"‘Not everyone who says to me, 'Lord, Lord', will enter the kingdom of heaven, but only one who does the will of my Father in heaven. On that day many will say to me, 'Lord, Lord, did we not prophesy in your name, and cast out demons in your name, and accomplish great things in your name?' Then I will declare to them, ''I do not know you. Depart from me, you who practice lawlessness.'” Matthew 7:21-23

There are quite a few theories and a deepening economic debate swirling around. Even Marx is being selectively resurrected to help explain what is going on. Everything can contribute something, but the less useful parts merely add to the noise and confusion.

I think the situation is a little more simple than many portray, but it is ironically elusive to most people's minds as they distort their models to accommodate the new realities, which are little different from the old realities, at least in the historical context. Reform is a slow horse to leave the gate when the games are still fixed.

Fraud is, after all, a confidence game. But when confidence fails, all the con men have left is fear and greed, and the darker emotions that come with them. So let's talk about anything and everything except what really happened, and make that discussion as complex as possible. Let's not fix what is broken, in small manageable bites. Let's attempt to reinvent and reorganize the entire system. As in corporations, when management fails, time to reorganize and redivide the power amongst the power brokers, rather than actually fix anything.

The sad truth is that most economic models are artificial constructs that crush the life out of reality according to the bias of their authors, and are used to justify behaviours that are in the self-interest in whatever group that promotes them. This is because except for some very basic ideas, macro-economics is not a science, but much more significantly a public policy discussion with some mathematical relationships added, and those largely of a statistical estimation.

This is a long discussion and it is a bit dated. But it is useful to remember where we are on this turn of the circle, and how we got here.

We are in the hysteria period of the financial crisis, an uneasy calm wherein the facade of the system is restored, more or less, and people are attempting to ignore the wreckage and the victims. The winners are standing on their piles of loot, unwilling to give anything up.

But they are not at peace, because they do not or can not talk about how and why this crisis happened, and so cannot be sure that it will not happen again. And they know that a society that is not willing to help the weak will not be able to protect the wealthy.

The economic system was beginning to totter in the 1980's, but it started to slip off the rails in the late 1990's with the final pushes of free market fundamentalism with the unleashing of the derivatives market, and the repeal of Glass-Steagall. The derivatives market is a monster that still remains untamed.

One cannot have a sustainable economy where the Financial Services sector continues to take an inordinate share of national income and corporate profits, which some estimate to be as high as 40 percent. And that largesse is used to virtually control the very system that is set up to regulate and control it.

For those who simply must have an easy answer, here it is:

The Banks must be restrained, and the financial system reformed, with balance restored to the economy, before there can be any sustained recovery.

The descent to hell is easy, but to return to the upper air is always the real task, the labor, especially when your hellion guides continue to herd you about using greed and fear alternatively. How can one attempt to recover, when they do not even know where they are, and do not remember how they got there?

So, here is some food for thought, and what I hope might be an interesting conversation amongst some bright people who don't always agree with each other. But each makes sense in their own way, and contributes to what seems to be an honest discussion, which is a scarce commodity in these times of universal deceit.

There is an obvious but still relatively select 'flight to safety' occurring as a forward looking group of investors flees the equity markets, seeking the safe havens of the precious metals, harder currencies, and government bonds. When and if a 'rush to safety' occurs the resulting impact might be terrific.

Where this will go I cannot say. But say what you will, that is what is happening now as reflected in the markets.

Most commentary that I have read about this flight to safety in the mainstream is naive, quite often spin, and too frequently bordering on slogans, ideology, and the idiotic.

The market was walked up by the futures and the HFT bots on light volumes for a rally that largely fell apart into the close. A stiff breeze will knock this market over, but it might very well take a rather stiff one, because there is little selling, and it seems light human participation in the markets at the moment. The only volume that appears is on the downdrafts. That is a recipe for disaster.

The Conference Board confidence measure today was very low as I had expected given the Michigan result, and the markets shook it off.

Most of the economic news this week will be a prelude to Friday's Non-Farm Payrolls report. The Fed Minutes were illuminating.

I think we need to be prepared for a higher than normal chance of a 'significant dislocation' in the financial system between now and the end of the year. That is still less than even probability however. If the government continues to gridlock on divergent extremes then the probability becomes higher.

What actual shape this 'break' might take I do not know, and will not care to speculate in detail. I am judging by the obvious strains in the real economy and the markets.

"It's not a monster movie. It's a supernatural thriller."

Ed Wood

Stocks need to climb out of a hole, and in order to do this they need to get the allocations from Treasuries. Watch Treasuries and VIX to see how 'real' these light volume rallies in stocks are.

Gold and Silver are rolling with the volatility.

Keep an eye on all the 50 and 200 DMAs and see which one is on top, and where they are going.

When listening to a speech like this, one has to remember who is speaking and under what conditions. A Fed Chairman has a thousand watt megaphone attached to his chest, and so he must speak quietly and calmly, in order not to disrupt markets and place the Fed in the middle of political controversies. Unless you have actually been close to or in a position of power, where your words carry great significance, it is all too easy to forget this.

Bernanke addressed his problem with the dysfunctional Congress, gridlocked by luddites and libertines, and the serpentine leadership style of Obama. He is trying to stand his monetary policy on a two legged stool, and it is not working. The all important fiscal side of economic governance is broken. Not so much that it is doing the wrong things. Rather, the process itself is broken, hopelessly frozen by ideological warfare and implacable extremes.

He reiterated that the Fed has the additional policy tools to deal with the situation, in addition to the unprecedented actions they have taken already, although there is a lack of consensus on his own Fed. It is significant that they have expanded their September meeting from one to two days in order to discuss this more fully.

Bernanke gave a particularly sharp rebuke to the Congress, at least by Fed Chairman standards, for the debt ceiling deadlock and discussions that recently shook confidence in the markets.

There is little doubt in my mind that the Fed will put some additional scalable programs in place before the end of the year. The introduction of new programs during a Presidential election year is typically considered to be only acceptable at extreme risks to the banking system and obvious duress to the economy.

As a reminder, there will be another Non-Farm Payrolls number out next week.

There are forces in the US that are on the offensive, and pushing for a crisis in order to better obtain their objectives. What Bernanke is doing is positioning the Fed on the sidelines as best he can, while signaling that they will act once again, overtly or quietly, to prevent a major financial breakdown.

