“A nation can survive its fools, and even the ambitious. But it cannot survive treason from within. For the traitor appears not a traitor; he wears their face and their arguments, he appeals to the baseness that lies deep in the hearts of all men. He rots the soul of a nation, he works secretly and unknown in the night to undermine the pillars of the city, he infects the body politic so that it can no longer resist. A murderer is less to fear. The traitor is the plague.” Marcus Tullius Cicero

"J. P. Morgan and Andrew Mellon made their billions through inter locking directorates and outright ownership of hundreds of nationally prominent enterprises. Glass-Steagall is one crucial piece of a litany of legislation designed to place checks and balances on the concentration of financial resources. To repeal it would be tantamount to bringing back the days of the robber barons. The unbridled activities of those gifted financiers crumbled under the dynamic forces of the capital marketplace. If you take away the checks, the market forces will eventually knock the system off balance."

Mark D. Samber, End Bank Law and Robber Barons Ride Again, NY Times, March 5, 1995

"In 1999, on signing Gramm-Leach-Bliley into law, Clinton said, 'This is a day we can celebrate as an American day' and that 'the Glass-Steagall law is no longer appropriate for the economy in which we live' and 'today what we are doing is modernizing the financial services industry, tearing down these antiquated laws and granting banks significant new authority' and 'This is a very good day for the United States.'"

"There is no reason to believe either equity swaps or credit derivatives can influence the price of the underlying assets any more than conventional securities trading does."

Alan Greenspan, July 24, 1998, Testimony on the Regulation of OTC Derivatives

"But bad economics was only a symptom of the real problem: secrecy. Smart people are more likely to do stupid things when they close themselves off from outside criticism and advice."

Joseph Stiglitz, What I Learned at the World Economic Crisis, April 17, 2000

"It is no exaggeration to say that since the 1980s, much of the global financial sector has become criminalised, creating an industry culture that tolerates or even encourages systematic fraud. The behaviour that caused the mortgage bubble and financial crisis of 2008 was a natural outcome and continuation of this pattern, rather than some kind of economic accident."

Charles H. Ferguson

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.”

Upton Sinclair

"We feel that fundamentally Wall Street is sound, and that for people who can afford to pay for them outright, good stocks are cheap at these prices."

Goodbody and Company, The New York Times, October 25, 1929

The market read between the lines of the FOMC decision and in particular Chairman Powell's remarks and assumed that the Fed is in a pivot to a less hawkish stance on interest rates.

And so gold and particularly silver rallied.

Stocks went stratospheric.

The Dollar dumped back to the 106 handle.

Whether this interpretation of the Fed's intentions is valid or not remains to be seen.

Certainly eyes will be on the data,

After hours the corporate earnings reports were a very mixed bag.

Tomorrow we will be getting an advance look at 2Q GDP.

Regardless of this backward look, history suggests that we are heading into a recession.

"So we may not be that far away from the next bubble bursting, and I could imagine, if I think about policy, what we just talked about, with the end of a recovery cycle, we’ve pumped $4 trillion in this country, $30 trillion globally, into the economy with monetary policy. So that’s tapped out.

We are now using fiscal policy to overheat a late-stage recovery in order to keep the Republicans in office. We are doing nothing to bolster underlying growth with educational reform, infrastructure reform, et cetera."

"I think it’s important in the power of finance and how pervasive this is throughout the economy, this has very little to do with Republicans and Democrats. In fact, some of the key opening doors for finance happened in the Clinton administration."

Rana Foroohar is an associate editor and global business columnist for The Financial Times, and CNN’s global economic analysts. She’s the author of Makers and Takers: The Rise of Finance and the Fall of American Business.

"What is most offensive is not their lying— one can always forgive lying— lying can be a delightful thing, for it leads to truth. What is offensive is that they lie, and worship their own lying."

Fyodor Dostoevsky, Crime and Punishment

“A true opium of [worldly] people is a belief in nothingness after death— the huge solace of thinking that for our betrayals, greed, cowardice, and murders that we are not going to be judged.”

Czesław Miłosz

Stocks continued selling today. What was particularly discouraging for the bulls is that there was no afternoon rally. In fact, the selling accelerated in the last hours of trading, and the major indices went out on the lows, and on heavier volume.

One might point to the new tariffs to come on China, and fears of a trade war. Earlier this week one would look to the Fed, and talk about the rising interest rates, probably the most carefully telegraphed monetary decision in history.

Perhaps it was the latest antics of Facebook, in the general growth of the abuse of privacy of the public by government and their corporations. One might also look to the dysfunction in Washington, and the misguided policies that have been crippling the middle and lower classes to the advantage of the one percent.

Let's skip the usual bullshit exercise of identifying the reasons for this sell off for the moment shall we?

Certain financial assets, like the major stock indices, led narrowly by the FANG tech stocks and the financials, had been lifted to new heights by what certainly looked like the utter mispricing risks.

And as we have seen in the last two asset bubbles and subsequent financial crises, prices continued rising to even greater over-valuations. They were lifted on a cloud of misrepresentations and the purposeful weakening of transparency and regulation, from the purveyors of stocks and their many purveyors of the big lie designed to support the economic status quo.

