As a reminder, this is a stock market option expirations week.

VIX shows complacency.

"You have accepted things you would not have accepted five years ago, a year ago, things that your father, even in Germany, could not have imagined. Suddenly it all comes to be, all at once. You see what you are, what you have done, or more accurately what you haven’t done. For that was all that was required of most of us: that we do nothing. You remember everything now, and your heart breaks. Too late. You are compromised beyond repair."

Milton Mayer, They Thought They Were Free

"The greatest triumph of the banking industry wasn’t ATMs or even depositing a check via the camera of your mobile phone. It was convincing Treasury and Justice Department officials that prosecuting bankers for their crimes would destabilize the global economy.”

Barry Ritholtz

"The man who knows the truth and has the opportunity to tell it, but who nonetheless refuses to, is among the most shameful of all creatures."

Theodore Roosevelt

Expecting the Unexpected: An Interview With Edmund Phelps

By Caroline Baum

Feb 11, 2013

In 2006, the Royal Swedish Academy of Sciences awarded the Nobel Memorial Prize in Economic Sciences to Edmund Phelps "for his analysis of intertemporal tradeoffs in macroeconomic policy." Phelps showed that, contrary to the original Phillips curve, there is no long-run trade-off between inflation and unemployment, only a short-term one. Translated into lay speech: You can fool some of the people some of the time and reduce unemployment by paying workers what looks like a higher wage. Eventually, they wise up to the fact that their higher nominal wage is a function of higher inflation, not a higher real wage. Unemployment reverts to its so-called natural rate.

Phelps is the director of Columbia University's Center on Capitalism and Society. I talked with him over the phone on Jan. 25 and Feb. 4 about his views on rational expectations: the notion that people’s expectations of economic outcomes are generally right and policy makers can’t outsmart the public....

Q: So how did adaptive expectations morph into rational expectations?

A: The "scientists" from Chicago and MIT came along to say, we have a well-established theory of how prices and wages work. Before, we used a rule of thumb to explain or predict expectations: Such a rule is picked out of the air. They said, let's be scientific. In their mind, the scientific way is to suppose price and wage setters form their expectations with every bit as much understanding of markets as the expert economist seeking to model, or predict, their behavior. The rational expectations approach is to suppose that the people in the market form their expectations in the very same way that the economist studying their behavior forms her expectations: on the basis of her theoretical model.

Q: And what's the consequence of this putsch?

A: Craziness for one thing. You’re not supposed to ask what to do if one economist has one model of the market and another economist a different model. The people in the market cannot follow both economists at the same time. One, if not both, of the economists must be wrong. Another thing: It’s an important feature of capitalist economies that they permit speculation by people who have idiosyncratic views and an important feature of a modern capitalist economy that innovators conceive their new products and methods with little knowledge of whether the new things will be adopted -- thus innovations. Speculators and innovators have to roll their own expectations. They can’t ring up the local professor to learn how. The professors should be ringing up the speculators and aspiring innovators. In short, expectations are causal variables in the sense that they are the drivers. They are not effects to be explained in terms of some trumped-up causes.

Q: So rather than live with variability, write a formula in stone!

A: What led to rational expectations was a fear of the uncertainty and, worse, the lack of understanding of how modern economies work. The rational expectationists wanted to bottle all that up and replace it with deterministic models of prices, wages, even share prices, so that the math looked like the math in rocket science. The rocket’s course can be modeled while a living modern economy’s course cannot be modeled to such an extreme. It yields up a formula for expectations that looks scientific because it has all our incomplete and not altogether correct understanding of how economies work inside of it, but it cannot have the incorrect and incomplete understanding of economies that the speculators and would-be innovators have...

Q: One of the issues I have with rational expectations is the assumption that we have perfect information, that there is no cost in acquiring that information. Yet the economics profession, including Federal Reserve policy makers, appears to have been hijacked by Robert Lucas.