But he is stressing that the Fed has done quite a bit already, and they cannot do it alone. The monetary actions are ineffective without a fiscal counterpart. Like most observers, the Fed sees a broken governance process, and the new super-committee is likely destined to fail in more gridlock. The Fed will not act again except under the duress of an approaching crisis, although they will have the programs in place in anticipation of that crisis.

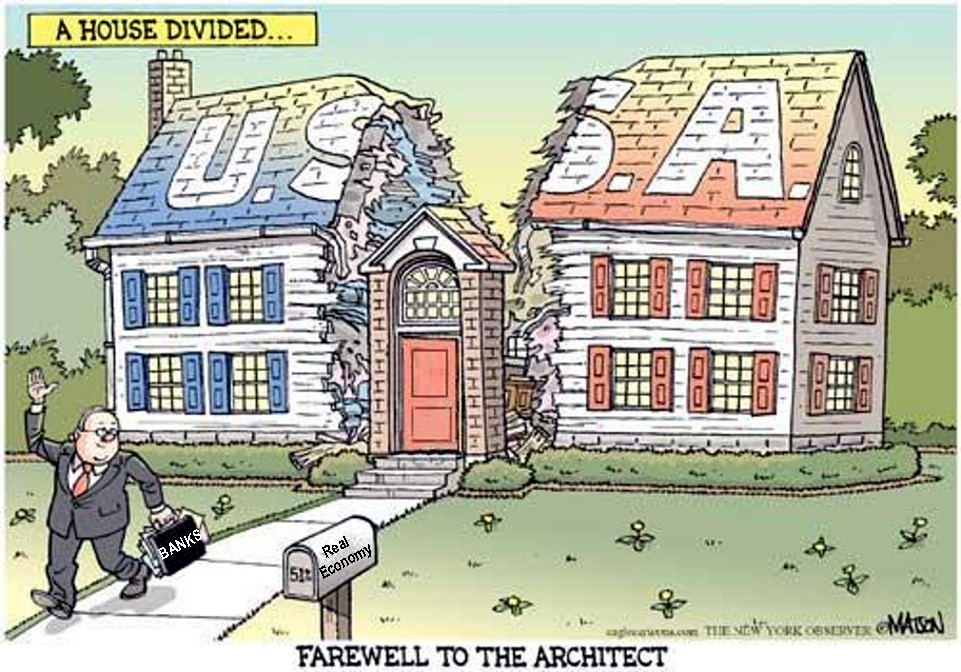

The US is a house divided against itself. Until the system of governance is repaired, the Fed cannot be reasonably expected to take up the burden of the nation's problems on its own.

So for the future, listen to what the Fed says, but more importantly, watch what the Fed does. And some of that may be opaque, at least for the time being.

This is not necessarily what I think, or what I would do if, God forbid, I was the Fed Chairman. This is what Bernanke is thinking in his own words, and what I believe he is doing, and to some extent, why he is doing it.

Fri Aug 26, 2011 10:00am EDT

JACKSON HOLE, Wyoming, Aug 26 (Reuters) - The following are highlights of Federal Reserve Chairman Ben Bernanke's speech on Friday to a central bank conference sponsored by the Kansas City Federal Reserve Bank.

On economic growth, inflation outlook:

"The recent data have indicated that economic growth during the first half of this year was considerably slower than the Federal Open Market Committee had been expecting, and that temporary factors can account for only a portion of the economic weakness that we have observed. Consequently, although we expect a moderate recovery to continue and indeed to strengthen over time, the Committee has marked down its outlook for the likely pace of growth over coming quarters.

"With commodity prices and other import prices moderating and with longer-term inflation expectations remaining stable, we expect inflation to settle, over coming quarters, at levels at or below the rate of 2 percent, or a bit less, that most Committee participants view as being consistent with our dual mandate."

On what the Fed's recent policy decision means:

"We indicated that economic conditions -- including low rates of resource utilization and a subdued outlook for inflation over the medium run -- are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013. That is, in what the Committee judges to be the most likely scenarios for resource utilization and inflation in the medium term, the target for the federal funds rate would be held at its current low levels for at least two more years."

On what other tools the Fed has:

"In addition to refining our forward guidance, the Federal Reserve has a range of tools that could be used to provide additional monetary stimulus. We discussed the relative merits and costs of such tools at our August meeting. We will continue to consider those and other pertinent issues, including of course economic and financial developments, at our meeting in September, which has been scheduled for two days (the 20th and the 21st) instead of one to allow a fuller discussion.The Committee will continue to assess the economic outlook in light of incoming information and is prepared to employ its tools as appropriate to promote a stronger economic recovery in a context of price stability."

On market volatility:

"Financial stress has been and continues to be a significant drag on the recovery, both here and abroad. Bouts of sharp volatility and risk aversion in markets have recently reemerged in reaction to concerns about both European sovereign debts and developments related to the U.S. fiscal situation, including the recent downgrade of the U.S. long-term credit rating by one of the major rating agencies and the controversy concerning the raising of the U.S. federal debt ceiling. It is difficult to judge by how much these developments have affected economic activity thus far, but there seems little doubt that they have hurt household and business confidence and that they pose ongoing risks to growth. The Federal Reserve continues to monitor developments in financial markets and institutions closely and is in frequent contact with policymakers in Europe and elsewhere."

On long-term economic growth prospects:

"It may take some time, but we can reasonably expect to see a return to growth rates and employment levels consistent with those underlying fundamentals ... Notwithstanding the severe difficulties we currently face, I do not expect the long-run growth potential of the U.S. economy to be materially affected by the crisis and the recession if -- and I stress if -- our country takes the necessary steps to secure that outcome."

On the impact of monetary and fiscal policy:

"Normally, monetary or fiscal policies aimed primarily at promoting a faster pace of economic recovery in the near term would not be expected to significantly affect the longer-term performance of the economy. However, current circumstances may be an exception to that standard view ... The quality of economic policymaking in the United States will heavily influence the nation's longer-term prospects. To allow the economy to grow at its full potential, policymakers must work to promote macroeconomic and financial stability; adopt effective tax, trade, and regulatory policies; foster the development of a skilled workforce; encourage productive investment, both private and public; and provide appropriate support for research and development and for the adoption of new technologies."

Some option expiration. Can you believe the nerve of these guys?

Bought the dip, and flipped out at the close. Didn't exactly see that coming, but why say no to free money?

I don't think we're in Kansas anymore, Toto. At least not judging by the size of these waves.

I maintained a core position mostly in gold. Some of the swings today in the miners were pretty impressive to say the least. I won't mention any particular names, but watch how miners perform on days like today, and you will be able to sort out the nuggets from the clinkers.

