“One day, we will have to stand before the God of history. And we will talk in terms of things we've done. And its seems to me that I can hear the God of history saying, 'That was not enough. For I was hungry, and you fed me not. I was naked, and you clothed me not. I was devoid of a decent sanitary house to live in, and you provided no shelter for me. And consequently, you cannot enter the kingdom of greatness.'" Martin Luther King

Showing posts with label gold flowing from West to East. Show all posts

Showing posts with label gold flowing from West to East. Show all posts

I found it interesting that in yesterday's Comex delivery report, Nova Scotia took delivery of 43 x 5000 ounces contracts, about 215,000 ounces of silver bullion, for their 'house account,' at the price of 14.08. I include that particular CME report below.

Apparently the Central Gold Trust has proposed a conversion of the Trust into an ETF, rather than accept the acquisition offer from Sprott. You may read that proposal as a PDF document.

The Sprott Funds are mildly negative in price to their NAV, which is the 'new normal' in this bear market leg in precious metals.

What is not so normal, at least in my recollection, is the deepening negative cash balance which I have estimated for Sprott Silver at a little over $430,000. And from the low level of cash in its account it looks like Sprott Gold is going to be following them soon, unless provisions are made to raise cash.

As you may recall, the Sprott underwriter Morgan Stanley gets a 4% cut on new offers of units, which has been the usual way in which Sprott has raised funds. With the premiums close to negative, they cannot execute such an offering without 'diluting' the value of the fund in that offering, which they have pledged in their prospectus that they will not do.

So it appears that selling bullion is the only way to raise the required funds. I have this from third parties, but Sprott has never said anything otherwise or objected to this interpretation.

Another interesting factor in the Sprott funds is the redeemability feature. Although it has not happened with silver, there have been a number of redemptions of gold bullion out of the Sprott gold Trust over the past couple of years. That is a good thing, that the process works, and that one might obtain their physical gold for private safekeeping.

But one might wonder what would happen if there was a 'run on physical gold' as some conjecture might occur, given the divergence in pricing between paper and physical. According to an informal source, there is no provision in the funds to block, slow down, or attempt to prevent any redemption of the gold or declare force majeure. The counterbalance for this is, of course, the market. In order to redeem bullion, one must buy the units in the market at a certain price. And if someone started buying up the Trust units in size, the price of those units would probably adjust to an increasing positive premium which would mitigate the attractiveness of a mass redemption. And in the case of a 'run on bullion' I would imagine that holders of units would refuse to sell. But nibbling at the bullion, as it is on almost all Western gold funds, has occurred.

I include the 'Total Holdings' of the Funds and ETFs for gold below to show the decline in bullion inventory. And to pre-emptively respond to the misinformation of the bullion banks' gold trolls, who like to claim that this rise and fall in gold inventory is merely a matter of price, I include the same time periods for silver bullion as well. Nine out of ten investors might notice that silver has had a steep decline in price from its all time highs as well.

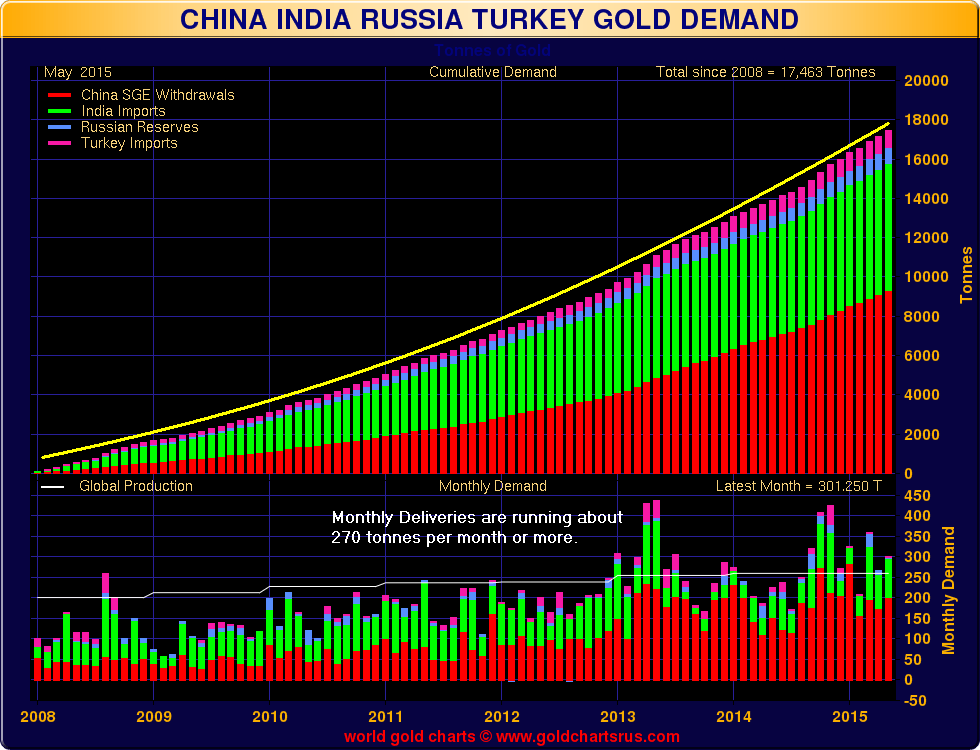

One cannot take a single data point alone, and even a cursory examination of the bullion flows globally shows a massive movement of gold bullion from West to East, with some significant declines in the 'free float' of gold in some traditionally strong Western markets, such as London for example.

And the outflows from the Asian markets into strong hands on the mainland and the Western exports to them have been absolutely astonishing. That the financial media and analysts ignore this, with some even denying it overtly, is shocking I suppose, unless you have been paying close attention to some of their more egregious service to the speculative financial interests for the last fifteen years.

By way of disclosure I own no shares in any of these Funds and ETFs at this time, and receive no money or gratuities from any of the funds which I discuss. I have owned all of them from time to time. I have owned most of the mining stocks from time to time, except for the more obscure 'juniors.' I do not prefer one over the other so much as each has its place and use in a portfolio.

As I have indicated recently I am cash heavy for the moment in my short term trading, waiting for the market to provide some additional information to prompt some action. This is normal now because I am no longer a very active trader. That is a younger man's game. I prefer to take more intermediate term positions and in size.

"People of privilege will always risk their complete destruction rather than surrender any material part of their advantage."

John Kenneth Galbraith, Age of Uncertainty

This is a response to Mr. Krugman's recent column as it was featured at Economist's View titled, Republican Lust for Gold

I am not in favor of a return to a gold standard.

