Wax on, wax off.

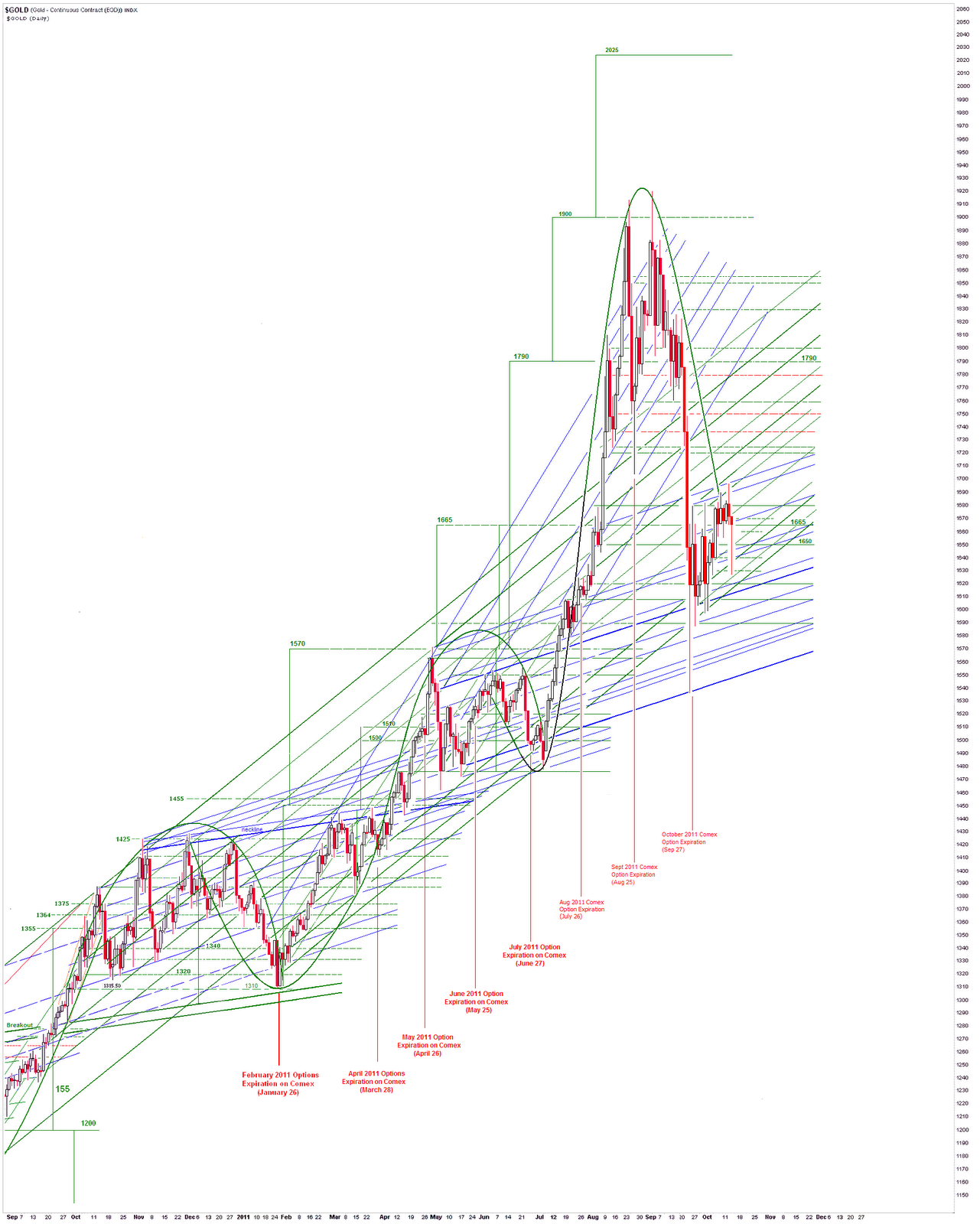

As a reminder, this is a stock options expiration week.

"You have accepted things you would not have accepted five years ago, a year ago, things that your father, even in Germany, could not have imagined. Suddenly it all comes to be, all at once. You see what you are, what you have done, or more accurately what you haven’t done. For that was all that was required of most of us: that we do nothing. You remember everything now, and your heart breaks. Too late. You are compromised beyond repair."

