17 May 2012

A Quick Look At the Market Technicals: SP500, Gold, Silver, VIX

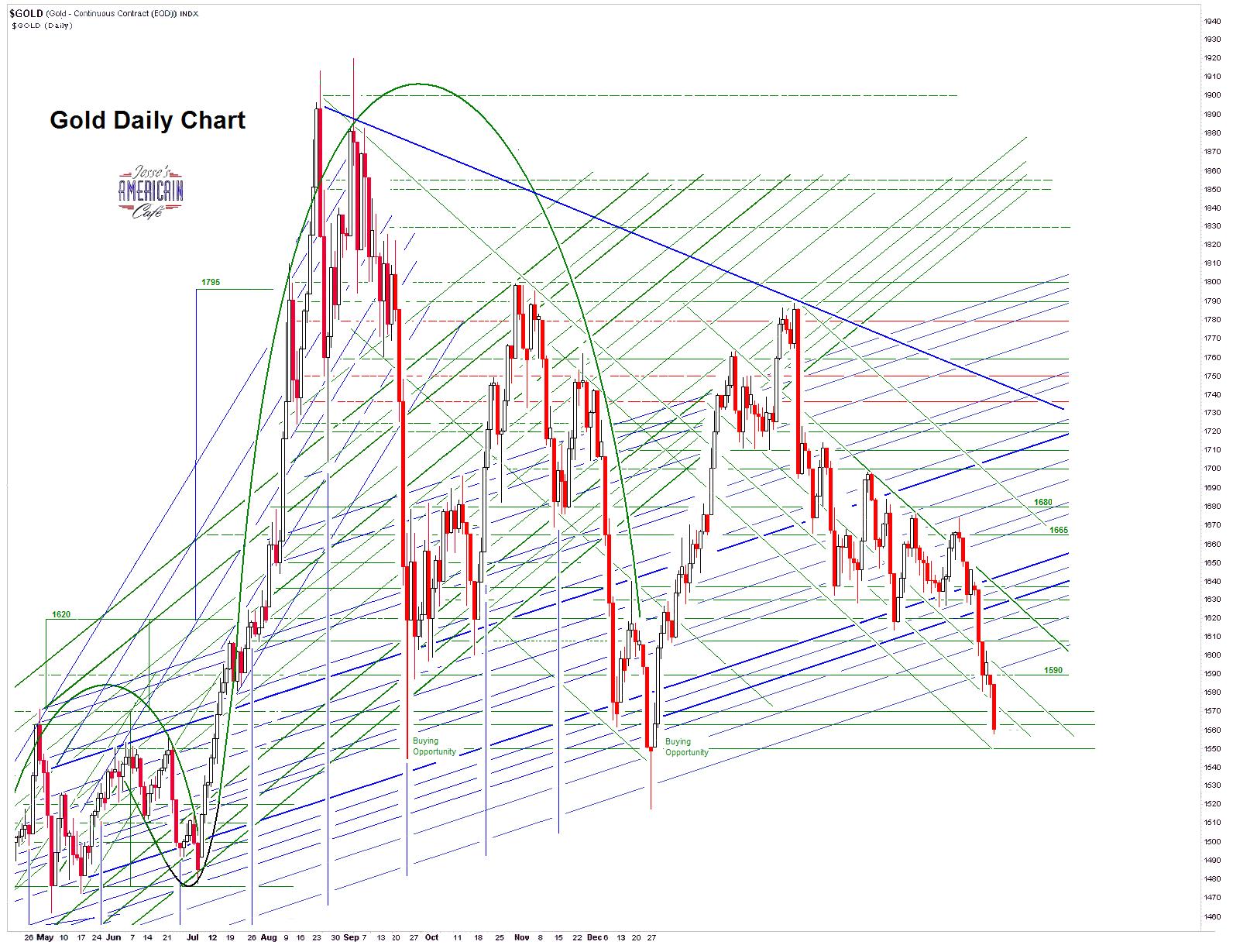

The gold and silver charts have not been updated for today's rally.

As is clear from the metals charts, gold and silver were DEEPLY oversold short term. So this *could* be a relief rally. The talking heads say it was because of the weak leading indicators this morning with overtones of QE3, but I think it is more likely that the momentum traders took it as low as it would go without hitting the physical markets and threatening a major divergence.

We will know if this is a new bull leg in the metals if they can take out and hold their exponential moving averages on the charts below decisively.

You cannot see it on this chart, but on my daily charts it appears that gold and silver are in a trading range, with the triangles being negated.

Stocks are also short term oversold. I hear that Facebook will go out at $38 per share tonight, and will likely color the market action tomorrow. The SP may tip its hand in the last hour of trading into the weekend.

It appears that tomorrow is the option expiration for May in stocks, and so I suspect that the selling today are the usual animal spirits one sees around such expirations, and tomorrow there will be quite a bit of pressure to maintain a 'stable market' for the secondary shenanigans on Facebook.

So I have taken off all stock short hedges and am letting the bullion run. I *might* put them on into the close before the weekend depending on what I see on the tape.

Another Take on Inequality From Nick Hanauer and the Restoration Roundtable

I would add that the source of the payment for the consumption is a major factor.

If it comes from a growing median wage that permits consumption and savings by the broader public, then the virtuous cycle is engaged.

However, if the consumption comes from borrowing and credit expansion with the benefits flowing overseas or to the wealthy, there is no virtuous cycle, or the amelioration of misery. Debt in this case is a narcotic.

In the end it is all about balance, and reform. Stimulus, taxing the rich, and austerity by themselves will only further distort the distortions. Although it should be noted that large imbalances in wealth go hand in hand in imbalances of power, which tend to erode the happy moderation of a functioning democracy with a vibrant middle class. And the 15% tax on capital gains and the other tax loopholes used by the wealthy is an exorbitant privilege, repugnant to a government by the people.

Imbalances in wealth and distorted domestic economies are often the impetus to war and empire, as nations ruled by the superwealthy seek overseas markets in colonies. Such economies only maintain themselves by continual expansion and domination.

The recovery, in whatever form it takes, will be sustainble when the median wage improves.

It is astounding how significantly one idea can shape a society and its policies. Consider this one.

If taxes on the rich go up, job creation will go down.

This idea is an article of faith for republicans and seldom challenged by democrats and has shaped much of today's economic landscape.

But sometimes the ideas that we know to be true are dead wrong. For thousands of years people were sure that earth was at the center of the universe. It's not, and an astronomer who still believed that it was, would do some lousy astronomy.

In the same way, a policy maker who believed that the rich and businesses are "job creators" and therefore should not be taxed, would make equally bad policy.

I have started or helped start, dozens of businesses and initially hired lots of people. But if no one could have afforded to buy what we had to sell, my businesses would all have failed and all those jobs would have evaporated.

That's why I can say with confidence that rich people don't create jobs, nor do businesses, large or small. What does lead to more employment is a "circle of life" like feedback loop between customers and businesses. And only consumers can set in motion this virtuous cycle of increasing demand and hiring. In this sense, an ordinary middle-class consumer is far more of a job creator than a capitalist like me.

So when businesspeople take credit for creating jobs, it's a little like squirrels taking credit for creating evolution. In fact, it's the other way around.

Anyone who's ever run a business knows that hiring more people is a capitalists course of last resort, something we do only when increasing customer demand requires it. In this sense, calling ourselves job creators isn't just inaccurate, it's disingenuous.