I am a reasonably well-educated, politically progressive professional, a likely supporter of Bernie Sanders as an economic reformer and an opponent of endless war, and certainly not the 'Wall Street Democrats.' I believe that the current 'debate' over the place of gold in the economy is breaking along ideological lines to the point of a religious fervor and intellectual blindness, on both sides.

I think of gold as an alternative store of wealth, which without any sanctions from the state pro or con can serve a very useful purpose. It gives people a 'choice.' It can act as a barometer of sentiment. And it serves a purpose, especially in times of pervasive fraud in the financial asset markets, as an asset without mispriced or even hidden counterparty risk if held directly.

And if you think that the problem of pervasive fraud has been fixed you are sorely mistaken.

If a system cannot stand the criticism offered by something which it cannot and probably ought not to control, then perhaps the fault is in the system, and not in the critics.

And while we are on the topic, what by any stretch of the imagination do you subscribe the issue of 'gold' to the Republican establishment? Who shut the gold window in 1971? One of the few things that Chairman Greenspan said is that statists from both sides of the aisle despise and fear gold because it constrains them in their quest for discretionary power. And he was right.

The current 'stimulus' is a massive failure because it has been trying to save a broken and largely unreformed financial system, rather than provide stimulus and support to the vast majority of the participants. It is the consequence of placing the highest priority in means and methods, because they are 'ours.' Our method, our model. First and foremost. Because we fear for our credibility.

And so the participants who are complicit in the fraud and those who are invested politically in the models and methods both become ensnared in a 'credibility trap,' and what Mike Lofgren has called 'the anti-knowledge of the elite.'

Unfortunately, Gresham's law is still works. Gold, and to a lesser extent silver, are flowing 'en masse' to Asia in almost astonishing numbers of tonnes each month. The numbers are there, little publicized and noted in the prestige media, but almost shocking. It has not yet made its way fully into official reporting mechanisms, even so called 'industry organs.'

Mr. Krugman, nine out of ten Americans will notice that the vast peoples of Asia and the Mideast are not 'Republicans.' The central banks of the world are hardly 'Republicans,' but they became net buyers of gold around 2007.

No, they are not the easily mocked Republicans.

But they are looking for a safe alternative to a monetary and financial system that is going off the rails, again. The modern hypothesis that all money is purely arbitrary is only feasible if one has the ability to make their purely arbitrary valuations stick. That is the Faustian bargain with the will to power, the endless war of the monetary relativists.

Would we make enemies of the whole world for the sake of a corrupt and unsustainable financial system? Alas, some would, and are doing so even now.

As I am sure you know, once a force like Gresham's Law goes into effect, which it already has, it can quickly turn into a torrent of consequences. Will we continue to argue until that event is upon us, as we did with the prevalent fraud in the housing bubble that was created by the same perpetrators who have continued to rig markets even until today?

The dogmatic modelist and political hack sees China and India and other nations buying gold and says, 'We must stop this! Control it!' The thinker sees a sea change in the monetary markets and says, 'we must understand why this is happening, and what we may be doing to provoke it. And if we are doing something wrong, then correct it.'

No I do not support the gold standard, not at all. It would be entirely inappropriate for a patient still in the ICU to be prescribed a regime of hard exercise and strict diet. And the corruption in this system is capable of corrupting anything, even an external standard.

Given the proper regulation, transparency, and judgement, a paper currency can emulate the steadiness of a gold standard while allowing for more latitude in times of distress. Do you really believe that we have held to that prescription with our serial bubbles, frauds and crises?

But I do feel quite strongly that the current policy of constant market intervention in the West, which is obviously happening to anyone who is capable and experienced in watching trade patterns, is going to tear a hole in the facade that this sick series of policy errors is becoming.

If one takes even a cursory look at the trade flows of gold, one can see that the flows into Asia and the Mideast are relentless, and growing. And the decline of 'free float' in the UK and US in particular is striking. The numbers are difficult to discover, but some have taken on that task.

The leverage and shuffling of free bullion around to dull the interest in leverage is approaching 300 to 1 in NYC and 200 to 1 in the 'physical' LBMA market in London is the kind of obvious error that one looks back at from the wreckage and says, 'What were they thinking?'

We made a mistake. A big one. We have tolerated a farcically ineffective program of 'reform' and a massive top down stimulus focused on the 'system' with an austerity for the public that is going to rip a tear in the social fabric which will take years, and a significant amount of pain, to mend.

It is going to happen, no matter what models or arguments you may wish to stick your head in. I am not trying to argue a point. I am trying to encourage people to at least look at what is happening, and to stop comforting themselves with obviously faulty numbers and metrics from a system that has stopped serving most participants in favor of a powerful few.

This is going to end badly. I was more demure when we had similar discussions here like this prior to the housing bubble collapse. 'And no one could have seen it coming.' Because their eyes were closed and they comforted themselves with what they wanted to hear.

There is, at some point, going to be a dislocation in the international currency and bond markets. And it will be noticeable, unless we change our ways and embrace honesty, transparency, broader equity, and reform.

It will not come from the political process, because that has also been broken by the power of big money. That has become so painfully obvious that the only way to continue to justify it is to declare corporations to be 'people' and bribery to be 'free speech.'

People may think of themselves as 'Keynesians,' and what the 'other side' thinks about Keynes is admittedly mostly an ideologically tainted caricature. But first and foremost what made Keynes effective was his practical focus on the desired results and not to a preconceived model which crushes out the better part of reality in its understandable and unfortunate inadequacy that is common to all 'models.' Keynes was an independent thinker who was confident enough to occasionally change his mind without worrying overmuch about his credibility, and not an acolyte of some constraining school of thought made dogma.

No, rather than a 'gold standard' now I think gold should stand alone, and be allowed to speak whatever truths it may. As for any use of it by nations, let them make what use of it as they wish. It is a tool. But once they make it 'official' they cannot seem to keep from trying to cage it, and control it. But by then it is merely collateral damage of a growing corruption and fraud of finance, rarely without an accomplice in monetary economics.

At some point the thought leaders will have to rise above their own political enthusiasms and personal aspirations and begin to honestly and openly address what is going wrong. And then perhaps we may begin to push for the return of some of the basic principles hammered out in the 'New Deal' which we so foolishly allowed to be weakened and then overthrown in the 1990s, and even until now.

And, Mr. Krugman, that was a decidedly bipartisan effort. And the players and their enablers who brought us that misery are still active, unabashedly, in the highest circles of power.

The gold pool is expressing some interesting dynamics that appear to be winding towards a denouement of sorts.

