"The more power a government has the more it can act arbitrarily according to the whims and desires of the elite, and the more it will make war on others and murder its foreign and domestic subjects. Power will achieve its murderous potential. It simply waits for an excuse, an event of some sort, an assassination, a massacre in a neighboring country, an attempted coup, a famine, or a natural disaster, to justify the beginning of murder en masse."

R. J. Rummel, Mass Murder and Genocide, 1994

The objective is nothing less than for the Anglo-American banking cartel to control the world's money supply. One major currency is almost as good as one world government.

MarketWatch Fitch May Cut Greece Debt to 'Junk'

By Sue Chang

December 21, 2010

SAN FRANCISCO (MarketWatch) -- Fitch Ratings on Tuesday placed Greece's BBB-long-term foreign- and local-currency issuer default ratings on downgrade review, raising the possibility that Greece's sovereign rating may be cut to junk in the near future. "A Rating Watch Negative indicates that there is a heightened probability that Greece's sovereign ratings will be downgraded," said Fitch in a statement. The review is expected to be completed in January and will focus on Greece's fiscal sustainability, the country's economic outlook and the political will of the government to carry out reforms, Fitch said.

"And Caesar's spirit, ranging for revenge,

With Ate by his side come hot from hell,

Shall in these confines with a monarch's voice

Cry 'Havoc!' and let slip the dogs of war;

That this foul deed shall smell above the earth

With carrion men, groaning for burial."

US equities seem to be drifting higher on very low volumes, led by the SP 500 futures which are reaching up for 1251, the better to paint a bright holiday season for the Wall Street insiders and their political cronies.

The primary industry in the US is now financial engineering (less euphemistically known as fraud), and it appears that business is still brisk and quite profitable despite the recent crisis.

I have some expectation of a rather sharp decline in equities, but I will not get out ahead of it, given the Fed's willingness to keep providing fresh dollars to their banking friends who are papering their way to prosperity at the expense of the many.

Bloomberg TV is running an interesting special on gold today titled "The Dark Side of Gold."

As one might expect it contains the usual claims that gold is in a bubble and poses a danger to the public in a variety of dimensions.

What I thought was a bit unique is that they are now blaming the entire gold rally on the creation of the GLD ETF.

Indeed, Carol Massar said today that before the gold ETF "gold was trading at $400 and the only people buying gold were conspiracy theorists who were hiding it in their pantries."

In her defense Carol, along with a number of the talking heads on financial TV, are just news readers, and one might as well blame the weatherman for reading the Weather Service forecasts.

But I don't suppose it might have occurred to whoever wrote this 'special report' to mention that the central banks, who had been steadily selling their gold reserves for the last twenty years, led by the US and England, had started to become net buyers of gold led by the BRIC countries, an event of tremendous significance among many others of a general change in the markets and the beginnings of a largely unreported 'currency war.'

And it is my experience that when a writer or analyst starts reaching for ad hominem remarks of a non-satirical nature that they are just plain out of facts and faltering in a desire to win an argument that is running against them.

This reminds me of what the dean of financial letters recently said about a similar performance on Bloomberg:

"I listened to Kitco's Nadler on the Bloomberg channel this morning. He's been bearish on gold for months, and I thought he sounded like a know-nothing fool today. Why didn't Bloomberg interview someone who's been bullish and right about gold?" Richard Russell

The big changes are almost never caught by those close to the action, or with a vested interest in some aspect of the status quo that blinds them to change. It is the nature of the big changes, what makes them 'big.' This reminds me so much of early November 2009 when economist Willem Buiter launched into a couple of irrational rants about gold bullion in the Financial Times, a few weeks before shed his Maverecon status to join the ranks of Citigroup.

When 'news outlets' or 'analyst/economists' with ties to Wall Street start coming out with such outlandish statements, gold may likely be going another leg higher in the following months.