That's why our current policies are so upside down. When you have a tax system in which most of the exemptions and the lowest rates benefit the richest, all in the name of job creation, all that happens is that the rich get richer.

Since 1980 the share of income for the richest Americans has more than tripled while effective tax rates have declined by close to 50%.

If it were true that lower tax rates and more wealth for the wealthy would lead to more job creation, then today we would be drowning in jobs. And yet unemployment and under-employment is at record highs.

Another reason this idea is so wrong-headed is that there can never be enough superrich Americans to power a great economy. The annual earnings of people like me are hundreds, if not thousands, of times greater than those of the median American, but we don't buy hundreds or thousands of times more stuff. My family owns three cars, not 3,000. I buy a few pairs of pants and a few shirts a year, just like most American men. Like everyone else, we go out to eat with friends and family only occasionally.

I can't buy enough of anything to make up for the fact that millions of unemployed and underemployed Americans can't buy any new clothes or cars or enjoy any meals out. Or to make up for the decreasing consumption of the vast majority of American families that are barely squeaking by, buried by spiraling costs and trapped by stagnant or declining wages.

Here's an incredible fact. If the typical American family still got today the same share of income they earned in 1980, they would earn about 25% more and have an astounding $13,000 more a year. Where would the economy be if that were the case?

Significant privileges have come to capitalists like me for being perceived as "job creators" at the center of the economic universe, and the language and metaphors we use to defend the fairness of the current social and economic arrangements is telling. For instance, it is a small step from "job creator" to "The Creator". We did not accidentally choose this language. It is only honest to admit that calling oneself a "job creator" is both an assertion about how economics works and the a claim on status and privileges.

The extraordinary differential between a 15% tax rate on capital gains, dividends, and carried interest for capitalists, and the 35% top marginal rate on work for ordinary Americans is a privilege that is hard to justify without just a touch of deification.

We've had it backward for the last 30 years. Rich businesspeople like me don't create jobs. Rather they are a consequence of an eco-systemic feedback loop animated by middle-class consumers, and when they thrive, businesses grow and hire, and owners profit. That's why taxing the rich to pay for investments that benefit all is a great deal for both the middle class and the rich.

So here's an idea worth spreading.

In a capitalist economy, the true job creators are consumers, the middle class. And taxing the rich to make investments that grow the middle class, is the single smartest thing we can do for the middle class, the poor and the rich.

Thank You.

Nick Hanauer

Prepare to meet Nick Hanauer. He's a venture capitalist from Seattle who was the first non-family investor in Amazon.com. Today he's a very rich man. And, somewhat jarringly, he's screaming to anyone who will listen that he, and other wealthy innovators like him, doesn't create jobs. The middle class does - and its decline threatens everyone in America, from the innovators on down.

From The Inequality Speech That TED Won't Show You at National Journal.

Corzine Syndrome: JPM's Stealth Prop Trading Unit Was Crafted for Risky Profit and Reported Directly To Jamie Dimon

I want to put a spike in all this spin around the CEO defense, that poor Jamie could not have possibly known what was going on in London because the company was so large, and he is such a busy man. Sarbanes-Oxley was designed to put a stop to that lame excuse touted out by defense lawyers and apologists in the media every time something like this happens.

The CIO operation was transformed under Jamie's direction as a dodge to the impending Volcker Rule, set to take effect in July, that prohibited this kind of risky prop trading by institutions backed with deposit insured money and both explicit and de facto government guarantees.

He wanted it up to be what it was, an opaque profit center. It probably sounded like a good idea, taking a risk hedging and reduction function and turning it in to a profit center. Because of the accounting differential between the CIO and the portfolios it was alleged to hedge, one could take profits and not realize losses in a quarter, which provided a nice billion dollar cushion for earnings. Every industry has their accounting dodges like this that allow a company to 'manage earnings.' In tech it is in acquisition accounting and inventory writedowns.

But in their clumsy piggishness, the JPM CIO traders took their usual overly large and manipulative positions, as they have done in other markets, masquerading as hedges. But this particular credit market was too narrow and specialized, and they stepped on the toes of savvy market insiders. And it blew up in their faces.

When the media called Jamie on it a few months ago, after traders complained that 'the London Whale' was rigging market prices, he called it a legitimate hedging operation and dismissed it as 'not a problem.'

The same thing is going on in other markets as well, even now, and on a much larger scale with larger positions and more leverage. The difference is that it is smaller traders and the public that are being hurt, while much of the risk is being misrepresented and unrealized, for now.

And so the regulators are sitting on their hands and doing nothing about it because they are being discouraged from taking action by powerful interests in the Administration and the Congress. JPM has long been known as the government's 'go to guy' when something needs to be done to unofficially intervene in markets.

Remember, it was pressure from the Geithner Treasury and the Fed at the behest of JPM that created the loophole that would have permitted the CIO unit to continue to function as a prop trading unit even after the Volcker Rule supposedly shut such risky ventures down.

And they are afraid of what will happen to JPM if these market positions, particularly in the derivatives and metals markets, are exposed for what they really are, and their own involvement in allowing it to happen for so long. That is the credibility trap, and the reason for the remarkable lack of investigation and prosecution of financial fraud.

International Financing Review

JP Morgan investment unit played by different high-risk rules

16 May 2012

The JP Morgan Chase unit that lost more than US$2 billion through a failed hedging strategy had looser risk controls than the rest of the bank, according to people familiar with the situation.

The risk of losses is tallied by the bank using a so-called value at risk (VaR) calculation. However, the Chief Investment Office, the unit responsible for the high-profile loss that JP Morgan disclosed last Thursday, had a separate VaR system.

It used a less stringent calculation that gave a lower risk assessment of its trades, according to people who previously worked at the bank.

The unit also reported directly to CEO Jamie Dimon, a factor which allowed it to maintain a separate risk monitoring set-up to other parts of the investment bank, these people said.

“It was very large, but was never very transparent, and it wasn’t clear that they had an appropriate funding cost,” said the source with direct knowledge of the CIO. “They were running more risk than the investment bank – and with no peer review process (from those in the investment bank).”

Despite repeated warnings from executives inside the firm as long ago as 2005, the CIO unit remained notably free from oversight.

A source with knowledge of the situation said that these warnings included the size of the CIO, the fact that its risk reporting was not transparent and the scope for the unit to get “bigger and bigger” because it had a lower cost of funding than the rest of the investment bank.

Until April, the CIO unit’s unusual autonomy allowed it to build up risky positions without triggering alarms.

Indeed, the unit was encouraged to be a profit center, as well as hedging against risk, a source with direct knowledge of the unit said. Ina Drew, who headed the unit, earned more than US$15 million in each of the past two years, making her among the highest-paid executives at the bank and one of the most compensated women on Wall Street.

Drew could not be reached for comment... (Did you check under the bus? That is where masters-of-the-universe like Corzine and Dimon throw the ladies when they are done using them to establish plausible deniability. - Jesse)

Read the rest here.

16 May 2012

Gold Daily and Silver Weekly Charts - Facebook, Greece, and the Hollow Men

I am leaving a bit early this evening.

Facebook and Greece are dominating the market, and both in their own ways are contributing to the selling.

The wiseguys see Facebook coming out at around 36-38 and intend to run it up I think to the 60+ are and then dump it for a quick return. So they are raising cash and, gasp, selling even AAPL to do it.

