"The money was all appropriated for the top in the hopes that it would trickle down to the needy. Mr. Hoover was an engineer. He knew that water trickled down. Put it uphill and let it go and it will reach the driest little spot. But he didn't know that money trickled up. Give it to the people at the bottom and the people at the top will have it before night anyhow. But it will at least have passed through some poor fellow’s hands."

Will Rogers, 5 December 1932

"It is no exaggeration to say that since the 1980s, much of the global financial sector has become criminalised, creating an industry culture that tolerates or even encourages systematic fraud."

Charles H. Ferguson

"Quantitative easing is a gigantic confidence trick. It was promised that it would yield new investment. It has not. It was promised that it would 'pump money into the economy'. It has not. It was also feared that printing money would lead to hyper-inflation. It has not, for the simple reason that no one gets to spend the money. It is a bookkeeping transaction between a central bank and a commercial bank. It means nothing as long as banks are told to build up their reserves (or drive up the speculative value of financial paper assets)."

Simon Jenkins

"We so easily forget. Once the cry of so-called prosperity is heard in the land, we all become so stampeded by the spirit of the god Mammon, that we cannot serve the dictates of social conscience. We are here to serve notice that the economic order is the invention of man; and that it cannot dominate certain eternal principles of justice and of God. The test of our progress is not whether we add more to the abundance of those who have much; it is whether we provide enough for those who have too little."

Franklin Delano Roosevelt

“Evil when we are in its power is not felt as evil, but as a necessity, or even a duty."

Simone Weil

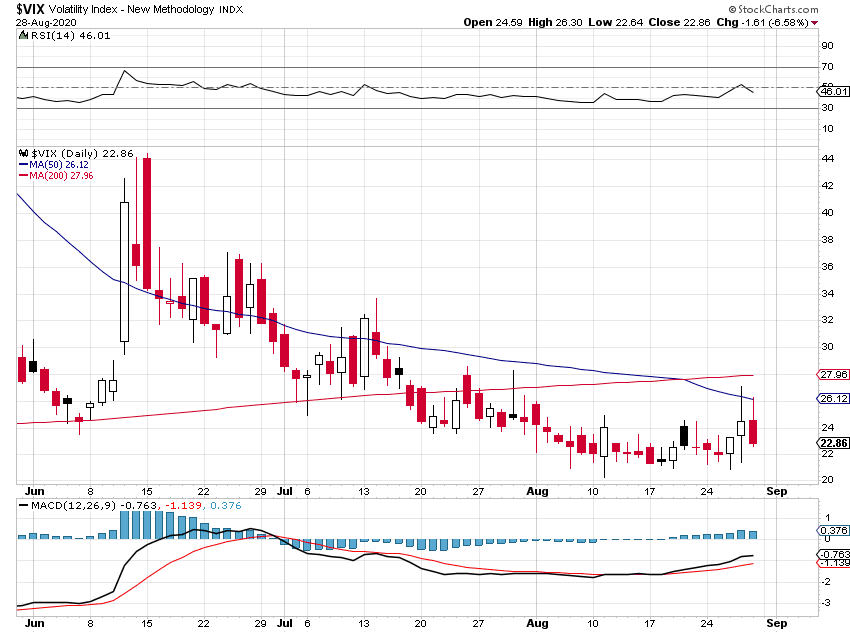

Stocks were pushing higher today, on hopes for Fed dovishness (e.g. moneyprinting) as far as the eye can see. And within a fiscal regime that guides most of the money, if not all of it, to the top one percent.

The Dollar moved loved, skidding down towards the 92 handle.

Gold and silver rallied.

The unsustainable will not be sustained, except through ever-increasing force and fraud.

Need little, want less, love more.

For those who abide in love abide in God, and God in them.

Have a pleasant weekend.