Milton Mayer, They Thought They Were Free

"Since I entered politics, I have chiefly had men's views confided to me privately. Some of the biggest men in the United States, in the field of commerce and manufacture, are afraid of somebody, are afraid of something. They know that there is a power somewhere so organized, so subtle, so watchful, so interlocked, so complete, so pervasive, that they had better not speak above their breath when they speak in condemnation of it.

They know that America is not a place of which it can be said, as it used to be, that a man may choose his own calling and pursue it just as far as his abilities enable him to pursue it; because to-day, if he enters certain fields, there are organizations which will use means against him that will prevent his building up a business which they do not want to have built up; organizations that will see to it that the ground is cut from under him and the markets shut against him. For if he begins to sell to certain retail dealers, to any retail dealers, the monopoly will refuse to sell to those dealers, and those dealers, afraid, will not buy the new man's wares.

And this is the country which has lifted to the admiration of the world its ideals of absolutely free opportunity, where no man is supposed to be under any limitation except the limitations of his character and of his mind; where there is supposed to be no distinction of class, no distinction of blood, no distinction of social status, but where men win or lose on their merits...

A great industrial nation is controlled by its system of credit. Our system of credit is privately concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men who, even if their action be honest and intended for the public interest, are necessarily concentrated upon the great undertakings in which their own money is involved and who necessarily, by very reason of their own limitations, chill and check and destroy genuine economic freedom...

Shall we try to get the grip of monopoly away from our lives, or shall we not? Shall we withhold our hand and say monopoly is inevitable, that all that we can do is to regulate it? Shall we say that all that we can do is to put government in competition with monopoly and try its strength against it? Shall we admit that the creature of our own hands is stronger

than we are?

We have been dreading all along the time when the combined power of high finance would be greater than the power of the government. Have we come to a time when the President of the United States or any man who wishes to be the President must doff his cap in the presence of this high finance, and say, "You are our inevitable master, but we will see how we can make the best of it?"

We are at the parting of the ways. We have, not one or two or three, but many, established and formidable monopolies in the United States. We have, not one or two, but many, fields of endeavor into which it is difficult, if not impossible, for the independent man to enter. We have restricted credit, we have restricted opportunity, we have controlled development, and we have come to be one of the worst ruled, one of the most completely controlled and dominated, governments in the civilized world--no longer a government by free opinion, no longer a government by conviction and the vote of the majority, but a government by the opinion and the duress of small groups of dominant men.

If the government is to tell big business men how to run their business, then don't you see that big business men have to get closer to the government even than they are now? Don't you see that they must capture the government, in order not to be restrained too much by it? Must capture the government? They have already captured it.

Are you going to invite those inside to stay inside? They don't have to get there. They are there. Are you going to own your own premises, or are you not? That is your choice. Are you going to say: "You didn't get into the house the right way, but you are in there, God bless you; we will stand out here in the cold and you can hand us out something once in a while?"

At the least, under the plan I am opposing, there will be an avowed partnership between the government and the trusts. I take it that the firm will be ostensibly controlled by the senior member. For I take it that the government of the United States is at least the senior member, though the younger member has all along been running the business. But when all the momentum, when all the energy, when a great deal of the genius, as so often happens in partnerships the world over, is with the junior partner, I don't think that the superintendence of the senior partner is going to amount to very much.

And I don't believe that benevolence can be read into the hearts of the trusts by the superintendence and suggestions of the federal government; because the government has never within my recollection had its suggestions accepted by the trusts. On the contrary, the suggestions of the trusts have been accepted by the government.

There is no hope to be seen for the people of the United States until the partnership is dissolved. And the business of the party now entrusted with power is going to be to dissolve it.

Those who supported the third party supported, I believe, a program perfectly agreeable to the monopolies. How those who have been fighting monopoly through all their career can reconcile the continuation of the battle under the banner of the very men they have been fighting, I cannot imagine. I challenge the program in its fundamentals as not a progressive program at all. Why did Mr. Gary suggest this very method when he was at the head of the Steel Trust? Why is this very method commended here, there, and everywhere by the men who are interested in the maintenance of the present economic system of the United States? Why do the men who do not wish to be disturbed urge the adoption of this program? The rest of the program is very handsome; there is beating in it a great pulse of sympathy for the human race. But I do not want the sympathy of the trusts for the human race. I do not want their condescending assistance.