The current trajectory could change if the price is allowed to rise to clear the market, or any number of other seemingly improbable events.

The silver market is also acting very oddly. I have not gotten a real handle on that, other than soaring premiums for coins and a lack of serioius buying in the US compared to the rest of the world. Similar to gold in some ways, although the central banks have no stockpiles of silver with which to rescue the bullion banks, again.

It is funny but few seem to notice these things, or even care, for whatever reasons that people do not notice something until it is too late to do anything meaningful.

I think that sometimes we can become 'victims of the ordinary.' When the same thing happens again and again, we expect the same thing to happen next, and any change from this pattern seems almost unimaginable.

"My main focus is to try to bring into context the size of the "London Float" out of the shadows and into the light of day. The London Float being the working supply of gold available to meet the markets daily needs.

One must treat this with the consideration that much of the known gold shown is already owned & not available to meet the markets needs - not unless the owner wants to sell. The presumption being that the Central Banks reserves are not available to the market. They do lease/swap but under their own intent and of late the trend has been to not lend in risky markets but rather to claw back physical into direct ownership.

The years around 2000 were when the Mine Hedge Book was most active with approx 3200 tonnes being lent into the markets by the Central Banks. By 2007 much of the Hedge Book had been closed out & they were under 1000 tonnes falling under 100 tonnes by 2013. From 2011 gold repatriations of Central Bank reserves started & since then have only grown.

So one presumption from this study is that over time the stance of the Central Banks has been to reduce their lending and bring their gold closer to home. Hence the presumption that the gold held in the Bank of England is mostly all there, unencumbered and released from leasing and swaps. Obviously some will still be lent out but the presumption is that the tonnages lent out are far smaller than in the past...

The UK Imports approx 602 tonnes per year & exports approx 388 tonnes per year (since 1999) according to the EuroStats database (thanks kindly Koos). However with the recent gold demand from Asia these statistics have changed dramatically. Since the start of 2011 the UK has imported 2982 tonnes & exported 3998 tonnes with net exports of 1016 tonnes seeing exports double their normal average to 800 tonnes per year.

This leaves the London Vaults with a FLOAT of between 1361 tonnes and 200 tonnes with the probability that it is closer to the lower number. If it is closer to 200 tonnes then London does have a problem as a FLOAT of this size is not enough to cover their flows for 4 months."

It is reasonable to estimate that London, in all the vaults, has only about 900 to 250 tonnes of gold available for physical delivery, which is a shockingly low figure given the current demand from 'The Silk Road' nations alone that is running about 1,700 tonnes per year. And even that 250 number is questionably high, depending on the status of the gold in the Bank of England.

The objective is to attempt to determine how much available physical gold for delivery can be wrung out of London and New York, in excess of what can be had from scrap, minining and leasing. We are calling that 'the gold float,' and it is feeding the demand for bullion in Asia. At that point we might estimate when the pressure on price becomes irresistible.

We are thinking months, not years, at least with things as they are.

I wish to acknowledge up front the debt that is owed to Ronan Manly and Nick Laird especially for the data contained herein, as well as Koos Jansen for his ground breaking work in estimating Asian gold demand, and Bron Sucheki for his participation.. I have listed some of the pertinent published articles below.

It is regretful that one can only provide estimates. But that is the nature of this beast that operates with secrecy of supply and distortion of actual demand.

What manner of business is this to enable price discovery in a public market, by covering so many fundamentals with secrecy? Where is the mining community in all this?

The LBMA is said by those who are in a position to know these things to be running 90:1 or more leverage to each of its unallocated ounces of gold, which according to Jim Rickards is all of them.

The potential claims per deliverable ounce at the Comex right now is at an historic nosebleed high by of about 255:1, supposedly because the owners which to avoid a 'short squeeze' in bullion, although the party who said this did not say 'where.' London probably, maybe Switzerland.

Peter Hambro says that "there is not enough physical about. There are endless promises."

In a nutshell, we now know that physical gold for global delivery, of which the London vaults are a major supplier, are rather tight, especially given the increasing demand for physical bullion in the East.

There is plenty of room for questioning the numbers and casting doubt on them, while hiding behind a curtain of exchange secrecy. One might suppose that the gold bullion bank apologists will be hard at it soon enough again.

They too often do not help to advance the understanding of the public, preferring to selectively twist the data to say 'all is well.' They deride the supply problems that people in the industry are encountering, always saying they are not real. And they like to include all the gold that exists in the warehouses for their calculations, whether someone else already owns it and is clearly not interested in selling at these prices.

More details would be useful, because if we could obtain a better idea on the extent of central bank leasing, we would be better able to estimate the risks and the relative fragility in the highly leveraged and hypothecated supply of gold in New York and London.

One would think from the known data that the unallocated gold in London is counter-claimed many times, and even the allocated and custodial gold is likely to have multiple claims upon it. So the actual 'gold float' is probably quite a bit less than 1,361 tonnes. Each of us has our own favorite ballpark number ranging from 900 to 250 tonnes and less, not fully accounting for leases and leverage on the remaining stock.

Nick Laird had a secondary outlier estimate which he expressed in colloquial Australian, which I dare not repeat here. But it was quite low. lol. Maybe four months worth of float left.

And it would certainly be nice to have more information about silver, especially since to my knowledge the central banks have dealt their own supply away some years ago and there are quite a few indications of tightness of supply, although not in the Comex yet.

I do consider this analysis to be a work in progress, Nick Laird and Ronan Manly are the key data organizers I believe, with help from Koos Jansen and Bron Suchecki, and the odd bit from Jesse the consulting detective. So I would look to their sites for explication of their methods and sources. Ronan Manly in particular is a public source and he goes into quite a bit of detail.

Given the struggle it has been to obtain the data, and the refusal of central bank personnel to discuss their own supplies on orders from above, there may surely be gaps and errors in this, but not for lack of effort.

If I have any major concern it is that the management, the exchanges and the regulators, will allow the traders to sleep walk themselves into a rather serious situation. And don't we know how little self-restraint these traders have been showing.

The remedy for this situation is not even more leverage, or more hypothecation of the unallocated stock, or even more leasing by the central banks, or more programs in India to dampen demand.

The longer they allow this price rigging and leveraging up, the slower productive mines will come on line, and the worse the tightness on the remaining physical supply will become. But as they say in New York and London, 'nothing is broken yet.'

The market solution for this tightness of supply is HIGHER PRICES and not increasingly ludicrous jawboning, spin, and bear raids.

And if higher prices might inconvenience the policy and perception management aspirations of the Wall Street financiers, their enablers and associated hirelings, well then too bad. Try to behave more responsibly, and stop attempting to make the rest of the world pay for your excessive gambling losses and poor judgement.

