"Always fight for progress and reform, never tolerate injustice or corruption, always fight demagogues of all parties, never belong to any party, always oppose privileged classes and public plunderers, never lack sympathy with the poor, always remain devoted to the public welfare, never be satisfied with merely printing news, always be drastically independent, never be afraid to attack wrong, whether by predatory plutocracy or predatory poverty.”

Joseph Pulitzer, Retirement address

"Day by day the money-masters of America become more aware of their danger, they draw together, they grow more class-conscious, more aggressive. The [first world] war has taught them the possibilities of propaganda; it has accustomed them to the idea of enormous campaigns which sway the minds of millions and make them pliable to any purpose. American political corruption was the buying up of legislatures and assemblies to keep them from doing the people's will and protecting the people's interests; it was the exploiter entrenching himself in power, it was financial autocracy undermining and destroying political democracy."

Upton Sinclair, The Brass Check

"It’s not just political spin, however, that explains the rose-colored coverage [in the media]. Another explanation is that the media is plain stupid — quick to accept guidance from economists on Wall Street, for example, who have a vested interest in making everything wonderful."

John Crudele, Americans Have Not Gotten a Raise In 16 Years

"In 1983, 50 corporations controlled most of the American media, including magazines, books, music, news feeds, newspapers, movies, radio and television. By 1992 that number had dropped by half. By 2000, six corporations had ownership of most media, and today five dominate the industry: Time Warner, Disney, Murdoch's News Corporation, Bertelsmann of Germany and Viacom."

Independent Lens, Democracy on Deadline

"The elite want to keep us fighting left and right, so we don't pay attention to the top-down."

Jimmy Dore

Showing posts with label financial media. Show all posts

Showing posts with label financial media. Show all posts

10 September 2019

Matt Taibbi, Katie Halper, and Jimmy Dore: Why Is the Media So Bad

22 July 2015

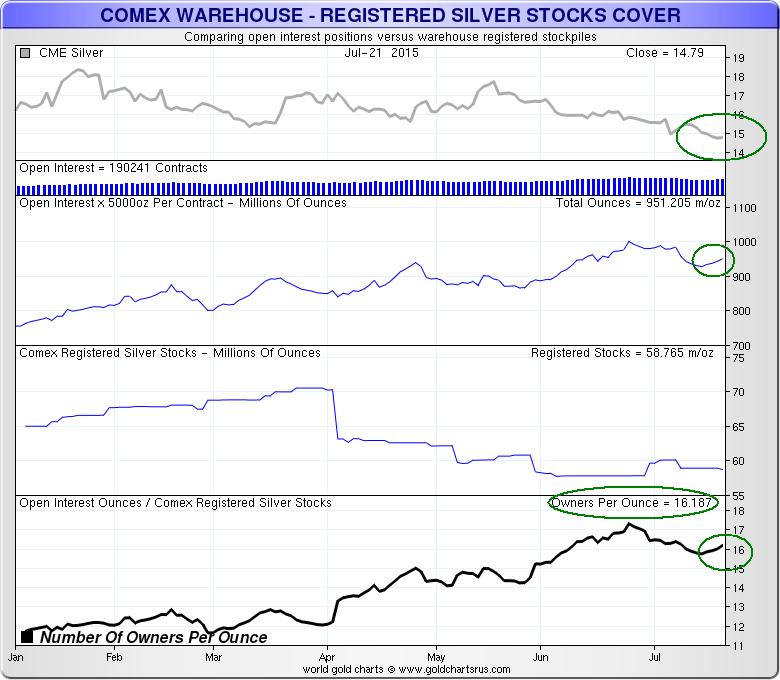

Free Markets At Work - Gold and Silver 'Owners Per Ounce'

"The government is the potent omnipresent teacher. For good or ill it teaches the whole people by its example. Crime is contagious. If the government becomes a lawbreaker, it breeds contempt for law; it invites every man to become a law unto himself; it invites anarchy.To declare that the end justifies the means -- to declare that the government may commit crimes -- would bring terrible retribution."Louis D. Brandeis

I was curious to see what the big price smackdown had done at The Bucket Shop relative to the 'claims per ounce' in the precious metals.

