skip to main |

skip to sidebar

You can't tell the players without a scorecard.

These are the 'official statistics.'

The truth is yet to be told.

Everything was bouncing today, even the dollar.

The tech stocks were notable laggards, and the miners did not get back all the losses of the past couple of days.

Follow through is everything.

We had the bounce as expected. It came on support, and from a short term oversold condition.

The next few days will tell if this is just a dead cat bounce or the beginning of a short term trend reserval.

Both the US and the UK have now taken downgrades to their sovereign debt, although the US is sloughing their own off because it came from a European agency.

The miners were hit much harder than bullion today, in keeping with the stock market weakness.

Four Simple Indicators for Precious Metals - Hussman

We might see a technical bounce around here in stocks, not something based on fundamentals. Stuffing the dysfunctional banks with money is not working, but the Fed and Washington seem incapable of taking effective new types of action.

Pawlenty's proposal of more tax cuts for corporations and the wealthy, while shifting more of the burden to the middle and lower classes, is probably the last gasp of a dying theory that still breathes life and does damage.

Neither stimulus nor tax cuts will work on an economy that is broken from years of public policy that favored job destruction and median wage stagnation. It is like putting gas into a car wrapped around a telephone pole.

And yet the US finds itself in a credibility trap, wherein the power brokers are complicit in national theft, and cannot stop themselves and each other from 'going in for the kill.' This is what I had forecast in 2005, and I think it is happening now.

And they may get it, the kill, one way or the other.

The sentiment has become decidedly bearish, and we now have six down days in a row on Wall Street, something not seen since February 2009.

One might look for a technical bounce somewhere around here, but it may take something from the Fed or Washington to turn the market around.

Here is my rough translation of the original Feri stuft die Bonität der USA herab.

"Man muss manchmal in den sauren Apfel beißen."

The Banks must be restrained, and the financial system reformed, with balance restored to the economy, before there can be any sustained recovery.

Feri Downgrades the Creditworthiness of the United States

By Harald Weygand

Wednesday, 06.08.2011, 08:56

Homburg, 8 June 2011 - The Bad Homburg €uro Feri Rating & Research AG downgraded the first credit rating agency's credit rating for the United States from AAA to AA. Feri analysts justify the downgrade by the continuing deterioration of the creditworthiness of the country due to high public debt, inadequate fiscal measures, and weaker growth prospects.

"The U.S. government has fought the effects of the financial market crisis primarily by an increase in government debt. We do not see thank that there is sufficient attention being paid to other measures, "said Dr. Tobias Schmidt, CEO of Feri Rating & Research AG €. "Our rating system shows a deterioration in economic health, so the downgrading of the credit ratings of U.S. is warranted."

For the third consecutive year the deficit of the United States is in double digit percentages relative to gross domestic product (GDP). "Deficits of such magnitude are not a sustainable fiscal policy. We would reconsider the rating when the U.S. government creates a long-term sustainable budget," said Schmidt.

Feri Rating is listed on the Federal Financial Supervisory Authority (BaFin) as an EU credit rating agency approved and created with more than 20 years experience in sovereign ratings. Every month, the Feri analysts evaluate sovereign credit ratings from the perspective of a foreign investor based on the ability and willingness of countries to repay their debts. The credit ratings have eleven possible gradations between "AAA" (best credit) and "Default".

About Feri Rating & Research AG

Feri Rating & Research AG is a leading European rating agency for analysis and evaluation of investment markets and products and one of the largest economic forecasting and research institutes. Currently, the company with about 50 employees and has approximately 1,000 customers in addition to its headquarters in Bad Homburg with offices in London, Paris and New York.