Here are a few additional charts from Nick Laird's site at goldchartsrus.com to break out a bit more detail and to provide some context for the estimated physical supply compared to physical demand.

"Nor can private counterparties restrict supplies of gold, another commodity whose derivatives are often traded over-the-counter, where central banks stand ready to lease gold in increasing quantities should the price rise."

Alan Greenspan, Testimony Before the Committee on Banking and Financial Services, U.S. House of Representatives July 24, 1998

"Secrecy is completely inadequate for democracy, but totally appropriate for tyranny."

Malcolm Fraser

We are going to have an option expiration on the Comex on this Thursday the 24th. I am not expecting it to be a big event, since October is a light contract, with the real attention and action being concentrated in December.

However, there are over one thousand puts at the 1125 strike, so the cynical me might call that good support.

If I were trying to skin the specs and holders of options with shallower pockets, I would take gold down to about 1120ish, suck in more puts and scare the calls out, and then take the price up and skin all those put holders at expiry.

But this is a one dimensional view of the market, and does not take into account the trade in London and in the vastly out of control derivatives markets. Or the side action in the miners and ETFs for that matter.

There were no (zero) deliveries for gold and silver at The Bucket Shop yesterday.

The slow bleed out of the bullion warehouses continues.

I recall some fellow, I think it was from Barclays, saying that the record low plunge in deliverable (registered) gold bullion at the Comex was because those who owned it did not wish to see it stopped out 'in a short squeeze.'

And I remember thinking at the time, what short squeeze is he referring to? The non-delivery Bucket Shop?

And then the rumours regarding the shortage of delivery ready bullion at the LBMA came out, Peter Hambro said it was 'almost impossible to find,' and a few analysts noticed that the gold is in backwardation, meaning a premium is being paid for real gold in hand.

And then Rickards said that he thought a couple of Banks were in a pinch on delivery in London and were hedging their exposure in the futures in New York. As he noted, London is a 'fractional reserve' system, as is The Bucket Shop with a stated assumption of 2% redemptions, as are some unallocated depositories.

If this game of musical gold gets dodgy, it could begin to fall apart as fast as MF Global swirled down drain. I would not wish to see that. I would greatly prefer honest markets that are not so recklessly fragile, in which the small investors is not exposed to so much unknown counterparty risk.

The Banks participating in the London fix are now Barclays, HSBC, SocGen, Bank of Nova Scotia, UBS, and Goldman Sachs.

The Banks which Rickards said were rumoured to be caught short physical deliveries and had been hedging on the Comex with longs are JPM and Citi.

I should note that Jim, for all his expertise and knowledge which I do not dispute, has been leaning in this direction before but certainly early. He suggested that there might be a run on gold back in 2010.

So here we are. They will never admit there is a problem with this, never. They will keep doubling down while the music is playing and if it stops, they will run to the Treasuries and the central banks for a rescue, while keeping their profits and bonuses.

In the absence of enforcement of the rules and effective regulation I am afraid that the only thing that will stop this nonsensical looting is a bullion brick in the face.

The price discovery mechanism in the precious metals market is to hide the true state of the supply behind a wall of secrecy, and to jawbone the demand lower by saying ridiculous things and befuddling the average investors.

But there it is. The flow of gold and silver, a massive exodus of wealth moving from West to East, covered up by a storm of paper.

And the peoples of Asia are letting the malarkey of the bullion Banks and their apologists just float by on the breeze, while they keep stacking the only financial asset without counterparty risk.

As a caution, even if it proves that the highly leveraged LBMA in London, being backed up by the incredibly over-leveraged Comex, is indeed in a developing short squeeze, as Greenspan reminded us, the central banks have gold which they can lease out to their friends in the Banks, so it can be sold off in Asia, with a promise to return it at some future date.

As Sir Eddie George said, they were 'staring at the abyss' if a failure to deliver were to occur, and prompt a run on available gold forcing an unwind of the paper house of cards.

That may keep the books balanced, but it really does not solve the problem, the systemic fraud that is going on in this as it has in so many other markets.

I get the impression that Asia is in this for the long haul, and will not be deterred.

“Our clients will call up saying ‘I hear the Comex is running out of gold, what do you make of it?’ and our quick answer is that this is a non-issue,” Jeffrey Christian, managing director at CPM Group, said in a telephone interview.

“Even if you look at the fact that registered stocks have declined, the fact of the matter is most Comex futures contracts” are cash-settled, and traders don’t take delivery of the metal, he said.

While the percentage of Comex gold open interest covered by total Comex reported stocks has fallen over the past year and a half, it “remains very high by historical standards and presents no perceptible risk of imminent problems with deliveries,” CPM Group said in a report dated Sept. 14...

Barclays Plc said in a report this week that emerging-market demand for gold has shifted some metal into Asia, and that “coverage of physical stocks in Comex remains solid.”

“Anything that has more upside than downside from random events (or certain shocks) is antifragile; the reverse is fragile.”

Nassim Taleb, Antifragile

Gold is anti-fragile. This is why it must be handled with care, and not with fragile systems. Gold is intractable to the kinds of manipulation by the financial system that can bend paper to its will. This is why they hate gold, and seek to paper over it with leverage and secrecy.

Above is a commentary on the physical bullion situation at the Comex as it was reported at Bloomberg News yesterday. The 'deriding', which means ridicule and contempt, is coming from CPM group's Jeff Christian, and from a report from Barclays.

The title of the article is a bit odd, because I have not see any 'theories' about this subject at least here, just presentations of the facts using exchange provided information. And as for deriding, it seems more like a sign of weakness and fear than solid reassurance. But that is just my own experience in seeing that sort of thing when someone points out a changing situation that could pose a problem.

One thing the story fails to make clear is that only registered gold is deemed deliverable to fulfill futures contracts. Yes, all the gold in all the warehouses could potentially satisfy demand, IF IT WAS UP FOR SALE. But it is not.

The total supplies at the Comex have as much to do with the current demand for bullion as all the automobiles in your neighborhood have on the price that you are going to pay tomorrow for a used car, eg. the calculation cannot include items that are not up for sale. Yes there are many cars that would satisfy your requirements. But only those that are for sale are available for you to drive home.

Jeff Christian says that "even if you look at the fact that registered stocks have declined..."

Yes, 'even if' you look at the heart of the argument, 'registered stocks have declined,' and that is quite the understatement of the facts.

Here is the history of 'registered gold bullion' on the Comex going back to 2001.