And I warn every progressive Republican that by lending his assistance to this program he is playing false to the very cause in which he had enlisted. That cause was a battle against monopoly, against control, against the concentration of power in our economic development, against all those things that interfere with absolutely free enterprise. I believe that some day these gentlemen will wake up and realize that they have misplaced their trust, not in an individual, it may be, but in a program which is fatal to the things we hold dearest.

If there is any meaning in the things I have been urging, it is this: that the incubus that lies upon this country is the present monopolistic organization of our industrial life. That is the thing which certain Republicans became "insurgents" in order to throw off. And yet some of them allowed themselves to be so misled as to go into the camp of the third party in order to remove what the third party proposed to legalize. My point is that this is a method conceived from the point of view of the very men who are to be controlled, and that this is just the wrong point of view from which to conceive it...

One of the wonderful things about America, to my mind, is this: that for more than a generation it has allowed itself to be governed by persons who were not invited to govern it. A singular thing about the people of the United States is their almost infinite patience, their willingness to stand quietly by and see things done which they have voted against and do not want done, and yet never lay the hand of disorder upon any arrangement of government.

There is hardly a part of the United States where men are not aware that secret private purposes and interests have been running the government. They have been running it through the agency of those interesting persons whom we call political "bosses." A boss is not so much a politician as the business agent in politics of the special interests. The boss is not a partisan; he is quite above politics! He has an understanding with the boss of the other party, so that, whether it is heads or tails, we lose. The two receive contributions from the same sources, and they spend those contributions for the same purposes...

The critical moment in the choosing of officials is that of their nomination more often than that of their election. When two party organizations, nominally opposing each other but actually working in perfect understanding and co-operation, see to it that both tickets have the same kind of men on them, it is Tweedledum or Tweedledee, so far as the people are concerned; the political managers have us coming and going. We may delude ourselves with the pleasing belief that we are electing our own officials, but of course the fact is we are merely making an indifferent and ineffectual choice between two sets of men named by interests which are not ours."

Woodrow Wilson, The New Freedom, 1913

"In 1912, 'an unprecedented number' of African Americans left the Republican Party to cast their vote for Democrat Wilson. They were encouraged by his promises of support for their issues.Wilson did not interfere with the well-established system of Jim Crow and backed the demands of Southern Democrats that their states be left alone to deal with issues of race and black voting without interference from Washington.

While president of Princeton University, Wilson discouraged blacks from even applying for admission, preferring to keep the peace among white students than have black students admitted.

Black leaders who supported Wilson in 1912 were angered when segregationist white Southerners took control of Congress and many executive departments. Wilson ignored complaints that his cabinet officials had established official segregation in most federal government offices, in some departments for the first time since 1863. New facilities were designed to keep the races working there separated. Eric Foner says, "His administration imposed full racial segregation in Washington and hounded from office considerable numbers of black federal employees."

"With Progressive ("Bull Moose") Party candidate Theodore Roosevelt and Republican nominee William Howard Taft dividing the Republican Party vote, Wilson was elected President as a Democrat in 1912.

In his first term as President, Wilson persuaded a Democratic Congress to pass major progressive reforms including the Federal Reserve Act, Federal Trade Commission Act, the Clayton Antitrust Act, the Federal Farm Loan Act and an income tax. Wilson brought many white Southerners into his administration, and supported the introduction of segregation into many federal agencies."

"Brandeis's positions on regulating large corporations and monopolies carried over into the presidential campaign of 1912. Democratic candidate Woodrow Wilson made it "the central issue," and, according to Wilson historian Arthur Link, "part of a larger debate over the future of the economic system and the role of the national government in American life." Whereas the Progressive Party candidate, Theodore Roosevelt felt that trusts were inevitable and should be regulated, Wilson and his party aimed to "destroy the trusts" by ending special privileges, such as protective tariffs and unfair business practices that made them possible.

On that basis, Brandeis, though "nominally a Republican," supported Wilson and urged his friends and associates to join him. The two men met for the first time at a private conference in New Jersey that August and spent three hours discussing economic issues. Mason notes that Brandeis came away from the meeting a "confirmed admirer of Wilson, whom he described in letters to his friends as possessed of a remarkable mind and likely to make 'an ideal president.'" Wilson thereafter began using the term "regulated competition," the concept that Brandeis had developed, and made it the essence of his program. In September, Wilson asked Brandeis to "set forth explicitly the actual measures by which competition can be effectively regulated."