If the Fed does nothing tomorrow, and only hints around at it, give the market a little time, maybe a week or two, to pry some candy out of Benny's goody bag.

The gold and silver traders are really feeling the stress.

Famed analyst and metals perma-bear Jon Nadler elaborates---

Volatility remains elevated, to say the least, and the major indices appear to be 'coiling for a move,' as they say.

Hurricane Bernanke may provide whatever is required to make that move happen tomorrow, either by what he does, or does not do.

I would look for some aftershocks from this in the coming weeks as additional economic data rolls in.

I ended up NOT going short stocks, since playing the dip in gold and some miners today and flipping out of them into the close provided a more than sufficient amount of short term kicks, bangs and thrills. I had to remind myself that I am not a daytrader these days, and such extravagant profits are often illusory, being quickly dissipated by losses.

Ben Bernanke and his gangsta bankas have been following the approach outlined in this paper from 2004, Monetary Policy Alternatives at the Zero Bound: An Empirical Assessment, which is excerpted below, and also in his famous 'printing press' speech on avoiding deflation from 2002.

I have written about this before several times over the years, but perhaps it is a good time to review the Fed's game plan.

The first item, communications to model and influence the perception of the markets, is obvious. Jawboning is a major element of any financial intervention. Acknowledging or denying the intervention is all about the message as well.

The most recent statement from the Fed, for example, about keeping rates at the zero bound for the next two years, depending on how the economy fares, is a good example of this. Other actions they may take through their own speeches, and the statements of informal intermediaries in the industry and the press, are good examples as well.

The expansion of the Fed's Balance Sheet is also known as quantitative easing, and that has been done at least twice now, and in epic proportions.

The third option, the targeted purchasing of certain assets, has been done to a large extent to support the banking and mortgage system, but not necessarily the real economy. This is the program by which the Fed has been taking non-traditional assets into its portfolio in the various vehicles it has constructed in order to shore up the shaky creditworthiness of the TBTF asset profiles.

What the Fed is not doing in a major program yet, although it certainly has done it in the past, is to conspiculously shift the duration of its Treasury bonds portfolio in order to achieve certain interest rate objectives, effectively setting caps on target rates up the curve.

In 1961 in a program called Operation Twist, the Fed moved the duration of its portfolio to help lower longer term rates. It should be noted that OT1, if you will, was conducted during the fixed exchange rate period known as Bretton Woods I, which included the redeemability of dollars for gold. Also, although the short end of the Treasury curve was not at the zero bound, it was not viewed as adjustable for policy constraints than the zero bound.

So there are some subtle differences perhaps in any OT2 which the Fed might announce this week, or soon thereafter.

John F. Kennedy was elected president in November 1960 and inaugurated on January 20, 1961. The U.S. economy had been in recession for several months, so the incoming Administration and the Federal Reserve wanted to lower interest rates to stimulate the weak economy. Under the Bretton Woods fixed exchange rate system then in effect, this interest rate differential led cross-currency arbitrageurs to convert U.S. dollars to gold and invest the proceeds in higher-yielding European assets. The result was an outflow of gold from the United States to Europe amounting to several billion dollars per year, a very large quantity that was a source of extreme concern to the Administration and the Federal Reserve.

The buying of the longer end of the curve, moving out from the bills to the shorter notes, has been telegraphed repeatedly to the markets this year. So it does appear likely.

The effects would be to lower real rates more broadly across the curve, perhaps taking them all negative, or at least closer to zero on the longer end depending on how one wishes to calculate inflation. I think the Fed uses their chain deflator. I doubt its accuracy for practical purposes, but let's not quibble.

This is 'bad' for the dollar and good for gold and longer dated Treasuries which will enjoy a brief rally. However it will drive yield hungry investors to seek other alternatives, perhaps in the stock market and overseas. It may shake up the Treasury markets on the longer end moreso than we might expect if there is an erosion in confidence in the US' ability to put its house in order without devaluation of the dollar debt. That erosion may be well-founded.

Such a policy move is intended to stimulate consumption and investment in situations where the middle of the curve and out is used as a benchmark for setting non-governmental interest rates. There is thinking that by moving out from the short maturies, the pull lower on the even longer rates will be more pronounced.

I do not think this alone will work. Banks are reluctant to lend at any price, and lowering the rates would not improve the credit risk profile of potential borrowers.

The Fed could also reduce the interest it pays on reserves to zero, or even place a negative rate on it. This would stimulate banks to put the money to work in the markets for projects with positive yields. This is not so different from the Fed's actions in driving consumers out of short term bonds and zero interest savings accounts, which they have done from time to time.

There is some further indications that the Fed will be using a reverse repo mechanism in order to grow bank credit in a more targeted fashion. I will not get into that further here, because if it does develop I am sure there will be much more lucid explanations given in some detail based on Fed announcements.

But it does follow the theme of actively stimulating lending in ways other than lowering rates, even on the longer ends of the curve.

The Fed might couple this with government guarantees on loans for example, for certain situations where the government wishes to stimulate activity, such as housing for example. It is hard to imagine anything like this passes through the dysfunctional Congress.

There is another option that the Fed has, which is not cited in the summary of this paper shown below.

For this we have to turn to Chairman Bernanke's famous speech on Deflation in 2002 in which he stated that 'the Fed's owns a printing press' and highlighted various steps which they might take to insure that deflation does not happen in the US, the ability and the resolve of the Fed to prevent it, and some of the options the Fed might have if they reach the infamous zero bound:

However, a principal message of my talk today is that a central bank whose accustomed policy rate has been forced down to zero has most definitely not run out of ammunition. As I will discuss, a central bank, either alone or in cooperation with other parts of the government, retains considerable power to expand aggregate demand and economic activity even when its accustomed policy rate is at zero. In the remainder of my talk, I will first discuss measures for preventing deflation--the preferable option if feasible. I will then turn to policy measures that the Fed and other government authorities can take if prevention efforts fail and deflation appears to be gaining a foothold in the economy...

What has this got to do with monetary policy? Like gold, U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.

So what then might the Fed do if its target interest rate, the overnight federal funds rate, fell to zero? One relatively straightforward extension of current procedures would be to try to stimulate spending by lowering rates further out along the Treasury term structure--that is, rates on government bonds of longer maturities.