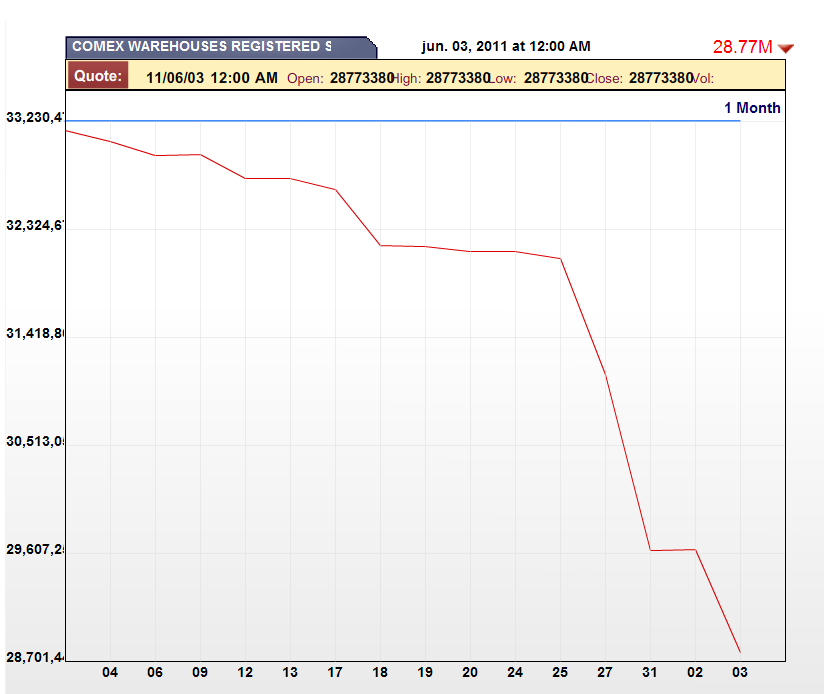

The ability of the Comex to deliver on the silver contracts continues to deteriorate.

Still running a long gold-short stocks pair. Added some silver long today, and doubled up the stock short, so the beta is leaning to the bearish side. I will adjust it tomorrow depending on how things look after the European close of trade.

The bullish case on these charts is for stocks to find a footing around the obvious support levels and create a slanted "W" double bottom with a nice summer rally back to the top of the channel trend resistance.

The bearish scenario involves a break of this support and a continuing decline into the Fed's decision on QE3 at the end of June.

Bernanke's waffling did not help stocks today.

I am still running the long gold-short stocks trade, but adjusted my beta and took the short position up a notch to a bearish lean.

The long gold - short stocks trade worked well today as stocks slumped yet again while gold held its own for a short gain on the bullion front.

The story is really in stocks, and whether they can hold key support levels, and not slip into a liquidation sell off.

Although the dollar crawled a little higher, there was no flight to safety into it.

Today we remember the Allied invasion of Normandy, a time when ordinary men and women did real, heroic things for the benefit of the many.

"Your task will not be an easy one. Your enemy is well trained, well equipped, and battle-hardened. ...The tide has turned. The free men of the world are marching together to victory. I have full confidence in your courage, devotion to duty, and skill in battle. We will accept nothing less than full victory. Good luck, and let us all beseech the blessings of Almighty God upon this great and noble undertaking."

General Dwight D. Eisenhower, 6 June 1944.

Another bad day for bully as stocks just could not hold any traction from the open.

We are approaching critical support levels for stocks. Much lower and we might begin a much more serious intermediate downtrend.

This is a subject that comes up periodically. Since the Fed's attorney recently answered Ron Paul's query, correctly I might add, that the Fed has no gold under its control, I thought I would reprise a previous blog entry on the subject of the US gold reserves.

The real question is not whether or not the Fed has any gold or direct control of it, which it does not, but rather, does the Fed have any knowledge of or any participation in gold swaps, leases or sales to foreign entities.

There is anecdotal information and plenty of stonewalling by the Fed to suggest that the answer to this question is not a straightforward 'no.'

Intra-day commentary was given here regarding the Jobs Report and the Credibility Trap that impedes a genuine recovery. Well, in addition to the rampant fraud that still infects the US financial system.

The long gold-short stocks trade worked again today, and the switch from the financial sector to a short on the broad equity index worked well.