I will be checking again tomorrow to see what the little extra kick we saw this morning might have accomplished.

In summary in silver the 'claims per ounce' actually rose a bit. This is not surprising so much because this is an active month for silver, and it clings stubbornly, almost as if by its fingertips, to the $15 handle.

Gold was as you know hit harder, being smacked down by an avalanche of futures contract selling into one of the quietest periods of the overnight trade.

The open interest actually declined a bit, but significant amount of new gold for delivery appeared, so the 'claims per ounce' as I prefer to call it dropped only to about 97:1.

They did, however, break the uptrend which had been driving towards 100:1.

Have you ever heard the rarely told story from the great bull market of the 1920's, about an unremembered 'publicist,' which is a five dollar word for a simple 'bagman,' named A. Newton Plummer?

'An investigation later discovered that business journalists for at least eight papers promoted stocks in their writing in return for bribes. The most embarrassing were at the Wall Street Journal, where reporters who wrote “Broad Street Gossip” and “Abreast of the Market” took payoffs for stock tips in the 1920s.The revelations about the Journal reporters came out during hearings by the Senate Banking and Currency Committee in 1932, more than three years later, when Congressman Fiorello LaGuardia produced cancelled checks written to the Journal reporters from publicist A. Newton Plummer. The stories based on the bribes had gone as far back as 1923. The Journal ran the story about the testimony before the committee on page 11 the next day.University of North Carolina, History of Business Journalism

We are very fortunate that such a thing could not happen today. Can you imagine any self respecting analyst or media type or politician accepting physical checks? In our modern era it would be much more likely to be hot tips on which way the HFT wind will be turning, or some drinks and dinner, maybe even hookers and blow. The only risks there might be some nasal cartilage or some extra time at the gym.

A. Newton Plummer apparently presented a whole suitcase full of cancelled checks to the Congress in 1932, and wrote a book about it titled The Great American Swindle Incorporated. There were only 2,000 copies printed. There is one in my library.

"I would say that practically all the financial journals were on the take. This includes reporters for The Wall Street Journal, The New York Times, The Herald-Tribune, you name it. So if you were a pool operator, you’d call your friend at The Times and say, “Look, Charlie, there’s an envelope waiting for you here and we think that perhaps you should write something nice about RCA.” And Charlie would write something nice about RCA. A publicity man called A. Newton Plummer had canceled checks from practically every major journalist in New York City."Robert Sobel in PBS, The Great Crash of 1929

Of course with so many other innovations in finance, the information sharing culture of privilege has moved from the inkstained cubicles of 'journalists' to the hallowed halls of the Congress. This was the most read story of all time at Le Café when first published.

And since then you will be happy to know that the Congress has officially told the SEC to go take a hike, that they are immune to any laws against insider trading and dealing in dodgy information, apparently even for 'pay.' There is even a cottage industry of lobbyists who share information with the Congress on behalf of hedge funds. Nice to see entrepreneurship at the lower levels who can never expect to bring in the big bucks making 'appearances' and giving 'speeches' for fabulous fees.

The precious metal pool operators can surely make some nice profits on their short bets on related items after their latest escapades, and then acquire quality mining assets on the cheap for the next trip up when you know what hits the twirling blades, thanks to their servants' gross mismanagement and policy errors.

Well done.

So many assume that the 'rig' in the metals is similar to the London Gold Pool and past operations that were undertaken in order to support some otherwise unsustainable policy and persuasion initiative.

What if something like this started out that way, but then found its momentum in some mutually lucrative private profiteering that proved too easy and tempting and perhaps inconvenient to stop? It certainly has been hard of late to overestimate the self-serving venality and audacious excesses of these jokers.

When you don't know, you don't know. And that is how they seem to like it, what 'it' is. In a society not of reason and laws but of secrecy and privilege, knowledge, like the ability to print and distribute money, is power.

.