As I have cautioned, when this mispricing of risk continued to expand,the 'trigger event' needed to knock the market off its blocks would decrease in required magnitude, until something incidental, or a cluster of rather minor incidents, would be enough to send prices down, and with a vengeance.

So far this latest market decline is what I would call a 'market break' and not a 'crash.' As a reminder, there was a disquieting market break in March 1929 that was quickly forgotten, until the market breaks of September, culminating in a bloody October.

The Father of Lies

It will not take much for some semi-official group to turn the markets around by buying the SP 500 futures at a key moment. There is not much fundamental stock picking in this market; it is all index ETFs and narrowing momentum.

Buying the futures to turn things around could be done by the Fed or some other NGO that is working with their compadres of the revolving door. One group wants to get rich, and the other wants to not be run out of town on a rail.

That has been a 'go to' solution since the mid-1990's. It is very possible that stocks will find a bottom, perhaps in a true selling capitulation, and then turn and run back up to perhaps a new high later this year, led by the usual suspects and their aficionados.

But if there is no financial reform, if there is no return to good governance and honesty in the major mechanisms of the financial system which, after all, is the capital allocation heart of any capitalist economy, there will once again be a crash, a staggering correction in prices, for the third time since the year 2000.

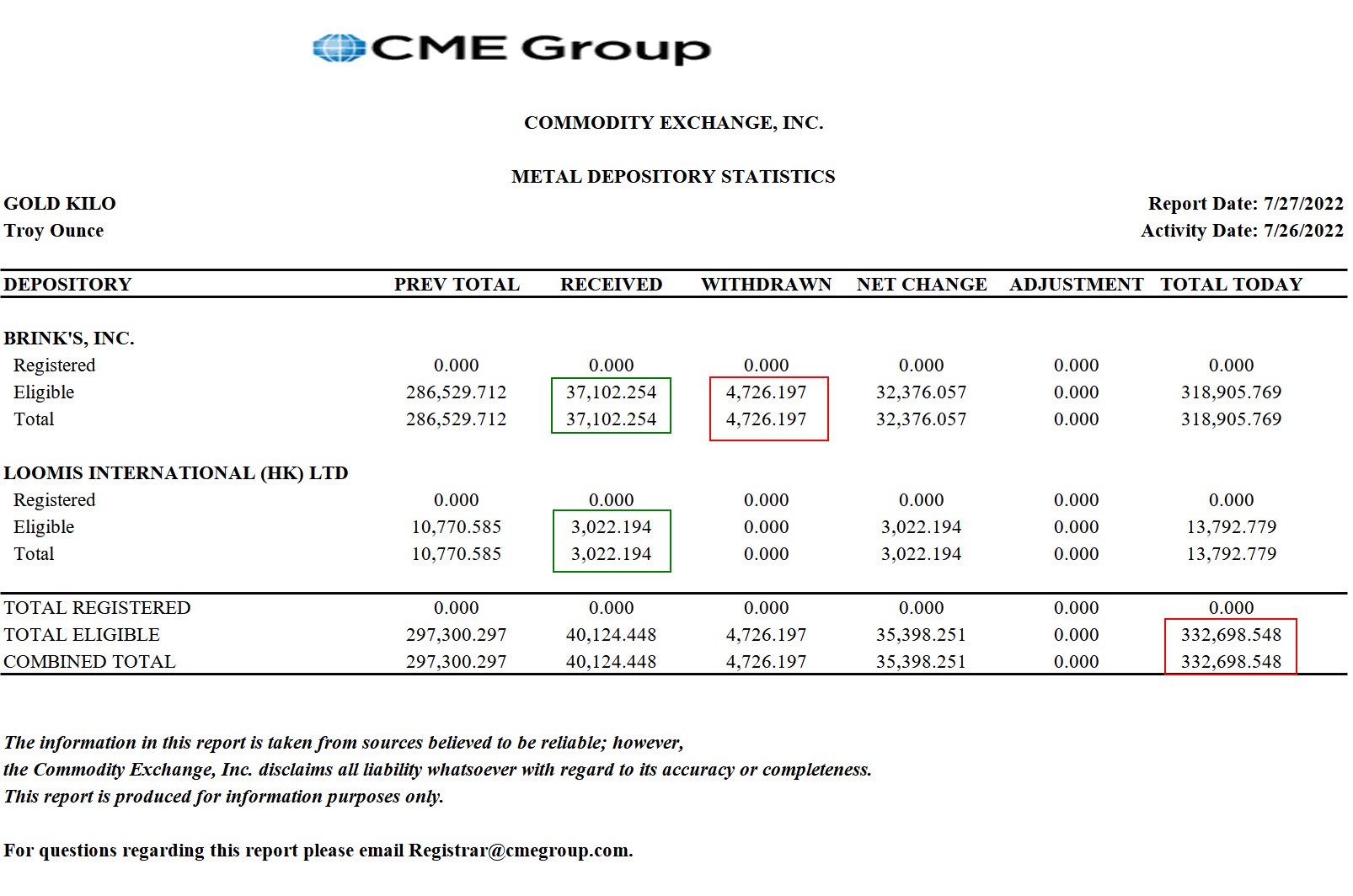

There was a very minor flight to safety today. The US Dollar managed to drift slightly higher within its recent trading range. And in the usual manner of the recent currency trading of the precious metals, gold and silver were off a bit in response.