After his victory in the November election, Wilson wrote to Brandeis, "You were yourself a great part of the victory." Wilson considered nominating Brandeis first for Attorney General and later for Secretary of Commerce, but backed down after a loud outcry from corporate executives that he had once opposed in court battles. He concluded that Brandeis was too controversial a figure to appoint to his cabinet.

Nevertheless, during Wilson's first year as president, Brandeis "played a key role in shaping the Federal Reserve Act," according to banking historian Albert Link. He adds that "Brandeis's arguments were decisive in breaking the deadlock on the banking issue." Wilson endorsed the banking proposals of Brandeis and Secretary of State William Jennings Bryan, who, Piott points out, felt that "the banking system needed to be democratized and its currency issued and controlled by the government," and convinced Congress to enact the Federal Reserve Act in December 1913."

Wilson secured passage of the Federal Reserve Act in late 1913. Wilson had tried to find a middle ground between conservative Republicans led by Senator Nelson W. Aldrich and the powerful left wing of the Democratic party led by William Jennings Bryan, who opposed all banking schemes and strenuously denounced private banks and Wall Street. The latter group wanted a government-owned central bank that could print paper money as Congress required. The compromise, based on the Aldrich Plan but sponsored by Democratic Congressmen Carter Glass and Robert Owen, allowed the private banks to control the 12 regional Federal Reserve banks, but appeased the agrarians by placing controlling interest in the System in a central board appointed by the president with Senate approval. Moreover, Wilson convinced Bryan's supporters that because Federal Reserve notes were obligations of the government, the plan met their demands for an elastic currency.

Having 12 regional banks was meant to weaken the influence of the powerful New York banks, a key demand of Bryan's allies in the South and West. This decentralization was a key factor in winning the support of Congressman Glass.[69] The final plan passed in December 1913. Some bankers felt it gave too much control to Washington, and some reformers felt it allowed bankers to maintain too much power. Several Congressmen claimed that New York bankers feigned their disapproval.

Wilson named Paul Warburg and other prominent bankers to direct the new system. While power was supposed to be decentralized, the New York branch dominated the Fed as the "first among equals".

The Guardian UK

France and Germany Agree to €2 Trillion Euro Rescue Fund

By David Gow in Brussels

France and Germany have reached agreement to boost the eurozone's rescue fund to €2tn (£1.75tn) as part of a "comprehensive plan" to resolve the sovereign debt crisis, which this weekend's summit should endorse, EU diplomats said."

The Guardian UK

France and Germany Agree to €2 Trillion Euro Rescue Fund

By David Gow in Brussels

France and Germany have reached agreement to boost the eurozone's rescue fund to €2tn (£1.75tn) as part of a "comprehensive plan" to resolve the sovereign debt crisis, which this weekend's summit should endorse, EU diplomats said."

Hard time's is here

And everywhere you go

Times are harder

Than there ever been before.

You know that people

They are drifting from door to door

But they can't find no heaven

I don't care where they go

People, if I ever can get up

Off a this old hard killin' floor

Lord, I'll never get down

This low no more.

Um, hm-hm-hm

Hm, um-hm

Hm, hm-hm

Hm, hm-hm-hm

Well, you hear me singing

This old lonesome song

People, you know these hard times

Can't last us so long

You know, you'll say you had money

You better be sure

But these hard times gonna kill you

Just drive a lonely soul

Skip James, Hard Time Killin' Floor Blues

"...On the occasion corresponding to this four years ago all thoughts were anxiously directed to an impending civil war. All dreaded it, all sought to avert it. While the inaugural address was being delivered from this place, devoted altogether to saving the Union without war, insurgent agents were in the city seeking to destroy it without war — seeking to dissolve the Union and divide effects by negotiation. Both parties deprecated war, but one of them would make war rather than let the nation survive, and the other would accept war rather than let it perish, and the war came.

