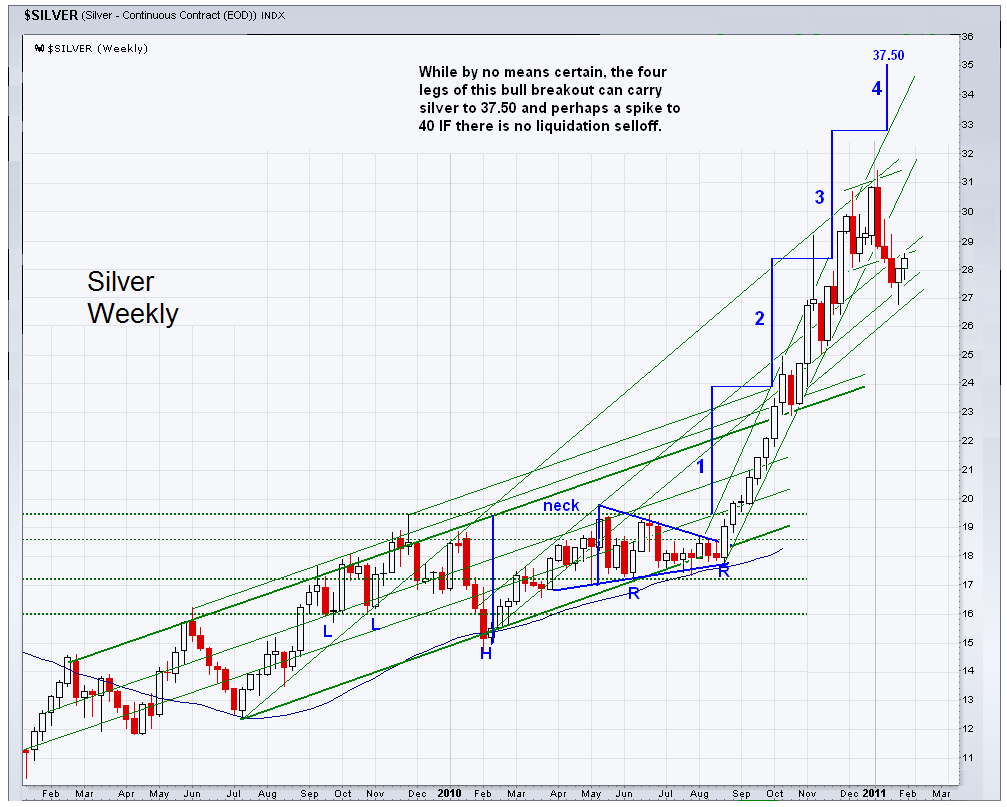

Silver is looking explosive. I think it will take a severe stock market correction of a certain type to slow it up.

The Wall Street wiseguys are getting a little edgy that mom and pop are not taking the handoff at the top of a mini stock bubble.

I will be quite interested to see how both gold and silver act in any pullbacks in the equity bubble. But until then its up and up on the Fed float.