"Our government is the potent, the omnipresent teacher. For good or for ill, it teaches the whole people by its example. Crime is contagious. If the government becomes a lawbreaker, it breeds contempt for law; it invites every man to become a law unto himself; it invites anarchy."

Louis Brandeis, Olmstead v. United States, 1928

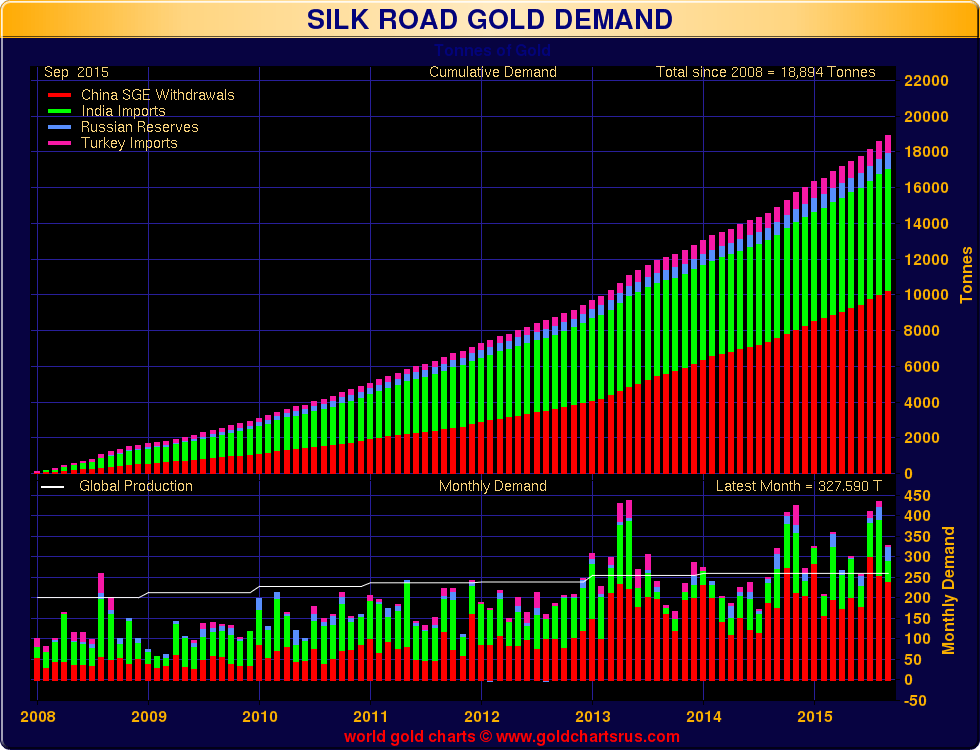

As you may recall the 'Silk Road' countries are China, India, Russia, and Turkey.

A recent article noted that flagging clearing volume for gold in London indicates a 'lack of interest' in the precious metals.

But does it really?

I think that anything like this must be viewed in the context of the global markets.

As has been shown here earlier, the 'float' of freely available, unencumbered physical gold has been declining in London and in New York, while at the same time volumes and delivery of physical bullion in Asia has been increasing.

So, is it demand for gold in decline, or is the real trading action in physical bullion moving from London and New York to the increasingly robust metals markets in Asia?

Gold is moving from West to East. And so is the locus of physical trading in these metals.

This is the other interpretation of the same facts within a broader context.

While much of the conversation regarding gold and silver centers on the Comex, the London Bullion Market Association which has a 200+ year history is lesser known amongst American readers. It has a significant role in the global physical bullion markets.

There are many more banking member of the LBMA, but they do not provide market making functions at this time.

This is from the LBMA website.

Of the fifteen LBMA Market Makers, five are full Market Makers and nine Market Makers. The five Full Market Makers quoting prices in all three products are:

Barclays Bank Plc

Goldman Sachs International

HSBC Bank USA NA *

JP Morgan Chase Bank *

UBS AG

*Also provide vaulting operations for physical bullion in London

The ten LBMA Market Makers who provide two way pricing in either one or two products are:

Citibank N A (S)

Credit Suisse (S,O)

Deutsche Bank AG (S,O)

Mitsui & Co Precious Metals (S)

Morgan Stanley & Co International Plc (S,O)

Societe Generale (S)

Standard Chartered Bank (S, O)

Bank of Nova Scotia -ScotiaMocatta (S, F)

Toronto-Dominion Bank (F)

BNP Paribas SA (F)

(S=Spot, O=Options, F=Forwards)

Definitions of Spot, Forward and Options

Spot (S). The current price in the physical market for immediate delivery of gold. This is normally taken to mean loco London delivery two working days after the date of the deal.