25 September 2014

Mr. Cohan Responds On His Silver Rigging Exposé - Two US National Publications Refused the Story

"We run carelessly to the precipice, after we have put up a façade to prevent ourselves from seeing it.”

Blaise Pascal

This is starting to make more sense.

Apparently Mr. William Cohan, a highly respected journalist, did look at all the relevant information he had been provided, and decided to write a story about rigging in the silver markets.

It was submitted and refused by at least two US publications which refused to run it.

It was submitted and refused by at least two US publications which refused to run it.

Based on past history, one might assume the two national publications that refused to publish it were on the order of The New York Times, and perhaps Bloomberg News or even possibly Forbes.

The actual reasons that they gave for refusing to publish the story are not stated. One can assume they were not sufficient for Mr. Cohan to decide to take his name off of it in his professional judgement, so we can only surmise.

So we cannot tell if this was editorial scruples, a failure in fact checking, or just good old fashioned minding of one's place.

So we cannot tell if this was editorial scruples, a failure in fact checking, or just good old fashioned minding of one's place.

Insiders never speak ill of insiders.

Bill was good with publishing the piece at ZeroHedge with his name on it. So he apparently still had confidence in what he had written.

That speaks volumes.

At that point the whistleblowing parties, if one might call them that, deferred, feeling perhaps that printing something like this on the web alone, even on a large and widely read site, would relegate it to something easily dismissible by the status quo. The Very Serious Players choose to read only properly vetted, fully credible and approved mainstream sources.

I am being a bit sarcastic, but not so much. The thought leaders and ruling class in the US are, alas, out of touch almost without regard to their origins. And one does not have to think too hard about it to discover why. They only read the right publications, watch the right shows, talk to the right people, say the right things, and think the right thoughts.

They live in virtual palaces and bubbles of ease and influence. To borrow a phrase from one of their less pliant pets, when they go out amongst the common people, it often resembles Prince Charles on a royal visit to Papua, New Guinea. As George Orwell noted in his diaries, 'apparently nothing will ever teach these people that the other 99% of the population exists.'

They exist, they just don't matter in the halls of power anymore.

I might have suggested some publishing options a little 'out of the box' like The Guardian or Der Spiegel. Choosing publications that might be less beholden to the New York financial powers seems as though it could be a more fruitful course of action. South China Morning Post, or even the Asia Times? Radio Free America?

So there you have it. We have a story. And the mainstream media refuses to publish it. And there is some wrangling about where and when it might achieve adequate exposure to do some good.

To: addresseesThank you all for writing me regarding Andrew Maguire's story of alleged "manipulation" in the silver market. As you may know, I was approached 11 months ago by a PR representative of Mr. Maguire's who wanted to introduce me to Andrew and to his attorney Gordon Schnell, at Constantine Cannon, in New York. I found what Andrew had to say very interesting, especially so in light of a piece I had written in the New York Times about the silver market three years ago. A Conspiracy With a Silver LiningI wrote up the story and submitted it to a national publication in the United States, which decided not to publish it. I then tried another, national financial publication, which also decided not to publish it. I then abandoned hope that the story would be published.About a month ago, Ned Naylor-Leyland contacted me and suggested that Zero Hedge might publish the story. I thought that would be a fine idea.Unfortunately, Mr. Schnell did not like the idea of Zero Hedge, nor apparently did his clients. They also declined to approve the use of key facts and key quotations that I felt needed to be included in the story to give it credibility. Part of my agreement with them was that they would be given quote approval and without their approval, I could not use their quotations or their information.They did not approve. At that point, without their cooperation, I did not feel the piece could be published. I explained that to Mr. Naylor-Leyland but he didn't seem much interested in those facts and then went on to encourage the publication of the piece to which you are all responding.All of which is to say, you are directing your passion to the wrong person. If you want the piece published, you need to reach out to Mr. Maguire and Mr. Schnell.Thank you for your interest and your passion on this topic.William D. Cohan

29 June 2013

Corporate Media: Journalism In the Service of the Powerful Few

"But the biggest clue that Sorkin's take on Greenwald was no accident came in the rest of that same Squawk Box appearance:

"I feel like, A, we've screwed this up, even letting him get to Russia. B, clearly the Chinese hate us to even let him out of the country."...As a journalist, when you start speaking about political power in the first person plural, it's pretty much glue-factory time."