Greece has the markets edgy for all the usual reasons. The status quo does not like it when people stand up to them.

The Open Interest in the precious metals on the Comex is doing some odd things, staying steady or even rising on sell offs. That is not long liquidation yet. It is more of a transfer or ownership and the expansion of 'the big short.'

More on this tomorrow.

SP 500 and NDX Futures Daily Charts - Facebook Cometh Tomorrow Night

Leaving a bit early today. Will catch up tomorrow.

Facebook will price after the bell tomorrow. Expectations are for about $36 per share or so.

There was some interesting hypocrisy on Capitol Hill this morning by the Republicans who are red-faced over the JPM antics, since they have been adamant about turning back regulations.

A friend sent this in to my email. I did not see it, so I do not know if it is literally true, but if so I thought my friend's observation was brilliant.

I watched part of a press conference today where the NYPD commissioner said, with a straight face, that a $50,000 SUV, stolen in NYC, could be sold in Africa for $150,000. Not surprisingly, not a single person there asked him why, if that was true, someone didn’t simply buy the vehicles and ship them there legally.

Hot Money Bets Backed By Taxpayers: Extreme Moral Hazard of 'Too Big To Fail' - Credibility Trap

The professor makes some excellent points about the real world of finance that bear some serious thought. He certainly left the Bloomberg spokesmodels yammering in search of a sound byte.

He misses a key point however. It is not that Jamie Dimon does not know, or even that he cannot know, about the risky speculation in his firm. It is that the system is so designed now that in the long run he is heavily incented not to care, as long as he can maintain a plausible deniability. There are management controls, policy, and objectives that flow down from the top in any large corporation. Dimon had a personal hand in recrafting the CIO to do what it was doing in order to sidestep the Volcker Rule. This was no rogue operation.

As long as the profits are rolling in, the band plays on and the players keep dancing.

It is the same problem that led to the financial crisis, and the collapse of so many of the brokerage and investment houses, followed by a policy that made a show of reform, but concentrated their recklessness selfishness into a few enormously larger vessels, making them all the more effective at gaming and corrupting the system.

That is the problem one faces when the public is apathetic, and the political leadership is composed of cynically pragmatic dealmakers and shallow but ardent ideologues driven by narrow personal expediency, not firmly rooted in history, moral principles, and stewardship for the broader public trust.

It touches on an age old scheme in the mix of banking and speculation that most modern day economists seem to have forgotten, perhaps conveniently. Better to keep one's nose buried in intricate obfuscation than speak to the heart of things, the things that really matter, and risk professional isolation.

It is a sweet deal when one is permitted to play with enormous sums of money and leverage, keeping the wins for yourself, and laying off the losses on the public, enabled by the Fed and a system thoroughly rotten with corruption.

And when they go along the road with you long enough, you can obtain permission to do almost anything, and have them turn a blind eye to it, rather than be exposed along with you. That is the credibility trap.

"Gentlemen! I too have been a close observer of the doings of the Bank of the United States. I have had men watching you for a long time, and am convinced that you have used the funds of the bank to speculate in the breadstuffs of the country.

When you won, you divided the profits amongst you, and when you lost, you charged it to the bank. You tell me that if I take the deposits from the bank and annul its charter I shall ruin ten thousand families. That may be true, gentlemen, but that is your sin!

Should I let you go on, you will ruin fifty thousand families, and that would be my sin! You are a den of vipers and thieves. I have determined to rout you out, and by the Eternal, (bringing his fist down on the table) I will rout you out."

Andrew Jackson, original minutes of the Philadelphia bankers sent to meet with President Jackson February 1834, Andrew Jackson and the Bank of the United States (1928) by Stan V. Henkels

(h/t Yves)

Goldman Data Admits to Naked Short Selling, Disclosing Client Positions, Abusive Legal Practices

“He should be someone we can work with, especially if he sees that cooperation results in resources, both data and funding, while resistance results in isolation.”

Goldman Sachs

"To be a sophisticate in the 21st century requires the ability to shut one's eyes and one's mind to anything that one does not want to see or think about. The more glaring that the contradiction between what is said and what is done becomes, the harder it is to remain sophisticated. The tragedy is that the only alternative, that of becoming an independent thinker, is looked upon as more terrifying than to go on pretending to be deaf, dumb and blind."

Bill Buckler, The Privateer

Is there any wonder why economics stands as a disgraced profession, and the mainstream media is so oddly silent on so many things? Financial corruption permeates and undermines the fabric of society and its thought, by action and example.

It both frightens and tantalizes, rewards and victimizes. And as that contagion spreads into the government, as it inevitably does seeking power and greed, no one is safe.

"False opinions are like false money, struck first of all by guilty men, and thereafter circulated by honest people who perpetuate the crime without knowing what they are doing."Standing for the truth can be isolating and painful, especially in a people who have given themselves over to selfishness and corruption. So much easier to take the money, and just go along to get along.

Joseph de Maistre

Often all one has to do is to close their eyes and say the words. It starts so easily. Who does not want to be flattered and favored, to be accepted as one of the better people, not one of them?

"This is the way in which he conceals from you the kind of work to which he is putting you...He scoffs at times gone by; he scoffs at every institution which reveres them. He prompts you what to say, and then listens to you, and praises you, and encourages you. He bids you mount aloft. He shows you how to become as gods.Do you imagine that this time will be different? This is how an educated people of ordinarily good spirits can learn over time to tolerate almost anything, and in the end ignore even torture, cruelty, and murder, and to defend the indefensible with glib lies and slogans, until one day their grandchildren look at them with horror and revulsion asking, 'How could you have allowed this? What were you thinking? What have you become?'

Then he laughs and jokes with you, and gets intimate with you; he takes your hand, and gets his fingers between yours, and grasps them, and then you are his."

J.H.Newman, The Time of Antichrist

Rolling Stone

Accidentally Released - and Incredibly Embarrassing - Documents Show How Goldman et al Engaged in 'Naked Short Selling'

By Matt Taibbi

May 15, 2012

It doesn’t happen often, but sometimes God smiles on us. Last week, he smiled on investigative reporters everywhere, when the lawyers for Goldman, Sachs slipped on one whopper of a legal banana peel, inadvertently delivering some of the bank’s darker secrets into the hands of the public.

The lawyers for Goldman and Bank of America/Merrill Lynch have been involved in a legal battle for some time – primarily with the retail giant Overstock.com, but also with Rolling Stone, the Economist, Bloomberg, and the New York Times. The banks have been fighting us to keep sealed certain documents that surfaced in the discovery process of an ultimately unsuccessful lawsuit filed by Overstock against the banks.

Last week, in response to an Overstock.com motion to unseal certain documents, the banks’ lawyers, apparently accidentally, filed an unredacted version of Overstock’s motion as an exhibit in their declaration of opposition to that motion. In doing so, they inadvertently entered into the public record a sort of greatest-hits selection of the very material they’ve been fighting for years to keep sealed...

Read the rest here.

Here is the link to the Goldman court filing.

Eliot Spitzer on JPM and Bank Reform

“For all sad words of tongue and pen, The saddest are these, 'It might have been'.”

John Greenleaf Whittier

Flawed indeed.

Slate

Flawed Dimon

By Eliot Spitzer

May 14, 2012

What to do with Jamie Dimon? The CEO and Chair of JPMorgan Chase has tried so hard in the past several years to seem the “good banker.” He is so charming and gracious, yet all the while lobbying, cajoling, pushing, and wheedling to eviscerate any semblance of real reform on Wall Street. He shrugged off the cataclysm of 2008 as just something that happened, like the weather—no need for any structural reform.