Forward (F). A transaction in which two parties agree to the purchase and sale of gold at a future date, commonly 1, 3, 6 and 12 months but also for longer dated tenors or dates into the future (see table above). Forward contracts are an important part of many swap arrangements.

Options (O). This gives the holder the right, but not the obligation, to buy or sell gold at a pre-determined price by an agreed date, for which he pays a premium (or a cost). The premium is the amount of compensation the seller receives from the buyer. The right to buy is commonly referred to as a call option and the right to sell as a put option.

Also from the LBMA website:

Loco London

The term Loco London refers to gold and silver bullion that is physically held in London. Only LBMA Good Delivery bars are acceptable for trading in the London market. The Loco London concept has evolved within the market. In the second half of the 19th century, gold from Californian, South African and Australian mines was sent to be refined and sold in London.

With this business as a base, and in tandem with the increasing acceptance of the London Good Delivery List, clients from all over the world opened bullion accounts with individual London bullion dealing houses. It soon become evident that these Loco London accounts, which were used to settle transactions between bullion dealer and client, also could be used to settle transactions with other parties, by transfers of bullion in London. Today all third party transfers, on behalf of London market clients, are effected through the London bullion clearing system. Each segment of the market is described below.

Note: In this case 'loco' may derive from the Latin word 'locus' meaning to put in the place or location. It is not an acronym that I know of, and is ordinarily not capitalized in LBMA documents. It does not imply that the London gold trade is 'loco' in the modern sense, although it is understandable why some should think so. I suspect that the loco London rule was intended to rule out gold held in vaults outside of the general vicinity of London and especially overseas. Remember that this is a very old organization with a long history. Shaken by claims of fraud and price manipulation, it seems to be in decline now, becoming a price leveraging paper market like New York, with the physical precious metals markets moving more to Asia.

I like Dean Baker quite well, and often link to his columns. On most things we are pretty much on the same page.

And to his credit he was one of the few 'mainstream' economists to actually see the housing bubble developing, and call it out. Some may claim to have done so, and can even cite a sentence or two where they may have mentioned it, like Paul Krugman for example. But very few spoke about doing something about it while it was in progress. The Fed was aware according to their own minutes, and ignored it.

The difficulty we have in the economics profession, I fear, is a great deal of herd instinct and concern about what others may say. And when the Fed runs their policy pennants up the flagpole, only someone truly secure in their thinking, or forsworn to some strong ideological interpretation of reality or bias if we are truly honest, dare not salute it.

Am I such a person? Do I actually see a fragile financial system that is still corrupt and highly levered, grossly mispricing risks? Or am I just seeing things the way in which I wish to see them?

That difficulty arises because economics is no science. It involves judgement and principles, and weighs the facts far too heavily based upon 'reputation' and 'status.' And of course I have none of those and wish none.

But it makes the point which I have made over and again, that all of the economic models are faulty and merely a caricature of reality. And therefore policy ought not to be dictated by models, but by policy objectives and a strong bias to results, rather than the dictates of process or methods. In this FDR had it exactly right. If we find something does not stimulate the broader economy or effect the desired policy objective, like tax cuts for the rich, using that approach over and over again is certainly not going to be effective.

Economics are a form of social and political science. And with the political and social process corrupted by big money, what can we expect from would be 'philosopher kings.'

The housing bubble was no 'cause' of the latest financial crisis. More properly it was the tinder and the trigger event. The S&L crisis was just as great, if not greater. Why then did it not bring the global financial system to its knees?

The interconnectedness of the global system with its massive and underregulated TBTF Banks, the widespread and often fraudulent mispricing of risk, all make cause for a financial system to be 'fragile.' In this thinking Nassim Taleb is far ahead of the common economic thought as a real 'systems thinker.' The Fed is not a systemic thinking organization because they are owned by the financial status quo, and real systemic reform rarely comes from within.

I see the same fragility which existed from 1999 to 2008 still in the system, only grown larger, global, and more profoundly influencing the political processes.

The only question is what 'trigger event' might set it spinning, and how great of a magnitude will it have to be in order to do so. The more fragile the system, the less that is required to knock it off its underpinnings.

And a crisis is not a binary, singular event. There is the 'trigger' and the dawning perception of risks, and the initial responses of the political, social, and regulatory powers to consider.