A: You’re right that people are grossly uninformed, which is a far cry from what the rational expectations models suppose. Why are they misinformed? I think they don’t pay much attention to the vast information out there because they wouldn’t know what to do what to do with it if they had it. The fundamental fallacy on which rational expectations models are based is that everyone knows how to process the information they receive according to the one and only right theory of the world. The problem is that we don't have a "right" model that could be certified as such by the National Academy of Sciences. And as long as we operate in a modern economy, there can never be such a model...

Q: In the world envisioned by rational expectations, there would be no hyperinflation, no panics, no asset bubbles? Is that right?

A: When I was getting into economics in the 1950s, we understood there could be times when a craze would drive stock prices very high. Or the reverse: An economy in the grip of weak business confidence, weak investment, would lead to loss of jobs in the capital-goods sector. But now that way of thinking is regarded by the rational expectations advocates as unscientific.

By the early 2000s, Chicago and MIT were saying we've licked inflation and put an end to unhealthy fluctuations –- only the healthy “vibrations” in rational expectations models remained. Prices are scientifically determined, they said. Expectations are right and therefore can't cause any mischief.

At a celebration in Boston for Paul Samuelson in 2004 or so, I had to listen to Ben Bernanke and Oliver Blanchard, now chief economist at the IMF, crowing that they had conquered the business cycle of old by introducing predictability in monetary policy making, which made it possible for the public to stop generating baseless swings in their expectations and adopt rational expectations. My work on how wage expectations could depress employment and how asset price expectations could cause an asset boom and bust had been disqualified and had to be cleansed for use in the rational expectations models.

Read the entire interview here.

"According to one story, Diogenes went to the Oracle at Delphi to ask for its advice and was told that he should 'deface the currency.' Following the debacle in Sinope, Diogenes decided that the oracle meant that he should deface the political currency rather than actual coins.He was said to have lived simply, 'like a dog,' and that this is how the Cynic school of philosophy received its name.

He traveled to Athens and made it his life's goal to challenge established customs and values. He argued that instead of being troubled about the true nature of evil, people merely rely on customary interpretations."

The name Cynic derives from ancient Greek κυνικός (kynikos), meaning "dog-like", and κύων (kyôn), meaning "dog."In his later life Diogenes was visited in Corinth by Alexander the Great, the king of Macedonia, who would go on to conquer Egypt and India.

Ex-Amaranth Trader, CFTC Unite to Ask Court to Toss Fine

By Tom Schoenberg & Brian Wingfield

Feb 7, 2013

A former natural-gas trader at Amaranth Advisors LLC, backed by the U.S. Commodity Futures Trading Commission, asked a federal appeals court to overturn a $30 million fine imposed by another regulator over alleged manipulation of the gas-futures market.

In a case that could determine the limits of the Federal Energy Regulatory Commission’s power to punish market manipulation, a lawyer for Brian Hunter told a three-judge panel in Washington today that the CFTC has sole jurisdiction over futures trading on the New York Mercantile Exchange. The CFTC, which filed papers supporting Hunter, also argued today.

“There was no notice, much less fair notice, to Brian Hunter that his conduct was being regulated by FERC,” Hunter’s lawyer, Michael Kim of Kobre & Kim LLP, said during the 40- minute argument.

The dispute highlights FERC’s growing role as a regulatory enforcer. Congress beefed up the agency’s powers in 2005 to ensure order in the energy trading markets after Enron Corp. traders triggered California blackouts earlier in the decade. Since January 2011, the commission has publicly disclosed 13 investigations it has conducted of alleged market manipulation....

Read the rest here.

"If you follow issues like Too-Big-To-Fail or Wall Street corruption long enough, you realize that the reason things don't get done about them by our government has very little to do with ideology or even politics, in the way most of us understand politics.

Instead, it's a bizarre, almost tribal mentality that rules our capital city – a kind of groupthink that makes extreme myopia and a willingness to ignore the tribe's ostensible connection to the people who elected them a condition for social advancement within."

