyMac, Bear Stearns, and Lehman -- that the losses will be roughly 50 to 80 cents on the dollar. The last thing we need is a further drain on our resources and subsidies by promoting this toxic-asset market. By promoting this notion of too-big-to-fail, we are allowing a pernicious influence to remain in Washington. The truth has a resonance to it. The folks know they are being lied to.

I keep asking myself, what would we do in other avenues of life? What if every time we had a plane crash we said: 'It might be divisive to investigate. We want to be forward-looking.' Nobody would fly. It would be a disaster.

We know that with planes, every time there is an accident, we look intensively, without the interference of politics. That is why we have such a safe industry.

Summarize the problem as best you can for Barron's readers.

With most of America's biggest banks insolvent, you have, in essence, a multitrillion dollar cover-up by publicly traded entities, which amounts to felony securities fraud on a massive scale.

These firms will ultimately have to be forced into receivership, the management and boards stripped of office, title, and compensation. First there needs to be a clearing of the air -- a Pecora-style fact-finding mission conducted without fear or favor. [Ferdinand Pecora was an assistant district attorney from New York who investigated Wall Street practices in the 1930s.] Then, we need to gear up to pursue criminal cases. Two years after the market collapsed, the Federal Bureau of Investigation has one-fourth of the resources that the agency used during the savings-and-loan crisis. And the current crisis is 10 times as large.

There need to be major task forces set up, like there were in the thrift crisis. Right now, things don't look good. We are using taxpayer money via AIG to secretly bail out European banks like Société Générale, Deutsche Bank, and UBS -- and even our own Goldman Sachs. To me, the single most obscene act of this scandal has been providing billions in taxpayer money via AIG to secretly bail out UBS in Switzerland, while we were simultaneously prosecuting the bank for tax fraud. The second most obscene: Goldman receiving almost $13 billion in AIG counterparty payments after advising Geithner, president of the New York Fed, and then-Treasury Secretary Henry Paulson, former Goldman Sachs honcho, on the AIG government takeover -- and also receiving government bailout loans.

What, then, is staying the federal government's hand? Have the banks become too difficult or complex to regulate?

The government is reluctant to admit the depth of the problem, because to do so would force it to put some of America's biggest financial institutions into receivership. The people running these banks are some of the most well-connected in Washington, with easy access to legislators. Prompt corrective action is what is needed, and mandated in the law. And that is precisely what isn't happening.

The savings-and-loan crisis showed that, too often, the regulators became too close to the industry, and run interference for friends by hiding the problems.

Can you explain your idea of control fraud, and how it applies to the current banking and the earlier thrift crisis?

Control fraud is when a seemingly legitimate corporation uses its power as a weapon to defraud or take something of value through deceit.

In the savings-and-loan crisis, thrifts engaged in control frauds in order to survive. Accounting trickery proved to be the weapon of choice. It is at work today with the banks, and it is their Achilles heel. You report that you are highly profitable when you engage in accounting-control fraud, not only meeting but exceeding capital requirements. These accounting frauds create huge bubbles, which in turn create large bonuses, which in turn lead to huge losses.

Why then is there so much smoke and so little action?

First, they are inundated by the problem. They are trying to investigate the major problems with severely depleted staffs. Honestly. We have lost the ability to be blunt. Now we have a situation where Treasury Secretary Geithner can speak of a $2 trillion hole in the banking system, at the same time all the major banks report they are well-capitalized. And you have seen no regulatory action against what amounts to a $2 trillion accounting fraud. The reason we don't see it -- aren't told about it -- is that if they were honest, prompt corrective action would kick in, and they would have to deal with the problem banks.

Are there any parallels between the current crisis and the savings-and-loan crisis that give you hope?

Of course. Objectively, our case was even more hopeless in the S&L debacle than in the current crisis. If we were able to do it in such an impossible circumstance back then, we have reason for hope in the current crisis. I know how easily things can get off course and how quickly things can turn back again. The thrift crisis went through several lengthy courses and distortions before it finally was resolved under the leadership of Edwin Gray, the chairman of the Federal Home Loan Bank Board, which oversaw FSLIC.

We went through almost a decade of cover-ups by a Washington establishment intent on helping thrift owners. Back then, we had the Justice Department threatening to indict Gray, the head of a federal agency, for closing too many thrifts. Next, there were those so-called resolutions, where the regulators worked day and night -- to create even bigger problems for the FSLIC. Years later, these so-called resolution deals had to be unwound at great expense by closing down even larger failures. Or how about the bill to replenish the depleted thrift-insurance fund that was blocked and delayed by then-Speaker of the House, Texas congressman Jim Wright?

You say the evidence of a breakdown in the regulatory structure comes from the fact that America avoided an earlier subprime crisis in the 1990s.

Exactly. Why had no one heard of the subprime crisis back in 1991? Because America's regulators also faced down the crisis early. The same thing happened with bad credits being securitized in the secondary market. Remember the low-doc or no-doc mortgages done by Citibank? Well, the problem didn't spread -- because regulators intervened.

Obama, who is doing so well in so many other arenas, appears to be slipping because he trusts Democrats high in the party structure too much.

These Democrats want to maintain America's pre-eminence in global financial capitalism at any cost. They remain wedded to the bad idea of bigness, the so-called financial supermarket -- one-stop shopping for all customers -- that has allowed the American financial system to paper the world with subprime debt. Even the managers of these worldwide financial conglomerates testify that they have become so sprawling as to be unmanageable.

What needs to be done?

Well, these international behemoths need to be broken down into smaller units that can be managed effectively. Maybe they can be broken up the way that the Standard Oil split up back in the early 1900s, through a simple share spinoff.

The big problem for the last decade is that we have had too much capacity in the finance sector -- too many banks have represented a drain on our talent and resources. All these mergers haven't taken capacity out of the system. They have created even bigger banks that concentrate risk to the taxpayer, and put off dealing with problems.

And a new seriousness must be put into regulation. We don't necessarily need new rules. We just need folks who can enforce the ones already on the books.

The bank-compensation system also creates an environment that leads to mismanagement and fraud. No one has to tell someone they have to stretch the numbers. It is all around them. It is in the rank-or-yank performance and retention systems advocated by top business executives. Here, the top 20% get the bulk of the benefits and the bottom 10% get fired. You don't directly tell your employees you want them to lie and cheat. You set up an atmosphere of results at any cost. Rank or yank. Sooner rather than later, someone comes up with the bright idea of fudging the numbers. That's big bonuses for the folks who make the best numbers. It sends the message -- making the numbers is what is most important. There is a reason that the average tenure of a chief financial officer is three years.

Compensation systems like I have just described discourage whistleblowing -- the most common way that frauds are found in America -- because the system draws upon the cooperation of everyone.

The basis for all regulation and white-collar crime is to take the competitive advantage away from the cheats, so the good guys can prevail. We need to get back to that.

Thanks, Bill.