There is no point in debating this, because the regulators and powerful groups like the Fed are caught in a credibility trap, which prevents them from seeing things as they are, and saying so.

So Mr. Baker, rather than looking for the bubble, let's say we have a fragile system still disordered and mispricing risk, with a few very large banks engaging in reckless speculation, mispricing risk for short term profits, manipulating markets, and distorting the processes designed to maintain a balance in the economy.

Rather than hold out for a 'new bubble' as your criterion, perhaps we may also consider that the patient is still on full life support after the last bubble and crisis. Why do we need to find a new source of malady when the old one is still having its way?

I think if one exercises clear and open judgement, they can see that we have stirred up the same pot of witches brew that has made the system fragile and vulnerable to an exogenous shock, and has kept it so.

A new crisis does not have to happen. This is the vain comfort in these sorts of 'black swan' events, being hard to predict. But they can be more likely given the right conditions, and I fear little will be done about this one until even those who are quite personally comfortable with things as they are begin to feel the pain,

The problem is not a 'bubble.' The problem is pervasive corruption, fraud, and lack of meaningful reform. The 'candidate' is the financial system itself, with its outsized hedge funds and the TBTF Banks with their serial crime sprees and accommodative regulators in particular.

And if one cannot see that in this rotten system with its brazenly narrow rewarding of a select few with the bulk of new income, then there is little more that can be said.

Neil Irwin, a writer for the NYT Upshot section, had an interesting debate with himself about the likely future course of the economy. He got the picture mostly right in my view, with a few important qualifications.

"First, his negative scenario is another recession and possibly a financial crisis. I know a lot of folks are saying this stuff, but it's frankly a little silly. The basis of the last financial crisis was a massive amount of debt issued against a hugely over-valued asset (housing). A financial crisis that actually rocks the economy needs this sort of basis.

If a lot of people are speculating in the stock of Uber or other wonder companies, and reality wipes them out, this is just a story of some speculators being wiped out. It is not going to shake the economy as a whole. (San Francisco's economy could take a serious hit.)

Anyhow, financial crises don't just happen, there has to be a real basis for them. To me the housing bubble was pretty obvious given the unprecedented and unexplained run-up in prices in the largest market in the world. Perhaps there is another bubble out there like this, but neither Irwin nor anyone else has even identified a serious candidate. Until someone can at least give us their candidate bubble, we need not take the financial crisis story seriously.

If we take this collapse story off the table, then we need to reframe the negative scenario. It is not a sudden plunge in output, but rather a period of slow growth and weak job creation. This seems like a much more plausible story...

Anyhow, a story of slow job growth and ongoing wage stagnation would look like a pretty bad story to most of the country. It may not be as dramatic as a financial crisis that brings the world banking system to its knees, but it is far more likely and therefore something that we should be very worried about."

In the first chart we see that there were about 57 tonnes of gold bullion withdrawn from the SGE into China in the latest week. This is not 'official reserves' but all gold without regard to the receiving party.

This pushes the cumulative withdrawals of Shanghai gold over the 10,000 tonne mark. Not bad for less than seven years in the business.

This does not include gold that flows through Hong Kong, or through any other non-exchange means purported to be used by the People's Bank of China.

On the second chart you can see that Year-To-Date Shanghai has released 2,119 tonnes into China. Compared to prior years 2015 is clearly going to be a new record if the withdrawals maintain this pace.

One thing that struck me on that second chart tonight is that Shanghai withdrawals took a definite leg up in 2013.

This is also the same year that the price of gold in Dollars was smacked lower, and the ratio of potential claims to registered gold on the Comex began to climb, and eventually start to go parabolic this year.

Perhaps the bullion bank apologists and shills are right, and this is all just meaningless, an optical illusion, or some fantasy. Gold is just like pet rocks, and the majority of the people in the world, and throughout recorded history for that matter, are just confused and demented.

As I mentioned earlier this evening, the tails risks look rather fat. One might wonder that even a dingy gray swan with a weak wing could trigger a fairly impressive set of 'unforeseeable incidents.'

They'll never learn. Why should they? Winning....

But perhaps we are much closer to the end of this than most people might imagine. Given the explosive ingredients in place it may be hard to miss.

Let us pray for those whose hearts are hardened against His grace and loving kindness by greed, fear, and pride, and the seductive illusion and crushing isolation of evil.

We pray that we all may experience the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness. And in so doing, may we obtain abundant life, and with it the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.