And let us not forget that there will be an option expiration for gold and silver on Monday.

Government bonds caught a bid, which was a bit odd in this interest-raising environment needed because things are just that good in the real economy right? We certainly don't want any overheating, as in higher wages for working people.

Wall Street will be dropping another IPO into the markets tomorrow in Dropbox, unless they call it off for reason of market conditions. I suspect that they will try to stabilize the markets while Wall Street squeezes this latest creation out.

This is not going to end well. But if we get another rally, all of this gloom will be forgotten, and it will be bread and circuses and the latest scandals of the rich and frivolous all over again.

And when it really hits the wall, when the financial system is thoroughly knackered, we can always blame Trump, or Russia.

It is correct to say that money velocity does not do anything. It does not do anything in the way that the speedometer on your car does not do anything. But it is an important measurement, a ratio of the amount of money being created and it relationship to productive, organic growth in the economy.

And it is well known that money velocity peaked in 1997, and has been in a steady decline since then. It is now at lows never seen before in the US economy. It, like the implications of the long term stagnation of median household income, remains largely unremarked, and if noticed, excused away as unimportant.

Tony is an expert on financial aspects of housing, among other things, and as you know I follow what he writes closely. He knows more about these things than anyone that I know. And he says what he means and means what he says, which is a sometimes neglected principle among mainstream economists these days.

But as I have a slightly different perspective on that period of time, I would take this a step further and draw a admittedly broader, less specialized conclusion. The article does not account for the massive tech bubble, which at the time was covered by the fig leaf of a 'new era internet economy,' giving it the name of the dot-com bubble, with which I happened to be intimately familiar.

Who can forget Chairman Greenspan's irrational exuberance speech which shanked the stock market in December of 1996.

Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past.

But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?

Alan Greenspan, The Challenge of Central Banking in a Democratic Society, 1996-12-05

As it turned out, Chairman Greenspan was blinded by ideology, as he himself admits years afterwards, never seeing a bubble that he didn't like. But his successors have followed the same sorry route of feeding the financiers to the detriment of the broader economy.

The problem was not the mortgage credit bubble per se, but rather the policy bias towards managing and regulating the economy itself, with an aggressive expansion of the money supply under Alan Greenspan (remember the Y2K scare) and Treasury Secretary Robert Rubin, along with bubbles in the usual suspects, in this case the financialization of housing and the tremendous bubble in the equity markets.

Do you recall the Time Magazine cover from 15 February 1999? The Committee To Save the World?

And how can we forget the Rubin doctrine of propping up the financial markets using the SP 500 futures before the fact, which he thought was cheaper than cleaning up the mess of a market crash after the fact. Remember The Working Group, aka The Plunge Protection Team, housed within the Exchange Stabilization Act, that came out of the scarring experience of the Crash of 1987, which itself was a precursor to the woes created by weakly regulated, artificially exotic financial instruments and mispriced risks?

A crisis is a very effective mechanism for enabling the abuse of power.

And let us not forget the overturning of Glass-Steagall in a decades long campaign richly underwritten by the Wall Street Banks, and the infamous Gramm-Leach-Bliley Financial Services Modernization Act of 1999.

In 1999, on signing Gramm-Leach-Bliley into law, Clinton said, 'This is a day we can celebrate as an American day' and that 'the Glass-Steagall law is no longer appropriate for the economy in which we live' and 'today what we are doing is modernizing the financial services industry, tearing down these antiquated laws and granting banks significant new authority' and 'This is a very good day for the United States.'

Columbia Journalism Review, Bill Clinton on Deregulation

One might say by way of analogy that Reagan made the nest, and Clinton laid the egg. But both Bush II and Obama have nurtured this chimera economy along. And we can have every expectation that the political establishment will continue to do so in the next presidency.

"It comes as a surprise to many people that, despite the fiasco at Citigroup and his role in causing the subprime mess, Rubin remains inside the circle at the White House. Nearly two decades after first migrating to Washington, he apparently is still calling the shots of U.S. financial and economic policy with the full support of President Barrack Obama.

Working through his favorite marionettes, Treasury Secretary Tim Geithner and Economic Policy Czar Larry Summers, most recently Rubin managed the defense of Wall Street following the great crisis. No matter what Secretary Geithner says or when he says it in public, you can be sure that those utterances have the full knowledge and approval of his handler Larry Summers and their common political owner and sponsor, Robert Rubin.

The causes for this are debatable and many, and I have considered it here many times as the credibility trap,

What we have now, an economy based on artificial support market resulting in a series of asset bubbles and crashes, with a growing inequality in income distribution. This is the natural outcome when a policy body decides to manage or 'stimulate' the economy by shoving freshly minted dollars top down through a weakly regulated, increasingly corrupt financial system whose outsized and largely unproductive profits act like a private tax on the real economy. It enriches a few, and enervates the productive working class.