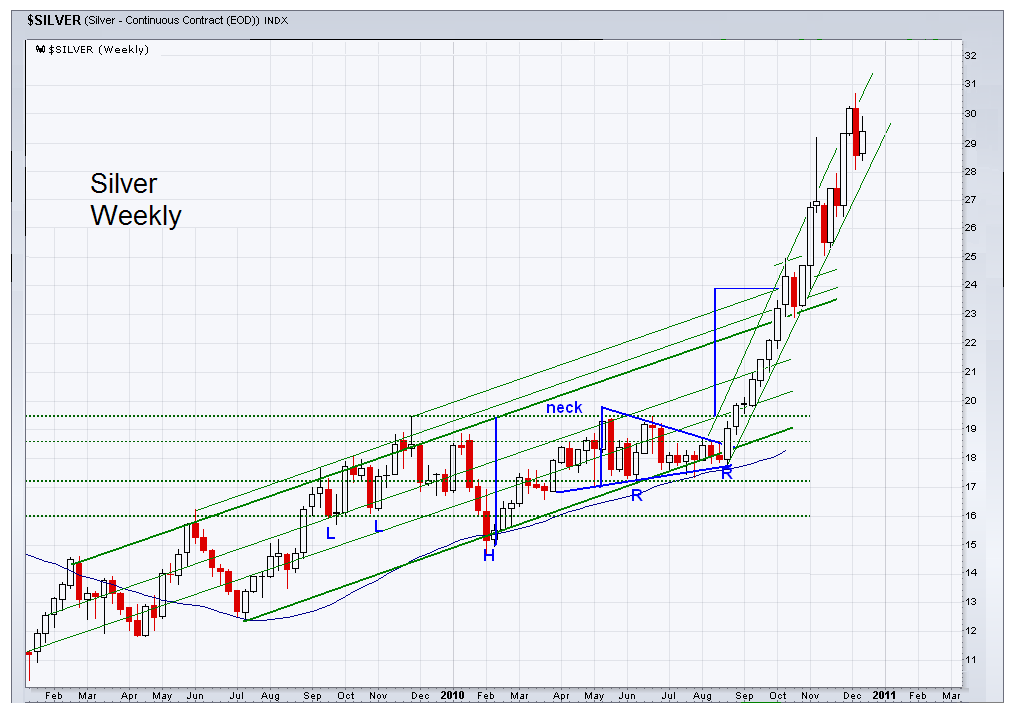

And a bit of a mystery is why there is almost never any mention of silver, which is making gold look like a bit of a slacker by comparison as an emerging store of value for wealth that fears the arbitrariness of the Wall Street dominated global financial system.

With regards to the global financial crisis, imposing austerity is not the answer. That is like starving the slaves to improve their condition by making the plantation more profitable. Looting the 'great house' and the barns to feed the slaves, at least temporarily, is not the answer either. The problem is obviously in the system itself.

But either expedient solution suits the external moneyed interests promoting the system who seek only to plunder and drain the assets and labor of others who are all their common prey, whether they feel their kinship or not. An unjust and unsustainable system tarnishes all participants and leaves them vulnerable to exploitation and decay.

It is the root causes of the debt and the imbalances in the system that must be addressed to make any reform sustainable. And this obviously includes addressing abuses such as the promotion of a global trade regime that is inherently unjust and imbalanced to the favor of the oligarchs of whatever political wrappings around the world who hold the greater profit to themselves and leave their people relatively impoverished and exploited. And it also includes the waging of unfunded wars to protect and promote privileged commercial interests, and a political funding system that is little more than soft graft and an open invitation to corruption by special interests.

It begins with a debilitating system of taxation by the moneyed interests on every commercial transaction in the form of fees and commissions, and the abuse of a money system that is little more than a fraud perpetrated by private interests for the benefit of a few at the expense of the many. If you wish a simple measure of this, then look to the median wage.

Greed is not good. Greed is a disease, an aberration of simple honest ambition and necessary provision taken to excess. It is a sin, a transgression against love. This simple distinction may be lost on a people no longer able to distinguish between virtue and sin, honor and expediency, appetite and gluttony, the means and the ends. Every great religion, every school of philosophy has cautioned throughout history on the perils of unbridled and unregulated greed.

And yet this generation would make a god of it, although they may not understand, or care, what it is that they are doing, and whom it is they serve. And yet they will be held to account for their willfulness, foolishness, and casual disregard for others.

Greed, often in company with hubris and fear, is a handmaiden of the corrupting influence of power and triumph of the will. Greed is contagious, and attacks the very contentment of society at its heart, turning it towards oligarchy and oppression.