There are at least two ways of bringing down longer-term rates, which are complementary and could be employed separately or in combination. One approach, similar to an action taken in the past couple of years by the Bank of Japan, would be for the Fed to commit to holding the overnight rate at zero for some specified period. Because long-term interest rates represent averages of current and expected future short-term rates, plus a term premium, a commitment to keep short-term rates at zero for some time--if it were credible--would induce a decline in longer-term rates.

A more direct method, which I personally prefer, would be for the Fed to begin announcing explicit ceilings for yields on longer-maturity Treasury debt (say, bonds maturing within the next two years). The Fed could enforce these interest-rate ceilings by committing to make unlimited purchases of securities up to two years from maturity at prices consistent with the targeted yields. If this program were successful, not only would yields on medium-term Treasury securities fall, but (because of links operating through expectations of future interest rates) yields on longer-term public and private debt (such as mortgages) would likely fall as well.

Lower rates over the maturity spectrum of public and private securities should strengthen aggregate demand in the usual ways and thus help to end deflation. Of course, if operating in relatively short-dated Treasury debt proved insufficient, the Fed could also attempt to cap yields of Treasury securities at still longer maturities, say three to six years. Yet another option would be for the Fed to use its existing authority to operate in the markets for agency debt (for example, mortgage-backed securities issued by Ginnie Mae, the Government National Mortgage Association). Historical experience tends to support the proposition that a sufficiently determined Fed can peg or cap Treasury bond prices and yields at other than the shortest maturities...

If lowering yields on longer-dated Treasury securities proved insufficient to restart spending, however, the Fed might next consider attempting to influence directly the yields on privately issued securities. Unlike some central banks, and barring changes to current law, the Fed is relatively restricted in its ability to buy private securities directly. However, the Fed does have broad powers to lend to the private sector indirectly via banks, through the discount window. Therefore a second policy option, complementary to operating in the markets for Treasury and agency debt, would be for the Fed to offer fixed-term loans to banks at low or zero interest, with a wide range of private assets (including, among others, corporate bonds, commercial paper, bank loans, and mortgages) deemed eligible as collateral. (Obviously the Fed has already been doing this as well).

Although a policy of intervening to affect the exchange value of the dollar is nowhere on the horizon today, it's worth noting that there have been times when exchange rate policy has been an effective weapon against deflation. A striking example from U.S. history is Franklin Roosevelt's 40 percent devaluation of the dollar against gold in 1933-34, enforced by a program of gold purchases and domestic money creation. The devaluation and the rapid increase in money supply it permitted ended the U.S. deflation remarkably quickly. Indeed, consumer price inflation in the United States, year on year, went from -10.3 percent in 1932 to -5.1 percent in 1933 to 3.4 percent in 1934.17 The economy grew strongly, and by the way, 1934 was one of the best years of the century for the stock market. If nothing else, the episode illustrates that monetary actions can have powerful effects on the economy, even when the nominal interest rate is at or near zero, as was the case at the time of Roosevelt's devaluation.

Each of the policy options I have discussed so far involves the Fed's acting on its own. In practice, the effectiveness of anti-deflation policy could be significantly enhanced by cooperation between the monetary and fiscal authorities. A broad-based tax cut, for example, accommodated by a program of open-market purchases to alleviate any tendency for interest rates to increase, would almost certainly be an effective stimulant to consumption and hence to prices. Even if households decided not to increase consumption but instead re-balanced their portfolios by using their extra cash to acquire real and financial assets, the resulting increase in asset values would lower the cost of capital and improve the balance sheet positions of potential borrowers. A money-financed tax cut is essentially equivalent to Milton Friedman's famous "helicopter drop" of money. (I think the Obama Administration used this as the rationale for extending the Bush tax cuts).

Of course, in lieu of tax cuts or increases in transfers the government could increase spending on current goods and services or even acquire existing real or financial assets. If the Treasury issued debt to purchase private assets and the Fed then purchased an equal amount of Treasury debt with newly created money, the whole operation would be the economic equivalent of direct open-market operations in private assets. (I believe the Fed has already been doing this with the help of a few Primary Dealers.)

In summation, I think Bernanke's next move will be to start capping the two and three year rates, with the five year to follow. The purpose will be to keep rates low for the purpose of enabling spending and devaluing the dollar. I do not think he will have to expand the Fed's Balance Sheet to accomplish this.

But it is important to note that while the Congress can enforce a debt ceiling on the US Treasury, there is no such hard ceiling on the Fed's Balance Sheet. And this is probably the genesis of Presidential candidate Perry's scarcely veiled threat to Mr. Bernanke and the use of the word 'treason.'

I am not saying that the Fed is right in what they are doing. I am using Bernanke's thinking, and his own words, to determine what the Fed is likely to do next. I have been using this model for the past five years, and it has served me well.

I have some sympathy for Bernanke, because he has few allies, especially among the libertine left and the luddites of the right, and the serpentine Obama. The major obstacle to the US recovery is a failure in governance.

I have very little sympathy for the manipulation of certain markets traditionally viewed as safe havens, based on the rationale outlined in Larry Summer's paper about Gibson's Paradox, and the linkage between interest rates and gold. That appears to be roughly analagous to machine-gunning the lifeboats.

Deflation or inflation are truly policy decisions in an unconstrained fiat currency regime such as that enjoyed by the US. On this Mr. Bernanke is correct, and anyone who thinks otherwise does not understand a fiat money system. It really is that simple. To their credit, the Modern Monetary Theorists understand it very well, except for the downside of excessive money creation in a co-dependent world, even if one does enjoy the exorbitant privilege of the world's reserve currency.

Various interests have been seeking to restrain the Fed, ranging from large creditors such as China, and the domestic monied interests who have already received their bonuses and bailouts, and who do not wish to see their dollar wealth erode. One is richer if all around them are made relatively poorer, or so some lines of thinking go. And of course there are the prudent savers, who have been fleeing the dollar to the relative safety of some foreign currencies and hard assets like gold and silver.

I would hope that by now that any reader here would know that, at least in my judgement, deflation through hard money and austerity, or inflation through stimulus and money printing, are both unable to achieve a sustainable economic recovery because the system is caught in a credibility trap in which the governance of the country is unable to act justly and reform the system without implicating themselves in the compliant corruption that caused the unbridled credit expansion, massive frauds, and financial collapse in the first place.

This was a major contributor to Japan's lost years. The lack of will was in the failure of their largely single party system to correct the inefficiencies and crony capitalism of the banks and their keiretsus that provided a drag on all stimulus and the real economy, siphoning off the additional money into unproductive projects and support for zombie corporations.

The Banks must be restrained, and the financial system reformed, with balance restored to the economy, before there can be any sustained recovery.