This is why I have said that until there is financial and political reform, there will be no sustainable recovery. And the longer this continues, the more that the organic productivity of the economy will decline. And the more socially explosive the situation may become.

"Over the last thirty years, the United States has been taken over by an amoral financial oligarchy, and the American dream of opportunity, education, and upward mobility is now largely confined to the top few percent of the population. Federal policy is increasingly dictated by the wealthy, by the financial sector, and by powerful (though sometimes badly mismanaged) industries such as telecommunications, health care, automobiles, and energy. These policies are implemented and praised by these groups’ willing servants, namely the increasingly bought-and-paid-for leadership of America’s political parties, academia, and lobbying industry.

If allowed to continue, this process will turn the United States into a declining, unfair society with an impoverished, angry, uneducated population under the control of a small, ultrawealthy elite. Such a society would be not only immoral but also eventually unstable, dangerously ripe for religious and political extremism.

Charles Ferguson, Predator Nation

I have little expectation now that reform will come from within. The power of the status quo is too great, and too prone to rewarding those who serve it, and silencing and impeding those who oppose it by progressive reform.

"'After dinner, 'Larry [Summers] leaned back in his chair and offered me some advice,' Ms. Warren writes. 'I had a choice. I could be an insider or I could be an outsider. Outsiders can say whatever they want. But people on the inside don’t listen to them. Insiders, however, get lots of access and a chance to push their ideas. People — powerful people — listen to what they have to say. But insiders also understand one unbreakable rule: They don’t criticize other insiders.'

I had been warned."

Elizabeth Warren, A Fighting Chance

How can we have missed this element of self-serving preservation of the status quo so broadly on display in the run up to our recent presidential election?

'Stimulus' in itself is no panacea. It must be productive and targeted towards increasing aggregate demand within a healthy economy which distributes the rewards for productive efforts broadly amongst its participants.

Whether it is affordable housing, infrastructure project such as roads, bridges, and modern power grids, the general improvement of the environment, or the expansion and improvement of those basic elements of a culture than lend value to peoples' lives, any project which can be considered stimulative can and will be turned into an unproductive boondoggle by a corrupt financial and political system. They contaminate everything that they touch.

And so I continue to make the observation that significant financial and political reform are the sine qua non for a genuine economic recovery.

Doing more of the same may make no sense, may even seem neurotic. And if it seems to defy common sense, that is because it does.

But it has one very special thing going for it. It has been and still is richly rewarding to a small group of very powerful people, something which we have seen repeatedly throughout the developing world, and even in the gilded, boom and bust eras of this country before.

"The crash has laid bare many unpleasant truths about the United States...

Recovery will fail unless we break the financial oligarchy that is blocking essential reform."

Confounded Interest Dying Money Velocity Began in 1995 with Massive Mortgage Credit Expansion

M2 Money Velocity (GDP/M2 Money Stock) peaked back in Q3 of 1997. And it has mostly gone down hill from there. As of Q2 2016, M2 Money Velocity is at the lowest point in history.

Why?

One explanation for the decline in velocity is the decline in labor force participation since early 2000 when labor force participation peaked. Fewer people participating in the labor force (as a percentage of the population) makes it more and more difficult to maintain velocity since GDP is lower despite the expansion of money.

Why is labor force participation declining? First, our population is aging and more and more people are retiring. Second, more and more students decided to attend and/or stay in school given the lousy jobs market. Third, some people have just given up trying to find a job and would prefer to rely on the state for food, housing, healthcare, etc.

A closer look reveals some bad AND good news. Labor force participation for ages 25-54 has been declining since 2007 (but showing some improvement in 2016). On the other hand, LFP for ages 65 and above (many of whom were pushed back into the labor force as a result of the financial crisis and housing bubble burst) has been growing steadily since 2008.

Actually, the economic world turned before labor force participation peaked in early 2000 and M2 Money Velocity peaked in 1997.A key economic indicator, core personal consumption expenditures YoY, was above 4% in the early 1990s only to fall to around 2% around 1995 prompting the Clinton Administration to enact policies leading to a dramatic increase in mortgage credit (creating a credit bubble) as a stimulative measure. This was the Clinton National Homeownership Strategy: Partners in the American “Dream.” nhsdream2 That turned into a nightmare for millions of American families.

1995 was the beginning of the incredible housing credit bubble that catastrophically exploded in 2008.

Core personal consumption expenditures (cPCE) YoY sagged after 1989 and hit 2% by mid 1990s and has struggled to reach 2% on a consistent basis ever since. As a result, GDP has been compromised and the massive expansion of mortgage credit helped created a massive house price bubble which burst … and things have never been the same since.

And with the fall of the House of Usher cards, mortgage equity withdrawal has fallen as well (putting a damper on personal consumption expenditures.

Remember, housing is a consumption good (to serve as shelter), not a productive asset like a factory. Trying to create economic growth through housing is a poor choice. So much so that The Federal Reserve is left blowing asset bubbles instead of stimulating actual economic growth.