Matt Taibbi, Neil Barofsky's Adventure in Groupthink

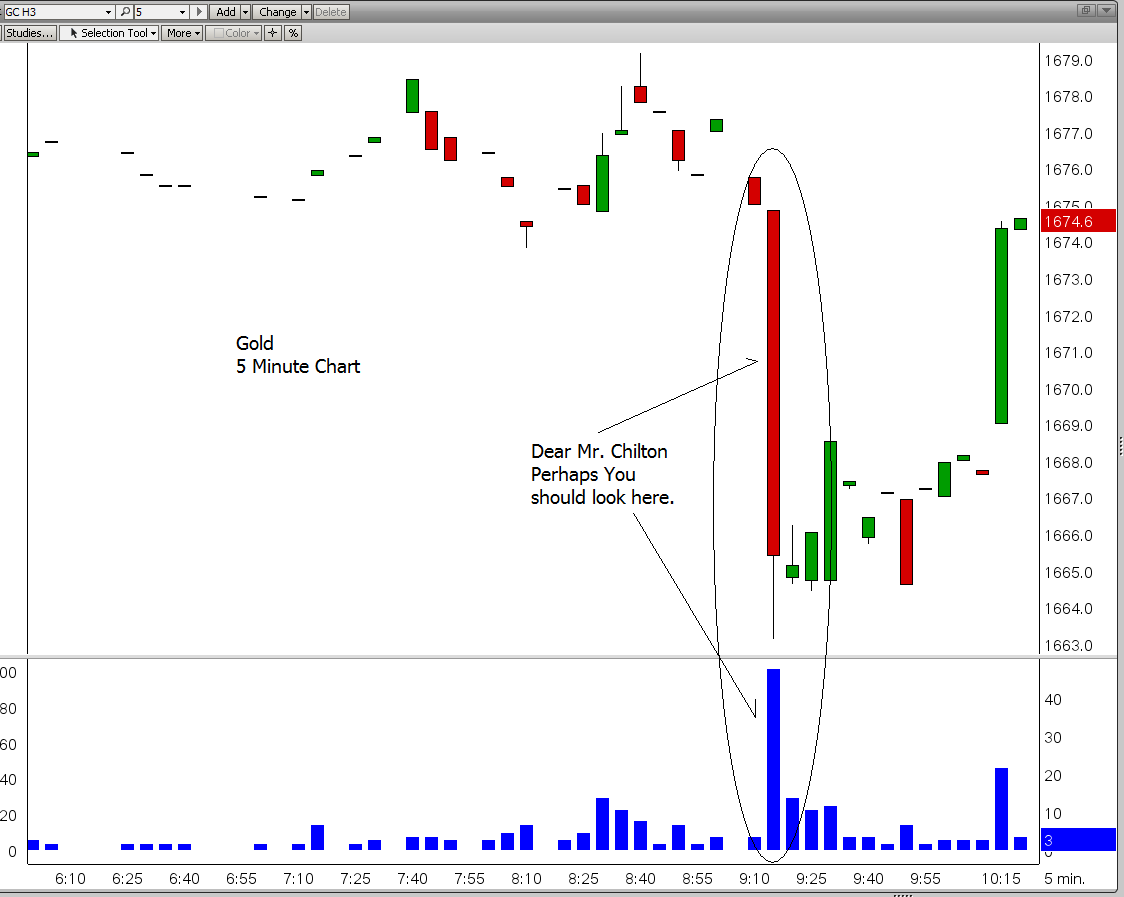

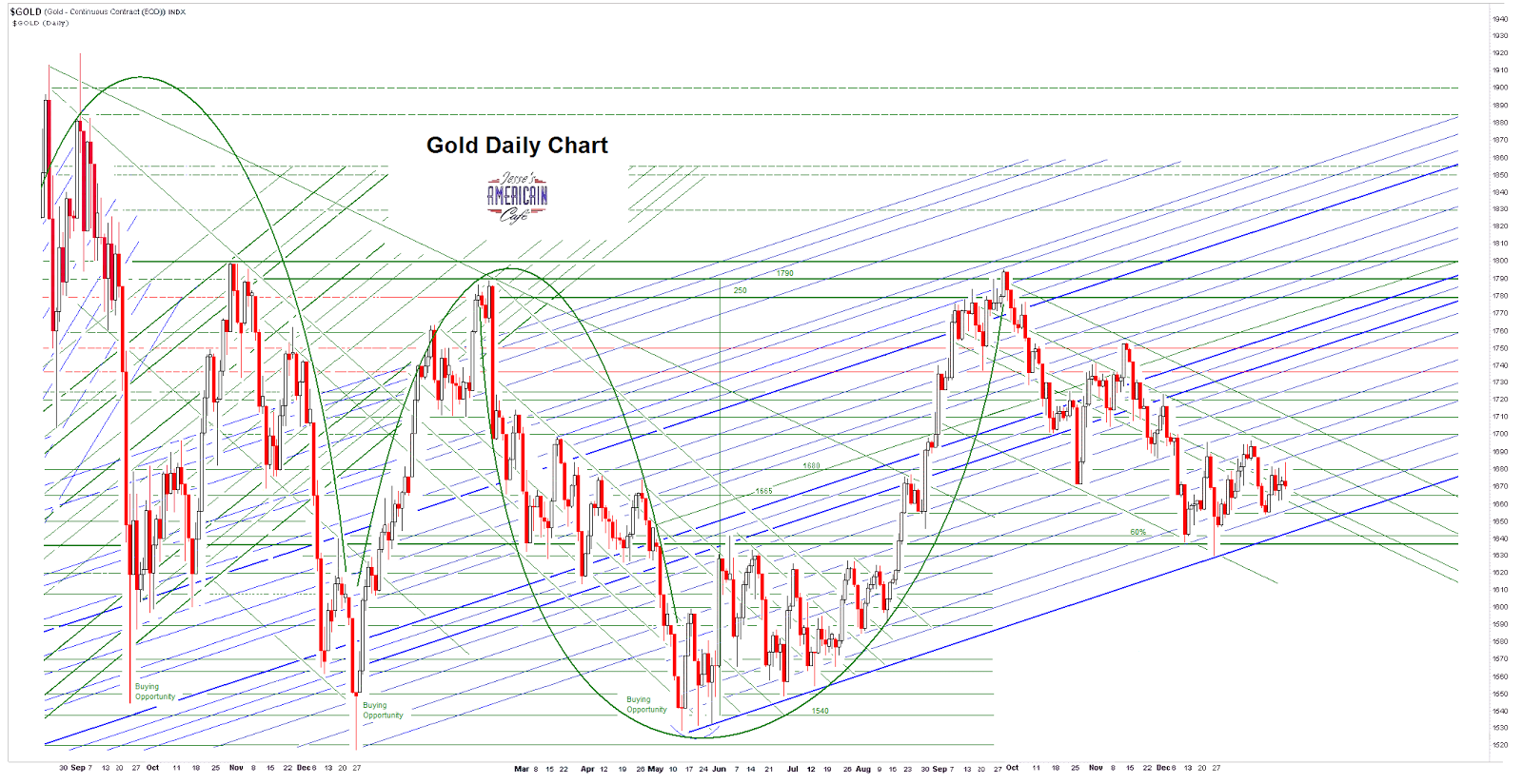

|

| Wednesday 6 February |

|

| Monday 4 February |

"High frequency trading software that focuses on feedback loops is a useful diversion to hide front-running, short squeezing, and other parasitic activities. The current BS about rotation out of bonds is merely an attempt to attract retail because they’ve run out of shorts to squeeze to take the markets higher.