"Greed is a bottomless pit which exhausts the person in an endless effort to satisfy the need without ever reaching satisfaction." Erich Fromm

Any system that promotes greed, gluttony, and insatiability as its highest goods and fundamental ideals is a cult of perversion and addiction on a scale with ancient Rome, an imbalanced insult to the natural law, with a fatal attraction to overreach, failure and self-destruction. What the US has today is not market capitalism that rewards the merits and work of individuals, but rather is the product of dishonest and disordered minds, a system of fraud and plunder by privileged oligarchs masquerading as fair and honest markets of legitimate valuation and price discovery.

"Because the free market system is so weak politically, the forms of capitalism that are experienced in many countries are very far from the ideal. They are a corrupted version, in which powerful interests prevent competition from playing its natural, healthy role." Raghuram G. Rajan

The Banks must be restrained, and the financial system reformed, with balance restored to the economy, before there can be any sustained recovery.

Financial Interests Dictate Sovereign Policy By Michael Hudson

December 18, 2010

"...The economic problem is not caused by sovereign debt but by bad bank loans, deceptive financial practice and neoliberal bank deregulation. Iceland’s Viking raiders, Ireland’s Anglo-Irish bank and other foreign banks are trying to avoid taking losses on financial claims that are largely fictitious, inasmuch as they exceed the ability of indebted economies to pay. The ‘crisis’ can be solved by making the banks write down their debt claims to realistic ‘junk’ valuations. There is no need to wreck economies by subjecting them to financial asset-stripping.

In such cases there’s a basic principle at work: Debts that can’t be paid, won’t be. The question is, just how won’t they be paid? As matters stand, countries are being told to subject themselves to massive foreclosure – not only a forfeiture of homes, but of national policy.

In this respect the sovereign crisis is a crisis of sovereignty itself: Who shall be in charge of the economy, its tax philosophy and public spending: elected officials acting in the public interest, or an intrusive financial oligarchy? The EU was wrong to tell governments to pay for following its advice – and pressure – to trust financial crooks and deregulate bank oversight. The European Central Bank should reimburse victimized governments for the bailouts that have been paid. This reimbursement can be done by levying a progressive tax policy and creating a central bank to help finance governments.

The proper aim of a national economy is to promote capital formation and rising living standards for the population as a whole. not a narrowing financial class at the top of the pyramid. So I see two major policies to lead the way out of this mess:

First, shift taxes back onto land and resource rent, and onto financial and capital gains. This will prevent another real estate bubble from being inflated by debt leveraging. By holding down housing prices, it will save labor from having to pay an equivalent amount in income tax. Low real estate taxes (under 1% until just recently) have not saved homeowners money in Latvia. Low property taxes merely have left more rental income to be pledged to banks, to capitalize into large mortgage loans.

Second, de-privatize basic utilities and natural monopolies to save Europe from rentiers turning it into a tollbooth economy. Europe needs a central bank that can do what central banks are supposed to do: create money to finance government deficits. But the European Central Bank and article 123 of the European Constitution as amended by the Lisbon Treaty prevents the central bank from lending to governments. This forces governments to levy taxes to pay interest to banks – for creating electronic credit that a real central bank could just as well create on its own computer keyboards.

Government banking is not necessarily inflationary. It finances what is necessary for economies to grow: investment in infrastructure and capital formation to raise productivity and minimize the cost of doing business.

What turns out to be inflationary is commercial bank lending. It inflates asset prices – unproductively. Banks lend mainly against real estate and other assets already in place, and stocks and bonds already issued. This is unproductive credit, not real wealth creation. The only way to keep this unproductive debt overhead solvent is to inflate asset prices more – by untaxing assets to leave more revenue to pay bankers on exponentially growing debts.

It doesn’t have to be this way. The recent 30 years of financial polarization is reversible. The alternative is to succumb to neoliberal austerity."

I think that most people know what needs to be done in their conscience, but their hearts have become so hardened over the past twenty years that the message will be ignored until after they undergo a period of suffering on the scale of the worst of the twentieth century. May God have mercy on us all.

Unless the Lord builds the house, the builders labor in vain.

Unless the Lord watches over the city, the guards stand watch in vain.

In vain you rise early and stay up late,

toiling for food to eat—

for he grants sleep only to those he loves.

The mechanics of what is happening with money now is fascinating, and seems to be clarifying in my mind. It is hard to imagine a more inherently ineffective system of capital and resource allocation than crony capitalism. It is a game which is rigged to deliver the money in the system to a minority of insiders, thereby bankrupting all the customers.