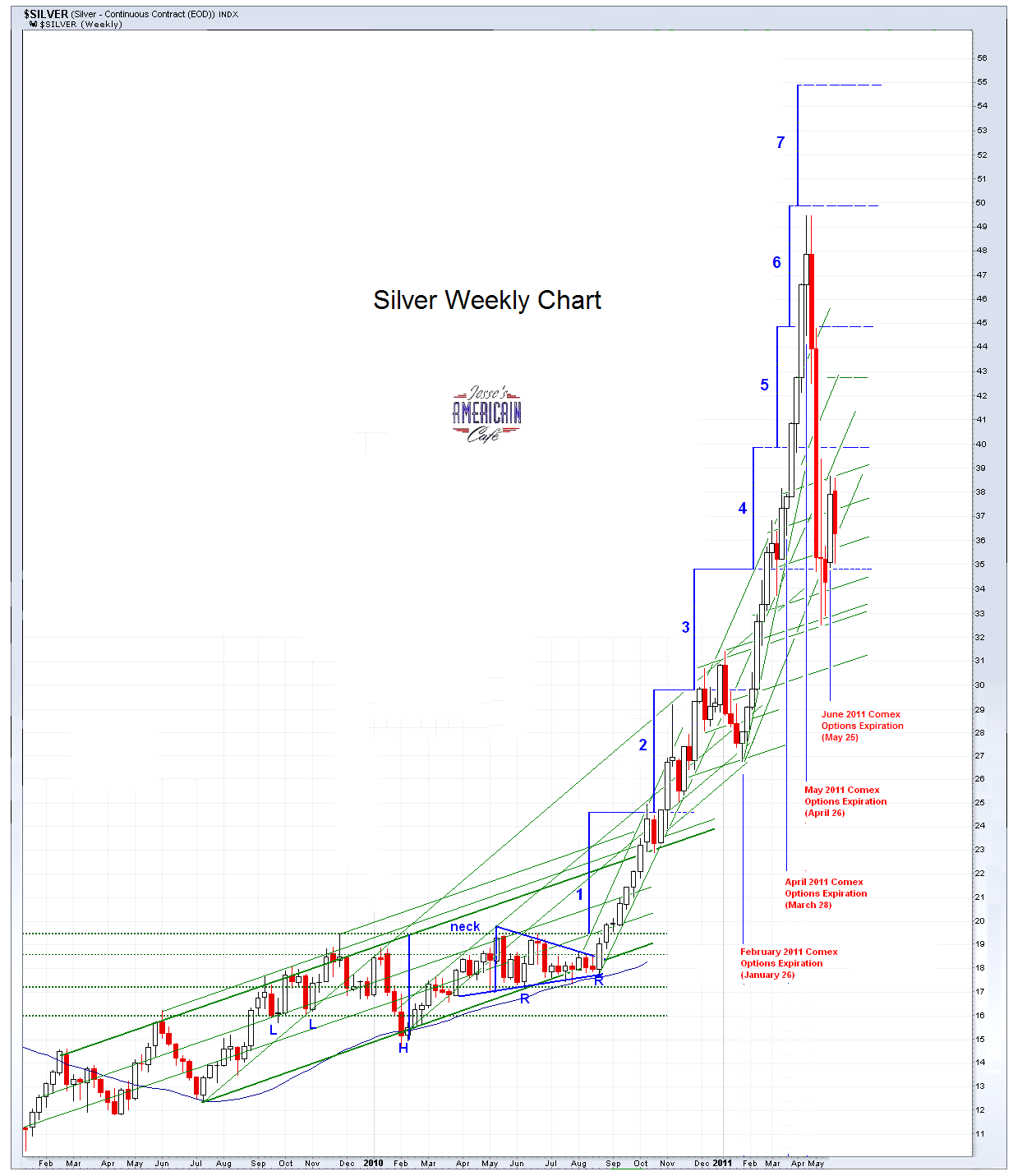

Silver is showing some weakness here based on its industrial component. That at some point will not matter if the Comex really does default on its silver contracts based on a shortage of real bullion.

I thought the dollar weakness today was remarkable especially considering the bid that the bonds caught.

Big things are happening. This sometimes seems like watching a tsunami approaching in slow motion, while most of the people are still playing on the beach, without a clue as to what is coming for them.

"Just as it was in the days of Noah, so also will it be in the days of the Son of Man. People were eating, drinking, marrying and being given in marriage up to the day Noah entered the ark. Then the flood came and destroyed them, sweeping them all away." Luke 17:26-28

A dismal Jobs Report, despite some attempts to paint a happy face on the numbers, brought US equities to another weekly decline and new lows for this short term trend.

This is the target area I had set for a low on the SP 500 futures if this is just a correction and not the start of a new bear trend. So we will see what happens next week.