One-eighth of the whole population were colored slaves, not distributed generally over the Union, but localized in the southern part of it. These slaves constituted a peculiar and powerful interest. All knew that this interest was somehow the cause of the war. To strengthen, perpetuate, and extend this interest was the object for which the insurgents would rend the Union even by war, while the Government claimed no right to do more than to restrict the territorial enlargement of it.

Neither party expected for the war the magnitude or the duration which it has already attained. Neither anticipated that the cause of the conflict might cease with or even before the conflict itself should cease. Each looked for an easier triumph, and a result less fundamental and astounding. Both read the same Bible and pray to the same God, and each invokes His aid against the other. It may seem strange that any men should dare to ask a just God's assistance in wringing their bread from the sweat of other men's faces, but let us judge not, that we be not judged.

The prayers of both could not be answered. That of neither has been answered fully. The Almighty has His own purposes. 'Woe unto the world because of offenses; for it must needs be that offenses come, but woe to that man by whom the offense cometh.' If we shall suppose that American slavery is one of those offenses which, in the providence of God, must needs come, but which, having continued through His appointed time, He now wills to remove, and that He gives to both North and South this terrible war as the woe due to those by whom the offense came, shall we discern therein any departure from those divine attributes which the believers in a living God always ascribe to Him?

Fondly do we hope, fervently do we pray, that this mighty scourge of war may speedily pass away. Yet, if God wills that it continue until all the wealth piled by the bondsman's two hundred and fifty years of unrequited toil shall be sunk, and until every drop of blood drawn with the lash shall be paid by another drawn with the sword, as was said three thousand years ago, so still it must be said 'the judgments of the Lord are true and righteous altogether'.

With malice toward none; with charity for all; with firmness in the right, as God gives us to see the right, let us strive on to finish the work we are in; to bind up the nation's wounds; to care for him who shall have borne the battle, and for his widow, and his orphan – to do all which may achieve and cherish a just and lasting peace, among ourselves, and with all nations."

Abraham Lincoln, Second Inaugural Address

"WHEN four years ago we met to inaugurate a President, the Republic, single-minded in anxiety, stood in spirit here. We dedicated ourselves to the fulfillment of a vision—to speed the time when there would be for all the people that security and peace essential to the pursuit of happiness. We of the Republic pledged ourselves to drive from the temple of our ancient faith those who had profaned it; to end by action, tireless and unafraid, the stagnation and despair of that day. We did those first things first.

Our covenant with ourselves did not stop there. Instinctively we recognized a deeper need—the need to find through government the instrument of our united purpose to solve for the individual the ever-rising problems of a complex civilization. Repeated attempts at their solution without the aid of government had left us baffled and bewildered. For, without that aid, we had been unable to create those moral controls over the services of science which are necessary to make science a useful servant instead of a ruthless master of mankind. To do this we knew that we must find practical controls over blind economic forces and blindly selfish men.

We of the Republic sensed the truth that democratic government has innate capacity to protect its people against disasters once considered inevitable, to solve problems once considered unsolvable. We would not admit that we could not find a way to master economic epidemics just as, after centuries of fatalistic suffering, we had found a way to master epidemics of disease. We refused to leave the problems of our common welfare to be solved by the winds of chance and the hurricanes of disaster.

In this we Americans were discovering no wholly new truth; we were writing a new chapter in our book of self-government.

This year marks the one hundred and fiftieth anniversary of the Constitutional Convention which made us a nation. At that Convention our forefathers found the way out of the chaos which followed the Revolutionary War; they created a strong government with powers of united action sufficient then and now to solve problems utterly beyond individual or local solution. A century and a half ago they established the Federal Government in order to promote the general welfare and secure the blessings of liberty to the American people.

Today we invoke those same powers of government to achieve the same objectives.

Four years of new experience have not belied our historic instinct. They hold out the clear hope that government within communities, government within the separate States, and government of the United States can do the things the times require, without yielding its democracy. Our tasks in the last four years did not force democracy to take a holiday.

Nearly all of us recognize that as intricacies of human relationships increase, so power to govern them also must increase—power to stop evil; power to do good. The essential democracy of our Nation and the safety of our people depend not upon the absence of power, but upon lodging it with those whom the people can change or continue at stated intervals through an honest and free system of elections. The Constitution of 1787 did not make our democracy impotent.