Now the chickens have come home to roost—at least 2 billion of them—and it is clear that Chase is like every other big financial institution with distorted incentives. Thanks to a backstop of a federal guarantee, these gigantic institutions get to keep all the upside of crazy bets while the government gives them all the downside protection they need. Earlier this year, Dimon pooh-poohed concerns about the risks his traders were taking. Did Dimon not understand those risks, not care to know about them, or actually mislead the public about them?

But it isn’t so much money, they cry! True, in the context of Chase’s balance sheet, a $2 billion loss can be absorbed. But it shows once again the impossibility of trusting the banks in the absence of structural reform and regulation to control their willingness to take almost unmitigated risk. Of greater significance than the size relative to Chase’s balance sheet is that the loss was in a relatively stable market in which most people are finding it easy to trade. Imagine if the market had been choppy—the losses could have been even more gargantuan—and if several institutions had been in the same position, then the aggregate effect could have become once again cataclysmic.

It was Chase’s own lobbying on Capitol Hill and with the Treasury, the Fed, and other agencies that made these bets arguably permissible within the scope of hedging under the Volcker rule. Had they not lobbied and pushed and delayed and made the rule more complicated, these bets would have been illegal or at a minimum so transparent as to have been smaller and less damaging. The banks love to complain about the complexity of these rules. But the rule as proposed by Paul Volcker was simple. It is only because of the very lobbying by the banks that the complexity and loopholes crept in...

Read the rest here.

15 May 2012

Gold Daily and Silver Weekly Charts - More Liquidation on Greece and Facebook

More concern on Greece and what will happen if it leaves the Euro had traders fleeing risk and commodities including gold and silver.

There is also quite a bit of secondary liquidation being done as traders raise cash for 'the Big Flip' when Facebook comes out after the bell on Thursday.

Expectations are for the stock to price in the 30's, and then run up in the secondary market into the 60's at which point those who had the IPO can liquidate if the momentum traders provide liquidity and institutions and mom and pop pick up the slack.

I am still long gold and short stocks. I hold no miners or silver. I am holding about 25% cash in my trading account and thinking about when to deploy it. Unless Europe collapses I think the bottom is very close. I would like to see an 'intraday V' to punctuate it.

SP 500 and NDX Futures Daily Charts - RNN Interviews Bill Black on JPM

Fears about what will happen with Greece and the Euro weighed on stocks.

There is also secondary liquidation as funds raise cash to play the big pop in the Facebook IPO which prices after the bell on Thursday.

Expectations are that the stock will come out in the 30's and pop higher to 50's at which point the momentum traders will start to flip it and hand it off to mom and pop and the pension funds.

14 May 2012

Nomi Prins: On JPM, the Whale Man, and Glass-Steagall

This is one of the better commentaries on JPM and the history and imperatives of banking regulation that I have seen recently.

I do not wish to beat this to death, but I have read too many glib economist and stock tout comments sloughing this off as 'no big deal.' Not surprisingly, these were many of the same people who said similar things during the build up of the credit bubble and the financialization of the real economy.

And I also expected something like this to happen in the derivatives markets, following the thefts of customer money at MF Global. It just happened a little sooner than I had imagined. Things are progressing quickly.

JPM Chase Chairman, Jamie Dimon, the Whale Man, and Glass-Steagall

By Nomi Prins

May 11, 2012

It was fitting that while President Obama and his Hollywood apostles broke fundraising records at a sumptuous $40,000 per plate dinner at George Clooney’s place, word of JPM Chase’s ‘mistake’ rippled through the news. Not long ago, Dimon’s name was batted about to become Treasury Secretary. But as lines are drawn and pundits take sides in the Jamie Dimon ego deflation saga – or, as I see it - why big banks should be made smaller and then, broken up into commercial vs. speculative components ala Glass Steagall – it’s important to look beyond the size of the $2 billion dollar (and counting) beached whale of a trading loss.

Yes, $2 billion in the scheme of JPM Chase’s book and quarterly earnings is tiny, a ‘trading blip’ as it’s been called by some business press. But that’s not a mitigating factor in what it represents. In this era dominated by a few consolidated and complex banks, the very fact that it’s a relatively small loss IS the red flag.

First - because the loss could (and will) grow. Second, because even if it doesn’t, it’s a blatant example of a big bank incurring un-due risk within a barely regulated, highly correlated financial markets. It only takes another Paulson hedge fund, or a trading desk at Goldman Sachs, to short the hell out of the corporates that JPM Chase is synthetically long, or take whatever the other side really is, to create a liquidity crisis that will further screw those least able to access credit – individuals, small businesses, and productive capital users.

We know this. We’ve seen this. We're in this. There’s no such thing as an isolated trading loss anymore. And yet Jamie Dimon, seated atop the most powerful bank in the world, has smugly led the charge to adamantly oppose any moves to alter the banking framework that allows him, or any bank, to call a bet - a hedge or client position or market-making maneuver - with central bank, government official, and regulatory impunity.

Flashback to the unimaginable in 1933

It’s 1933 and the country has undergone several years of painful Depression following the 1920s speculation that crashed in the fall of 1929. Investigations into the bank related causes began under Republican President, Herbert Hoover and continued under Democratic President, FDR...

Read the rest here.

Partnoy's Complaint: Lawmakers Must Heed the Wisdom of the 1930s

Here is Frank Partnoy's prescription for financial reform. Essentially he says that half measures are not sufficient. Wall Street will always find loopholes in weak regulation, and they have plenty of help in this in the halls of power in Washington, and in the think tanks, universities and the media.

Even President Obama seems to be in denial about the effectiveness of his reforms, and the health of the US banking system. Obama: JPM One of the Best Managed Banks His own Treasury pressured regulators and lawmakers to create the loophole that allowed the loss in London, and that his administration has a horrible record in investigating and prosecuting bank fraud.

I do not think the US is ready to insist on serious reform. It will take another crisis. The anti-regulatory slogans are too effectively ingrained in the public psyche. And self-deception is a powerfully addictive state of mind. Especially for those whose expansive lifestyles depend on it.

Financial Times

Rebuild the Pillars of 1930s Wall Street

By Frank Partnoy

May 13, 2012

...JPMorgan’s losses have generated renewed interest in tightening the “Volcker rule”, which would attempt to ban speculative trading by banks. Yet the losses also illustrate why the Volcker rule will not work. The synthetic credit trades were not proprietary bets; they were massive, mismatched hedges. (Well they were prop bets but were masquerading as hedges. But that merely underscores the problem with the Volcker Rule and regulating specific guidelines that can be circumvented by pathological liar as Mr Partnoy indicates in the next paragraph. - Jesse)

The current version of the rule arguably would not have barred these trades (It would have, except for the hedging loophole that JPM had obtained with the assistance of the Fed and the Treasury - Jesse). Moreover, wherever the line between speculating and hedging is drawn, Wall Street will easily find a way to step over it. It would be impossible for regulators to police what is a hedge and what is not.

A better way to stop the cycle of financial fiascos would be to emulate 1930s reforms, when Congress erected twin pillars of financial regulation that supported fair, well-functioning markets for five decades. First was a mandate that banks disclose important financial information. In today’s complex terms, that would mean disclosing not just a value-at-risk number but also worst-case scenarios. The law should require JPMorgan to tell investors what would cause a $2bn loss.