It is the same players that we saw enabling reckless behaviour in 1998: Citigroup, the Fed, and the Clinton-led Wall Street Democrats.

And here we are again, almost eighteen years later, watching the same short term, selfish behaviour by the big money banks putting the entire economy of productive individuals at risk again.

"There’s something big and scary going on behind the scenes but, as usual, the public isn’t reading about it on the front pages of the newspapers...

Dodd-Frank was supposed to push the derivatives out of the commercial banks which hold the insured deposits to prevent another taxpayer bailout, the so-called “push out” rule. But in December of 2014, Citigroup was able to sneak legislation into the must-pass spending bill to keep the government running that overturned the push-out rule...

Using its insured bank’s balance sheet as ballast, Citigroup’s bank holding company now ranks as the largest holder of all derivatives in the U.S. According to the Comptroller of the Currency, the very bank that blew itself up in 2008 and received the largest taxpayer bailout in history, now holds $55 trillion in notional amount of derivatives.

But far more alarming is the type of derivatives Citigroup appears hell bent on gaining market share in trading. Last week we reported that Citigroup is plowing into credit default swaps, the very derivatives that blew up the big insurance company, AIG, in 2008 and forced a government bailout of AIG to the tune of $185 billion...

On March 8 of this year [2016], the Office of Financial Research, which was created under the Dodd-Frank legislation to monitor the buildup of systemic financial risks, released a study on Credit Default Swaps. Its findings were deeply troubling...”

"The crash has laid bare many unpleasant truths about the United States. One of the most alarming, says a former chief economist of the International Monetary Fund, is that the finance industry has effectively captured our government—a state of affairs that more typically describes emerging markets, and is at the center of many emerging-market crises.

If the IMF’s staff could speak freely about the U.S., it would tell us what it tells all countries in this situation: recovery will fail unless we break the financial oligarchy that is blocking essential reform. And if we are to prevent a true depression, we’re running out of time."

“A true opium of the people is a belief in nothingness after death - the huge solace of thinking that for our betrayals, greed, cowardice, and even murders that we are not going to be judged.”

Czesław Miłosz

As economist Simon Johnson put it so aptly, there was a 'financial coup d'etat' in the States. It was the result of a longer term and well-funded effort as documented by PBS Frontline and others.

People forget all too quickly what has happened, even things that happened less than twenty years ago. Perhaps it is easily forgotten because there are so few counterexamples of honesty and decency these days in government and business to hold up in comparison. The UK and Canada are following in lockstep, as well as the central government for Europe in Brussels.

The Clintons, along with a large group of Republican Congressmen and compliant Democrats, put a 'for sale' sign not only on the Lincoln bedroom as you may recall, but on the rest of the White House and the Capitol, and indeed, the well being of the people of the United States.

They certainly did not do it alone, as it was a bipartisan effort to overturn the protections established in the darker days of the Great Depression. But the money was good, and it was there for the taking, and with it the enormous power to threaten or reward those around them.

And it became the thing to do in Washington and New York, to partner up with big money to take the public for a wild ride, as we have not seen since the beginning of the last century. Once again capitalism was unfettered, and became the rawest, the worst kind of short sighted and self-dealing 'capitalism' that is more corrosive looting than productive asset allocating. And so the New York - Washington metroplex enthusiastically engaged in a program of fabulous gains for themselves, and longer term pain for the country.

I do not have to read Robert Scheer's account to understand it; I saw this happening with my own eyes, almost in slow motion, as one might watch the events leading up to a train wreck. The actions of the participants were deliberate, and focused solely on amassing enormous fortunes for themselves and their friends, and damn the people and the consequences.

What the Clintons did was not to invent soft graft of political contributions and gratuities, sinecure positions after public office, and ridiculously generous payment for speeches and appearances. No, what they did was take what had been reviled as the worst of politics in craven service to big corporate interests, which had been largely but not exclusively the hallmark of their political opponents who were well established as servants to the corporate interests, and make it not only acceptable for establishment liberals, but downright fashionable.

Why would the Clintons, that wonderfully privileged and intelligent couple, do such a coarse and craven thing? One might think of about $130 million reasons offhand. Is anything just that simple? And what would you do if you were offered $130 million in easy money for you and your family to make a few key decisions, to look the other way at times, while having no fear of punishment, with all your many sins forgotten, excused, and ignored by a compliant press?

Oh yes, you are an angel and would of course say no, even if the corruption was unrolled slowly, one step at a time. But what do you think that the fellow next to you would do? The ones who cut people off in traffic, makes the rules for themselves, wishing to have their own way, to have power and a place at the highest table?

Is this a system likely to be honest, just, and sustainable? Is it designed for fairness and rewarding the best and most productive behaviour?

And like the utopian efficient market hypothesis, we are expected to believe that the powerful men of Big Money are just men of civic virtue who will give millions upon millions of dollars to politicians and expect nothing but fairness and objectivity in return, even if it is to their own disadvantage as required by justice.

No wonder so many politicians have become little more than marketing projects for Big Money, like brands of toothpaste and soft drinks. Pick any flavor that you wish, but despite the appearances of difference, they are all owned by just four or five big corporate interests, as is the mainstream media. Which by the way was enabled by the Clintons overturning the Fairness Doctrine.