And of course if almost no one asks for any of the gold, then there is no problem. Yep.

This is the problem. For anything except speculating with paper the Comex is now significantly fragile, moreso than at any time it has been in the last twenty years at least.

Jeff goes on to say that "most Comex futures contracts” are cash-settled, and traders don’t take delivery of the metal,"

And that is correct. Here is the history of deliveries, ignoring any cash settlements, on the exchange.

As should be easy to see, the amount of gold bullion deliveries is declining quite a bit.

The Comex lacks the market discipline of delivery of the goods and restraint on the potential hypothecation of available supply. What is acting to hold leverage to some reasonable level other than 'nothing has broken yet.'

Let's take a quick look at the ratio of total contracts to registered gold, that is gold up for sale.

The Comex is a significant price discovery market for the global gold supply. The data shows that it has diverged significantly from the physical bullion markets primarily in Asia.

While the inventories at the Comex remain flat overall and declining sharply with regard to deliverable bullion, the physical deliveries of gold into India and China are increasing steadily.

And I hasten to remind everyone that gold is truly a global market.

Nick Laird at sharelynx.com has created chart that tracks the known physical gold demand for what he calls 'The Silk Road.'

Even though I do not expect a default at Comex, as I have said many times before, the point is that if there is even a mild problem in one of the physical markets in Asia or London, the Comex is price positioned for a market dislocation and potential fails to deliver bullion on request.

The deliverable gold is a little under 6 tonnes. But even if price were no object, the total gold held in private hands in all the Comex warehouses is about 6,716,000 troy ounces, or roughly 209 tonnes. That is all of it no matter who owns it or why.

Or less than one month's supply for the Silk Road countries.

Normally none of this *should* be problem, although one has to admit that according to historical norms the amount of deliverable gold is very thin by any measure. Why is this? Why are the better informed withdrawing their bullion from the deliverable category? I read that they are afraid of the bullion being caught in a 'short squeeze,' but the trader who said that did not specify a short squeeze where.

This week I learned from an interview with Jim Rickards that some very large bullion banks were said to be using the Comex gold futures to hedge shorts in bullion delivery markets in London, called the LBMA.

That kind of a hedge might work to guard against paper losses, but against a genuine fail to deliver in a physical market you can see that the immediate deliverables at these prices are about 6 tonnes, which is a rounding error on the Silk Road.

It's the fragility, always the fragility.

What if something that is not completely normal and expected happens? What if, instead of 2% of the contracts asking for delivery, a delivery short squeeze in London prompts 4 or 5 percent of the contract holders to attempt to exercise their contracts to receive physical bullion to cover their obligations elsewhere?

The fragility of such an arrangement is bothersome to anyone from outside who looks at it from a systems engineering perspective.

If some firms are using the Comex as a backup system for gold deliveries in London and points east, it is hardly equipped to take that role without a significant market dislocation in price.

If I was only working short term trades and would never mind a settlement in cash, then the Comex seems like a fine place to do the trade.

However, if my goal is to have a solid claim on physical bullion, even within some reasonable length of time measured in several months, it does not appear that the Comex is appropriate for that particular objective.

Do you see the potential problem here that is so blithely 'derided?'

I do not wish to alarm anyone. I am putting out the word because I do not think people understand the situation that has developed, over the past two years in particular, as shown by the potential claims per ounce.

Globally huge market with increasing demand, a market where the available inventories are exceptionally thin, and a price that is derived without a tight rein on leverage and the discipline of delivery. What could possibly go wrong?

The usual retort is 'it has not broken yet.' Yes, and in the light of our experience over the past ten years or so, some might find rather thin comfort in that. The important thing is for traders and investors to be fully informed, that they may use financial instrument in a manner that is appropriate to their objectives.

For example, using Comex as a backup for bullion positions on the LBMA might be fine, if you are not expecting to receive delivery of bullion that can be used to satisfy your obligations there.

The exchange might consider another look at their rules in the light of this unusual 'leverage' of potential claims to bullion, rather than count on price fixing all problems, and few standing for delivery, especially in a changing and very dynamic global market.

I do not have good visibility into the leverage and available inventories at the LBMA in London. If those are in any way similar to the Comex, then I would take some action fairly quickly to secure my ownership of bullion given the potential for a misstep that spins out of bounds.

If you hold an allocated receipt that is as 'good as gold?' Tell that to the investors who used MF Global, and found their holdings sorted out in court against a lawyered up megabank.

I do not know Jeff Christian or the fellow from Barclays. I am sure that they have good reasons for what they are saying and the advice they appear to be giving to their customers. I am sure they can all work out all their concerns and particular issues among themselves.

Objectives amongst customers do vary and it is the fiduciary duty of any advisor to help them make an appropriate choice. And I can see many uses for Comex positions that are entirely suitable for some. A short term trader for instance, who in merely placing wagers that he expects to settle for cash.

But as for this article in Bloomberg, it is a bit of a gloss, heavier on the deriding and short on information for readers to use in making their own informed decisions. 'Trust us' and 'nothing has broken yet' are, as I said previously, non-starters these days.

I have set forth only a few of the oddities that are becoming apparent in the gold market. There are quite a few more, including backwardation and tightness in the London physical market as noted by Peter Hambro and an analyst at Mitsubishi recently, and in articles by Koos Jansen and Ronan Manly.

How about the pivotal London market, is it 'well-supplied?' How well supplied is it? What is the potential impact on the Comex of a bullion shortfall at the LBMA?

Has there ever been a 'stress test' of what it would be like at the Comex if there were an afternoon failure to deliver physical bullion in London? Or are you assuming as your baseline that such a shortfall could never happen in any non-Comex market? Is the process at Comex for some event like that, besides halting the exchange and forcing cash settlements?

I do think that one can become so involved in a system, for so long a period, that when it changes, when the market dynamics start shifting, the old hands may be the last to notice the forest for all those familiar trees. That is why companies bring in quality teams to inspect their processes for soundness and failure points.

What could have possibly changed in the global gold market in the past few years. "Barclays Plc said in a report this week that emerging-market demand for gold has shifted some metal into Asia,"

How about this? Some shift. Some metal.

Here is what Kyle Bass recently had to say about the situation. Maybe you can 'deride' him. Then again, maybe not.

In the light of how the MF Global debacle was sorted out by the courts, and based on a growing body of circumstantial evidence and market indicators, if you are holding your gold bullion 'insurance' in the form of unallocated or opaque holdings, or a hypothecated paper claim in one of the major exchange trading warehouses, you may wish to take measures to safeguard your ownership claims without much delay.