There were some 'screaming headines' at some blogs this morning about the BLS Birth Death Model, aka the 'imaginary jobs report, reaching some new heights, or lows if you will, of perfidy in misstating jobs growth with a reading of 206,000 imaginary jobs added.

In fact the number was in line if not historically a bit low for a May adjustment. It showed the type of seasonal hiring one might expect for the beginning of summer.

The seasonality factor was also very much in line.

I give the government very little credit on its statistical reporting, and have been a strong critic for many years, and take a back seat on debunking Washingon to no one. But there was nothing particularly unusual in this month's report from a statistical reporting standpoint.

It was bad enough on its own. The recovery has never really gained any organic traction and for reasons that I have cited repeatedly.

I have deseasonalized and backed out the imaginary jobs for each month, and posted what the monthly jobs number would look like without them as shown below. It's a choppy picture even with the seasonality factor to provide some smoothing.

This is why it is advisable to watch a moving nine month average. And I also greatly prefer to watch the changes in median wage, which is probably as much or more important than the actual jobs added. The recovery will not become organic and sustainable until people receive a living wage, able to buy a lifestyle consistent with a democratic republic based on their labor without onerous rents from debt.

This is not economic theory; this is simple common sense. If you want to have a consumer based economy, you cannot debilitate the consumers until they become serfs, because they one has obtained a different form of governance. Unless of course one can persuade the many to love their servitude and think hell a heaven.

The public policy argument revolves around the relationship between the distribution of power, and therefore the accumulation of economic power, as it always does throughout history. That is another matter. I am treating the economic argument and prognosis.

As for employment growth, the longer term 'trend' has not yet turned lower, and seems consistent with a stagflationary outlook. It is obviously in danger of rolling over, but it has not done so just yet.

America had been adding jobs for over twenty years with stagnant wage growth. And this was a result of the partnership between corporate America and the wealthy few with the government policy makers, especially including the Greenspan Federal Reserve. Warren Buffett called it a class war and there is no need to guess which class controls the discussion through the concentration of ownership in the mainstream media. The public cannot even mount a serious reform effort without it being quickly co-opted and used against their interests by a well-heeled propaganda machine.

As Simon Johnson famously observed, there was an economic coup d'etat in the States and it is still having its way with the public and much of the world at large. The financiers have breached the walls, and are sacking and looting the city. Neo-liberalism is little more than a resurgence of the corporatism of the earlier twentieth century, with the jackboots more selectively deployed overseas, at least for now.

And the global reaction against the Anglo-American banking cartel, and their infamous economic hitmen, is the substance of the ongoing currency war, the long standing struggle against colonialism. It is remarkable how with all the change, nothing of substance really changes, at least in regards to human behaviour.

A structural reform of the system is what is required, not short term stimulus or austerity at least for now. And in particular not austerity or more tax cuts for the wealthy which is the hallmark of an intellectually bankrupt theory.

The US economy is severely distorted after years of managerial abuse with an outsized financial sector and a bias towards domestic jobs destruction through an abandonment of long term public policy decisions and investments in favor of short term corporate profits and the public be damned.

And there is no reform because the political administration of the system and those who observe and report on it has been generally captured and corrupted, and is stuck in a credibility trap.

Intraday commentary here: Shenanigans as Moody's Warns on US Rating.

I thought it was rather cute when Adam Johnson of Bloomberg pointed to the weaker price of gold this afternoon as proof that the Moody's warning on US credit rating is no big deal. Perception management at its finest, and most obvious.

At the same time the dollar was rolling over hard, but no one seemed to notice.

Goldman Sachs received a subpoena from the Manhattan DA, and the financial sector was pulling down stocks after yesterday's big sell off.

The equity market is looking for a reason to rally from support here. Groupon has an IPO ready to launch and the Street likes to welcome them in steady markets. Let's see if the Non-Farm Payrolls report gives them anything to cheer tomorrow.

I did take off the Financial Sector short today and yesterday from my own portfolio, and added unleveraged gold and silver holdings on the intraday smackdown today.

I do have an open mind about a meltdown in the US financial markets, but the timing seems a bit early for now, unless there is an exogenous shock.

Let's see what happens.

The big news today was the downgrades in the financial sector, with Moody's warning on three of the TBTF banks, Citi, Wells and Bank of America.