In fact, in these last four years, we have made the exercise of all power more democratic; for we have begun to bring private autocratic powers into their proper subordination to the public's government. The legend that they were invincible—above and beyond the processes of a democracy—has been shattered. They have been challenged and beaten.

Our progress out of the depression is obvious. But that is not all that you and I mean by the new order of things. Our pledge was not merely to do a patchwork job with secondhand materials. By using the new materials of social justice we have undertaken to erect on the old foundations a more enduring structure for the better use of future generations.

In that purpose we have been helped by achievements of mind and spirit. Old truths have been relearned; untruths have been unlearned. We have always known that heedless self-interest was bad morals; we know now that it is bad economics. Out of the collapse of a prosperity whose builders boasted their practicality has come the conviction that in the long run economic morality pays. We are beginning to wipe out the line that divides the practical from the ideal; and in so doing we are fashioning an instrument of unimagined power for the establishment of a morally better world.

This new understanding undermines the old admiration of worldly success as such. We are beginning to abandon our tolerance of the abuse of power by those who betray for profit the elementary decencies of life.

In this process evil things formerly accepted will not be so easily condoned. Hard-headedness will not so easily excuse hardheartedness. We are moving toward an era of good feeling. But we realize that there can be no era of good feeling save among men of good will.

For these reasons I am justified in believing that the greatest change we have witnessed has been the change in the moral climate of America.

Among men of good will, science and democracy together offer an ever-richer life and ever-larger satisfaction to the individual. With this change in our moral climate and our rediscovered ability to improve our economic order, we have set our feet upon the road of enduring progress.

Shall we pause now and turn our back upon the road that lies ahead? Shall we call this the promised land? Or, shall we continue on our way? For "each age is a dream that is dying, or one that is coming to birth."

Many voices are heard as we face a great decision. Comfort says, "Tarry a while." Opportunism says, "This is a good spot." Timidity asks, "How difficult is the road ahead?"

True, we have come far from the days of stagnation and despair. Vitality has been preserved. Courage and confidence have been restored. Mental and moral horizons have been extended.

But our present gains were won under the pressure of more than ordinary circumstances. Advance became imperative under the goad of fear and suffering. The times were on the side of progress.

To hold to progress today, however, is more difficult. Dulled conscience, irresponsibility, and ruthless self-interest already reappear. Such symptoms of prosperity may become portents of disaster! Prosperity already tests the persistence of our progressive purpose.

Let us ask again: Have we reached the goal of our vision of that fourth day of March 1933? Have we found our happy valley?

I see a great nation, upon a great continent, blessed with a great wealth of natural resources. Its hundred and thirty million people are at peace among themselves; they are making their country a good neighbor among the nations. I see a United States which can demonstrate that, under democratic methods of government, national wealth can be translated into a spreading volume of human comforts hitherto unknown, and the lowest standard of living can be raised far above the level of mere subsistence.

But here is the challenge to our democracy: In this nation I see tens of millions of its citizens—a substantial part of its whole population—who at this very moment are denied the greater part of what the very lowest standards of today call the necessities of life.

I see millions of families trying to live on incomes so meager that the pall of family disaster hangs over them day by day.

I see millions whose daily lives in city and on farm continue under conditions labeled indecent by a so-called polite society half a century ago.

I see millions denied education, recreation, and the opportunity to better their lot and the lot of their children.

I see millions lacking the means to buy the products of farm and factory and by their poverty denying work and productiveness to many other millions.

I see one-third of a nation ill-housed, ill-clad, ill-nourished.

It is not in despair that I paint you that picture. I paint it for you in hope—because the Nation, seeing and understanding the injustice in it, proposes to paint it out. We are determined to make every American citizen the subject of his country's interest and concern; and we will never regard any faithful law-abiding group within our borders as superfluous. The test of our progress is not whether we add more to the abundance of those who have much; it is whether we provide enough for those who have too little.

If I know aught of the spirit and purpose of our Nation, we will not listen to Comfort, Opportunism, and Timidity. We will carry on.

Overwhelmingly, we of the Republic are men and women of good will; men and women who have more than warm hearts of dedication; men and women who have cool heads and willing hands of practical purpose as well. They will insist that every agency of popular government use effective instruments to carry out their will.

Government is competent when all who compose it work as trustees for the whole people. It can make constant progress when it keeps abreast of all the facts. It can obtain justified support and legitimate criticism when the people receive true information of all that government does.