Federal Reserve Monetary Policy Alternatives at the Zero Bound: An Empirical Assessment

Ben S. Bernanke, Vincent R. Reinhart, Brian P. Sack

8 April 2004

Abstract

The success over the years in reducing inflation and, consequently, the average level of nominal interest rates has increased the likelihood that the nominal policy interest rate may become constrained by the zero lower bound.

When that happens, a central bank can no longer stimulate aggregate demand by further interest-rate reductions and must rely on “non-standard” policy alternatives. To assess the potential effectiveness of such policies, we analyze the behavior of selected asset prices over short periods surrounding central bank statements or other types of financial or economic news and estimate “no-arbitrage” models of the term structure for the United States and Japan.

There is some evidence that central bank communications can help to shape public expectations of future policy actions and that asset purchases in large volume by a central bank would be able to affect the price or yield of the targeted asset.

Non-Technical Summary

Central banks usually implement monetary policy by setting the short-term nominal interest rate, such as the federal funds rate in the United States. However, the success over the years in reducing inflation and, consequently, the average level of nominal interest rates has increased the likelihood that the nominal policy interest rate may become constrained by the zero lower bound on interest rates. When that happens, a central bank can no longer stimulate aggregate demand by further interest-rate reductions and must rely instead on “non-standard” policy alternatives.

An extensive literature has discussed monetary policy alternatives at the zero bound, but for the most part from a theoretical or historical perspective. Few studies have presented empirical evidence on the potential effectiveness of non-standard monetary policies in modern economies. Such evidence obviously would help central banks plan for the contingency of the policy rate at zero and also bear directly on the choice of the appropriate inflation objective in normal times: The greater the confidence of central bankers that tools exist to help the economy escape the zero bound, the less need there is to maintain an inflation “buffer,” bolstering the argument for a lower inflation objective.

In this paper, we apply the tools of modern empirical finance to the recent experiences of the United States and Japan to provide evidence on the potential effectiveness of various nonstandard policies. Following Bernanke and Reinhart (2004), we group these policy alternatives into three classes:

using communications policies to shape public expectations about the future course of interest rates;

increasing the size of the central bank’s balance sheet, or “quantitative easing”; and

changing the composition of the central bank’s balance sheet through, for example, the targeted purchases of long-term bonds as a means of reducing the long-term interest rate.

We describe how these policies might work and discuss relevant existing evidence...

Well, it looks like an option expiration week to me.

I pulled my 'defensive positions' in the metals today (short positions), and came out of 'flat' to stick a toe into the gold and silver markets in terms of both metals and a couple of miners that looked rather oversold intraday.

As a reminder, tomorrow is options expiration on the Comex.

