I am finding this contraction in the premiums of the gold-only trusts GTU and PHYS to be extremely interesting. Both followed an expansion of the fund's units and large sales of overallocations to the underwriters, providing liquidity not only to expand the trust but also to game the shares.

This expansion facilitates an arbitrage on the premium in which one sells the trust and buys GLD for example. And the holding of units by the underwriters assures a ready supply of shares for shorting, if one assumes that the big punters even bother with the nicety of borrowing shares.

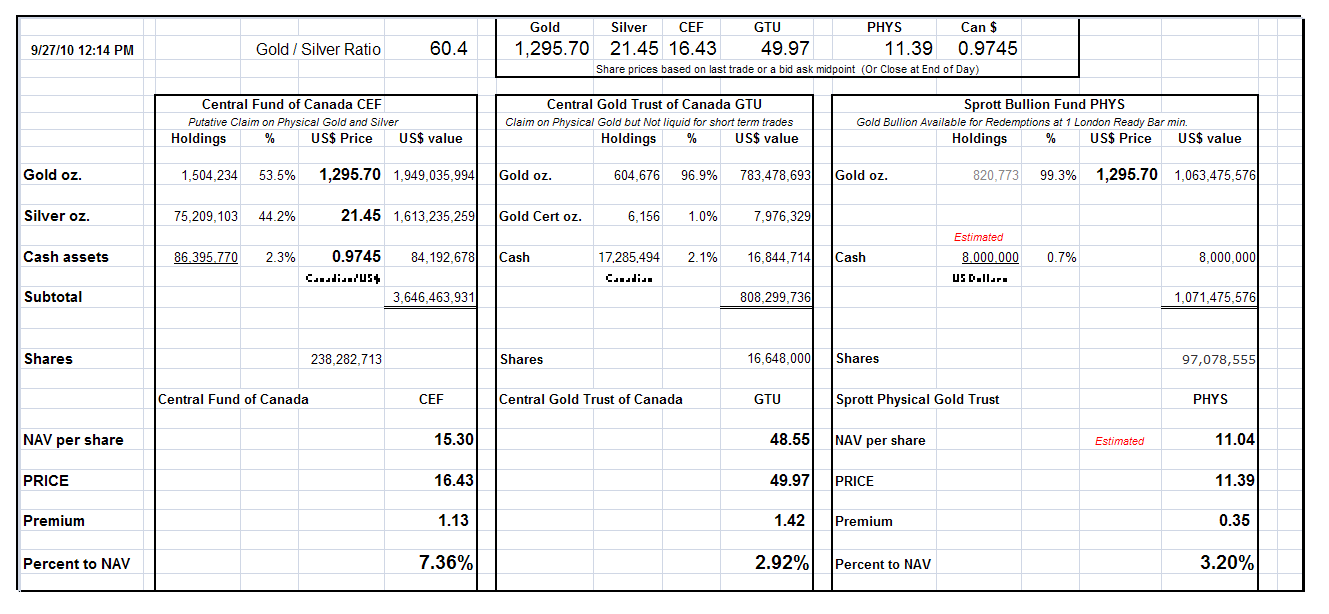

While the premiums remain uniform it does not matter since the NAV will track the bullion holdings, but it does create a sort of retrograde phenomenon in which the funds will briefly underperform bullion due to the contraction of their premium, especially in the case of PHYS, from the lofty 8% to the lowly 2%. It will be interesting to see if this holds, or if the range of premium reasserts on a new leg up in bullion, and the 'kick' of a possible short squeeze.

In the past a contraction of the premiums was often a signal of bearish sentiment, that the speculators were not willing to pay a premium because they felt that the move was nearing a top. One also has to wonder if this is the case once again.

Who can say? As Robbie Burns once observed:

But, Mousie, thou art no thy lane,

In proving foresight may be vain;

The best-laid schemes o' mice an 'men

Gang aft agley,

An' lea'e us nought but grief an' pain,

For promis'd joy!

Still thou art blest, compar'd wi' me

The present only toucheth thee:

But, Och! I backward cast my e'e.

On prospects drear!

An' forward, tho' I canna see,

I guess an' fear!

If you are trading for the shorter term, one needs to be aware of things like premiums and arbitrage. If you are buying and holding as an investor short term fluctuations become much less of an issue as other things increase in importance. You have to understand why you are buying something and what your own objectives are with it, and then be guided by them.

As in the case of the trusts, there are 'premiums' on stocks and options for example, that are not so readily determined because the exact valuations are not so simple and explicit.

This is why trading for the shorter term is a highly specialized craft and is not suitable for any but a few who have the time and knowledge to attempt it. I have been at it for many years, and still learn new things almost every day, all too often the hard way.

You may wish to keep this in mind if and when Mr. Sprott introduces his Physical Silver Trust.

Here is what the NAVs looked like in early September 2010. One 'benefit' of the added liquidity is that the spreads on the Buy - Ask for these trusts has narrowed significantly.