"Every society gets the kind of criminal it deserves. What is equally true is that every community gets the kind of law enforcement it insists on." Robert Kennedy

The CFTC hearing in Washington was about safeguards against, and limits on, naked short selling at the COMEX. The LBMA in London is a 'cash market' and while short selling is accepted, large leverage and blatant naked short selling is not. The crux of the scandal is that the Banks and hedge funds have been selling what they do not have in order to manipulate the price and cheat investors, in this market as they have been shown repeatedly to have done in other markets.

The story gets sticky in the States because, as disclosed in the motions in a New Orleans trial, the players filed a motion claiming immunity because they were acting in partnership with the Treasury and the Federal Reserve, and other central banks who were not within the Court's jurisdiction.

Watch this story unfold, and then make up your own minds. But be prepared for smears, diversions, misconceptions, and false denials. The accused parties will consistently try to ignore this, and change the subject. The attempts to pressure the media to ignore tihs altogether are a 'tell' if there ever was one.

I am shocked at the extent to which the Banks influence and control the American media. This was testimony at a public hearing, and it has been largely squashed. Judging by history, this is going to get ugly.

Thanks to the NY Post for breaking ranks with the mainstream media. Despite some significant behind the scenes pressure, the Post is actually publishing some words that the Banks do not wish the American people to hear. And many Americans to not wish to hear it, because it shakes their faith in the system, and threatens them with the unknown. And too many, including economists and even bloggers, are only too willing to 'go along to get along' and be invited to the posh gatherings of the famous, and receive some sinecure from the monied interests.

I do not know if this is true or not, or what the truth may be. But I do have a strong passion for bringing the light of day to shine on this, and for these markets to be much more transparent, as a reform, to prevent frauds which we do know have occurred and most likely are still occurring. For me the light of day is not smearing the messenger and making their life dangerously miserable, but that is what too often passes for journalism in the US today, as is seen in the case of other whistleblowers, most famously in the Plame affair.

Naked short selling in size is a cancer in the financial markets. And the way in which the Banks are obstinately fighting against any and all reforms that attempt to limit naked short selling shows the objective observer that they are firmly committed to a status quo that is designed to distort the markets and the real economy for their short term advantage.

Let's be clear about this: naked short selling in size is not a trading strategy, it is a means to a fraud.

This may be the Madoff ponzi scheme writ large, the heart of the darkness in the financial fraud that is the US financial system. The crowning achievement of the financial engineers at the Fed, who have built a Ponzi economy and an empire of fraud.

NY Post

Metal$ are in the pits

By MICHAEL GRAY

4:33 AM, April 11, 2010

Trader blows whistle on gold & silver price manipulation

There is no silver lining to the activities of JPMorgan Chase and HSBC in the precious-metals market here and in London, says a 40-year veteran of the metal pits.

The banks, which do the Federal Reserve's bidding in the metals markets, have long been the government's lead actors in keeping down the prices of gold and silver, according to a former Goldman Sachs trader working at the London Bullion Market Association.

Maguire was scheduled to testify last week before the Commodities Futures Trade Commission, which is looking into the activities of large banks in the metals market, but was knocked off the list at the last moment. So, he went public.

Maguire -- in an exclusive interview with The Post -- explained JPMorgan's role in the metals pits in both London and here, and how they can generate a profit either way the market moves.

"JPMorgan acts as an agent for the Federal Reserve; they act to halt the rise of gold and silver against the US dollar. JPMorgan is insulated from potential losses [on their short positions] by the Fed and/or the US taxpayer," Maguire said.

In the gold pits, Maguire sees HSBC betting against the precious metal's price without having any skin in the game in the form of a naked short.

"HSBC conducts an ongoing manipulative concentrated naked short position in gold. Silver is much easier to manipulate due to its much smaller [market] size," Maguire added.

"No one at JPMorgan is familiar with Andrew Maguire," said Brian Marchiony, a company spokesman. HSBC declined to comment. (Maguire seems to be creeping into the corporate consciousness. Earlier, JPM tried to deny that he even existed. Now they admit he exists but no one there knows him, despite his have traded alongside them for 40 years, and traded at a sister firm, Goldman. HSBC has at least enough conscience to simply sulk. - Jesse)