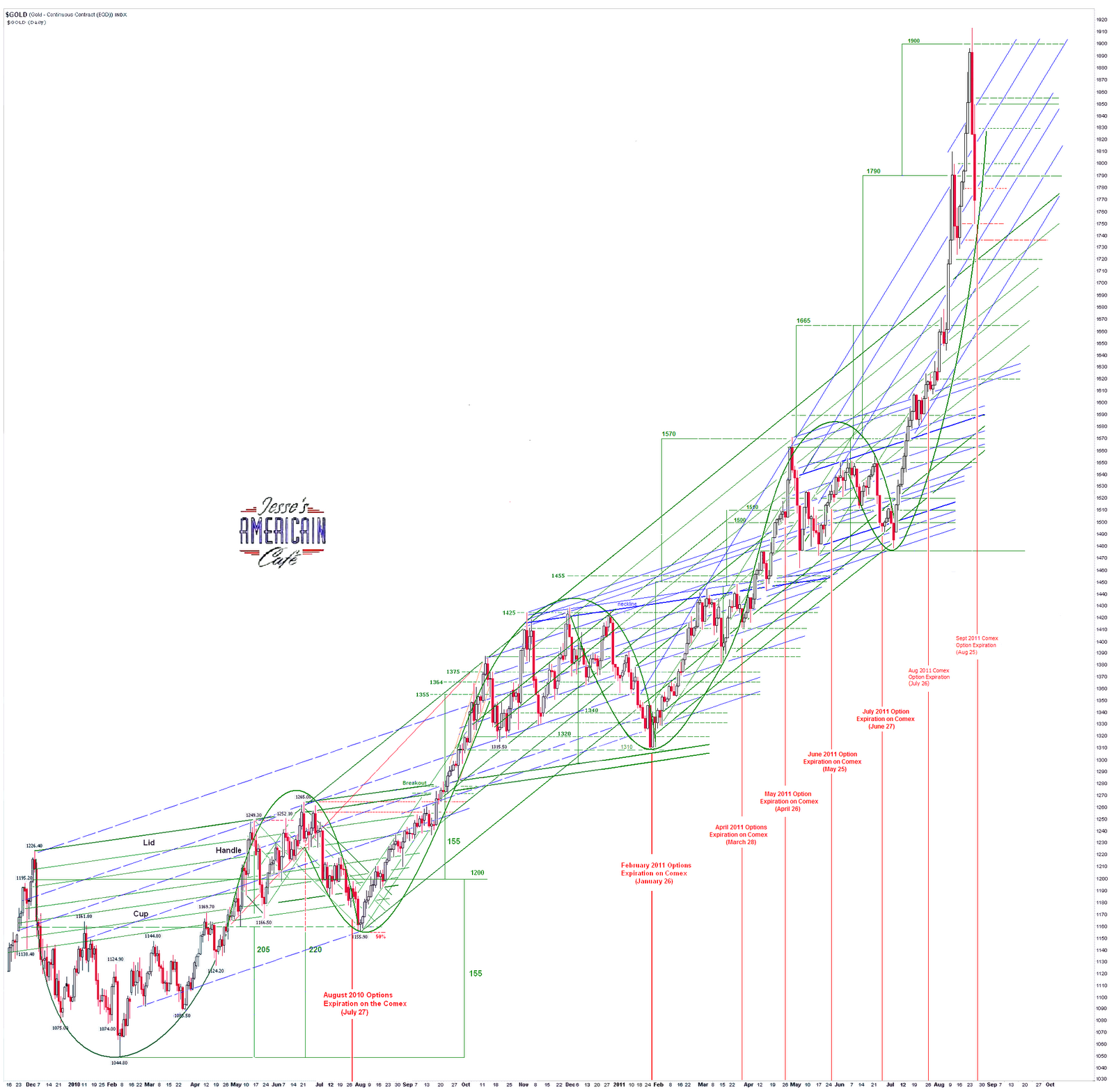

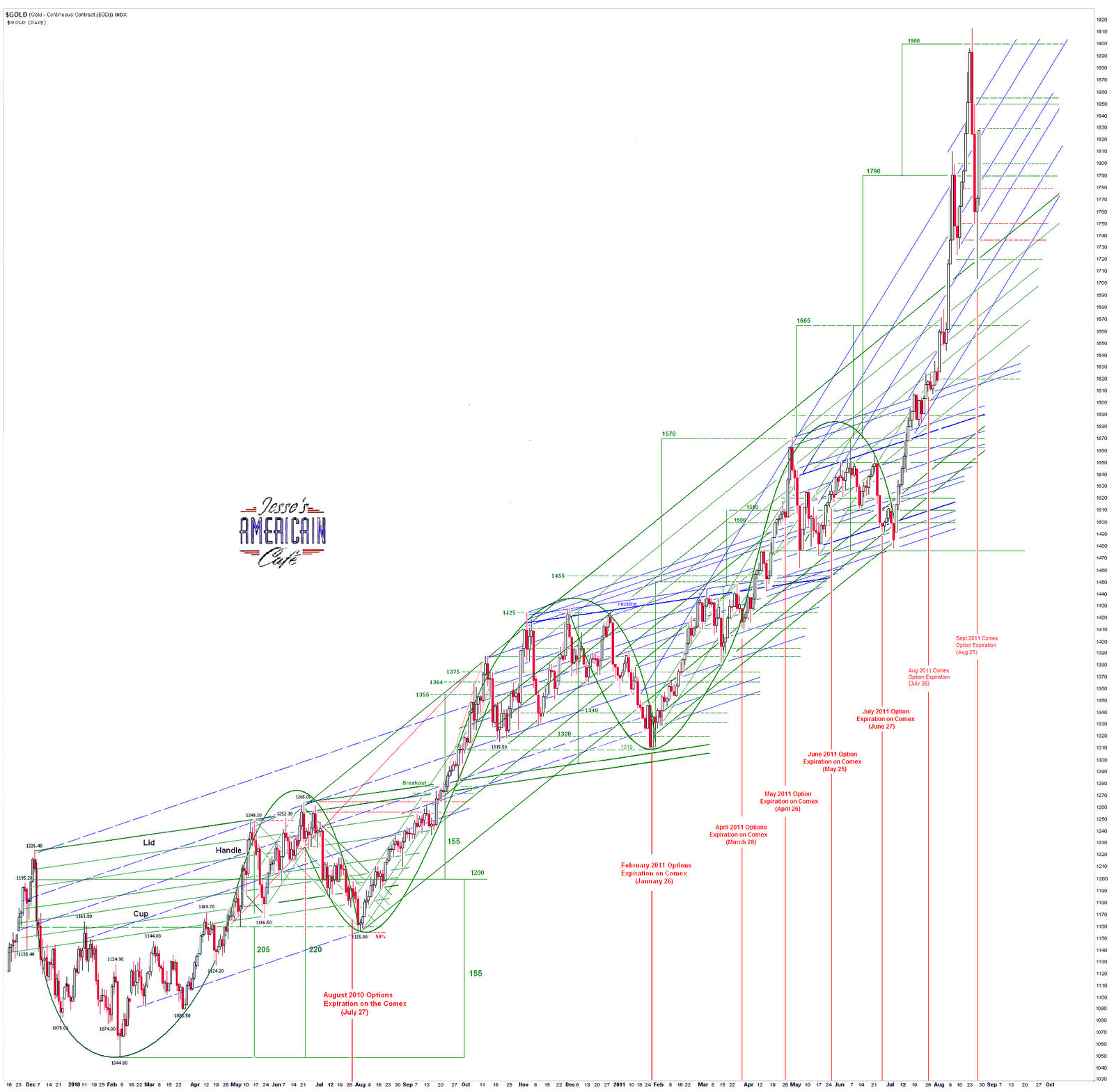

You should be able to spot the support on the chart (at 1720, the top of the green trendlines). That *might* hold, but we may not have a bottom in yet. However, unless there is a game changing event like a sudden balancing of the budget, I would be very surprised if 1658 does not hold in the worst case of a decline, with something north of 1700 more likely.

But I could be wrong. It is hard to forecast price movements in the short term when the biggest and most subsidized traders and the government act informally in collusion with the exchanges to put out a spin to support policy decisions. So we will have to wait and see how far this goes.

A lot of it is going to depend on what Benny has to say on Friday. I have not shorted stocks yet, although the temptation is on the table. Maybe tomorrow ahead of the Fed, once I see how the metals act in expiry.

I was performing useful, real world activities for much of the day.

Those wild and crazy free market capitalists and Wall Street welfare queens want another central bank handout, and might toss a tantrum if they don't get it. I don't expect Ben to actually DO anything this week, but he might drop some hints about playing games with the longer end of the curve.

If he doesn't do or say anything, the markets will test his resolve, next week at the latest.

The dissenting governors are prats, so Ben is really in a tough spot with few allies. His biggest problem is the Congress, the economic luddites on the right and libertines on the left, and of course the spinelessly serpentine Obama, but he can do little about them.

He might have the sack to call their bluffs and let the markets tank, standing on principle, but it is not in the nature of the Fed to do anything like that if it threatens the banking system. Bankers have a bias to propping things up, far beyond the point of hope.

The blatant and heavy handed bear raid in the metals, although a source of some profits and very much anticipated here, still makes one want to gag at its arrogant carelessness and cheap obviousness.

Marketwatch CME raises gold margin requirements again

August 24, 2011, 5:17 PM.

For the second time this month, the CME Group Inc., the parent company of the main metals and energy exchanges in the U.S., announced late Wednesday an increase in margin requirements to trade gold. It raised the amount of money needed to trade gold contracts by 27% to $9,450 per 100-ounce contract.

The move comes on the heels of a $104-an-ounce drop in gold futures prices, which some analysts had blamed partly on speculation that the CME would raise margin requirement again.

Gold’s approach to $2,000 an ounce “invited excess speculation and therefore margin concerns for exchanges,” said Richard Hastings, a macro strategist at Global Hunter Securities. “The quasi-exponential price behavior was dangerous and the exchanges today view this with significant concern — and act quickly.”

Steve Jobs is everything that Bill Gates pretends to be. I am sorry to see him pulling back from his duties at Apple for obvious health reasons.