Moody's also warned the US on its sovereign credit rating, if the debt ceiling issue is not resolved.

Groupon is bringing out its IPO, giving the Street about 750 million plus reasons to support the market for the near term, and the NDX diverged today from the financially heavy SP 500. Will investors learn from their recent LinkedIn experience? If so, it could send the market and the banks into a swoon.

Non-farm payrolls tomorrow. Look for a relief rally on anything over 100,000 jobs added, and further weakness on much below that.

My suspicion is that the Wall Street wiseguys will continue to run their bluffs and play with the world markets up until the weekend over which they will fold their cards and collapse, as this did with the bankruptcy of Lehman Brothers and the beginning of the great financial crisis. The great currency crisis will be no different.

And no one will understand how it could have happened. Congress will engage in well staged histrionics, and the regulators and economists will hide in their offices.

The three big US banks, Wells, BoA, and Citi, which have just been downgraded by Moodys, may be cut down in size.

But saving JPM, the Fed's house bank, will be put forward as a national priority. And as for Goldman, well, they know where more bodies are buried than a cemetary caretaker.

Moody's also warned on the credit rating of the US today, and the metals were hit by brutal bear raids, even while the dollar slumped. Draw whatever conclusions which you may, but it looked like an exercise in perception management from here.

It is a small point, but the drop cited in the last sentence in the piece below is incorrect. The Comex deliverable inventory was at 41 million ounces on April 18, and not two weeks ago.

The real story here is that the silver bullion market for real, available metal is very tight. The Comex needs to find a large supply of silver, unemcumbered and in suitable condition, to satisfy its contracts.

Wall Street's usual response to a crisis of this sort is to try and bluff their way out of it, and look for help from the regulators and government officials. When they run out of options, they settle out of court and pay a nominally large, but in reality token fine as a cost of doing business.

I cannot tell if there is a real story behind the 'reclassification' of the Scotia Mocata inventory, or if it is just customers pulling their inventory out of the deliverable category at one of Canada's major bullion banks. I am waiting to see if Harvey Organ has anything to say about this, since it was he and his son who first exposed the inventory problems there a few years ago, problems that were subsequently corrected.

Whatever the details, there is a growing problem at the Comex in terms of the product that provides the basis for their derivatives, the silver future contracts.

The decline in inventory will be resolved. This can be accomplished in one of three ways: a collapse in the silver market triggered by a collapse in the US economy, much higher prices which persuade holders of bullion to part with it, or a declaration of force majeure and a default on delivery of bullion in favor of other paper derivatives.

Much less likely would be a government intervention to save its friends in the Wall Street banks. If the Obama Administration invokes any sort of executive power to control the markets I expect massive civil disobedience from the public through the summer. Much more likely is a resolution cited above and a cover up. This is what they have been doing since 1990 at least.

As an aside, Goldman was served with subpoenas this morning by the Manhattan District Attorney's office as a follow up to the Levin Report on their role in the fraud and corruption surrounding the financial crisis.

There may be a bull market in Congressional hearings and subpoenas coming. The scandal reaches to the highest offices in the US government and financial establishment. Therefore the truth may never be revealed. But a reckoning is coming.

From Goldcore:

"The supply situation in the silver market gets more interesting by the day.

Registered COMEX silver inventories have fallen to multiyear lows at 29,631,268 ounces. In the last 5 days they fell from 32,132,903 ounces to Tuesday’s holdings of 29,631,268 ounces. As can be seen in the table below registered silver inventories fell every single day last week leading to a sharp fall of 8.4% in 5 days.

Registered metals are those metals which meet the standards for delivery under the silver futures contracts and for which a receipt from an Exchange-approved depository or warehouse has been issued. Eligible metals are those which meet the delivery standards as stated in the rules for which no receipt from an Exchange-approved warehouse has been issued.

This is a long term trend that has been seen since the early 1990s when total COMEX silver stockpiles were over 101.45 million ounces.

However, the scale of the drop in inventories since early 2008 is significant and the trend has accelerated in recent weeks.

Registered silver inventories are down a sharp 38.5% in just two weeks – from 41,044,280 to 29,631,268."

There was a general sell off in stocks the day after the end of month tape painting driven largely by very negative economic data. Friday is the Non-Farm Payrolls with a consensus that has been around 170,000. ADP came in very short this morning so the market became tense.