I would arrest him . . . and now I would almost arrest Glenn Greenwald, who's the journalist who seems to want to help him get to Ecuador."

Matt Taibbi, All Journalism Is Advocacy Journalism

"And remember, where you have a concentration of power in a few hands, all too frequently men with the mentality of gangsters get control. History has proven that."

John Dalberg Lord Acton

While I obviously can not agree with everything in this long documentary, Orwell Rolls In His Grave, I found the discussion and examples to be interesting.

I have included a short video clip concerning the standard visual media set piece afterwards just for fun.

The problem is not that there is advocacy in journalism. There is always advocacy in journalism, even despite a striving for objectivity. Taibbi goes to some lengths to show this in the piece I quoted from above.

The problem is the concentration of ownership in a few powerful hands, and the accompanying diminishment of the exposure of all the facts and perspectives. Even deciding what is not covered becomes a form of censorship.

Like the deregulation of the financial industry, the concentration of the media in a relatively few corporate hands was a ongoing trend that took a great leap forward under the presidency of Bill Clinton, and was then continued and reinforced under George Bush and Barack Obama. It was the conscious undoing of reforms from past lessons learned.

It is the concentration of ownership of the corporate media that is at the heart of the problem of the decline of independent journalistic standards. That, and the culture of unprincipled expediency in the service of power and shameless greed.

We are not responsible, but are culpable to the extent we accept this decline in decency and justice, even by doing nothing as simple as passing on a leaflet, conveniently electronic these days. As Sophie Scholl once said, many years ago in Munich, a people deserve the government which they are willing to tolerate.

13 August 2012

Bill Black Educates the Media On the Nature of Financial Fraud, With Little Apparent Effect

Although I linked to this last week, I thought I would like to feature it today.

In one of his rare appearances on the 'mainstream media' Bill Black educates the CNBC news anchor Maria Bartiromo and news contributor Bethany Maclean on the nature of financial fraud.

It is interesting to see the NBC news people acting as apologists for the financial powers, trotting out false arguments and talking over or rushing past the facts when they are presented. At least Bloomberg is more straightforward in their presentation of blatant hucksterism, making little pretense to journalism or presenting any other side of the Wall Street story. They are salespeople and spokesmodels for the financial industry and the monied interests.

Just putting a letter or two in front of a storied call sign, as in the case of MSNBC and CNBC, does not protect that brand from the tarnish of increasingly low standards and future scandal. All of the major media seems to be dancing to Rupert's pied piper's tune.

As storied NBC news anchor David Brinkley once said:

"Being an anchor is not just a matter of sitting in front of a camera and looking pretty."

"News is what somebody somewhere wants to suppress; all the rest is advertising." Lord Northcliffe

14 January 2010

Retail Sales "Unexpectedly Fall In December"

"Unexpected" only because we have been so systematically misled by the government and the financial media about the state of the US economy.

People bought in November in expectations and a believe in the recovery. And buying tailed off quickly in December as they realized it was a hoax: there would be instead of recovery a long cold Kondratieff winter.

Yahoo Finance

Retail sales unexpectedly fall in December

January 14, 2010, 8:34 am EST

WASHINGTON (Reuters) - Sales at U.S. retailers unexpectedly fell in December as consumer spent less on vehicles and an array of other goods during the holiday shopping month, data showed on Thursday, raising concerns about the durability of the economy's recovery.

The Commerce Department said total retail sales fell 0.3 percent last month, the first decline in three months, after rising by an upwardly revised 1.8 percent in November. Sales in November were previously reported to have increased 1.3 percent.

Analysts polled by Reuters had forecast retail sales gaining 0.5 percent last month...

Subscribe to:

Posts (Atom)