If I know aught of the will of our people, they will demand that these conditions of effective government shall be created and maintained. They will demand a nation uncorrupted by cancers of injustice and, therefore, strong among the nations in its example of the will to peace.

Today we reconsecrate our country to long-cherished ideals in a suddenly changed civilization. In every land there are always at work forces that drive men apart and forces that draw men together. In our personal ambitions we are individualists. But in our seeking for economic and political progress as a nation, we all go up, or else we all go down, as one people.

To maintain a democracy of effort requires a vast amount of patience in dealing with differing methods, a vast amount of humility. But out of the confusion of many voices rises an understanding of dominant public need. Then political leadership can voice common ideals, and aid in their realization.

In taking again the oath of office as President of the United States, I assume the solemn obligation of leading the American people forward along the road over which they have chosen to advance.

While this duty rests upon me I shall do my utmost to speak their purpose and to do their will, seeking Divine guidance to help us each and every one to give light to them that sit in darkness and to guide our feet into the way of peace."

Franklin Delano Roosevelt, Second Inaugural Address

"So, you can laugh at or disparage the demonstrators all you want. You can call them spoiled, silly or sophomoric. You can single out the fringe and think it’s representative of the whole. But that won’t change the fact that this demonstration has touched a nerve. A rag-tag group is standing up where the government, regulators, media and business elites have rolled-over and played dead. They are shining a light on the financial cancer at the heart of America."

Jim Rickards, Occupy Wall Street

"Tricks and treachery are the practice of fools, that don't have brains enough to be honest."

Benjamin Franklin

"Significant changes in the growth rate of money supply, even small ones, impact the financial markets first. Then, they impact changes in the real economy, usually in six to nine months, but in a range of three to 18 months. Usually in about two years in the US, they correlate with changes in the rate of inflation or deflation.This is much more than a liquidity trap. The financial system is broken. It is corrupted and distorted, and it is acting like a weight on the real economy. And the banking system has been broken since 1990's. Perhaps broken is not quite the right word since it implies some accident and not a willful campaign of intent.

The leads are long and variable, though the more inflation a society has experienced, history shows, the shorter the time lead will be between a change in money supply growth and the subsequent change in inflation."

Milton Friedman

Vanderbilt Magazine

Missteps to Mayhem

By Michael Burry

"...Our global village underestimated many risks throughout the 1990s, as is typical of a generally good economic time. As we faced 9/11, the stock market crash of 2002, the Enron and WorldCom scandals and eventually war, the Federal Reserve Board stepped in, cutting the discount rate it charged lenders from 6 percent to roughly 1 percent in order to stave off recession. Other key short-term interest rates followed.

Not coincidentally, from 2001 to 2003 we saw American home prices, which had largely moved in line with household income through the decades, suddenly accelerate up and away from the household-income trend line. Rapidly declining short-term rates hit lows not seen since the aftermath of the Great Depression, inducing a boom in adjustable-rate mortgages.

The homeowner’s dollar went further during that teaser-rate period, so home prices rose unnaturally. Risk would be low as long as home-price appreciation was strong under this paradigm, thanks to refinancing options.

It was a positive feedback loop with the full blessing of the U.S. government. Amid early fears that the housing market was getting ahead of itself in 2003, Federal Reserve Board Chairman Alan Greenspan assured everyone that national bubbles in real estate simply do not happen.

I disagreed. As I surveyed the national trends in housing, I wondered whether common sense ought to rule against the application of precedent to the unprecedented. But Greenspan went on to advise in 2004 that new types of adjustable-rate mortgages were being underutilized. In 2005 he allowed technology used by subprime lenders to get subprime borrowers into homes. Tragically for all of us, the Federal Reserve had authority to block lending activity it deemed unworthy of such treatment, but it had no will to do so...

By fall 2004, I noted for my investors that Countrywide Financial, a very large national mortgage lender, was reporting subprime mortgage originations up 158 percent year over year, despite a 24 percent decline in overall loan originations. Evidence was manifest: Banks were chasing bad credit, inclusive of housing speculators. The only question was how far they could go.