The second pillar was a robust anti-fraud regime that punished officials who did not tell the full truth. Unfortunately, this has been eroded by legislation and judicial decisions that make it more difficult for shareholders to allege fraud. Prosecutors are also reluctant to bring criminal cases, leaving the Securities and Exchange Commission to mount largely toothless civil actions. Instead, the law should punish anyone who defrauds investors by citing one value-at-risk number and then losing 30 times that amount.

By rebuilding these two pillars, regulators could create stronger markets and greater trust. At a minimum, they could wean bank managers, and themselves, off flawed maths. They could stop allowing banks to satisfy disclosure obligations simply by reporting one inevitably inaccurate value-at-risk number. They could give Mr Dimon more than a slap...

Read the entire article from the Financial Times here.

Gold Daily and Silver Weekly Charts - The Unhappy Life of Sir Francis Bacon

I ignored the markets for the most of today, although I did add a bit to my bullion position 'on the dip' as they say, and took a little off the more volatile portion of my short equity hedge. Today was a good day to avoid the noise and reconnect with the broad perspective.

I spent part of the day rereading Dean Church's biography of Sir Francis Bacon from my library. I first came across Church in references and descriptions of him from his contemporaries. I have of course read his Oxford Movement. He is an interesting man, and was a notable Dean of St. Paul's among other things.

This introduction to his biography of Bacon excerpted below struck home as somewhat emblematic of many of the figures of our own age, if not the generation itself, although I am quite certain that most of the public characters it might describe were not nearly so gifted as Bacon, being largely creatures of privilege, so they might not have sold themselves so cheaply or tragically as the great man did. They merely serve the system that raised them up.

Tragedy must entail the fall either from greatness, or from the failure to realize the greatness of potential. On the whole, I think Messrs. Geithner and Bernanke are fully valued, as they say, and then some. As for Obama, there is still some question, but it does not easily maintain a foothold. As for the rest, tools and cravens, soon and well forgotten as empty souls, dried leaves on cobblestones.

We are a people in need of moral giants but served, alas, by what we have deserved.

"All his life long his first and never-sleeping passion was the romantic and splendid ambition after knowledge, for the conquest of nature and for the service of man; gathering up in himself the spirit and longings and efforts of all discoverers and inventors of the arts, as they are symbolised in the mythical Prometheus.

He rose to the highest place and honour; and yet that place and honour were but the fringe and adornment of all that made him great. It is difficult to imagine a grander and more magnificent career; and his name ranks among the few chosen examples of human achievement.

And yet it was not only an unhappy life; it was a poor life. We expect that such an overwhelming weight of glory should be borne up by a character corresponding to it in strength and nobleness. But that is not what we find.

No one ever had a greater idea of what he was made for, or was fired with a greater desire to devote himself to it. He was all this. And yet being all this, seeing deep into man's worth, his capacities, his greatness, his weakness, his sins, he was not true to what he knew.

He cringed to such a man as Buckingham. He sold himself to the corrupt and ignominious Government of James I. He was willing to be employed to hunt to death a friend like Essex, guilty, deeply guilty, to the State, but to Bacon the most loving and generous of benefactors.

With his eyes open he gave himself up without resistance to a system unworthy of him; he would not see what was evil in it, and chose to call its evil good; and he was its first and most signal victim."

R. W. (Dean) Church, Francis Bacon

SP 500 and NDX Futures Daily Charts

By and large a tedious day, better spent reading than watching. High drama and all that, but the Facebook IPO awaits.

I did add some bullion 'on the dip' and trimmed up the more volatile hedge which had swollen in value.

Keiser Report Interviews John Titus of 'Bailout' Which Premieres on 16 May in Chicago

There is a fairly nice description of the 'credibility trap' in this very interesting discussion between Max Keiser and John Titus.

I had said in my major forecast from 2005 that at some point the Bankers would make the US an 'offer which they think that they cannot refuse.' The film references that sort of negotiation tactic. There is another crisis coming, and another offer which will involve more than just money.

Here is a link to the complete show 'Central Bank Monarchs' including the discussion with Stacey Herbert.

Carl Levin On JPM's Exploitation of the Loophole Which the Fed and Treasury Helped to Create

Carl Levin does a good job of bringing the discussion back on point again and again.

12 May 2012

Tavakoli: JPMorgan May Be a Trading Accident Waiting To Happen

I think the next financial crisis is less than two years away, and it will strike the global real economy as badly as the banking crisis with the collapse of Lehman Brothers.

Jamie Dimon's SNAFU: JPMorgan's Other Derivatives' Losses

By Janet Tavakoli

05/12/2012

In an August 2010 commentary about JPMorgan's losses in coal trades I wrote: "The commodities division isn't the only area in which JPMorgan is vulnerable. Credit derivatives, interest rate derivatives, and currency trading are vulnerable to leveraged hidden bets. Ambitious managers strive to pump speculative earnings from zero to hero."

At issue is corporate governance at JPMorgan and the ability of its CEO, Jamie Dimon, to manage its risk. It's reasonable to ask whether any CEO can manage the risks of a bank this size, but the questions surrounding Jamie Dimon's management are more targeted than that. The problem Jamie Dimon has is that JPMorgan lost control in multiple areas. Each time a new problem becomes public, it is revealed that management controls weren't adequate in the first place.

JPMorgan's Derivatives Blow Up Again

Jamie Dimon's problem as Chairman and CEO--his dual role raises further questions about JPMorgan's corporate governance---is that just two years ago derivatives trades were out of control in his commodities division. JPMorgan's short coal position was over sized relative to the global coal market. JPMorgan put this position on while the U.S. is at war. It was not a customer trade; the purpose was to make money for JPMorgan. Although coal isn't a strategic commodity, one should question why the bank was so reckless.

After trading hours on Thursday of this week, Jamie Dimon held a conference call about $2 billion in mark-to-market losses in credit derivatives (so far) generated by the Chief Investment Office, the bank's "investment" book. He admitted:

"In hindsight, the new strategy was flawed, complex, poorly reviewed, poorly executed, and poorly monitored."

But lets get back to commodities. For several years, legendary investor Jim Rogers has expressed his concern to me about JPMorgan's balance sheet, credit card division, and his belief that Blythe Masters, the head of JPMorgan's commodities area, knows so little about commodities. Jim Rogers is an expert in commodities and is the creator or the Rogers International Commodities Index. He also sells out-of-the-money calls on JPMorgan stock. So far, that strategy has worked out well for him. (Rogers gave me permission to publicly reflect his views and his trades.) Moreover, JPMorgan is still grappling with potential legal liabilities related to the mortgage crisis.

Is Jim Rogers justified in his harsh view of JPMorgan's commodities division? After he expressed his concerns, JPMorgan's coal trade made the news, and it appeared to me that Jim Rogers is on to something. For those of you who missed it the first time, my August 9, 2010 commentary is reproduced below in its entirety. Dawn Kopecki at Bloomberg/BusinessWeek broke the story wherein Blythe Masters' quotes first appeared...

Read the rest here.

JPMorgan Used Political Influence With Fed and Treasury to Create London Loss Loophole In Volcker Rule

"It is impossible to calculate the moral mischief, if I may so express it, that mental lying has produced in society. When a man has so far corrupted and prostituted the chastity of his mind as to subscribe his professional belief to things he does not believe, he has prepared himself for the commission of every other crime."

