Christopher Cox recently admitted that the SEC has willfully overlooked significant abuses in the equity markets. One thing on which we agreed with John McCain was that his tenure at the SEC is a national disgrace and he should have been dismissed. Given the US stock market bubbles over the past eight years one can hardly disagree.

It is becoming obvious that there is significant price manipulation in the commodity markets, to the point where they have become nothing more than Ponzi schemes in which the object of the investment will never be delivered, and a market roiling default will occur.

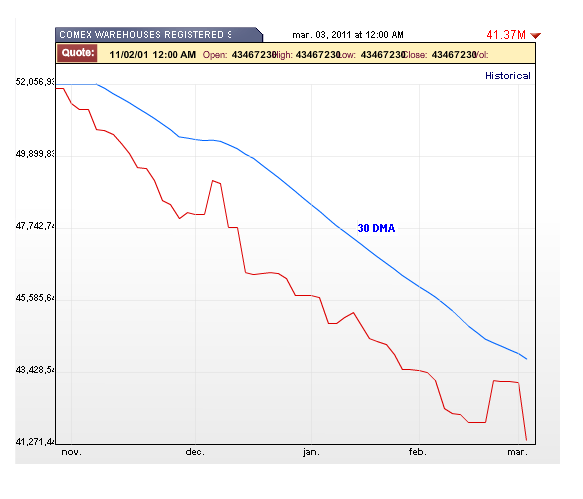

Below is one example in the oil markets. Silver is an even better example. Ted Butler has documented the abuse on numerous occasions, and has been ignored in the same way those exposing the Madoff Ponzi scheme to the SEC were also willfully and repeatedly ignored.

The problem with commodities price manipulation is even worse than the manipulation of stock prices since it involves the capital formation of the means of production with significant lead times. Not only does this manipulation cheat investors and small speculators, but it causes significant, damaging misalignments in supply and demand in the real economy. The example of the electricity markets in California and the Enron fraud was the wake up call that was ignored.

It is beyond simple fraud. This has disproportionate and severely damaging effects on other countries in the global economy.

The perfect solution, the complete market restructuring is complex, and is detailed below. Expect the market manipulators to wallow in the complexity and create loopholes for future exploitation.

However, there is an 80% effective solution that is simple. Transparency of positions is a first step. The second step is to impose strict position limits for those who are not hedging actual and verifiable inventory and production.

The position limits for the 'naked shorting' is appropriate for those who believe that the market price is incorrect. But there comes a time when the naked shorting becomes so large that it IS the market, and the consequences of such outrageous manipulation are real and significant.

Constantly tinkering with regulations and making them more complex is not the answer. The root of the problem has been the lack of enforcement and the bad actions of a handful of banks that have become serial market manipuators since the overturn of Glass-Steagall. There really are no new financial products or frauds. There are just variations on familiar themes.

It is not clear that the solution can come from within the US. Violence never works, and writing our Congress and voting for a reform candidate have now been done, although we should continue this.

A practical solution may be ultimately imposed on the US by the rest of the world, and that is a less attractive prospect than an internal solution.

Reuters

NYMEX oil benchmark again in question

By John Kemp

December 23rd, 2008

The record differential between the front-month and more liquid second-month contracts at expiry last week once again raised pointed questions about whether the NYMEX light sweet contract is serving as a good benchmark for the global oil market, or sending misleading signals about the state of supply and demand.

The expiring January 2009 contract ended down $2.35 on Friday at $33.87, while the more liquid February contract actually rose 69 cents to settle at $42.36 - an unprecedented contango from one month to the next of $8.49.

Criticism of the contract is not new, and past calls for reform have been successfully sidelined. But with policymakers taking a keener interest as a result of wild gyrations in oil prices this year, and a continued focus on regulatory changes to improve market functioning in future, there is at least a chance changes will be adopted as part of a wider package of futures market adjustments.

AN UNREPRESENTATIVE PRICE

During the surge to $147 per barrel earlier this year, OPEC repeatedly criticized the NYMEX reference price for overstating the real degree of tightness in the physical market and causing prices to overshoot on the upside. (That was the point, see Enron for details - Jesse)

While rallying NYMEX prices seemed to point to an acute physical shortage and need for more oil, Saudi Arabia could not find buyers for the 200,000 barrels per day (bpd) of extra oil promised to U.N. Secretary-General Ban Ki-moon or the 300,000 bpd promised to U.S. President George Bush in June.

Bizarrely, rather than acknowledge there was something wrong with the reference price, some market participants suggested Saudi Arabia should increase the already large discounts for its physical crude to achieve sales in a market that clearly did not need the oil, and was not paying enough contango to make storing it economic (contango is where the futures price is above the spot market). (There is nothing bizarre about it. That is standard disinformation by the frauds and their mouthpieces - Jesse)

The NYMEX WTI price may have achieved unprecedented media fame as a result of the “super-spike”, but a futures price to which producers and consumers were paying ever larger discounts for actual barrels was clearly not a good indication of where the market as a whole was trading. (It was a fraud. Lots of people lost lots of money in it. It was a great excuse to build a Ponzi scheme in a market price, raise the price of gasoline to $4 gallon, and then take the market down. This is the 1929 model of market manipulation pure and simple - Jesse)