I wrote something overnight, On the LBMA and Their Unallocated Holdings, in which I lay out the case, based on facts and some presumably informed speculation from Jim Rickards, that there is a serious physical shortfall in gold bullion developing that may not resolve as readily as it did in 1999, when the Bank of England presumably bailed out the trading houses.

Commodity backwardation is not all that unusual. But it is somewhat unusual in the precious metals. And in combination with a few other items, it seems worthy of note and some preventative measures.

Koos Jansen notes that gold is now in backwardation in both London and New York.

"Not often in financial markets is the future price of gold is lower than the spot price (live), but lately we’ve witnessed such an event in both the New York and London gold market. This is called backwardation, the opposite of contango.

What causes backwardation and will it increase the price of gold? In my opinion there are two possible scenarios: the market expects the gold price to fall in the future, or there is scarcity now."

Please note that I am not suggesting that you should rush out and take large long positions in gold with the maximum leverage, pile into penny miners hoping for a 'home run'.

I suppose that quite a few will miss this caution since it is not heralded with blaring headlines of imminent doom, but perhaps those who need to hear it will do so. And I am sure that the apologists and the paperati will find their usual ways to dismiss all this, and urge us to ignore all these odd doings in the warehouses. Such are the times.

And I am not ruling out a much larger development behind the scenes with regard to the international monetary regime, that is 'leaking out' from official sources to banking cronies who may act on it ahead of time. But I have no strong indications of that. The IMF seems incapable of resolving the developing monetary crisis because of Anglo-American intransigence.

This is a purely circumstantial case. As was the case that Harry Markopolos presented for years on Bernie Madoff. And it may be wrong, or it may be right and vastly understated. But I think that we have means, motive, and opportunity, and so one may advisably act with caution. And so I have discharged my conscience in not remaining silent while potential trouble looms and the denizens of the markets take care of themselves. It is not so easy a decision to make when you do not have sound evidence because of secrecy and misinformation. And I am sure many will take this, use it as their own, and wrap this in florid headlines and dire predictions of doom.

I suspect at this point that a price correction is still possible as a remedy, but I am not so optimistic to rule out a greater effort to cover it all up that will make things exponentially worse, in the manner of the London Whale and MF Global and LTCM and so many examples of reckless hubris.

There is quite a bit of official interest in bailing out these wanton rich boys from their gambling debts and assorted scrapes, as Sir Eddie George of the Bank of England noted in 1999. And the central banks may rise to the occasion and lease out the people's gold on the cheap to get them out of this one as well. And all under the radar, hush hush. Insiders never speak ill of insiders, or do anything to inhibit the kleptocracy.

"Nor can private counterparties restrict supplies of gold, another commodity whose derivatives are often traded over-the-counter, where central banks stand ready to lease gold in increasing quantities should the price rise."

Alan Greenspan, Congressional Testimony, July 24, 1998

The denouement of the New York-London Gold Pool is coming, but it may not be here yet. These things tend to drag on and on, wearing most everyone who suspects them out. Lots of people make claims about 'paper markets'. They paper the landscape with them. And if something happens, they will all claim to be the first. The point is to drill down and attempt to assemble the data against determined effort to distort and obfuscate and hide it.

There are people who make calls, and people who make money. I don't make 'calls.' I try to calculate odds, and then take some guidance from the probabilities. There are no sure things in this life, except that we will all meet the same end, and I believe will be called to account for our actions.

Timely caution is advisable, perhaps on a number of fronts.

"The August turbulence in global [equity] markets has produced significant shifts, including a 6.6% fall in equity prices. The currencies of emerging market countries have depreciated substantially against the G-4, while emerging market borrowing rates for sovereigns and corporates [bonds] have moved higher. Global oil prices have been whipsawed as have G-4 bond yields.

The speed and magnitude of these movements is reminiscent of past episodes in which financial crises emerged or the global economy slipped into recession. However, nothing appears to be breaking. Global activity indicators have, on balance, disappointed but remain consistent with a modest pickup in the pace of growth. Additionally, despite the turbulence in financial markets, there is no sign of unusual stress in short-term funding markets or of a credit crisis in any large Emerging Markets economies."

Bruce Kasman, Chief Economist, JP Morgan

So be of good cheer, nothing appears to be breaking, yet.

"We looked into the abyss if the gold price rose further. A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake. Therefore at any price, at any cost, the central banks had to quell the gold price, manage it."

Sir Eddie George, Bank of England, September 1999

Below is a partial transcript of an interview with Jim Rickards on The Gold Chronicles from July 16, 2015.

You may listen to the entire interview here. This transcript is for the portion that runs from about minute 31 through 42. It is a very interesting interview and if you have the time you might wish to listen to the whole thing.

The reason I wished to share this transcript is the nice, compact description that Jim gives of the LBMA and how they manage their gold bullion contracts.

What provoked this discussion was an earlier question about the reported very large long positions of two banks, JPM and Citi, on the Comex that were noted back in May-June of this year.

Jim's supposition is that they must have had a physical gold short exposure elsewhere, and possibly on the LBMA. As Jim relates it the Banks do not typically take large positions in one direction but tend to work on spreads and make their profits with leverage on those fairly thin trades. And Jim should know since that massive buildup of leverage on thin trades that refused to perform is what blew up LTCM while he was there.

As is clear from this interview, the LBMA is a 'fractional reserve' exchange, with much of the gold being hypothecated some number of times.

IF there is a shortage of physical bullion developing, it will most likely appear in either London or Switzerland. That is because London is the gold hub for the West, and they tend to operate on some multiple of claims to actual free holdings. And Switzerland is where the gold is procured and refined for the formats of the Asian markets

As you know, I have been looking carefully for some time at the odd happenings with physical bullion on the Comex. At least they seem very odd to me if not to some others. You can be the judge.

And as you may recall, there were some pieces in the news about the 'tightness' of gold in London and the dearer prices being paid for gold available for immediate delivery. Again, nothing huge, but another point of data.

And of course there is Goldman in there taking delivery of bullion for their house account reportedly.

And this flurry of schemes coming out of India to do more domestic mining, and monetize the gold held by private individuals and their temples, to stem the demand for bullion imports.

IF the Banks were short of physical bullion in London around July when Jim gave this interview, then by his estimates we would tend to see the strains on the free holdings of physical bullion about-- now.

I do not know what has caused Jim to say that "people are taking their gold out of banks and putting it into new vaults because they’re losing confidence in the banking system. These new vaults are private storage vaults owned by private companies, not by banks." I do not have his level of contacts. But it does seem that there is a slow but steady bleed of bullion out of the Comex warehouses. And 'deliverable' gold is at record low levels.