He is a one of the great ones.

Steve Jobs resigns from Apple, Cook becomes CEO By Poornima Gupta and Edwin Chan

SAN FRANCISCO (Reuters) - Silicon Valley legend Steve Jobs on Wednesday resigned as chief executive of Apple Inc in a stunning move that ended his 14-year reign at the technology giant he co-founded in a garage.

Apple shares were suspended from trade before the announcement. They had gained 0.7 percent to close at $376.18.

The pancreatic cancer survivor and industry icon, who has been on medical leave for an undisclosed condition since January 17, will be replaced by COO and longtime heir apparent Tim Cook.

"I have always said if there ever came a day when I could no longer meet my duties and expectations as Apple's CEO, I would be the first to let you know. Unfortunately, that day has come," he said in a brief letter announcing his resignation.

The 55-year-old CEO had briefly emerged from his medical leave in March to unveil the latest version of the iPad and later to attend a dinner hosted by President Barack Obama for technology leaders in Silicon Valley.

Jobs' often-gaunt appearance has sparked questions about his health and his ability to continue at Apple.

"I will say to investors: don't panic and remain calm, it's the right thing to do. Steve will be chairman and Cook is CEO," said BGC Financial analyst Colin Gillis.

On Friday Uncle Ben will be speaking from Jackson Hole, and the markets are eagerly awaiting some words regarding any version of QE3.

This is of course one of the best signs of how utterly dislocated and distorted the real economy can be.

It is also a clear sign of how many 'free market capitalists' are really on the government feedbag, from bailouts to subsidies to tax breaks, of one kind or another.

The reason for dropping of the sell orders and associated derivative bets, lifting of gold into the oxygen depletion zone, with a subsequent series of bear raids, is obviously in honor of the September options expiration this week on the Comex, and the Jackson Hole speech of Mr. Bernanke regarding the Fed's next steps on currency debasement.

But for those who were looking for a margin increase, do not despair. We forget that there is a new kid on the block. Eric McWhinnie at the Wall Street Cheat Sheet reminds us that:

"The prior sharp selloff was seen on August 11. This is significant because the CME increased gold margins by 22%, effective after the close of business on August 11. The same beat down method seen in silver months earlier, was seen in gold. However, gold recovered quite well until yesterday’s sharp selloff. So what caused this familiar selloff in gold and silver? Another margin hike!

Late Tuesday, it was announced that The Shanghai Gold Exchange increased gold margins for forward contracts, the second time this month. Li Ning, an analyst at Shanghai CIFO Futures said, 'Gold prices on the global market have been rallying strongly and at an increasingly faster pace. The margin hike is a pre-emptive move in case prices crashed and caused great volatility in the market. The Shanghai Futures Exchange could raise margins on its gold futures contract soon too.'”

I doubt very much that the Shanghai forwards increase caused this pullback. More likely Shanghai saw the setup for this week as I did last week, and sought to protect itself.

But nonetheless it is a good reminder that this is not your father's gold market anymore, with new players and exchanges entering the game, but perhaps it will be more like your great-grandfather's gold market over time.

This too shall pass. The tune may change, but the fundamentals remain the same. Banking cartels do not create wealth; they can merely attempt to confiscate and redistribute it, as stealthily as possible. And therefore bullion is their enemy since it forces them into the open.

I found this email from a reader to be very interesting, and I asked him for permission to share it with you.

Most students of economics are aware of the tendency of 'perfect competition' to zero economic profit over time, unless there is a continual renewal and reinvention of the business, under the guidance of a wise, insightful, and responsive management. Even the best enterprise involves a risk of loss, the expense of well paid employees, and significantly hard work, all combined with a bit of luck. Little wonder that a minority of businessmen find this arrangement less satisfactory that other alternatives, which unfortunately includes various forms of cheating, if not outright fraud.

And therefore there is a constant tendency of participants in capitalist systems to foster the unreasonable profits of cartels and the stable pricing power of monopolies, natural or otherwise, with a measure of discretionary control over resources and choices, legislation and information, and political and monetary power.

Corporations are creatures of the law, and inferior to it. Without it, they don’t exist. What better way to create the supreme monopoly and maintain it in perpetuity than to skew the law in one’s favor?

When corporations obtain an inordinate amount of power over the social fabric of regulation and governance, the creation of an oligarchy distorts the real economy through the accumulation of too much power in too few hands, in the manner of the central planning bureaucracies of the old line communist nations.

And this is why the standard economic solutions of both stimulus and austerity for normal cyclical excess can be doomed to failure, as they are at this time. The system itself has become distorted and broken, and is badly in need of reform. Whatever one puts into it will come out badly, and be turned to fruitless purposes, corrupted by the unprecedented concentration of power in the hands of the few, the partnership of the Wall Street banks, big media, multinational corporations, and their servants in the government.

The hallmark of a corrupt enterprise is that while it has the power to confiscate and destroy, it cannot create sustainable organic growth and recovery that benefits the broader public.

The modern, somewhat romantic theory of naturally efficient markets peopled by inhumanly rational and altruistic individuals is a fairly modern twist on the noble savage ideal of Rousseau, and just as other-worldly and impractical when applied to a modern society. Certainly no one who has driven recently on a modern highway in rush hour could believe it.

The corrupting tendencies of the concentration of power is an intriguing idea, with an historical resonance from the trust-busting Teddy Roosevelt, and his distant cousin Franklin, as well as the famous observation of Lord Acton:

"And remember, where you have the concentration of power in a few hands, all too frequently men with the mentality of gangsters get control. History has proven that."

Nineteenth century Americans viewed the business trusts as un-American "internationalists, and heartless, abusive exploiters of the public interest." And rightly so. They looked for relief to the reform of their government, and the power of democracy and the law.

This struggle of the individual to maintain a balance of power with the organizations, whether they be the corporation or the state, is a recurrent theme, a continuing saga throughout human history. Big Government and Big Business have both been inimical to human freedom.

Whether such an accumulation of power in a few hands is achieved by the gun and star chamber, or the pen and the bribe, may not matter to the end result, which is a society plagued by corruption, stagnation, and at its end, a growing instability with a resort to physical force and more overt repression on its own people.

Central Planning - It's not Just for Communists Anymore By Matthew K

23 August 2011

Vancouver, BC

It's been a rough few weeks for the capitalist system, which bestrides the globe like a teetering colossus. Not only has there been stock market turmoil worldwide, and the temporary threat of a US default on its debts, but an esteemed, mainstream economist suggested that Karl Marx was right. In the Wall Street Journal, no less! Karl Marx Was Right

That would be Nouriel Roubini, whose claim to fame came from timely warnings about the US housing bubble and subsequent US stock market collapse.. It is important to note that he only said that Marx was right in that capitalism could collapse on itself, not that it actually would.