If you can put aside your moral outrage, this strategy is a thing of beauty – disgusting, evil, and fraudulent but beautiful in its execution."

|

| Why Bears Should Tread Carefully |

"The enemy of the conventional wisdom is not ideas but the march of events."

John Kenneth Galbraith

"Present market conditions now match 6 other instances in history: August 1929 (followed by the 85% market decline of the Great Depression), November 1972 (followed by a market plunge in excess of 50%), August 1987 (followed by a market crash in excess of 30%), March 2000 (followed by a market plunge in excess of 50%), May 2007 (followed by a market plunge in excess of 50%), and January 2011 (followed by a market decline limited to just under 20% as a result of central bank intervention). These conditions represent a syndrome of overvalued, overbought, overbullish, rising yield conditions that has emerged near the most significant market peaks – and preceded the most severe market declines – in history:

- S&P 500 Index overvalued, with the Shiller P/E (S&P 500 divided by the 10-year average of inflation-adjusted earnings) greater than 18. The present multiple is actually 22.6.

- S&P 500 Index overbought, with the index more than 7% above its 52-week smoothing, at least 50% above its 4-year low, and within 3% of its upper Bollinger bands (2 standard deviations above the 20-period moving average) at daily, weekly, and monthly resolutions. Presently, the S&P 500 is either at or slightly through each of those bands.

- Investor sentiment overbullish (Investors Intelligence), with the 2-week average of advisory bulls greater than 52% and bearishness below 28%. The most recent weekly figures were 54.3% vs. 22.3%. The sentiment figures we use for 1929 are imputed using the extent and volatility of prior market movements, which explains a significant amount of variation in investor sentiment over time.

- Yields rising, with the 10-year Treasury yield higher than 6 months earlier.

The blue bars in the chart below identify historical points since 1970 corresponding to these conditions.

"Corruption is a tree, whose branches are

of an immeasurable length: they spread

Everywhere; and the dew that drops from thence

Hath infected some chairs and stools of authority."

Beaumont and Fletcher, The Honest Man's Fortune

"Stop and think once more about what has just happened on Wall Street: its most admired firm conspired to flood the financial system with worthless securities, then set itself up to profit from betting against those very same securities, and in the bargain helped to precipitate a world historic financial crisis that cost millions of people their jobs and convulsed our political system.

In other places, or at other times, the firm would be put out of business, and its leaders shamed and jailed and strung from lampposts. (I am not advocating the latter.) Instead Goldman Sachs, like the other too-big-to-fail firms, has been handed tens of billions in government subsidies, on the theory that we cannot live without them. They were then permitted to pay politicians to prevent laws being passed to change their business, and bribe public officials (with the implicit promise of future employment) to neuter the laws that were passed—so that they might continue to behave in more or less the same way that brought ruin on us all.

And after all this has been done, a Goldman Sachs employee steps forward to say that the people at the top of his former firm need to see the error of their ways, and become more decent, socially responsible human beings. Right. How exactly is that going to happen?

If Goldman Sachs is going to change, it will be only if change is imposed upon it from the outside—either by the market's decision that it is no longer viable in its current form or by the government's decision that we can no longer afford it. There is a bizarre but lingering aroma in the air that the government is now seeking to prevent the free market from working its magic in the financial sector-another reason that the Dodd-Frank legislation is still being watered down, and argued over, and failing to meet its self-imposed deadlines for implementation.

But the financial sector is already so gummed up by government subsidies that market forces no longer operate within it. Could Goldman Sachs fail, even if it tried? If someone invented a cheaper way to finance productive enterprise, would they stand a chance against the big guys?

Along with the other too-big-to-fail firms, Goldman needs to be busted up into smaller pieces. The ultimate goal should be to create institutions so dull and easy to understand that, when a young man who works for one of them walks into a publisher's office and offers to write up his experiences, the publisher looks at him blankly and asks, 'Why would anyone want to read that?'"

Michael Lewis, The Trouble With Wall Street