A number of the old hands of politics see where this is heading, and have already taken the money and run, some to hide in their studies, to try and create a new legacy for themselves, and others to move to K Street as lobbyists and get filthier rich while it lasts.

But the problem still remains, Once thoroughly corrupted, a system finds it hard to correct itself, especially if the consequences for big rewards are more of an inconvenience than punishment, if there are any serious drawbacks at all.

The American people seem to be attempting to rouse themselves, to use their right of suffrage to bring about the change, the necessary reform, that has eluded them for quite some time. Let us hope that this effort will not be squashed in the manner of other protests, such as Occupy Wall Street, have been through almost ruthless and coordinated nationwide public relations campaigns and even violence from the government and the media.

The ‘Clinton Bubble’: How Clinton Democrats Fostered the 2008 Economic Crisis

By Robert Scheer

Since the collapse happened on the watch of President George W. Bush at the end of two full terms in office, many in the Democratic Party were only too eager to blame his administration. Yet while Bush did nothing to remedy the problem, and his response was to simply reward the culprits, the roots of this disaster go back much further, to the free-market propaganda of the Reagan years and, most damagingly, to the bipartisan deregulation of the banking industry undertaken with the full support of “liberal” President Clinton. Yes, Clinton. And if this debacle needs a name, it should most properly be called “the Clinton bubble,” as difficult as it may be to accept for those of us who voted for him.

Clinton, being a smart person and an astute politician, did not use old ideological arguments to do away with New Deal restrictions on the banking system, which had been in place ever since the Great Depression threatened the survival of capitalism. His were the words of technocrats, arguing that modern technology, globalization, and the increased sophistication of traders meant the old concerns and restrictions were outdated. By “modernizing” the economy, so the promise went, we would free powerful creative energies and create new wealth for a broad spectrum of Americans—not to mention boosting the Democratic Party enormously, both politically and financially.

And it worked: Traditional banks freed by the dissolution of New Deal regulations became much more aggressive in investing deposits, snapping up financial services companies in a binge of acquisitions. These giant conglomerates then bet long on a broad and limitless expansion of the economy, making credit easy and driving up the stock and real estate markets to unseen heights. Increasingly complicated yet wildly profitable securities—especially so-called over-the-counter derivatives (OTC), which, as their name suggests, are financial instruments derived from other assets or products—proved irresistible to global investors, even though few really understood what they were buying. Those transactions in suspect derivatives were negotiated in markets that had been freed from the obligations of government regulation and would grow in the year 2009 to more than $600 trillion...

Clinton betrayed the wisdom of Franklin Delano Roosevelt’s New Deal reforms that capitalism needed to be saved from its own excess in order to survive, that the free market would remain free only if it was properly regulated in the public interest. The great and terrible irony of capitalism is that if left unfettered, it inexorably engineers its own demise, through either revolution or economic collapse. The guardians of capitalism’s survival are thus not the self-proclaimed free-marketers, who, in defiance of the pragmatic Adam Smith himself, want to chop away at all government restraints on corporate actions, but rather liberals, at least those in the mode of FDR, who seek to harness its awesome power while keeping its workings palatable to a civilized and progressive society.

Government regulation of the market economy arose during the New Deal out of a desire to save capitalism rather than destroy it. Whether it was child labor in dark coal mines, the exploitation of racially segregated human beings to pick cotton, or the unfathomable devastation of the Great Depression, the brutal creativity of the pure profit motive has always posed a stark challenge to our belief that we are moral creatures. The modern bureaucratic governments of the developed world were built, unconsciously, as a bulwark, something big enough to occasionally stand up to the power of uncontrolled market forces...

Read the entire article with a link to the preceding excerpt from the book here.

In December 1996, with the support of Chairman Alan Greenspan, the Federal Reserve Board issues a precedent-shattering decision permitting bank holding companies to own investment bank affiliates with up to 25 percent of their business in securities underwriting (up from 10 percent).

This expansion of the loophole created by the Fed's 1987 reinterpretation of Section 20 of Glass-Steagall effectively renders Glass-Steagall obsolete. Virtually any bank holding company wanting to engage in securities business would be able to stay under the 25 percent limit on revenue. However, the law remains on the books, and along with the Bank Holding Company Act, does impose other restrictions on banks, such as prohibiting them from owning insurance-underwriting companies.

In August 1997, the Fed eliminates many restrictions imposed on "Section 20 subsidiaries" by the 1987 and 1989 orders. The Board states that the risks of underwriting had proven to be "manageable," and says banks would have the right to acquire securities firms outright...

As the push for new legislation heats up, lobbyists quip that raising the issue of financial modernization really signals the start of a fresh round of political fund-raising. Indeed, in the 1997-98 election cycle, the finance, insurance, and real estate industries (known as the FIRE sector), spends more than $200 million on lobbying and makes more than $150 million in political donations. Campaign contributions are targeted to members of Congressional banking committees and other committees with direct jurisdiction over financial services legislation.