Most people are familiar with the spectacular failures of central planning in the Communist regimes. According to the resurgently fashionable Austrian school of economics, an economy is too complex to be managed by one expert, or even one committee of experts, regardless whether the clubhouse door reads "Politburo" or "Shark Tank."

According to the Austrians, society's fastest path to prosperity consists of allowing every person to decide freely what is in their best interest, with the emphasis on individual transactions.

A biological analogy comes from flocks of birds, schools of fish, and ant colonies, among others. These swarms function extremely well, despite being composed of simple creatures following simple rules, and despite the anarchic lack of a leader directing things. Our own "simple critter rules" in modern society are probably along the lines of "try to get a higher paying job, and pay lower prices for stuff, within the laws of the land, and without making too many enemies."

A business analogy comes from Toyota. Their quality went from hopeless to fearsome by training every employee to be competent enough to figure out how to do their own job better, and then allowing them to do so. If their management tried to dictate how each task was to be done, they might have peaked at early-80’s American car maker quality levels.

In a similar way, they decided not to try to predict the right production levels for each model, colour, and trim. Instead they pre-built enough cars to fill dealership inventory, and each time a customer purchased a vehicle, they would build one more of that same model, colour, and features. In economic nerd speak, they responded to that "market signal". So if 5% of Corolla drivers wanted a green car with deluxe extras, in the long run 5% of Corolla production would consist of deluxe green vehicles.

Since the flaws of central planning and benefits of distributed decision-making occur in the public sector, the private sector, and even in biology, we can generalize that the USSR's economic problem was ultimately that a small group of people would decide how to (mis)allocate most of the country's resources.

In the past thirty years, there's been an immense concentration of wealth -- particularly in Anglo-American countries (the US, UK, us, the Aussies). The US is at the leading edge of this trend, with the top 1% owning 42% of the wealth, or about six times as much as the bottom four fifths of the population, and a significant portion of the means of production and public information (media) and influence over the course of society.

In recent decades Western capitalism has moved towards the central planning model of a relatively small number of people in charge of directing the allocation of resources. This narrowing of perspective has in turn led to policies progressively more disastrous for the moved and the shaken... which was the Soviet denouement.

I have to credit the influence of the thoughtful blog of a well-to-do American entrepreneur and military strategist, and especially this particular posting. Central Planning and the Fall of US Empire

Capitalism's path back from the self-perpetuating central planning will require a more equitable, or at least a less inequitable, distribution of wealth and power, by which to rebuild the middle class and promote decision making based on individual choice and a more widely based entrepreneurial meritocracy. Which is what Roubini was complaining about, in saying that too much wealth was being redistributed from labour to capital.

It would be a terrible irony if Marx was proven correct, and unchecked capitalism destroyed itself by evolving the self-crippling features of a centrally planned communist economy. One can only hope that we can reform our current market systems before things get worse.

Gold was lifted into the oxygen depletion zone above $1,900 overnight, and as predicted, the bear raids were launched today in force, together with nonsensical commentary from the financial demimonde.

"...the market in physical gold is tiny, and largely comprised of nutcases."

No wonder the Anglo-American financial cartel is in such decline. Blind is the arrogance of faded empire, when it can no longer succeed by telling their client states what to do.

And of course the television spokesmodels were able to cite the overnight peak and say, "Wow, strap on my seatbelt. Gold is down $60!" Better rush into the rock solid safety of equities. Here are a very nice selection of stocks for you, at recently marked down prices.

Yes, they really are that obvious.

So what next? Gold and silver will probably be subject to additional bear raids as the Comex expiration is not until Thursday the 25th, and Bernanke will be speaking from Jackson Hole on Friday the 26th.

This does not yet have the feel of the May option expiration silver smack down, with its serial margin increases by the Exchange. The gold market has a strong underlying bid now with Venezuela repatriating its gold, and strong buying by non-Western nations and their central banks.

There is a currency war underway, and the primary bone of contention is the nature of the world's reserve currency and fiat based international trading regime. There are ancillary issues of course, but the position of the US dollar, the petro-dollar if you will, as the world's reserve currency is key.

The biggest risk to Venezuela is not in transporting the gold. It is the counter party risk, of obtaining the return of their sovereign property from the Anglo-American banking cartel.

"As mentioned in previous quarterlies, the main long-term risk is that after two massive bubbles and two equally massive resurrection programs, the Fed may be out of ammunition.

Should more building blocks fall and a serious global double-dip develop, then the pattern of market behavior this time may be more historically typical. That is, instead of quickly recovering, markets will become cheap and stay below long-term averages for several years as was the case pre-Greenspan."

Jeremy Grantham

A big technical relief rally in stocks despite some very poor economic news, earthquakes and an approaching hurricane, lol.

The market was on support and deeply oversold. Yesterday was the 'stutter step' at support that indicated they were going to try and take it back up today no matter what. And so they did.

All eyes on Jackson Hole. I doubt Benny will roll anything out of significance, but some jaw-boning is de rigeur.

There is no economic recovery for people, just corporate people.

A wild day in the markets today as stocks came in much higher and then tanked, with the CDS spreads on Bank of America running much higher along with gold and to a lesser extent silver.

On Friday Bernanke will be speaking at Jackson Hole, and the markets are looking for some indication of the latest subsidy to the markets from the Fed. If not a flat out QE3, then perhaps Benny will speak about a program to control the longer end of the yield curve.

All this uncertainty had investor flocking into the safe haven of gold sending it to the 1890's. This has been a brutal rally for the metals bears.

This Thursday the 25th is the option expiration on the Comex. I have to admit that I am concerned that gold has been allowed to rise up into the oxygen depletion zone here, as had been done with silver not all that long ago, and that applications of bear raids and margin increases will bring it tumbling back down to support.

I wouldn't try and get in front of this comet, because we are not quite sure what is driving it. Chavez' margin call on the Bank of England's gold could be triggering this parabolic run. It would nice if gold consolidated its gains soon. I am playing the markets defensively for now.

Let us pray for those whose hearts are hardened against His grace and loving kindness by greed, fear, and pride, and the seductive illusion and crushing isolation of evil.

We pray that we all may experience the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness. And in so doing, may we obtain abundant life, and with it the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.