Thomas Paine

Using political influence with the Fed and the Treasury, JP Morgan overrode concerns at the SEC and CFTC to create a broad loophole in the Volcker Rule which was designed to allow them to continue risky and highly leveraged 'prop trading' in their CIO unit under the phony rationale of 'portfolio hedging.' This is the backstory on the antics of the 'London Whale' and quite likely their rationale of 'hedging' to justify enormous and manipulative positions in other markets.

Throughout the lead up to the financial crisis, banking lobbyists used their friends at the Fed and the Treasury to suppress the warnings of regulators and undermine reforms to protect the public interest.

One of the most infamous instances was the bullying of Brooksley Born and the silencing of her warning as chairman of the CFTC by Alan Greenspan, Robert Rubin, and Larry Summers. PBS Frontline: The Warning.

This crony capitalism is one of the reasons why the financial system collapsed, and why the markets are still so dangerously unstable, despite the determined efforts to disguise it with liquidity and lax regulation. The responsibility for this goes back to the Clinton and Bush Administrations at least.

It is time to stop apologizing for and tolerating the soft corruption that has characterized the Obama Administration's policy on the financial sector since day one. The price of giving him a pass on this failure to do his job and making excuses for him is too high. The excuse that Romney will be worse is not acceptable.

The Banks must be restrained, and the financial system reformed, with balance restored to the economy, before there can be any sustained growth and recovery.

NY Times

JPMorgan Sought Loophole on Risky Trading

By Edward Wyatt

May 12, 2012

WASHINGTON — Soon after lawmakers finished work on the nation’s new financial regulatory law, a team of JPMorgan Chase lobbyists descended on Washington. Their goal was to obtain special breaks that would allow banks to make big bets in their portfolios, including some of the types of trading that led to the $2 billion loss now rocking the bank.

Several visits over months by the bank’s well-connected chief executive, Jamie Dimon, and his top aides were aimed at persuading regulators to create a loophole in the law, known as the Volcker Rule. The rule was designed by Congress to limit the very kind of proprietary trading that JPMorgan was seeking.

Even after the official draft of the Volcker Rule regulations was released last October, JPMorgan and other banks continued their full-court press to avoid limits.

In early February, a group of JPMorgan executives met with Federal Reserve officials and warned that anything but a loose interpretation of the trading ban would hurt the bank’s hedging activities, according to a person with knowledge of the meeting. In the past, the bank argued that it needed to hedge risk stemming from its large retail banking business, but it has also said that it supported portions of the Volcker Rule.

In the February meeting was Ina Drew, the head of JPMorgan’s chief investment office, the unit that suffered the $2 billion loss...

JPMorgan wasn’t the only large institution making a special plea, but it stood out because of Mr. Dimon’s prominence as a skilled Washington operator and because of his bank’s nearly unblemished record during the financial crisis.

“JPMorgan was the one that made the strongest arguments to allow hedging, and specifically to allow this type of portfolio hedging,” said a former Treasury official who was present during the Dodd-Frank debates.

Those efforts produced “a big enough loophole that a Mack truck could drive right through it,” Senator Carl Levin, the Michigan Democrat who co-wrote the legislation that led to the Volcker Rule, said Friday after the disclosure of the JPMorgan loss.

The loophole is known as portfolio hedging, a strategy that essentially allows banks to view an investment portfolio as a whole and take actions to offset the risks of the entire portfolio. That contrasts with the traditional definition of hedging, which matches an individual security or trading position with an inversely related investment — so when one goes up, the other goes down.

Portfolio hedging “is a license to do pretty much anything,” Mr. Levin said. He and Senator Jeff Merkley, an Oregon Democrat who worked on the law with Mr. Levin, sent a letter to regulators in February, making clear that hedging on that scale was not their intention.

“There is no statutory basis to support the proposed portfolio hedging language,” they wrote, “nor is there anything in the legislative history to suggest that it should be allowed.”

While the banks lobbied furiously, they were in some ways pushing on an open door. Officials at the Treasury Department and the Federal Reserve, the main overseer of the banks, as well as the Comptroller of the Currency, also wanted a loose set of restrictions, according to people who took part in the drafting of the Volcker Rule who spoke on the condition of anonymity because no regulatory agencies would officially talk about the rule on Friday.

The Fed and the Treasury’s views prevailed in the face of opposition from both the Securities and Exchange Commission and the Commodity Futures Trading Commission, which regulate markets and companies’ reporting of their financial positions. Both commissions and the Federal Deposit Insurance Corporation, which insures bank deposits, pushed for tighter restrictions, the people said...

Read the rest here.

11 May 2012

Gold Daily and Silver Weekly Charts - Facebook Cometh, So Paper Prevails

More capping pressure on the metals today. With Open Interest holding steady and the accumulation patterns intact it seems more like short selling to hold down price. That can only last for so long, and is the stuff of V bottoms.

The Facebook IPO prices next Thursday and that is a 'big event' for the Street.

But let's see how Europe fares. Liquidity panics are painful in the short term. I do not favor any stocks for now, and maintain gold bullion positions with hedges. As always I do not touch any long term positions.

I have posted the Comex option dates below for the next few months. This is traditionally a heavy delivery period for the next two months, so let's keep an eye on how that goes. These low prices might be considered a gift for those seeking physical bullion.

As the swallows return to San Juan Capistrano, so the children, or I should say young men and women now, return from university and their far flung enterprises this evening.

And so the old man must take his early leave, and make preparations for their return, and especially the return of their hearty appetites.

Have a pleasant weekend.

May 24 Comex June gold options expiry

May 24 Comex June copper options expiry

May 26 Comex June miNY gold futures last trading day

May 29 Comex May silver futures last trading day

May 29 Comex May copper futures last trading day

May 29 Comex June E-mini copper futures last trading day

May 29 Comex June miNY gold futures last trading day

May 31 Comex June gold futures first notice day

May 31 Comex June copper futures first notice day

May 31 Nymex June palladium futures first notice day

June 26 Comex July silver options expiry

June 26 Comex July copper options expiry

June 26 Comex July silver futures last trading day

June 27 Comex June gold futures last trading day

June 27 Comex June copper futures last trading day

June 27 Comex June E-micro gold futures last trading day

June 27 Comex July E-mini copper futures last trading day

June 27 Comex July miNY silver futures last trading day

June 27 Nymex June palladium futures last trading day

June 29 Comex July silver futures first notice day

June 29 Comex July copper futures first notice day

June 29 Nymex July platinum futures first notice day

SP 500 and NDX Futures Daily Charts - The Facebook IPO Cometh

JPM dropped a bit of a bombshell last night, as the great Jamie Dimon confessed the losses at their London based CIO 'hedging operation.'

I had to chuckle today as the Street mavens attempted to direct and deflect that event, so as not to interfere with the much awaited Facebook public offering is expected to be priced next Thursday, May 17th.

I expect that the Street will rally to the support of the major indices in order to hold up demand for this fat cow of an IPO.

I imagine that it will price to expectations, or possibly just below, but obtain a decent initial performance based on nothing else than pure price manipulation and a shortage of shares for borrowing.

And then I think it will be cut in half, perhaps over a period of weeks. But it depends quite a bit on what else is happening in the macro world, particularly with regard to European debt and the next round of US quantitative easing, no matter the paper in which they choose to wrap it. Liquidity floats even dead fish.