PBS Frontline: The Long Demise of Glass-Steagall

"It is difficult to get a man to understand something, when his salary depends upon his not understanding it."

Upton Sinclair

The Glass-Steagall Law was enacted as a key reform in 1933, the depths of the Great Depression, in the overall effort to prevent the corruptions and abuses of the 1920's from enabling such a dire result again.

And together with other safeguards, such as antitrust laws and prosecutions for fraud, it worked.

It worked, that is, until a long, and extremely well-funded effort by a few Wall Street Bankers, and strongly enabled and supported by the Federal Reserve, overturned this law piece by piece sixty years later in the 1990's.

It is almost amazing to watch the new American ruling class, and those who bask and benefit in their power, continue to spin fairy tales about what went wrong, what caused it, and what we need to do about it.

The high leverage and inherently dangerous asset concentration in the financial sector enabled by the Clinton-Bush tag team has taken down the American economy, and is keeping it down in a 'new normal' of stagnation by corruption.

This situation recently caused ex-President Jimmy Carter to observe that the US is now 'just an oligarchy, with unlimited political bribery being the essence of getting the nominations for president or to elect the president. And the same thing applies to governors and U.S. senators and congress members.'

In our despair, we turn to-- Bush or Clinton. It looks less like an election that offers an honest examination of the issues, and more like a power struggle between competing oligarchies in a banana republic, with inflammatory issues, paid demonstrations, and bought off analysis designed to distract and diffuse any serious attempts at change.

And always, behind the scenes, are the oligarchs, Wall Street, and the Fed.

The corrupting power of big money on politics, the media, and public discourse is at the root of our problems.

Is there a mainstream economist anywhere who has the moral fiber to stand up to the Fed and and their grotesque series of policy errors to tell the emperor that they are naked? Or to tell the scions of Wall Street that they are enriching themselves but strangling the real economy? Is there a politician who will refuse to be bought off that has not already been made obscenely rich by a corrupt and rotten system?

How quickly the sycophants to the power of place and money fall all over themselves to support the sources of our misery.

Greed is not good. Greed kills.

New York Times Pushes False Narrative on the Wall Street Crash of 2008

By Pam Martens and Russ Martens: August 3, 2015

William D. Cohan has joined Paul Krugman and Andrew Ross Sorkin at the New York Times in pushing the patently false narrative that the repeal of the Glass-Steagall Act in 1999 had next to nothing to do with the epic Wall Street collapse of 2008 and the greatest economic calamity since the Great Depression. (See related articles on Krugman and Sorkin below.)

The New York Times has already admitted on its editorial page that it was dead wrong to have pushed for the repeal of Glass-Steagall but now it’s dirtying its hands again by publishing all of these false narratives about what actually happened.

In a July 30 column, Cohan ridicules Senators Elizabeth Warren and John McCain over their introduction of legislation to restore the Glass-Steagall Act to separate insured deposit banks from their gambling casino cousins, Wall Street investment banks. The Senators are being joined in their call to restore Glass-Steagall by a growing number of Presidential aspirants, including Senator Bernie Sanders and former Governor of Maryland, Martin O’Malley, both running as Democrats.

Hillary Clinton, another Democratic presidential hopeful whose husband, Bill Clinton, signed the bill during his presidency that repealed Glass-Steagall, does not see the need to restore Glass-Steagall...

Hillary Clinton and her husband Bill are charter founders of the Wall St Wing of the Democratic Party. They removed one of the great counterbalances to the corporatists, and have organized political corruption into a cottage industry like Lansky and Luciano organized crime into a business.

The problem is that neither most Republicans nor many Democrats make any bones about serving Big Money first anymore. It is understood that this is how things are. Soft corruption and the revolving door is the fashion.

Mitch McConnell's new chief is a former lobbyist for Koch, for example. And the Republican presidential field is devoted to Big Money while confounding their constituents with emotional sideshows and manipulative pandering to their worst impulses and scapegoating.

Reich's ideas of reinstating Glass Steagall and a nominal Financial Transactions tax have potential. It was a mistake to repeal Glass-Steagall in the first place. I wonder who presided over that? Oh yes, Bill and Hill. And NAFTA. Everything had a price tag including the Lincoln bedroom and Presidential pardons. Very entrepreneurial.

The emphasis on the Transaction Tax should be very 'nominal' and without exemptions on professionals and institutions and 'market makers' so that the HFT crowd and raw speculation from the Banks' trading desks are the targets, and not the average investor.

I also think the Fed itself, in particular the NY Fed, should be banned from making trades in anything but the official and quasi-official bond markets. And all their public markets activity should be transparent with no more than a quarter lag.

The Congress and their staffers cannot be exempt from 'insider trading' and selling information for favors to the funds and trading desks. I mean, come on. Management of companies and the media get plenty of access to insider information as well, and they are not above the law because 'it is too hard' not to use it.

Given the regulatory capture we have today I am not optimistic about reform until there is another crisis. There are only a handful of genuine reformers, but many flavors of opportunists in sheep's clothing.

So Robert, how can you be so gung ho for reform, but so unqualifiedly endorsing the unreformed Hillary Clinton?