It is said that in a purely competitive capitalist system, all businesses are vectored to zero profit in a process of creative destruction. As a certain class of participants clearly recognizes this they take every opportunity to corrupt and game the system through fraud. This is why markets must have regulators. At times the fraud overcomes the regulation to such a degree that the normal market balances are rendered ineffective and the system passes to a crony capitalist system, if not an outright oligarchy.

In a crony capitalist system a similar outcome can be achieved, but with the insiders and powerful interests holding most of the money which ultimately becomes worthless because the foundation of the money, the labor of the people, is destroyed.

In other words, greed compels the materially obsessed to obtain the greatest piles of chips, but in the long term renders their chips to be worthless because they are unable to stop their fraud and plundering even when it is in their best interests. They are not governed by rationality or conscience or even common sense. For periods of time oligarchies are able to survive in an uneasy equilibrium enforced by power, but ultimately these wicked wither and die on their great piles of gains.

I now give more weight to the potential for hyperinflation, and will be exploring this topic during 2011. The Congress and the Fed are reckless to the point of self-destruction.

The pattern in the gold market has greatly clarified. It is now following a more gradual path higher as the banks of the world resist its upward trajectory, and the many still do not recognize the inherent value of bullion in the face of currency devaluation.

The gradual rise will take gold much higher over time than a parabolic spike higher would, although it demands more patience as things unfold.

At some point it will regain a more aggressive track higher, and then likely consolidate and resume a more gradual rise for a time.

Silver is on an aggressive but sustainable rally path. The many years of suppression and the leverage in this market may call out a path and price much higher on a percentage basis than gold.

I like to buy both, but given a choice I would tend now to overweight silver for trading, and gold for the long term investment and wealth protection.

The 50 Day Moving Average once again provided support for a dip in bullion. I tended to view the bear raid today as tied to option expiration in equities moreso than in the bullion itself. Mining stocks have been hot, and the call buying may have gotten ahead of itself, setting up an incentive for players to hit the metals and take down the industry associated stocks.

Although the CFTC has enabled a position disclosure trigger at 10% at which the regulators can ask a market participant to show their net swaps, the actual position limits discussion was tabled today for a future meeting.

Tomorrow is December options expiration for equities and the funds are also painting the tape to make their bonuses round up nicely into the year end.

Let's see how the markets go as they hit all our targets in the currently active chart formations. Wait for it, because Benny is in there pumping and it may take a stumble to turn this trend around, which for now is up.

"Currency values and precious metals prices can be volatile, but the long-term weakness in the U.S. dollar and relative purchasing-power-preservation attributes of gold and silver, and the stronger currencies outside the dollar, remain in place. As with systemic risks in the United States, risks in other areas of the world — such as among the countries using the euro — likely will be addressed by the spending or creation of whatever money is needed (indications of any needed U.S. backing are in place) in order to prevent systemic failure.

Keep in mind that the U.S. remains the proverbial elephant in the bathtub in terms of pending effective sovereign bankruptcies. The various European crises remain an intermittent foil for the U.S. dollar, pulling market attention away from the unfolding solvency crisis in the United States and a likely move to massive selling against the U.S. currency.

Accordingly, high risk of the early stages of a hyperinflation beginning to unfold by mid-2011 continues. Rising inflation should become increasingly broad, reflecting an increasingly serious problem in the first-half of 2011.”

This seems mildly reminiscent of the setup which Soros and unnamed Swiss parties engaged in when they took down the Bank of England's defense of the British Pound and its official peg to the Euro.

Will the US ultimately feel compelled to defend some of the gold and silver shorts, both in terms of bullion and derivatives, held by its Wall Street Banks? You could allow for the possibility, if you will, that there is a corresponding web of derivatives that has a links, and a possible chokehold, on a few key European institutions, particularly in England and Germany, involving counterparty derivatives and CDS, and collateral damage to professional and political careers. Ugly stuff, rather messy really. But there are historic precedents.

There should be no confusion that this involves not only a few large Wall Street players, but also elements, past and present, in the US Treasury and the Federal Reserve. It makes the unfolding insider trading scandal look like a neighborhood numbers racket.

Therefore we should not discount the possibility that if a default should occur there will be an emotional and political reaction put forward as a means of deflecting the disclosure of the true nature of the financial corruption.