Our son is coming home from university this evening, and a godson is coming here on a two week leave from the military, so I must make preparations for their hearty appetites. I have missed them greatly and will be very happy to see them. Children can be a worry and a heartache yes, I know that well, but also a great consolation and joy to a world weary heart.

Have a pleasant weekend.

JP Morgan Failure Shows the Incompetency of the Fed As Regulator And a Corrupted Government

|

| ...And They Repeatedly Fail to Protect the Public From It. |

"How can we expect righteousness to prevail when there is hardly anyone willing to stand up for a righteous cause?

Such a fine, sunny day, and I have to go..."

Sophie Scholl, last words

The spin machine is revving up, and the spokesmodels are gesticulating wildly, in an effort to direct and deflect this failure of governance at JPM.

See how manfully Jamie Dimon has come clean on this. And look how well the Fed's capital standards are protecting us from a failure at JPM because of this unfortunate but 'manageable' trading mistake.A craven Congress, dominated by a hard core of one-percenter bully boys, an Obama Administration intimately tied to Wall St. cronies, and the Federal Reserve, which is a private institution of financial establishment insiders making a weak attempt at self-regulation cloaked in secrecy, have failed the public once again.

Jamie and the regulators could not possibly have known (CEO defense) what was going on in their firm because the world is now so complex. They will try and work harder so don't disturb them or bad things will happen to us and it will be your fault. But this will be a buying opportunity!

Simon Johnson points out what many may miss in all this. The side effects of the continuing campaign by the banks' lobbyists to weaken reform have given us a hint of the next financial crisis to come which will be caused by a collapse in the derivatives market. And who could have seen it coming.

And I would like to make the point, and nail it to the door of the spineless media, that JPM had to admit, while the position was still open, that their 'hedge' had blown up in their faces, and that it was no hedge at all, but a thinly disguised attempt to circumvent the curbs on proprietary trading. More simply, they were preparing to flout the law and were brazenly lying about it, and their use of leverage and very risky bets in search of enormous bonuses. And they are doing the same thing on a much larger scale in other markets.

And it is no coincidence that financial fraud prosecutions under the Obama Administration are at a twenty year low, and the media and even his political opposition say almost nothing about it.

"All governments suffer a recurring problem: Power attracts pathological personalities. It is not that power corrupts but that it is magnetic to the corruptible."The credibility trap has captured our leadership. They cannot change course without admitting their failures, and to admit their failures is to weaken or even lose their grip on power. And so it's steady as she goes, onto the rocks. Better a general than a personal failure, risking other people's lives to protect your gains, because there is opportunity in a crisis as long as you still have a seat in the game.

Frank Herbert

The cheating, stealing, and lying will continue until the system finally collapses, or until the people finally wake up, take responsibility for their government, and demand meaningful reform.

JP Morgan Debacle Reveals Fatal Flaw In Federal Reserve Thinking

By Simon Johnson

May 11, 2012

Experienced Wall Street executives and traders concede, in private, that Bank of America is not well run and that Citigroup has long been a recipe for disaster. But they always insist that attempts to re-regulate Wall Street are misguided because risk-management has become more sophisticated – everyone, in this view, has become more like Jamie Dimon, head of JP Morgan Chase, with his legendary attention to detail and concern about quantifying the downside.

In the light of JP Morgan’s stunning losses on derivatives, announced yesterday but with the full scope of total potential losses still not yet clear (and not yet determined), Jamie Dimon and his company do not look like any kind of appealing role model. But the real losers in this turn of events are the Board of Governors of the Federal Reserve System and the New York Fed, whose approach to bank capital is now demonstrated to be deeply flawed.

JP Morgan claimed to have great risk management systems – and these are widely regarded as the best on Wall Street. But what does the “best on Wall Street” mean when bank executives and key employees have an incentive to make and misrepresent big bets – they are compensated based on return on equity, unadjusted for risk? Bank executives get the upside and the downside falls on everyone else – this is what it means to be “too big to fail” in modern America.

The Federal Reserve knows this, of course – it is stuffed full of smart people. Its leadership, including Chairman Ben Bernanke, Dan Tarullo (lead governor for overseeing bank capital rules), and Bill Dudley (president of the New York Fed) are all well aware that bankers want to reduce equity levels and run a more highly leveraged business (i.e., more debt relative to equity). To prevent this from occurring in an egregious manner, the Fed now runs regular “stress tests” to assess how much banks could lose – and therefore how much of a buffer they need in the form of shareholder equity.

In the spring, JP Morgan passed the latest Fed stress tests with flying colors. The Fed agreed to let JP Morgan increase its dividend and buy back shares (both of which reduce the value of shareholder equity on the books of the bank). Jamie Dimon received an official seal of approval. (Amazingly, Mr. Dimon indicated in his conference call on Thursday that the buybacks will continue; surely the Fed will step in to prevent this until the relevant losses have been capped.)

There was no hint in the stress tests that JP Morgan could be facing these kinds of potential losses. We still do not know the exact source of this disaster, but it appears to involve credit derivatives – and some reports point directly to credit default swaps (i.e., a form of insurance policy sold against losses in various kinds of debt.) Presumably there are problems with illiquid securities for which prices have fallen due to recent pressures in some markets and the general “risk-off” attitude – meaning that many investors prefer to reduce leverage and avoid high-yield/high-risk assets.

But global stress levels are not particularly high at present – certainly not compared to what they will be if the euro situation continues to spiral out of control. We are not at the end of a big global credit boom – we are still trying to recover from the last calamity. For JP Morgan to have incurred such losses at such a relatively mild part of the credit cycle is simply stunning.

The lessons from JP Morgan’s losses are simple. Such banks have become too large and complex for management to control what is going on. The breakdown in internal governance is profound. The breakdown in external corporate governance is also complete — in any other industry, when faced with large losses incurred in such a haphazard way and under his direct personal supervision, the CEO would resign. No doubt Jamie Dimon will remain in place.

And the regulators also have no idea about what is going on. Attempts to oversee these banks in a sophisticated and nuanced way are not working.

The SAFE Banking Act, re-introduced by Senator Sherrod Brown on Wednesday, exactly hits the nail on the head. The discussion he instigated at the Senate Banking Committee hearing on Wednesday can only be described as prescient. Thought leaders such as Sheila Bair, Richard Fisher, and Tom Hoenig have been right all along about “too big to fail” banks (see my piece from the NYT.com on Thursday on SAFE and the growing consensus behind it).

The Financial Services Roundtable, in contrast, is spouting nonsense – they can only feel deeply embarrassed today. Continued opposition to the Volcker Rule invites ridicule. It is immaterial whether or not this particular set of trades by JP Morgan is classified as “proprietary”; all megabanks should be presumed incapable of managing their risks appropriately.

Read the rest here.

10 May 2012

Sharkboy Hits Dock - JPM Takes 'Significant Loss' in Derivatives Book - 'Could Get Worse'

|

| How Are the Mighty Fallen |

“The enormous loss was just the latest evidence that what banks call ‘hedges’ are often risky bets.”

Senator Carl Levin

"From top to bottom of the ladder, greed is aroused without knowing where to find a comfortable foothold. Nothing can calm it, since its goal is far beyond all it can attain. Reality seems valueless by comparison with the dreams of fevered imaginations; reality is therefore abandoned."

Emile Durkheim

After the bell JPM announced that it is taking a $2 Billion loss in its London derivatives book. The news drove down US bank stocks and the SP futures dropped a quick 12 points.