Ominously, fraud jumped. The point at which the provision of credit was most lax, in my mind, would mark the point of maximal price in the asset. I imagined the top end of the housing market would be marked by a climate in which borrowers of subprime quality were enticed to buy with teaser-rate monthly payments near zero. I was very aware lenders would take this to the nth degree. Banks could sell loans they did not want to keep through Wall Street, to investors who were ravenous for yield.

Importantly, because subprime mortgages were being turned into securities, there were mandatory regulatory filings—and that’s how I educated myself about the sector. At times I felt I was the only one reading these filings.

By summer 2005 these documents revealed that interest-only mortgages had taken a substantial share in the subprime market. Just a year or so after they were introduced, more than 40 percent of subprime originations were passing through Wall Street on their way to investors. This was up from 10 percent a year earlier. At the same time, second-lien mortgages ramped up significantly. Stated income options available to borrowers inspired a new vernacular: the “liar loan.” In some mortgage pools, 40 percent of subprime loans were for second or vacation homes...

Incredibly, it would be reported later that more than $60 trillion in credit derivatives were in effect at their peak. To use a bit of hyperbole: That is roughly equal to the gross product of the entire world. How could that be? Credit derivatives on an underlying asset could be worth multiple orders of magnitude more than the asset itself because all asset-backed derivative securities are settled in cash—pay as you go. That was the secret sauce of the Doomsday Machine.

And so the crisis unfolded, with the market providing a signal far too late. Federal Reserve Chairman Ben Bernanke and Treasury Secretary Hank Paulson continued to underestimate the situation. I was apoplectic.

Paulson now claims that even if he had known what was going to happen, he couldn’t have done anything about it. He had just joined the U.S. Treasury in the summer of 2006. But he came from the top job at Goldman-Sachs, and once he was treasury secretary, he orchestrated government takeovers of AIG, Fannie Mae and Freddie Mac—absolutely unthinkable actions just a few years ago. Paulson was anything but an impotent tool, but if he actually felt that way, it is a devastating commentary on how our government works.

As books and articles about the crisis proliferate, it becomes clear that at nearly every failed institution and every relevant department of government, someone had insight every bit as good as mine, and in many cases better. However, none of these people was in the top job. That our CEOs, our governors and our chairmen did not see this coming, did not adequately prepare their constituencies, is an indictment of the manner in which we choose and enable our leaders...

I worry about the future of a nation that would refuse to acknowledge the true causes of the crisis. A historic opportunity was lost. America instead chose its poison as its cure, and the second “Greatest Generation” would never be born.

Today I expect the U.S. government to attempt continuing an easy money policy into the next presidential term—past the meat of the foreclosure crisis, and past the corporate and public financing humps that are upcoming. Junk bonds, incredibly, again are at all-time highs. Quantitative easing seems to be working for now. But this is an invalid validation of what America is doing, a Pyrrhic gamble. As we continue to debase our currency, Bernanke says he is not printing money. Yet I receive an email every day from the Fed saying we just bought another $7 billion or $8 billion in treasuries, monetizing the debt. The scope and breadth of quantitative easing raise severe questions about the Treasury’s needs.

Government borrowing of money for the purpose of injecting cash into society, bailing out banks, brokers and consumers, is an easy decision for a population that has not yet learned that short-sighted easy strategies are the route to long-term ruin. We never quite achieved the catharsis necessary to stoke a deep reevaluation of our wants, needs and fears.

Importantly, the toxic twins—fiat currency and an activist Fed—remain even more firmly entrenched with the financial reforms of last year. The Federal Reserve, having acquired new powers of regulation, has insisted that nothing in the field of economics or finance was of any help in predicting the crisis—period, no more comments. It’s a worthless conclusion that guarantees we’ll make the same mistake again and again.

We need better leaders, but frankly this isn’t going to happen. A problem cannot be solved if it is never acknowledged.

Taxes need to be raised, spending needs to be cut, and loopholes need to be shut if we are to have any hope of returning to a stable base. Home ownership should not be a policy of the U.S. government. The banking system needs substantial reform and bank breakups. Glass–Steagall needs a second run in a strong form. And 22.5 million public workers have no business unionizing against the taxpayer. The list of things that won’t happen—but should happen—goes on and on.

By 2020, interest expense on our national debt could very well exceed $1 trillion. All personal income taxes collected in the U.S. in one year do not total $1 trillion. Our country’s math is scary big, but even scarier is that it simply doesn’t work...