One would hope that the Banks were wise, and would not pyramid their web of wagers in size and term, hoping that the shortages of physical gold do not become deeper and more stubbornly set. This could turn into a feedback loop of shortage and demand that would have Sir Eddy George back staring into the abyss once again.

But alas, this time the central banks are net buyers, not sellers. And the gold manipulators must contend with the great engines of physical demand in the East. Surely by now the Banks must have learned their lessons about recklessly gambling with other people's money and assets.

What have we learned, at long last, about bailing these fellows out?

What makes this a more potentially serious problem is that the willful battering of the miners may make a resilient source of non-central bank supply more difficult to ramp up A typical gold project takes many years to get into meaningful production.

Perhaps the central banks will use the people's sovereign wealth, this time in the form of gold as well as paper, to bail out their banking buddies from their reckless wagering once again.

When I was in Switzerland for Physical Gold Fund, we actually saw the gold that belongs to the investors in Physical Gold Fund. We had auditors, they had bar numbers and manifests, and we went item by item. Those bars actually belonged to the fund.

That’s not true with these LBMA agreements. You don’t have any allocated gold. That means a bank can have, say, one ton of gold and they can sell 20 tons of gold. They use the one ton to back all 20 of those contracts. In effect, they’re short 19 tons. They own one ton physical and sell 20 tons to a bunch of institutional investors or high-net-worth individuals who want to own gold, so they’re short.

They depend on their customers not asking for the gold. As long as this is all on paper, it works fine. Where it breaks down is if the customer comes in and says, “You know that unallocated gold? I would like to make it allocated and actually have the physical gold. In fact, not only do I want it allocated, but I would like you deliver it from your vault to a private vault run by Brinks or Loomis or one of the big secure logistics providers.”

That is what’s going on. People are taking their gold out of banks and putting it into new vaults because they’re losing confidence in the banking system. These new vaults are private storage vaults owned by private companies, not by banks.

Going back to my original scenario, the bank has one ton of gold and they sell 20. If even five customers show up and say, “I’d like my gold,” one ton each, you’re now short four tons. You have one ton of physical, but you have five tons of requests from five different customers. You’re short four tons, so you have to go out into the market and buy four tons of market. Guess what? That’s a big order. Good luck finding it. You can find it eventually, but you might not be able to find it quickly. So you have price exposure. You’re suddenly short the gold because your customers are demanding it.

What would you do? You’d go out and buy the futures. Now you’re hedged. You’re short to the customer who sent you the notice, you’re long on the futures, but you’re price exposure is hedged. Now you can take 30 or 60 days or however long it takes to source the physical and make delivery to the customer. The customer may think the gold is sitting in the vault and can be delivered tomorrow, but trust me, they can’t. They’ll be lucky to get it in 30 days and could even take a few months.

When I see a massively long futures position, it suggests to me – again, to be clear, I cannot prove this – that banks are turning up short in some other part of the operation, probably on these unallocated gold forwards. Customers are taking their gold out of the bank, the bank has to deliver to those customers, they’re short, they’re getting long futures to hedge, and they’re going to spend the next couple months going out and buying gold.

“The City itself lives on its own myth. Instead of waking up and silently existing, the city people prefer a stubborn and fabricated dream; they do not care to be a part of the night, or to be merely of the world. They have constructed a world outside the world, against the world, a world of mechanical fictions which contemn nature and seek only to use it up, thus preventing it from renewing itself and man.”

Thomas Merton, Raids On The Unspeakable

Here are the current numbers and some recent history on the registered (deliverable) gold bullion inventories held at all of the Comex warehouses in the US. One must view these number within the context of the greater world market for precious metals.

There is much more gold that is privately held in storage in these warehouses that is of an eligible form to be sold if the owner should choose to do so.

Last month JPM was notable for choosing to sell bullion at current prices in large numbers. So I would imagine that as we move into active delivery months that JPM may be worth watching.

It is correct to say that very few contracts for gold bullion in NY actually result in anything more than a speculative trade, some wager. The last I heard only a very small number of contracts, on the order of a few percent, resulted in 'delivery.'

The current total of all registered gold is 182,611 troy ounces, or roughly 5.68 metric tonnes.

There are a total of almost 8 million ounces of eligible gold in all the US Comex Warehouses. I have included that chart at the end. So some will say, 'see, there is more than sufficient gold in the warehouses. This is all nonsense.'

And to that we may respond, yes, but at what price? That gold is presumably private property and not for sale at these prices, except for 182,611 ounces of it.

Anyone who discusses the dynamics of supply and demand in a purportedly 'free market' without even a nodding consideration to the notion of price as a factor is making no sense.

Why show you all this? Some say it means nothing, that I do not understand the markets. Well, perhaps that is true. Then what harm is there in allowing people to see what has happened for themselves.

As you may recall, Goldman was seen taking a large delivery of gold for their house accounts in August. And the amount of gold posted at the Comex 'for sale' at these prices is at historic lows. How can one not wonder at this?

I am certainly not suggesting that there will be hard default at the Comex. How could one expect that in a relatively small market that almost always settles in cash and is dominated by a few, very large insiders who are actively working both sides of the trade? No, if there is a default anywhere, it will precipitate in a physical marketplace where bullion changes hands and form, more likely in London, perhaps even Switzerland. And then it will cascade to all the other markets quickly.

The portion of the gold in London that is not specifically 'spoken for' and held closely is considered to potentially be part of 'the float.'

There have been recent observations by people such as Peter Hambro that it is becoming almost impossible to obtain physical bullion in London at these prices, only endless promises. Even the financial media seems to have realized that there is a tightness in the physical supply of gold.

And yet, with all this the price discovery seems to go on as usual undaunted, divergent from the underlying physical supply issues, except for an increasing leverage of claims to ounces, and backwardation in pricing so that a premium must be paid for actual physical delivery.

This is a very dangerously developing situation, the kind that leads to market dislocations.

There are new calls for the increased 'monetization' of gold, by hypothecating existing bullion to satisfy third party collateral shortfalls. This is a weak form of purchase, a 'rental' that promises to replace what has been further sold, perhaps in multiples, with the product itself being refined into a different format and purity, and then shipped overseas.

And the supply of readily available gold seems to be quietly withdrawing from the markets.