It would be most interesting and possibly entertaining to see if Ron Paul's congressional committee could be able to mount an effective investigation into the matter, or if events will take place to pre-empt and redirect such an inquiry to manage the potential collateral damage to careers and possibly governments, both at home and abroad.

It's never really the act itself, often minor infractions undertaken for practical purposes or what could be rationalized as such by some. Rather it is always the corruption of the policy actions to personal gain, and the subsequent cover-up, that tends to gather substance over time into a first class scandal, acts of felony and high crimes, and all the revelations that follow.

“Oh what a tangled web we weave, When first we practice to deceive." Sir Walter Scott

Non-event FOMC statement, the last of 2010, which is what had been expected. The macro retail sales picture was painted in high gloss, but the big miss by Best Buy cuts deeper to the heart of the truth.

The US is becoming two nations, one of privileged fraud and illusion, and another of harsh reality, difficult circumstances, and unnecessary hardship.

The first paragraph is the only thing that has changed and that from slow to insufficient. The Fed is dour on the jobless recovery and its self-sustainability.

"Information received since the Federal Open Market Committee met in September confirms that the pace of recovery in output and employment continues to be slow. Household spending is increasing gradually, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. Housing starts continue to be depressed. Longer-term inflation expectations have remained stable, but measures of underlying inflation have trended lower in recent quarters."

Contrast this opening paragraph from the Fed's November 3 Statement with their latest below.

Release Date: December 14, 2010 Federal Reserve Open Market Committee Statement

Information received since the Federal Open Market Committee met in November confirms that the economic recovery is continuing, though at a rate that has been insufficient to bring down unemployment. Household spending is increasing at a moderate pace, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. The housing sector continues to be depressed. Longer-term inflation expectations have remained stable, but measures of underlying inflation have continued to trend downward.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Currently, the unemployment rate is elevated, and measures of underlying inflation are somewhat low, relative to levels that the Committee judges to be consistent, over the longer run, with its dual mandate. Although the Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, progress toward its objectives has been disappointingly slow.

To promote a stronger pace of economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate, the Committee decided today to continue expanding its holdings of securities as announced in November. The Committee will maintain its existing policy of reinvesting principal payments from its securities holdings. In addition, the Committee intends to purchase $600 billion of longer-term Treasury securities by the end of the second quarter of 2011, a pace of about $75 billion per month. The Committee will regularly review the pace of its securities purchases and the overall size of the asset-purchase program in light of incoming information and will adjust the program as needed to best foster maximum employment and price stability.

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels for the federal funds rate for an extended period.

The Committee will continue to monitor the economic outlook and financial developments and will employ its policy tools as necessary to support the economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Sandra Pianalto; Sarah Bloom Raskin; Eric S. Rosengren; Daniel K. Tarullo; Kevin M. Warsh; and Janet L. Yellen.

Voting against the policy was Thomas M. Hoenig. In light of the improving economy, Mr. Hoenig was concerned that a continued high level of monetary accommodation would increase the risks of future economic and financial imbalances and, over time, would cause an increase in long-term inflation expectations that could destabilize the economy.

Well, it could be worse. He could be short silver, too.

S - A - V - E - - - M - E - - - B - E - N - N - N - n - n - n - n - n ...

"I listened to Kitco's Nadler on the Bloomberg channel this morning. He's been bearish on gold for months, and I thought he sounded like a know-nothing fool today. Why didn't Bloomberg interview someone who's been bullish and right about gold?"

The US dollar did a quietly impressive 'cliff dive' today.

Harvey Organ's metals commentary is interesting this evening. It appears that some rather large customers are pulling their silver bullion out of storage in the Comex vaults. Trying to beat the Christmas rush?

From an interview with Timothy Verdon, Art Historian and Canon of the Cathedral of Florence.

"God is infinitely beyond human comprehension – God is God, we are creatures. And yet in everything that the Judeo-Christian tradition tells us about God, it is clear that God wants to communicate with his creatures, God wants to be known by his creatures.

The whole point of the law and the prophecy in ancient Israel was that God wanted his creatures to understand him and themselves – a creature is a reflection, to some degree, of the Creator. This will of God to make himself understood – and in that process help us understand ourselves – reaches fulfilment in Christ. Christ is the Word of God where the Scriptures are many words that come from God and are filtered through the inspired authors; Christ is the very Word that all those other words try to give partial expression to.