Now the market risks overshooting in the other direction. Intense pressure on the front month in recent weeks has more to do with the contract’s peculiarities (in particular storage restrictions at the delivery point) than a further deterioration in oil demand or a market vote of no-confidence in the 2.2 million barrels per day further cut in oil production announced by OPEC at the end of last week. (The beauty about price manipulation is that it works in both directions. Different damage, but the same jokers get to pocket their fraudulent gains - Jesse)

The collapse in NYMEX prices nearby risks exaggerating the real degree of oversupply and demand destruction, sending the wrong signal to producers and consumers about the wider availability of crude in the petroleum economy. (It may take a few countries along with it. But that may be by intent. Chavez and Putin are not on the Friends of W list - Jesse)

DOMESTIC PRICE, GLOBAL BENCHMARK

The NYMEX contract is for a very special type of crude oil (light sweet) delivered at a very special location (Cushing, Oklahoma) in the interior of the United States. It is not representative of the majority of crude oil traded internationally (most of which is heavier and sourer) and delivered by ocean-going tankers.

These specifications made sense when the contract was introduced as a benchmark for the U.S. domestic market.

U.S. refiners have a strong preference for light oils, for which they were prepared to pay a premium, because of their much higher yield to gasoline. The inland delivery location, centrally located and near the main Texas oilfields, rather than one on the coast, made sense for a contract that tried to capture the “typical” base price for crude oil paid by refiners across the continental United States.

But these specifications make much less sense now the NYMEX price is increasingly used a benchmark for the global petroleum economy, in which light sweet crudes are only a small fraction of total output. Just as NYMEX prices sent the wrong signals about physical oil availability on the way up, distorting the market and triggering more demand destruction than was really necessary, they now risk sending the wrong ones on the way down.

Earlier this year, the problem was a relative shortage of light sweet crude oils at Cushing, while all the extra barrels being offered to the market by Saudi Arabia were heavier, sourer crudes that could not be delivered against the contract. Moreover, extra Saudi crudes would have arrived by ship, and the pipeline and storage configurations around Cushing would have made it difficult to deliver them quickly against the contract.

Financial speculators were able to push NYMEX higher safe in the knowledge Saudi Arabia could not take the other side and overwhelm them by delivering physical barrels to bring prices down. The resulting spike exhibited all the characteristics of a technical squeeze: tight contract specifications ensured there could be shortage of NYMEX light sweet inland oils even while the global market was oversupplied by heavier, sourer seaborne ones.

Now the opposite problem is occurring. Crude stocks at Cushing have doubled from 14.3 million barrels to 27.5 million since mid-October. Stocks around the delivery point are at a near-record levels and approaching the maximum capacity of local tank and pipeline facilities (https://customers.reuters.com/d/graphics/CUSHING.pdf).

As a result, the market has been forced into a huge contango as storage becomes increasingly expensive and difficult to obtain, ensuring the expiring futures trade at a substantial discount.

But Cushing inventories are not typical of the rest of the U.S. Midwest (https://customers.reuters.com/d/graphics/PADD2_EX_CUSHING.pdf) or along the U.S. Gulf Coast (https://customers.reuters.com/d/graphics/PADD3.pdf), where stock levels are high relative to demand but nowhere near as overfull as in Oklahoma.

Once again the problem is geography. Coastal refiners have responded to the downturn by cutting imports of seaborne crude, limiting the stock build. But the inland market is the destination for some Canadian crudes that have nowhere else to go, and the pipeline configuration means they cannot be trans-shipped to other locations readily.

Light sweet crude has been piling up in the region, with refiners choosing to deliver the unwanted excess to the market by delivering it into Cushing.

NEW GRADES, NEW DELIVERY POINTS

The easiest way to make NYMEX more representative would be to widen the number of crude grades that can be delivered, and open a new delivery point along the U.S. Gulf Coast. Both reforms would link the contract more tightly into the global petroleum economy. (The easiest way would be to do exactly as I suggested above. It can be done with the stroke of a pen and the kick of a few asses - Jesse)

NYMEX already permits some flexibility in delivery grades. Sellers can deliver UK Brent and Norwegian Oseberg at small fixed discounts to the settlement price, and Nigerian Bonny Light and Qua Iboe, as well as Colombia’s Cusiana at small premiums.

In principle, there is no reason the contract cannot be modified further to allow a wider range of foreign oils to be delivered at larger discounts to the settlement price.

More importantly, NYMEX could open a second delivery location along the Gulf Coast, increasing the amount of storage capacity available, and linking it more closely into the tanker market.

If prices spiked again, a coastal delivery location would make it much easier for Saudi Arabia to short the market and deliver its own barrels into the rally. By widening the physical basis, it would also make it easier to support the market by cutting international production and avert a glut trapped around the delivery location.

So far, the market has continued to resist change. But there are signs policymakers might enforce one. (No one likes to give up a successful fraud voluntarily until the clock runs out - Jesse)

Earlier in the year, Saudi Arabia strongly hinted western governments should look at reforming their own futures markets rather than call for production of even more barrels of oil that could not be sold at the prevailing (unrealistic) price. (Saudi Arabia is the US's creature so any criticism is coming from a loyal source and credible - Jesse)

Naturally, some of the reform impetus has ebbed along with prices and demand. But policymakers continue to show interest in structural reforms, as was evident at last week’s London Energy Meeting, and there is an increased willingness to challenge unfettered market dynamics.

It is still possible the incoming Obama administration might force contract changes as part of a wider package of reforms designed to improve the functioning of commodity markets, reduce volatility and send clearer, more consistent price signals to the industry and consumers.