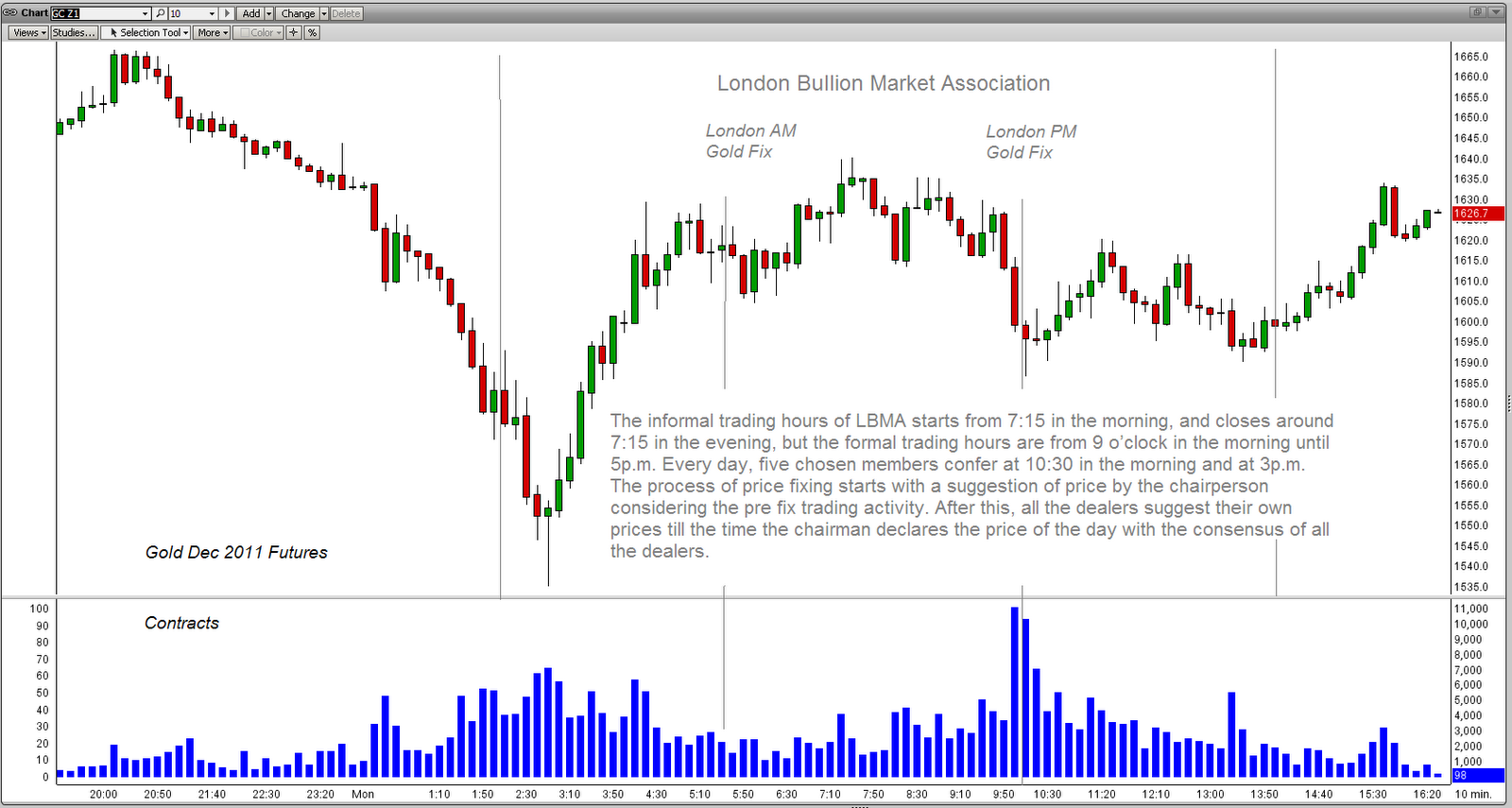

Also during the CFTC hearing, Jeff Christian, founder of the commodities firm CPM Group, said that the LBMA, the physical delivery market for gold and silver in the UK, has been using leverage, which is another way to depress the price of gold and silver.

Christian said that the LBMA -- the same market Maguire trades in -- has leverage of about 100-1 on the gold bars settled on the exchange. In layman's terms, that means if 100 clients requested their bullion bars be delivered, the exchange could only give one client the precious metal. (Note: the LBMA is not a 'futures' market like the COMEX where naked short selling is an accepted, if not entirely explicit, practice. The CFTC hearing was essentially about safeguards against and limits on naked short selling on the COMEX, despite the noise and distractions surrounding it. - Jesse)

The remaining requests would have to be settled for cash equivalent. "That is tantamount to a default on the trade," says Bill Murphy, chairman of the Gold Antitrust Action committee...

Read the rest here.