A Treasury official, speaking off the record, noted, "We may be dancing on the edge of a crevasse, but we're still better than Europe. Neener neener."

Isn't this transformation of the CIO office at JPMorgan part of Jamie Dimon's strategy to skirt curbs on proprietary trading and take very large positions in OTC derivatives in order to greatly increase bank profits?

I thought we were told that these massive bets were in the CIO section because they were 'hedges against risk' for JPM's corporate portfolio exposure. You know, the same way that Blythe Masters has assured the public that their massive bets in commodities are all merely hedges?

See JPM 'London Whale' Trader Bruno Iksil Driving Derivatives Market With 'Massive Positions and Excess Capital'

Smells like the Corzine strategy at MF Global to me. And it was even being run out of London, the locus of financial frauds. What a coincidence!

Wait until their commodity derivatives book blows up. When Blythe Masters famously said that 'the rest of the market is scared shitless of us' perhaps it was true, but not for the reasons that she had imagined.

I hope this doesn't hurt all the 'civilized people' who have their money tucked away in bank shares. The disclosure earlier today from Chris Whalen about Wells Fargo's accounting practices might have made Charlie Munger soil his wee undies. Well at least he is confident that the US will once again provide bailouts at the expense of 'handouts' to the poor and middle class.

Someone has to step in and protect capitalism from the capitalists. They'll never learn on their own.

Barron's

JP Morgan Reveals Large Trading Loss; Shares Hammered

By Avi Salzman

May 10, 2012, 5:29 P.M. ET

JPMorgan Chase (JPM) fell 6.5% after-hours after saying it incurred “significant mark-to-market losses in its synthetic credit portfolio.”

CEO Jamie Dimon apologized on a conference call at 5 p.m. for “egregious mistakes” and an “unbelievably ineffective” trading strategy meant to hedge trading positions.

He said the company’s Corporate division was likely to post an $800 million after-tax loss, higher than its previous expectations for a plus or minus $200 million. JPM’s chief investment office lost $2 billion on its synthetic credit positions while recording a $1 billion gain, mostly by selling credit exposures. (which will blow up at some later date in the manner of financial pyramid schemes - Jesse)

“[I]n hindsight, the new strategy was flawed, complex, poorly reviewed, poorly executed and poorly monitored,” he said, according to an initial transcript. “The portfolio has proven to be riskier, more volatile and less effective an economic hedge than we thought.

“The strategy was badly executed, badly monitored,” he said, without going into detail about the specific trading strategy.

The company’s 10-Q , released just before the conference call, says:

“Since March 31, 2012, CIO has had significant mark-to-market losses in its synthetic credit portfolio, and this portfolio has proven to be riskier, more volatile and less effective as an economic hedge than the Firm previously believed. The losses in CIO’s synthetic credit portfolio have been partially offset by realized gains from sales, predominantly of credit-related positions, in CIO’s AFS securities portfolio.”

Analysts on the conference call were clearly perplexed by the sudden change. JP Morgan was considered to have among the cleanest balance sheets of the major banks. Dimon also noted that the loss could give fuel to critics who say that banks are still too lightly regulated.

Other major banks were also falling on the news...

Financial Times

What do you mean the vault is 'empty?'

JPMorgan loses $2bn in ‘egregious’ error

By Tom Braithwaite in New York

JPMorgan Chase announced a surprise $2bn trading loss on credit derivatives trading, which chief executive Jamie Dimon blamed on “errors, sloppiness and bad judgement” and warned “could get worse”.

The shock disclosure, made after the market closed in a regulatory filing, sent shares in the bank down by about 6 per cent and prompted renewed calls for tougher regulation.

JPMorgan said the mark-to-market losses came in the bank’s chief investment office, a unit set up to invest excess deposits, which has drawn controversy after hedge funds alleged it was taking big proprietary bets.

Proprietary trading is set to be banned in the US by the forthcoming “Volcker rule” and the losses revealed on Thursday are likely to stiffen regulators’ resolve to enforce that ban broadly.

Carl Levin, a Democratic senator who has pushed for a strict interpretation of the rule, said “the enormous loss” was “just the latest evidence that what banks call ‘hedges’ are often risky bets”. He called for “tough, effective standards... to protect taxpayers from having to cover such high-risk bets”.

“It plays in to the hands of a bunch of pundits out there,“ Mr Dimon said on a hastily convened conference call. “This trading may not violate the Volcker rule but it violates the Dimon principle.”

...Turbulent credit markets exacerbated flaws in the trading strategy, JPMorgan said. Since the company does not want to conduct a fire sale of its positions, it is stuck with the exposure for some time.

“There is going to be a lot of volatility here and it could easily get worse this quarter – or better, but could easily get worse – and the next quarter we also think we have a lot of volatility,” Mr Dimon said.

JPMorgan also restated its “value at risk”, a measure of maximum possible daily losses, of the CIO in the first quarter from $67m to $129m.

Read the rest here.

Happier Days for Jamie and Blythe with Bruno Iksil at the Wheel

Dramatic re-enactment of JPM's Pan European Derivatives Victory Tour from Zurich to London

Max Keiser Interviews Chris Whalen on the Banks, And Accounting at Wells Fargo

This is an interesting discussion. I have enormous respect for Chris Whalen, bearing in mind that he is very much a member of the banking community and this must by its very nature affect his priorities if but a little.

And of course, Max is always Max, and always interesting. When he shifts his schtick into low gear (pun intended) he is an excellent interviewer. I wonder if Comedy Central could handle his style. He burned out the BBC fairly quickly when he called for bankers to be sent to the guillotine. Hunter Thompson drives the Shark to Wall Street. Or perhaps more like Lenny Bruce, for those who remember him, the older crowd like me.

Although I think most of what he says is quite to the point, I don't necessarily agree with Chris when he complains that on one hand that the Fed has not done enough to reform the banks, but on the other hand he suggests the Fed raise rates so that the unreformed banks can make more money on their interest rate carry trades, even if it harms the real economy.

I think a strong enough reform of the banks, the real banks, would help reduce their need for outsized returns, and take them off the Fed feedbag. And Chris alludes to that glancingly later on when he talks about JPM. Max hits that point hard, but Chris just doesn't seem to get it quite yet. And Chris defers somewhat to Jamie D. but unleashes on Jon Corzine. Corzine won't be buying any rating services anytime soon.

The Fed interest rate policy is a blunt instrument, and it does definitely penalize savers. But there are other ways to deal with that than by simply raising rates overall to help subsidize the banks, given the extraordinarily weak recovery in the real economy, which at the end of the day is what public policy should be all about. And of course Chris makes no reference to the intense bank lobbying that helped to weaken Dodd-Frank and the Volcker Rule and make them more complex and less effective. I seem to recall Yves Smith taking him to task on that, and she was right.

But overall it is good. His opinions on Wells Fargo are rather blunt and could be an eye opener to some. The American banking system is still a snakepit, and it makes we grind my teeth a bit when the triumphalists on Bloomberg television compare the US 'success' in financial recovery to other nations.

Here is the original source for this excerpt titled provocatively "I Steal Therefore I Am."

Again I apologize for having to direct viewers to Russia Today to obtain this information about the US financial system, but there is a decided lack of frank discussion like this in the American media, except perhaps on Comedy Central and a few isolated outposts on PBS.

Subscribe to:

Posts (Atom)