Christ assumes a form that makes him intelligible to human beings – the Word becomes flesh. And then the Gospel of John immediately adds that he dwelt among us, and we saw his glory. What Christ did while he was on earth was to reveal the identity, the personality of the Father: all of the wonderful things that he did that reveal the father – the words he spoke, the miracles, the acts of mercy – even after Christ’s Resurrection and Ascension, they continue...

What’s the relationship of all of this with art which is my specific field? The relationship is simple. When Christ took a Body – when the Word of God took a body from the humanity of Mary – it was to be seen. Christ is now invisible except in the abstract forms of the sacraments – we see water and we know that we’re being cleansed, we see bread and wine and we know that his Body and Blood are present, but we don’t really see the body and blood. But somehow the extreme simplicity of that communication that God wanted in Christ’s Incarnation is now filtered by a symbolic system of sacraments and signs. So we don’t actually see, but the art of the Church allows us to see. It extends down through the centuries, something like that privileged experience of the people of Jesus’ own time when they saw him and intuited that there was more than just a man here. Art allows us to continue to enjoy that experience...

So the ancient desire of human beings to see God, Moses on the mountain asks God to show him his face…. In Christ people really contemplated the Face of God. Christ tells us that we see him in the poor and the needy, and so on. But the works of visual art that surround these privileged moments in which [people] come into direct contact with Christ, and which usually tell stories from the life of Christ, or of Mary or of the saints, in whom we also contemplate Christ – the works of art are part of this process.

Much of what I’ve done as an art historian is to try to remind other art historians of this whole dimension that I’m describing, which usually has not been discussed. And that’s a grave omission, because the artists and the patrons were more or less conscious of all of this. They lived within this system. So the art historians should be aware of it, because if not they are going to talk about these works in a way which is misleading. Certainly the style, the economical features – all of these things are interesting and real and an important part of the history of art, but the larger framework within which these works were meant to function was something more like what I’ve been describing.

I try to call the attention of colleagues to these things, and even more, perhaps, I try to reawaken Christians to the extraordinary eloquence and beauty of this visual heritage which today ordinary believing Christians have the equipment to understand. They may not be art historians but they have keys to understanding the works of architecture and painting and sculpture that many art historians don’t have. And those keys come from their own faith, from the simple experience of life in church, the life of the sacraments.

One could add that something that Christians tend not to reflect upon and that historians of art and of sacred music and sacred architecture similarly tend not to reflect upon, is that the great work of art that Christianity has produced since its beginning is the Liturgy.

What believing Christians have been harried by the Spirit to do right from the beginning is to seek those poetic forms of expression and those physical actions and those material objects that can be called into play to express their faith. Really Jesus himself taught us to do this. At the Last Supper, he took bread, and then he said words: “This is my Body”. Jesus, who is himself the Word made flesh, in order to communicate, takes physical things that already have their own range of meanings and says words that open that implicit range of meanings to a much more specific and explicit communication.

So Jesus himself is the first teacher of how you combine things and actions and words in order to create a composite work, which is basically a work of art. At the Last Supper, he puts on an apron, he kneels down, he washes their feet. He’s continually doing things that invite reflection and then making sure that we understand what he’s doing.

What I’m saying is that you can’t really just talk about the visual art of the Church, or the music of the Church, or the Liturgy. All of this is part of a single creative impulse that flows from the experience of Christ himself, the Word who becomes flesh. A conceptual expression of God who becomes visible and tangible. The First Letter of St John says that this is what we have seen and touched and contemplated with our own eyes; it’s a total sensory and intellectual experience. The Liturgy is that. So an artist working for the church and for its Liturgy is within this millennial creative action which, in the last analysis, is a continuation in time and space of the Creation described in Genesis."

An epic struggle between power and the people, that surprisingly so few among the people really understand even today.

“The money power preys upon the nation in times of peace, and conspires against it in times of adversity. It is more despotic than monarchy, more insolent than autocracy, more selfish than bureaucracy. It denounces, as public enemies, all who question its methods, or throw light upon its crimes. It can only be overthrown by the awakened conscience of the nation."

Let us pray for those whose hearts are hardened against His grace and loving kindness by greed, fear, and pride, and the seductive illusion and crushing isolation of evil.

We pray that we all may experience the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness. And in so doing, may we obtain abundant life, and with it the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.