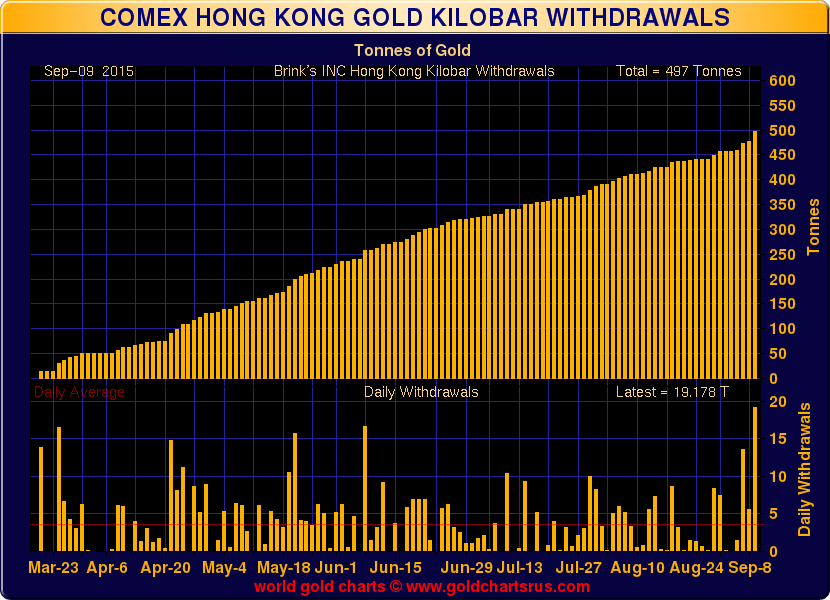

In Hong Kong when you buy gold and take it out of the exchange warehouses it is called a withdrawal.

In other words, you do something with your bullion besides letting it sit around in some exchange warehouse to be passed around and hypothecated 230 times.

The other day at the Hong Kong Comex Metals Exchange 19.17 tonnes of .999 gold kilobars were taken out.

That is about 616,329 troy ounces. Taken out by buyers in a single day. That is a new record for the young exchange.

I hear they have quite a few over-the-counter dealers now, whose mission it is to faciliate the offtake of physical bullion.

Maybe that is why the Comex Hong Kong exchange trading volumes are so low, but the physical offtake levels are so high. They are serious about their business.

Not bad but still not as much as Shanghai does, overall. See the second chart.

It is almost like the New York - London float of unencumbered gold bullion available for delivery is— melting away.

It is an interesting phenomenon that is often overlooked and underappreciated outside of the certain small circles of those who watch these sorts of things.

Gold is flowing from West to East. What it means and will mean is worth considering.

In the bottom portion it is easily seen that the monthly offtake is steadily increasing. And it is also apparent that China is outpacing India in the accumulation of gold.

These charts are from Nick Laird, who chronicles all things gold and silver, at Sharelynx.com.

Bloomberg reports that Sprott may be planning an 'unsolicited bid' for the acquisition of the Central Gold Trust and the Silver Bullion Trust. The planned acquisition would cut the 'trading gap' or NAV discount of the Gold Trust.

The market has already cut the recent discount to NAV roughly in half this morning with a rally in the price of GTU. Markets tend towards the arc of price discovery, if sometimes more slowly, even in a climate of persistent manipulation. And once begun, those adjustments have sometimes then come suddenly, which 'no one could have foreseen,' as we saw in the most recent financial crisis of 2007.

"Sprott Asset Management LP is planning to make an unsolicited offer to acquire Central GoldTrust and Silver Bullion Trust valued at $800 million, a person with knowledge of the matter said.

An offer at that level would reflect a 3.5 percent discount to the combined market value of the trusts at the close Wednesday of about $829 million. The proposal could come as early as Thursday, said the person, who asked not to be identified because the information is private.

The trusts, which buy and hold substantially all of their assets in respective metals in bullion and certificates, have been under pressure from investor Polar Securities Inc., the Toronto-based hedge fund. Polar has been urging the trusts to change how unitholders can redeem their investment as a means of closing their trading gaps.

Sprott aims to use its broader marketing platform and investor relations expertise to close the historic trading gap on both targets between their unit price and their net asset value, said the person familiar with the situation. Sprott projects it will add about $3.14 per unit in value to Central GoldTrust and 95 cents a unit to Silver Bullion by closing that gap, the person said.

J.C. Stefan Spicer, president and chief executive of both Central GoldTrust and Silver Bullion, declined to comment. Glen Williams, a spokesman for Sprott, declined to comment."

In other industry news, Bloomberg also reported that growing Swiss exports indicate that 'gold bars are leaving U.K. vaults for Switzerland, where they’re refined and sent to Asia. India and China.' Or in other words, gold is flowing from west to east.

Sometime recently challenged that notion of gold flowing East, as just a slogan. Look, he said, at the mighty gold inventories on the Comex. Yes, I have looked, and what is truly available at these prices is a rounding error on the physical markets in Asia and the Mideast.

Right now, at these prices, there are a total of 567,928 ounces of registered gold available for delivery in all of the Comex warehouses. That is a little under 18 tonnes. The Central Gold Trust alone, a fairly modest player in the bigger scheme of things, holds 698,496 ounces of gold bullion. It appears that Sprott is bidding to pick up all of it, and at a discount to spot. How is that for mispricing of value?

And yet all of this, all of the Comex and these trusts, this is just about what is being taken out of the Shanghai gold exchange alone each week. And then there is India, Russia, and the Mideast.

The crux of this, of course, is the implied threat of the West, led by the US, to throw their own gold reserves on the table to keep the prices of bullion artificially low and 'under control.' Really? Throw down then, and see what happens next. Because once that is done, there is no going back. And the dislocation that follows may bring down more than a few bullion banks with it.

Someone needs to sit down with these central banking lads and give them a more realistic assessment of what price levels they can ever hope to sustain given the highly distorted dynamics of the markets which they themselves are perpetuating. I am sure their bullion banker buddies will tell them whatever they wish to hear while the fees are flowing.

I suspect that the real gap here is the divergence between the physical markets and the paper markets. And after several long years of persistent market rigging it is yawning. You might do well to mind that gap, because it may close at some point, and that move could be sudden, and noticeable.

Let us pray for those whose hearts are hardened against His grace and loving kindness by greed, fear, and pride, and the seductive illusion and crushing isolation of evil.

We pray that we all may experience the three great gifts of our Lord's suffering and triumph: repentance, forgiveness, and thankfulness. And in so doing, may we obtain abundant life, and with it the peace that surpasses all understanding.

It is available for your use at no cost, but with attribution and a link to the original posting.

I make every attempt to respect the rights of others. If you feel that something here has infringed your work please let me know and I will correct it immediately. It is not always easy to determine the status of material posted to the Internet with regard to fair use and public domain.