Why don't more Beltway and media progressives and liberals come out for Liz Warren or Bernie Sanders? Because they want reform, but cannot offer their supporters the biggest Washington payoff, which is money and power, which are the mother's milk of the politically corrupt.

Here is a reprint of a warning that was published in the NY Times in 1995 about Robert Rubin's and Alan Greenspan's misguided attempts to overturn Glass-Steagall.

Any reasonably informed student of economic history ought to have understood this argument.

There was a well-funded, decade long campaign led by the Banks to overturn Glass-Steagall. A lot of propaganda was written, and lot of political connections were made, and a lot of money was spent.

Too many were willfully blind. Some through their devotion to utopian ideology. Others through devotion to their careers. And even more just kept their heads down and hid their noses in their books and reams of irrelevant data.

And for the most part they still are, with many caught in a credibility trap.

NY Times End Bank Law and Robber Barons Ride Again

Sunday, March 5, 1995

To the Editor:

Re "For Rogue Traders, Yet Another Victim" (Business Day, Feb. 28) and your same-day article on Treasury Secretary Robert E. Rubin's proposal to eliminate the legal barriers that have separated the nation's commercial banks, securities firms and insurance companies for decades: The American Bankers Association, Senator Alfonse M. D'Amato, Representative Jim Leach and Treasury Secretary Rubin are gravely misguided in their quest to repeal the Glass-Steagall Act.

Their contention that insurance companies, commercial banks and securities firms should be freed from legislative obstructions is predicated on fallacious, historically inaccurate statements. If the Baring Brothers failure does not give them pause, a history lesson is our only hope before the Administration and bank lobby iron out their differences and set the economy back 90 years.

The argument that American financial intermediaries will become "more efficient and more internationally competitive" is false. The American financial system is the most stable, most profitable and most dynamic in the world.

The notion that Glass-Steagall prevents American financial intermediaries from fulfilling their utmost potential in a global marketplace reflects inadequate understanding of the events that precipitated the act and the similarities between today's financial marketplace and the market nearly a century ago.

Although Glass-Steagall was enacted during the Great Depression, it was put in place because the Aldrich-Vreeland Act of 1908, the blue-sky laws following 1910 and the Federal Reserve System of 1913 failed to keep the concentration of financial power in check.The investment climate that ultimately led to Glass-Steagall was one filled with emerging markets, interlocking control of productive resources and widespread bank ownership of securities.

Ever since railroad securities began driving secondary capital markets in the late 1860's, "emerging markets" have existed for investors looking for high-yield opportunities, and banks have been primary agents in industrial development. In the 19th century, emerging markets were scattered throughout the United States, and capital flowed into them from New York, Boston, Philadelphia and London. In the same way, capital flows from the United States, Japan and England to Latin America and the Pacific rim -- today we just have more terms to define the market mechanisms.

The economy and financial markets were even more interconnected in the 19th century than now. Commercial and investment banks could accept deposits, issue currency, underwrite securities and own industrial enterprises. With Glass-Steagall lifted, we will chart a course returning us to that environment.

J. P. Morgan and Andrew Mellon made their billions through inter locking directorates and outright ownership of hundreds of nationally prominent enterprises. Glass-Steagall is one crucial piece of a litany of legislation designed to place checks and balances on the concentration of financial resources. To repeal it would be tantamount to bringing back the days of the robber barons.

The unbridled activities of those gifted financiers crumbled under the dynamic forces of the capital marketplace. If you take away the checks, the market forces will eventually knock the system off balance.

MARK D. SAMBER

Stamford, Conn.

Feb. 28, 1995

The writer is a management consultant specializing in business history.

This is a walk through the twentieth century, and how the United States became, by design, a combination military, industrial, and financial global superpower. And how the US dollar hegemony was created over a number of political administrations by groups of well connected, powerful families and friends.

It may seem a bit long, but she opens it for questions about the 48 minute mark, so it really is not. Nomi speaks briskly with many fact laden vignettes and scenarios that help to explain how the current system has evolved.

The facts she brings out about the 50's onwards were sometimes new to me, and absolutely fascinating. About minute 40 she shows the culmination of this historical process with the Clinton Whitehouse, and begins to describe where we are today, and how it appears that the problem will be insoluble without some major events taking place to change this alliance in power between the financial and the political.

The talk served to solidify some of my own thinking, and removed some of the shadows of doubt that I have had about where things are going and why.

She does is not able to delve into the international ties between the global central Banks, particularly between London and New York. She instead concentrates on what she might call 'the Big Six' of American Banks, which is a large enough subject itself.

I strongly recommend that you listen to it if you are at all interested in this subject.

Or if you have the time to invest, you may wish to read her book which also sounds very interesting. I have not done so yet, and I am not sure when I could get to it.

But this video is a very good start, and will probably make you much better informed than 90 percent of the people out there. Whether that is a good thing or not is another matter.

Let us pray for those whose hearts have grown cold, and become hardened against His grace by greed, fear, and the seductive illusions of pride.

We ask to receive the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness—so that we may obtain abundant life, and the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.