Initially silver held up fairly well and gold even rallied on a flight to safety, but a concerted bear raid took the price down back down again. Silver in particular took a calculated late day short at driving the price lower.

There was some general intraday commentary here on the coming break in confidence in the US markets and a likely drop in the US dollar if foreign holders experience revulsion at the corruption of the management and reporting of the currency.

“There is definitely going to be another financial crisis around the corner because we haven’t solved any of the things that caused the previous crisis. Are the derivatives regulated? No. Are you still getting growth in derivatives? Yes.”

Mark Mobius, Bloomberg

More bear raids today but they failed to detract from the flight to safety into gold as the precious metal significantly diverged from stocks, at least for today. Silver, being more correlated with industrial activity, felt the slump in stocks a bit harder.

Although the stock market decline is steep, and tied to bad economic results which were ignored during the month end paint job, it does have the smell of a wash and rinse within the trend channel, on manageably light volumes. This magic lantern show and churning is how the big trading desks make their money and their nearly perfect trading records. An intraday chart of the SP futures are below.

Let's see if the key support around 1300 holds if we get that far. For a trader this somewhat predictable volatility is like a steady paycheck, but for the average person it can be a source of understandable anxiety and confusion, which themselves are the currency of fraud.

I would like to make a brief comment to clarify my understanding of the premiums to NAV in closed end funds.

The premiums do not indicate that one trust or fund is better than another. I use them rather to select entry and exit points for that particular fund.

There are differences among the funds, and that is a data point of information about the market. PSLV has a reasonably good redemption policy on actual physical silver, and it therefore commands a higher premium to NAV than funds which do not have a reasonable redemption policy AND a high confidence level that the silver is actually there for the taking.

Based on all the data, there seems to be a strong indication that there is a widening gap between 'paper silver' derivatives and obligations and the physical bullion market. The wider that gap becomes, the greater the noise the market will make when the value at market and price discovery is free to operate.

In other words, the Comex looks as though it is heading towards a very severe market dislocation. When and if it does happen the pundits and players will feign surprise, and then some of the naysayers will become 'I told you so's.' But most of them will just climb under a rock somewhere and wait for another opportunity to emerge with the inevitable ups and downs of markets.

What we can expect now is even more volatility and increasingly blatant attempts to save the big players who are trapped, especially those too interconnected to fail. This failure of the markets is a result of the corrupting partnership between government and large corporations based on personal greed and amoral expediency.

I am now starting to wonder if this event will be associated with a failure in confidence in the dollar, and some sort of exchange or bank holiday. The timing of any event such as this is problematic for a variety of reasons having to do with lack of transparency and regulatory failure. A major break in the markets and a liquidation of assets could significantly set it back and delay it.

But the Comex deliverable inventory represents a sort of a visible indicator, if not a countdown, of how difficult the situation is becoming to manage.

If those in a position of authority wished to quietly debase the national currency without alarming creditors or the public, they could hardly do better than to surrepititiously promote theories that made people believe that bad times and money printing would make the currency stronger, despite all historical evidence, even to the point that they would disbelieve their own observations of higher prices and a dwindling savings, until it was too late, and the crony capitalists had secured most of the valuable and enduring assets favored by the independent judgement of people outside the system.

Even better if it prepares the many to welcome the strong hand of an autocrat government that is prepared to 'do something' to make their dream worlds come true, no matter the prices paid in freedom and fresh injustice and corruption.

This is the darker, the less probable side of what I am seeing and my interpretation of it, and so I would hope that it is wrong. More likely the jokers in charge will try and muddle through until external events force they hand, and then pain begins to be handle out in even larger portion according to some formula yet to be determined.

I do think that much of the current political discussion in Washington and New York (and probably London as well) revolves around the shaping of that formula for the distribution of pain. The monied interests wish to hand the public, and most likely the world at large, a shit sandwich, and compel them not only to eat it, but to pay dearly for the privilege as well. Whether or not they can accomplish this is another matter. But they are giving it a good try.

Let us therefore allow the market to reveal all its secrets to us in good time, and trade it according not to what we think could happen, but what is actually happening as we can best understand it. The key to success in this is knowledge, experience, and above all, humility.